High margins, rising profits, significant director ownership and a modest valuation are among the attractive credentials of Foresight Group. Maynard Paton studies the fund manager’s positive progress based on investing in a ‘decarbonised future’.

I am not a great fan of the fund-management industry.

I cannot think of another sector where the employees typically collect enormous salaries while the customers can pay hefty charges yet sometimes get very little in return.

Quite often us amateur investors are much better off with simple index trackers rather than falling for the industry’s persuasive advisers and glossy brochures.

Yet here I am about to study Foresight Group — a fund manager that seems to be defying the wider sector trends of client-money outflows and squeezed management fees.

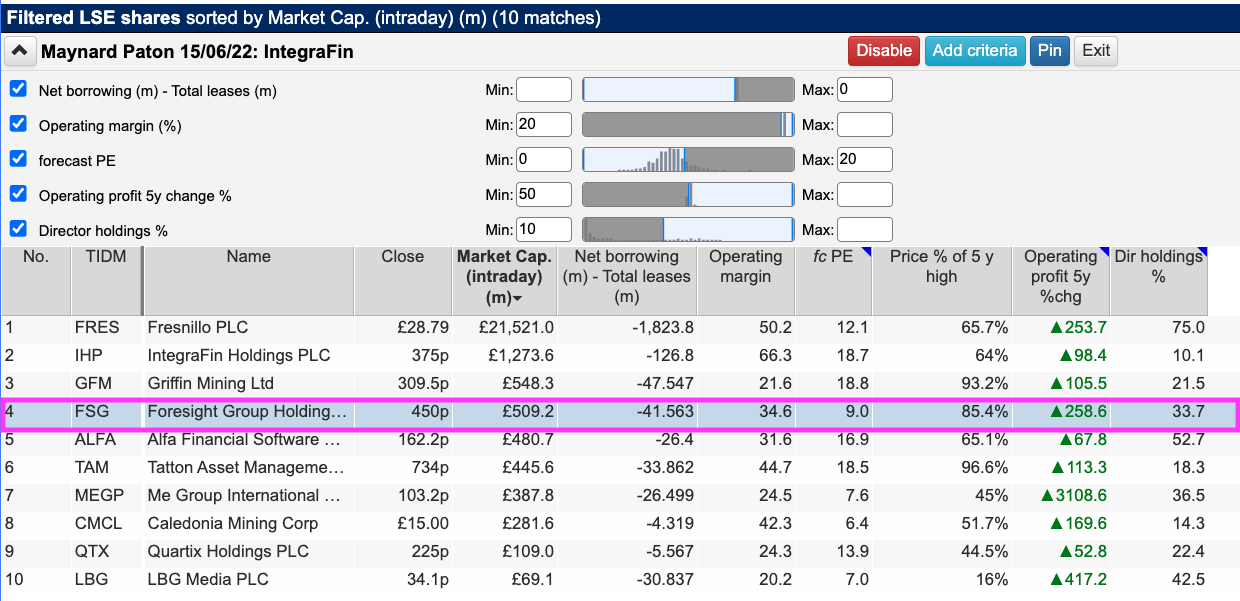

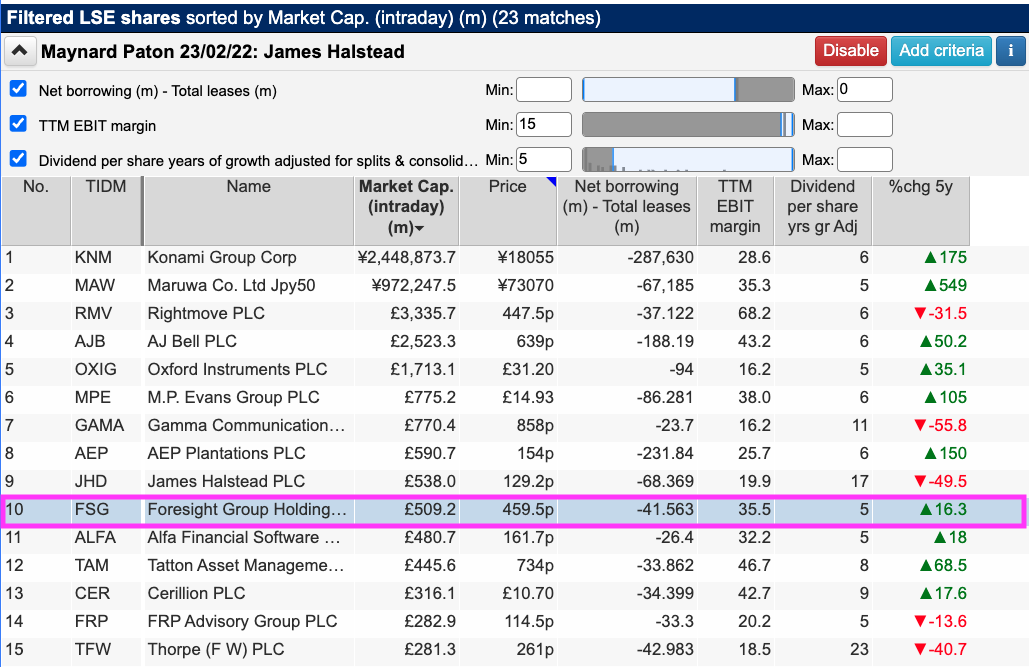

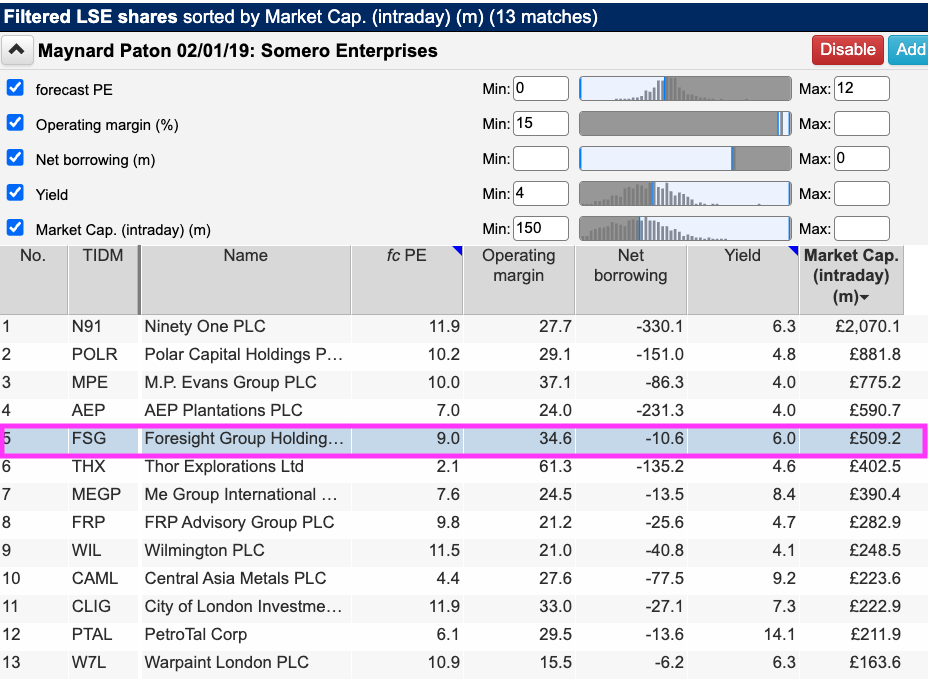

Foresight has recently appeared on the ShareScope screens I employed to identify Integrafin, James Halstead and Somero Enterprises:

(You can run these screens for yourself by selecting the “Maynard Paton 15/06/22: Integrafin” , “Maynard Paton 23/02/22: James Halstead” and “Maynard Paton 02/01/19: Somero” filters within ShareScope’s fabulous Filter Library. My instructions show you how.)

(You can run these screens for yourself by selecting the “Maynard Paton 15/06/22: Integrafin” , “Maynard Paton 23/02/22: James Halstead” and “Maynard Paton 02/01/19: Somero” filters within ShareScope’s fabulous Filter Library. My instructions show you how.)

Foresight’s high margin, net cash position, rising profits, modest valuation and significant director shareholdings may be enough to put my industry prejudices aside.

Let’s take a closer look.

Introducing Foresight Group

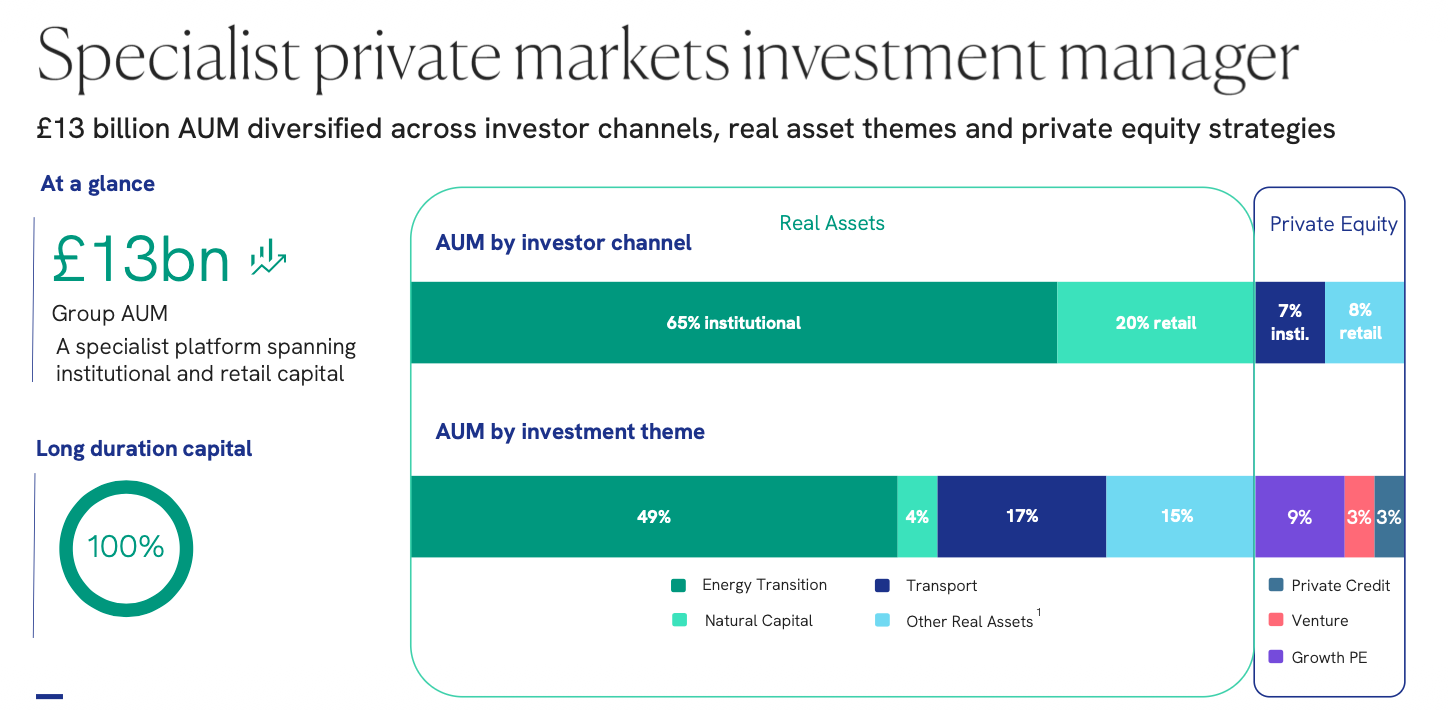

Foresight was established during 1984 and presently manages funds worth £13 billion on behalf of more than 200 institutional customers and approximately 40,000 retail investors:

Founder Bernard Fairman recounted during this Fund Shack podcast how difficulties raising money for venture-capital strategies prompted Foresight to instead seek investors to back “clean tech” and solar power in particular:

“We pursued a losing strategy that no one wanted, namely venture capital. We carried on with venture capital for far too long and didn’t see the world was changing. After 2000, we got the boom and the bust in tech and I started looking at how we could move from an area where we couldn’t raise any money to an area where we could.

And so after a few years, we ended up with what I call renewable-energy infrastructure. I think I was one of the first, if not the first in the UK, to use that phrase. And indeed to build an asset class.

It was a time people were talking about clean tech. I needed a bridge from tech to something that people wanted to invest in. Clean tech provided the bridge.

But it wasn’t the latest fuel-cell technology, it was a solar farm. We were the first in the UK to start investing in solar in 2007-8. We got into that area, not because of some kind of quasi-religious conviction, but because we could see that solar in particular would be the cheapest form of energy generation… And so it is proving.”

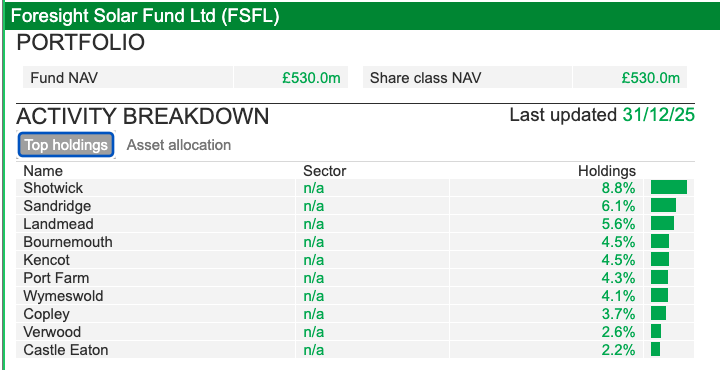

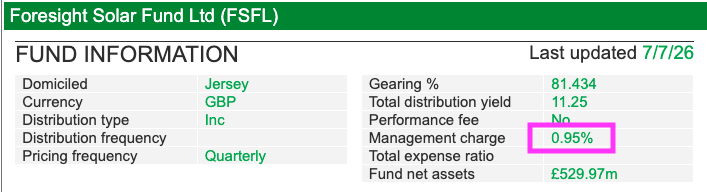

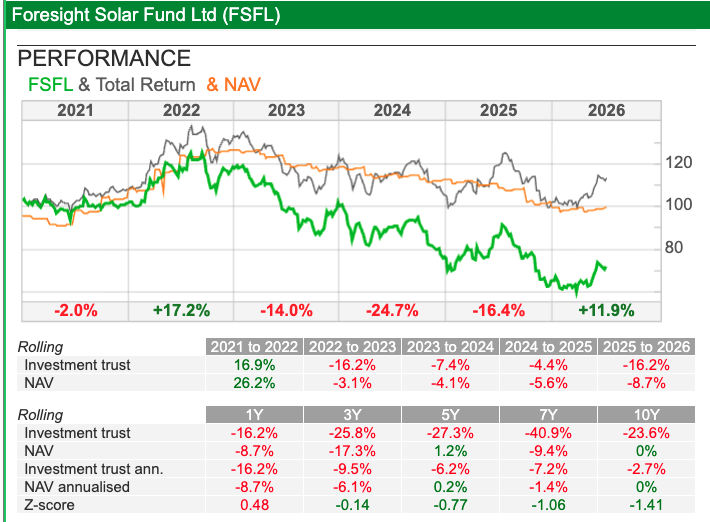

The early solar investments eventually led to Foresight launching Foresight Solar (FSFL), an investment trust dedicated to solar farms. FSFL today owns approximately 50 solar farms within the UK alongside a handful in Spain and Australia that in total sport a net asset value beyond £500 million:

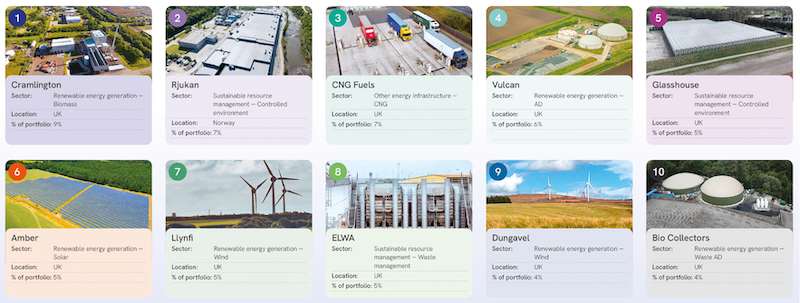

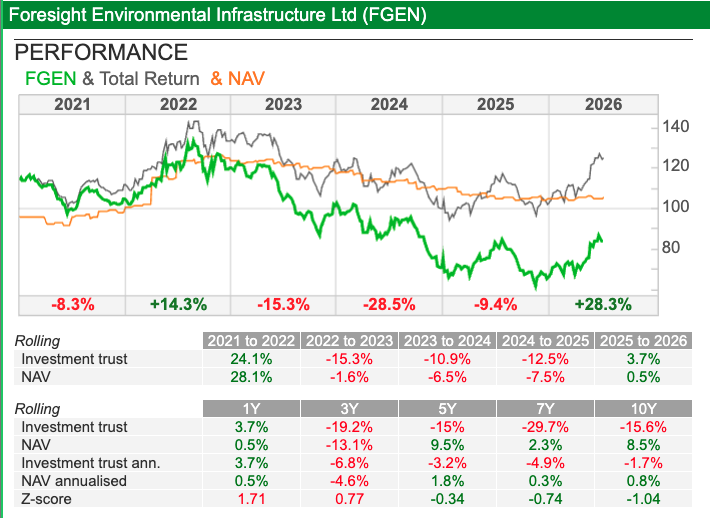

Foresight’s other investment trust, Foresight Environmental Infrastructure (FGEN), operates a more diversified portfolio that include biomass plants, wind farms, waste-treatment centres and biomethane facilities, and boasts a net asset value that exceeds £600 million:

Foresight describes its renewable-energy investments — which represent approximately 85% of client money and also supports projects such as afforestations, electric buses, hydropower stations and battery-storage systems — as ‘real assets’.

Complementing Foresight’s ‘real assets’ are various private-equity portfolios that invest in SMEs throughout the UK and Ireland and which support approximately 15% of assets under management.

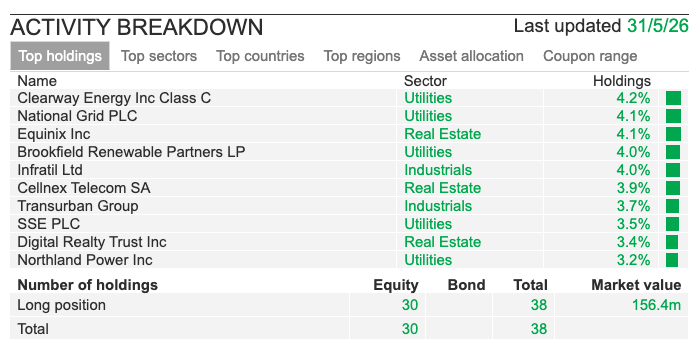

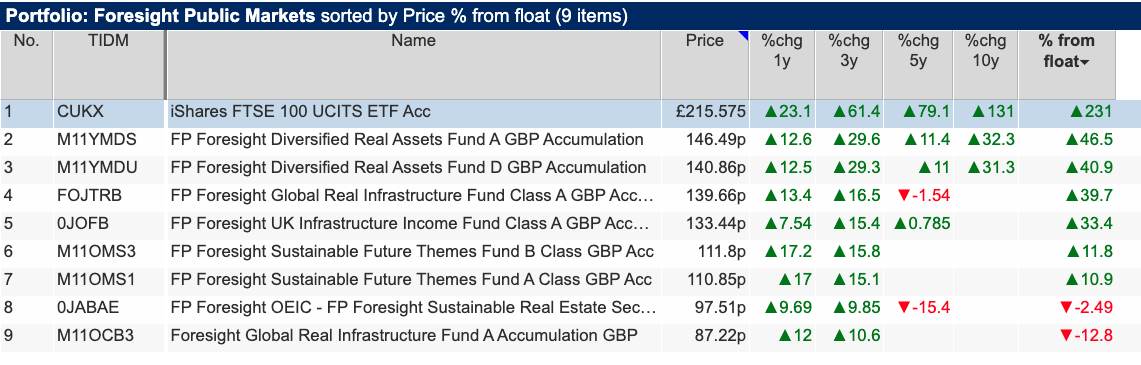

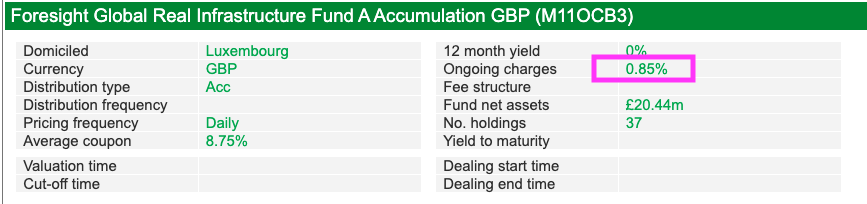

As well as the two investment trusts, retail investors have been able to invest through a handful of open-ended Foresight funds. The FP Foresight Global Real Infrastructure Fund for example invests in companies that “own or operate critical infrastructure assets which provide a net social or environmental benefit“. Holdings include National Grid and SSE:

However, Foresight announced last month these ‘public market’ funds, with total client money of £1 billion, would be sold due to “ongoing challenges in the sector creating a need to operate at ever increasing scale“.

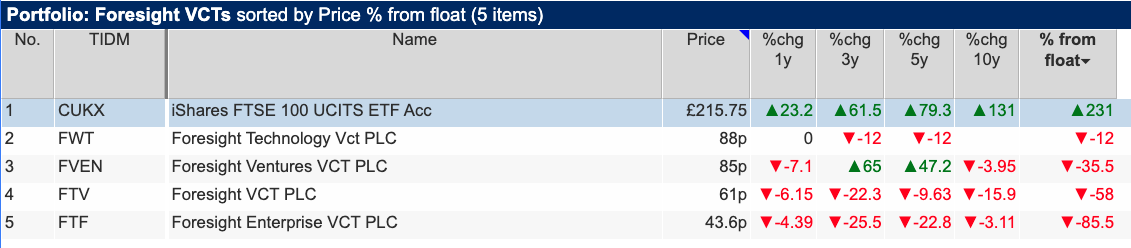

Poor returns may have also persuaded Foresight to sell its public-market funds. Clients would have been far better off with a standard FTSE 100 tracker over the last one, three, five and ten years:

That said, the group’s clients should not be too surprised with their modest gains given Foresight’s funds target returns of 3% ahead of UK inflation, yields of 5% or simply “capital growth over five years“.

Foresight’s venture-capital trusts have not fared any better than the public-market funds…

…while the group’s two investment trusts have also struggled against the FTSE:

Note that the bulk of client money is invested by institutions within funds in which Foresight does not provide any public performance information.

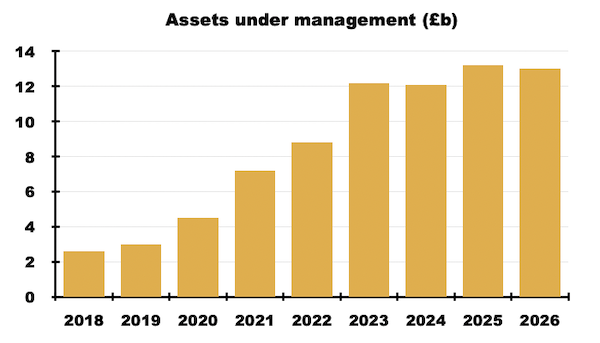

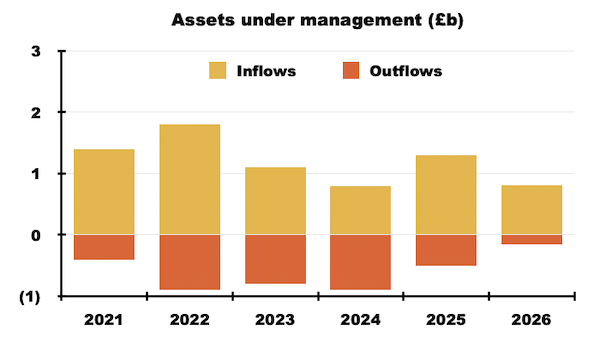

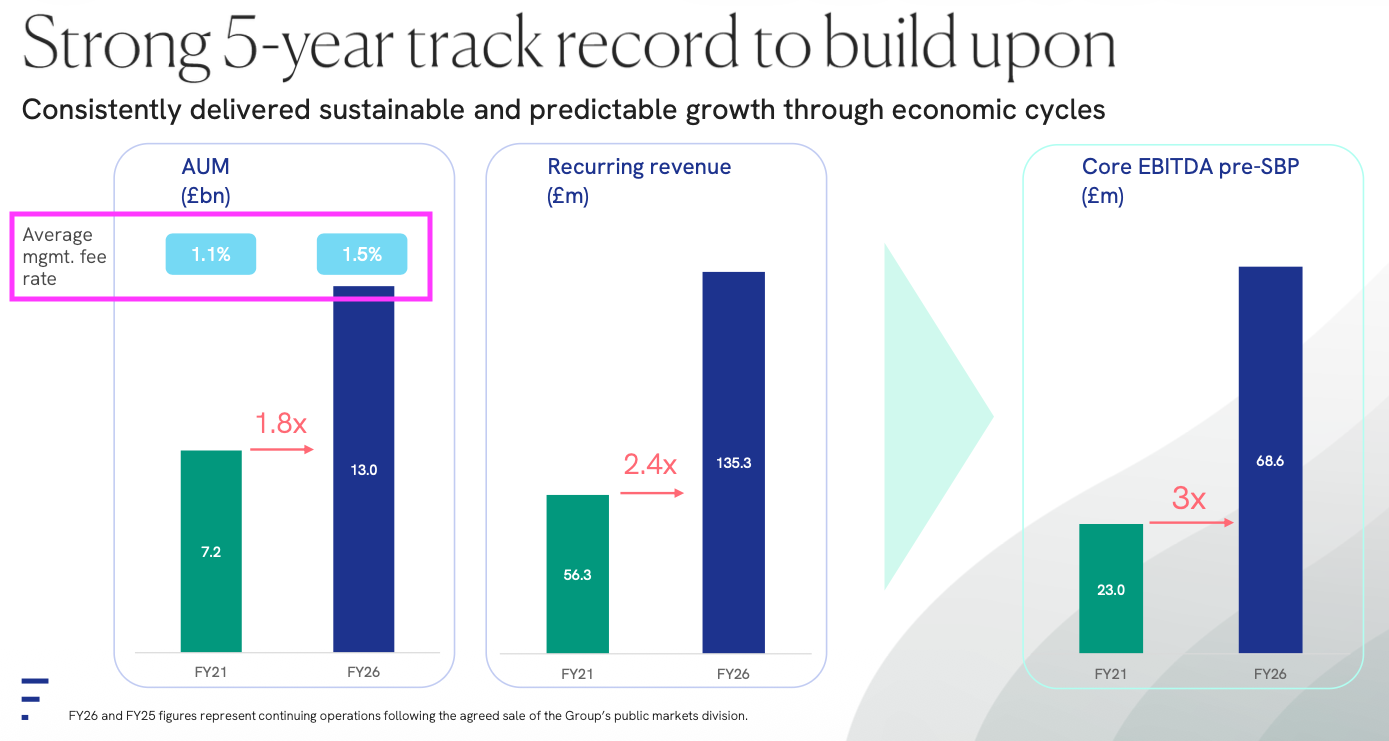

Despite the underwhelming retail returns and mysterious institutional returns, total assets under management have quintupled since 2018:

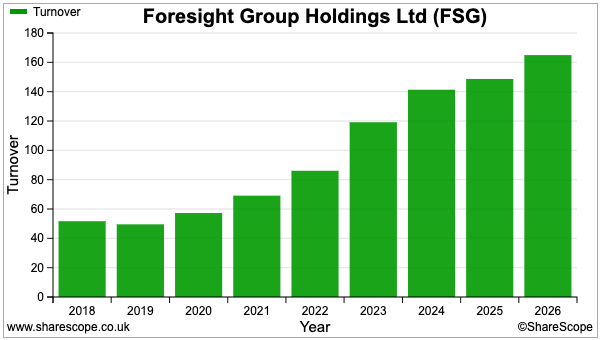

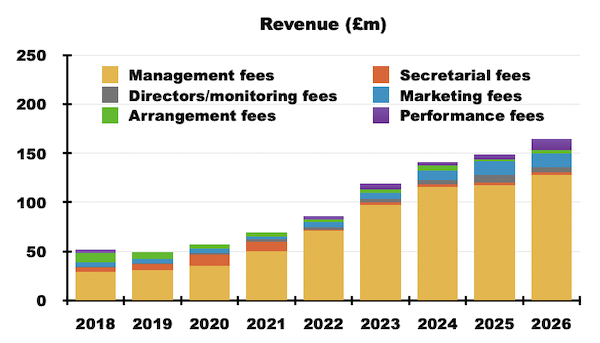

The greater client money has pushed revenue from £52 million to £165 million:

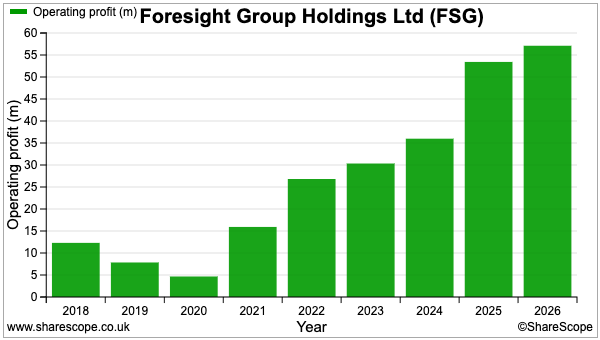

Operating profit in turn has advanced from £12 million to £57 million, with the reduced profit during 2020 in part due to higher staff costs after the group converted its partnership structure into a conventional salaried-employee model:

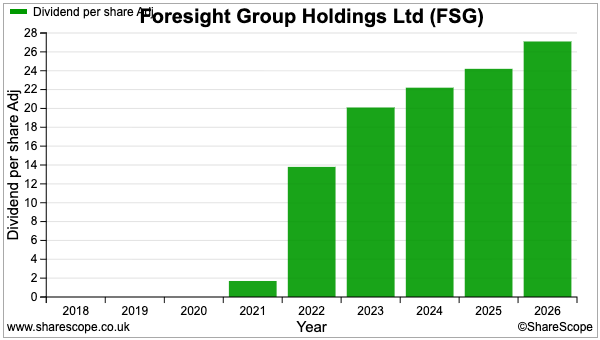

The dividend has been lifted every year following the 2021 flotation:

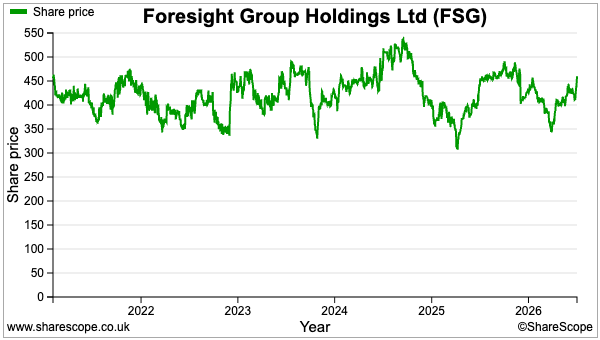

But Foresight’s shares have not made great headway since they joined the main market. The 420p flotation price compares to the recent 460p that supports a £509 million market cap and a spot in the FTSE 250:

Funds under management

Foresight is one of the very few UK fund managers that has attracted new client money in recent years.

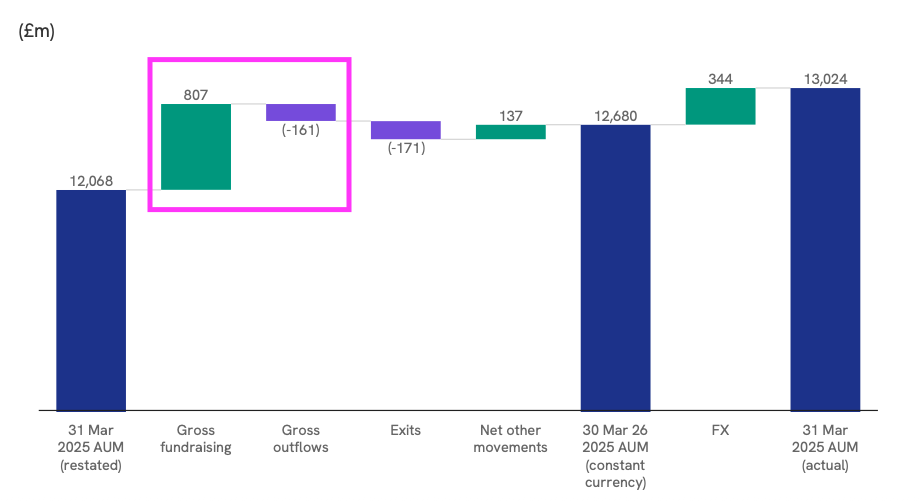

Investors added some £807 million to the group’s funds versus withdrawals of only £161 million during 2026:

My calculations indicate a net £3.5 billion has been raised since 2021:

The net inflows contrast with hefty outflows elsewhere in the sector. For example:

- Liontrust Asset Management has witnessed net client money of £20.0 billion withdrawn since 2023;

- Impax Asset Management has witnessed net client money of £22.4 billion withdrawn since 2023, and;

- Jupiter Fund Management witnessed net client money of £18.5 billion withdrawn between 2021 and 2024.

The group’s client-money expansion has been helped by acquisitions that have brought in more than £5 billion since 2021.

Another remarkable feature of Foresight’s progress is the resilience of the group’s management-fee rate. The 2026 results in fact claimed the rate had improved from 1.1% of client money to 1.5% between 2021 and 2026:

I can’t reconcile Foresight’s 1.5% calculation, given 2026 revenue of £165 million versus assets under management of £13 billion leads to an overall fee rate of approximately 1.2%.

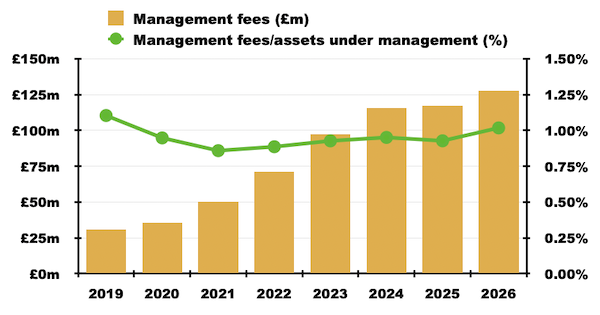

My calculations nonetheless do indicate Foresight has maintained its underlying fee rate. Revenue is split into a number of different sources:

Management-fee revenue of £128 million last year supported a 1.0% average fee rate with client money at £13 billion:

ShareScope shows the group’s investment trusts and standard retail funds charging less than 1% per annum…

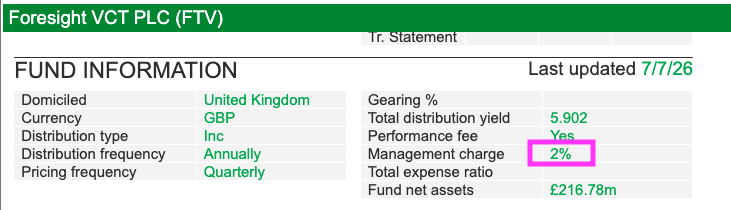

…and shows the VCTs levying a 2% charge:

Foresight’s flotation document meanwhile indicates the institutional funds might charge “up to 2.25%” a year.

Foresight’s management fees are accompanied by:

- Secretarial fees for fund-administration services;

- Director fees for Foresight staff appointed as fund directors;

- Arrangement fees (typically receipts from one-off transactions), and;

- Performance fees (mostly earned through superior ‘carried interest’).

A particularly pernicious source of income is marketing fees, which slice 2% or so from the initial sums raised from retail investors.

Last year Foresight recorded marketing fees of £14 million after raising £630 million through “higher-margin retail vehicles“.

Immediately losing 2% of your money does not seem conducive to great returns, which those earlier fund performances listed by ShareScope appear to underline. But maybe the tax advantages of the VCTs in particular can offset any steep charges.

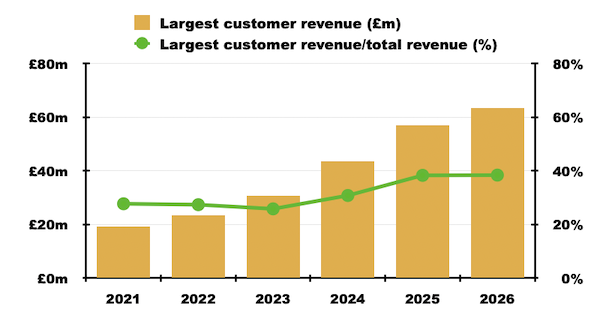

At least one customer seems undeterred by the fees. Foresight’s largest client last year contributed £63 million to revenue…

“In accordance with IFRS 8 paragraph 34, the Group has a single customer with revenues which amount to 10% or more of Group revenue. Total revenues from this customer in 2026 were £63,300,000 (2025: £56,925,000), of which £54,252,000 (2025: £44,754,000) was attributable to Real Assets and £9,148,000 (2025: £12,171,000) to Private Equity“.

…that supported 38% of the group’s top line.

The largest customer has tripled its payments since 2021:

Foresight has not disclosed the identity of its largest customer, but “cornerstone” investors named in the flotation document included European Investment Bank, UK Green Investment Bank and British Business Bank.

Financials

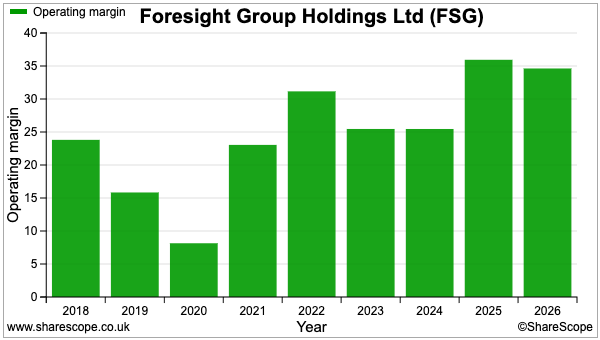

My earlier ShareScope filters had each identified Foresight’s high operating margin.

The group in fact converted almost 35% of all those aforementioned fees into profit last year:

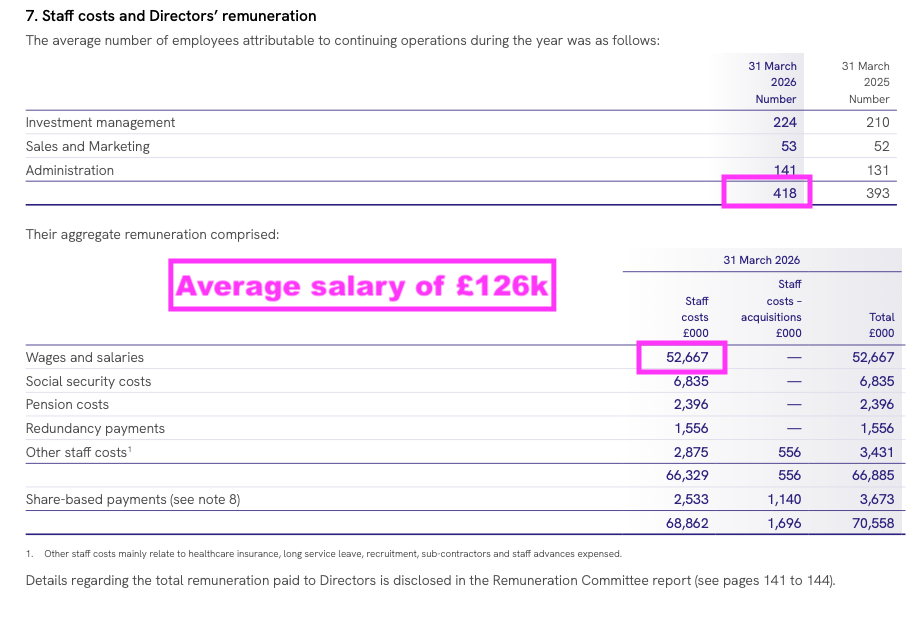

Foresight’s largest cost is its workforce. Last year almost £69 million was expensed on employees:

The average wage per employee for 2026 was £126k, which seems remarkably low for a fund-management business. Add in all the other staff costs and last year’s aggregate remuneration per head came to £169k.

For perspective, Liontrust last reported aggregate remuneration per employee of £296k, while Impax reported £240k and Jupiter some £446k.

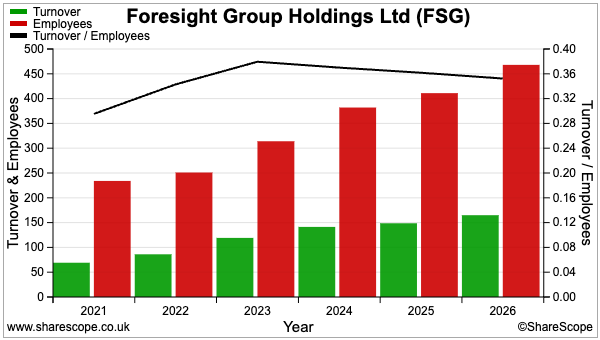

Foresight’s workforce productivity sadly does not suggest the business has obvious economies of scale:

Revenue per employee has bobbed between £300k and £400k since 2022.

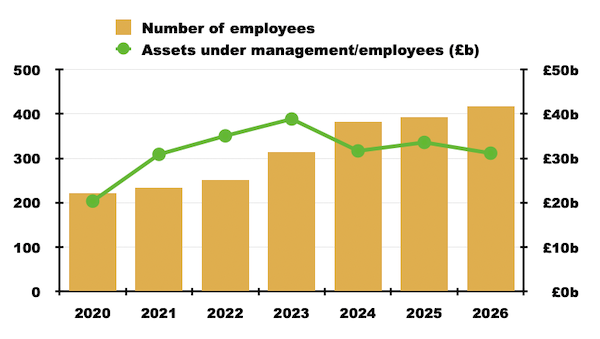

Assets under management per employee has similarly demonstrated a somewhat stagnant performance:

Foresight’s £31 million client money per employee compares to £105 million, £88 million and £115 million at Liontrust, Impax and Jupiter respectively.

The much greater assets per employee — and in turn the greater fees per employee (e.g. £1 million at Jupiter!) — can therefore justify the higher remuneration at those other three firms.

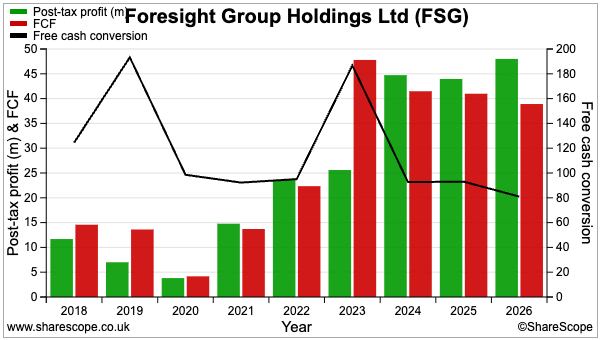

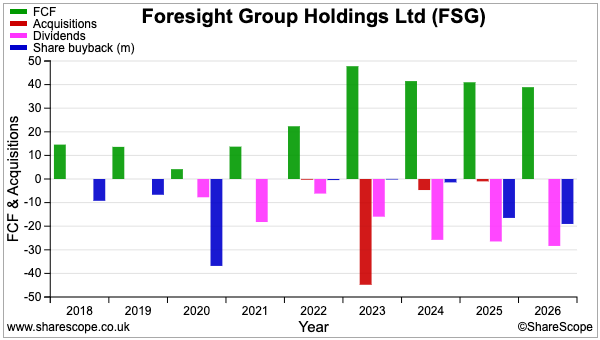

Foresight’s reported profits have generally translated into free cash at a rate of 90% or more:

Last year’s sub-par 81% conversion was due to a £5 million earn-out consideration for an earlier acquisition. Foresight is not afraid of spending considerable sums on other businesses — two purchases totalling £44 million were undertaken during 2023:

The two 2023 deals have not gone entirely to plan:

- The £31 million purchase of Infrastructure Capital led to a £6 million impairment following higher-than-expected redemptions. The final earn-out meanwhile “remains in dispute and is now subject to legal proceedings“.

- The £13 million purchase of technology-venture funds from Downing then led to a £3 million write-off following “NAV valuation decreases“.

Foresight’s cash flow is also used for buybacks. Some £34 million has been spent during the past two years purchasing shares in part to mitigate dilution from the group’s option scheme.

Balancing the cost of the purchases has been a handful of treasury share sales to institutional investors, which have in aggregate raised £11 million versus their original cost of £10 million.

Potential dilution does not look huge at present, given the 2026 results showed 2.8 million treasury shares compared to 3.9 million outstanding options and 116 million issued shares. A further £40 million has been earmarked for buybacks for 2027 and 2028.

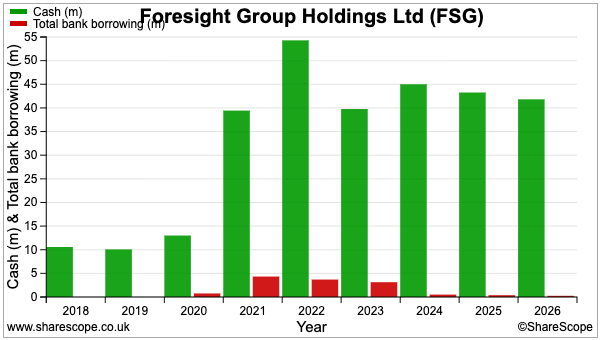

The 2021 flotation raised £32 million after fees and despite the acquisitions and buybacks, cash has reassuringly remained above £40 million while bank debt has become minimal:

Boardroom

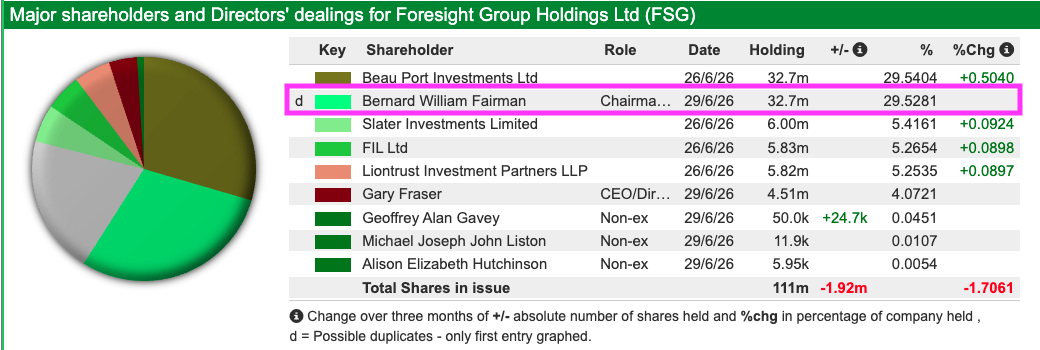

The aforementioned Bernard Fairman remains Foresight’s executive chairman and largest shareholder:

After selling 41% of his stake at the flotation, Mr Fairman still retains a near-30% position valued at approximately £150 million:

I note Mr Fairman spent £1.6 million buying more Foresight shares during 2025 at 400p, with the RNS stating his purchase reflected “confidence in the Company successfully achieving its growth ambitions”.

Mr Fairman alongside chief executive Gary Fraser and chief investment officer David Hughes interestingly form a 35% ‘concert party’ for the purposes of the Takeover Rules. A by-product of this shareholder agreement are welcome limitations on executive remuneration:

“Consistent with prior years, Executive Directors continue to waive their entitlement to pension benefits, do not participate in annual bonus arrangements and are not eligible for PSP awards due to the restrictions arising from the concert party agreement established at IPO.”

Despite the group’s higher profits, Mr Fairman’s salary has been kept at £550k since 2022. His annual dividend income meanwhile runs at a very useful £8.8 million.

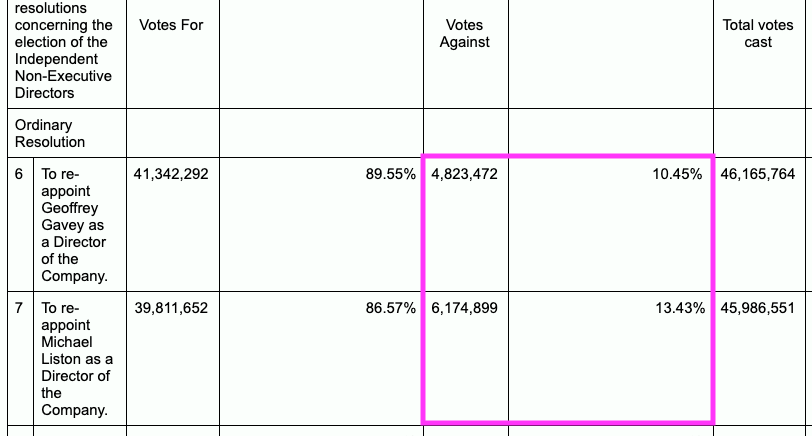

Be aware that not everyone is happy with the board’s membership. Notable protest votes against two of the three non-execs were lodged at the 2025 AGM:

I do wonder if the protest votes are linked to Foresight being registered in Guernsey. Companies House reveals the two contentious non-execs are resident in the Channel Islands, and a new non-exec appointed earlier this year lives there as well.

Favouring residents of the Channel Islands for non-exec roles may well leave Foresight with a limited pool of potential talent.

Foresight’s AGM has always been held in Guernsey and the 2026 event will be hosted at the end of this month at a luxury St Peter Port hotel:

Companies House also reveals Mr Fairman is a Jersey resident, so I doubt the AGM location will change anytime soon. I note last year’s AGM allowed senior managers not resident in the Channel Islands a chance to visit at the group’s expense:

“In July 2025, the Board held its annual Strategy Day in Guernsey, bringing together the Board and Executive Committee to validate the Group’s five-year plan and long-term growth vision.”

Mr Fairman turns 77 next month and shareholders may well increasingly enquire about his potential retirement and the future of his near-30% shareholding. I suspect Mr Fairman’s 40-plus years of private-equity investing could easily lead him to negotiate his own M&A exit.

In the meantime, Foresight’s chief executive seems a safe pair of hands. He has worked for the group for 22 years, served previously as chief financial/operations officer and owns shares worth £21 million.

Valuation and verdict

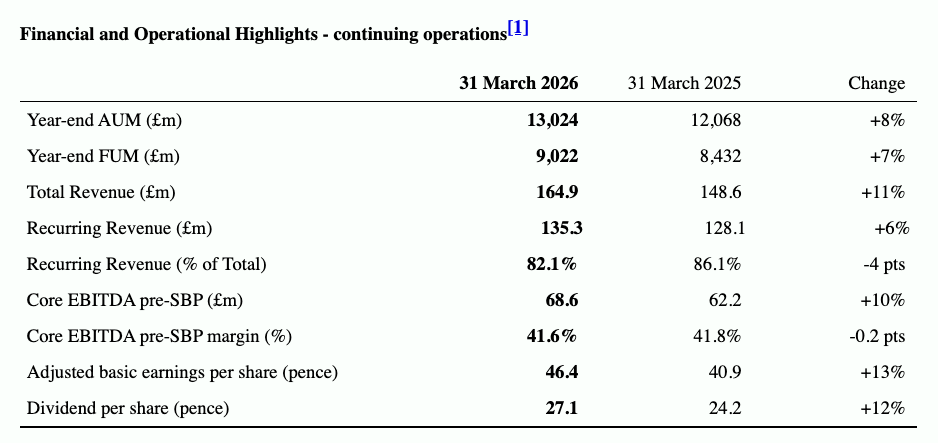

The 2026 results published last month showed double-digit advances to revenue, earnings and the dividend:

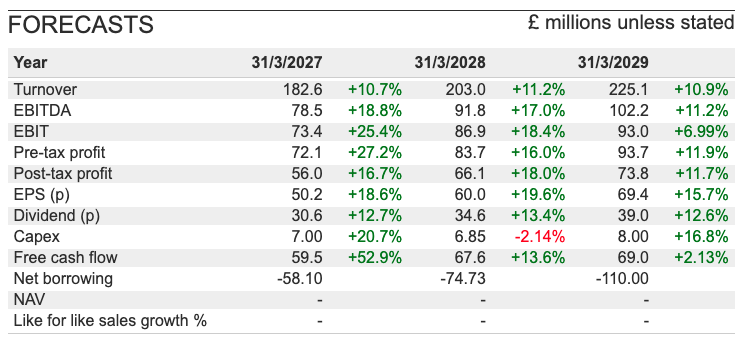

Brokers expect the double-digit growth to continue for the next three years:

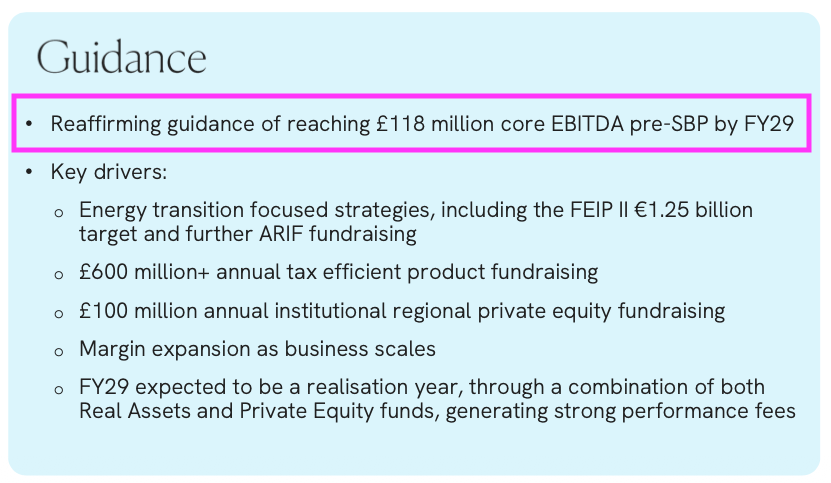

The projections are supported by Mr Fairman confirming Foresight remains “committed to [its] medium-term growth guidance.” He reckons ‘core EBITDA’ before share-based payments will reach £118 million by 2029:

Core EBITDA before share-based payments was £69 million for 2026, implying this particular profit measure will advance by 71% during the next three years.

Even with accelerated fundraising into Foresight’s ‘energy transition’ portfolios, client money advancing 71% by 2029 without further acquisitions does seem somewhat of a stretch.

I see the guidance notes above refer to “FY29 expected to be a realisation year… generating strong performance fees“, which implies that year’s outcome could be bolstered by major ‘one-off’ returns.

Mind you, Foresight’s chief executive intriguingly talked of his long-term goals for assets under management reaching £20 billion (versus £13 billion today) and the core EBITDA margin improving to beyond 50% (versus 42% today) during this results webinar Q&A.

The 460p shares do not appear expensive trading at 10x 2026 adjusted earnings and less than 7x earnings predicted for 2029:

The trailing 27.1p per share dividend meanwhile supplies a near-6% income that might expand to 9% should the forecasts prove accurate:

Whether the estimates become reality will of course depend on Foresight attracting greater client money… which in turn will ultimately depend on appealing portfolio returns. At least judging by the mixed progress of Foresight’s investment trusts…

…I would speculate client interest has been maintained primarily by persuasive advisers and glossy brochures extolling the long-term promise of a ‘decarbonised future‘.

That long-term promise remains intact for now as client money — particularly from retail investors — continues to pour in. But I do wonder whether Foresight’s customers are truly receiving value for money. Let’s just say the aforementioned 2% marketing fees in particular seem to favour shareholders over the end client.

All told, Foresight has not entirely ridden my prejudices against the sector…

…but I am pleasantly surprised the group’s remuneration appears under good control. That control I am sure is due to the influence of Mr Fairman, his near-30% stake and presumably his preference to receive a healthy dividend rather than pay substantial amounts to employees.

Assuming you can live with the group’s charging structure, its history of acquisition write-downs, that particularly large customer and the Channel Islands bias, Foresight does at present appear one of the more appealing industry operators.

And its shares ought to enjoy good upside potential should the business actually achieve that £118 million core EBITDA target.

But be warned: my previous ShareScope profiles within this sector have demonstrated that if client-money inflows turn into client-money outflows, the share-price damage can be substantial regardless of whether the shares are priced at 10x earnings or 40x earnings.

Until next time, I wish you safe and healthy investing with ShareScope.

Maynard Paton

Disclosure: Maynard does not own shares in Foresight Group.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.