Updated: August 2024

ShareScope is packed full of useful financial data. This data holds the key to understanding the financial health and value of any company you are looking at.

To a new or inexperienced investor, the mass of numbers may seem a little daunting. That’s quite understandable but it shouldn’t be. If you understand basic arithmetic then you can understand a company’s finances with a little bit of effort and the help of ShareScope.

Most of the numbers that you will see in ShareScope come from a company’s three main financial statements. These are:

- The balance sheet

- The income statement

- The cash flow statement

All these statements are linked and show how money moves around a company. To be a good investor you need to understand what’s in these financial statements and what the numbers mean. If you can master this, then you are well on the way to being a better investor.

I’m going to explain the three main statements before getting on to how to use them. I’ll start in this chapter with the balance sheet.

First things first

Before a company can start generating sales and profits it usually has to invest some money to buy things to help it do that. It will use money from its owners (shareholders) and possibly a bank loan to buy things such as land, buildings, computers and stocks of goods to sell. It will often need reserves of cash to pay any employees before profits start rolling in.

The balance sheet is arguably the most important of the three main financial statements. You should study it closely before investing in any company.

A thorough study of a company’s finances can take a long time. With ShareScope though, you can breeze through one in a matter of minutes once you’ve grasped the basics. It won’t be a forensic study of a balance sheet but you will be able to weigh up a company’s finances very well.

What is a balance sheet?

A balance sheet shows a company’s financial position at a specific point in time – usually the end of a year.

This is an important point. A company’s balance sheet tomorrow will look slightly different than it does today. It is made up of all the company’s financial transactions over a period. In short, it will tell you what a company owns (assets) and what it owes (liabilities).

Companies publish their balance sheets every year in their annual report and accounts. Companies listed on the stock exchange will publish them every six months and sometimes every three months.

Balance sheets always balance

As the name suggests a balance sheet always balances. It is based on something known as the accounting equation which says that:

Total Assets = Total Liabilities + Total Equity

Or

Net Assets = Shareholders’ Equity or Total Equity

I’ll explain what these terms mean shortly but this is the way that most companies present their balance sheets. Before we start looking at a real company’s balance sheet, I’m going to spend a little bit of time showing you how a balance sheet works in practice.

Hopefully, once you understand the basics, you’ll be able to get a better understanding of a real company by looking at its balance sheet.

John’s Property Company

Let’s look at a very simple example to see how a balance sheet works.

A friend of yours – let’s call him John – has inherited £50,000. He decides to buy a house for £100,000 to rent out.

He pays for the house by using £40,000 of his inheritance as a deposit and borrows £60,000 from a bank. He keeps £10,000 on hand to spend on the house. John sets up a property company and his accountant draws up the first balance sheet as shown in the table below:

| Non-Current Assets (House) | £100,000 |

|---|---|

| Cash | £10,000 |

| Total Assets | £110,000 |

| Mortgage | £60,000 |

| Total Liabilities | £60,000 |

| Share Capital (John’s investment in the house) | £50,000 |

| Total Equity | £50,000 |

| Total Equity + Total Liabilities | £110,000 |

The balance sheet has two sides to it. One side lists all the company’s assets (what it owns or is owed).

The other side of the balance sheet looks at how those net assets are financed by the company’s shareholders and other liabilities such as borrowings.

As you can see, the balance sheet balances. Total assets do equal total assets plus total liabilities of £110.000. Net assets also equal shareholders’ or total equity.

Assets of the house and the cash add up to total assets of £110,000. Take away the outstanding mortgage of £60,000 and we are left with net assets of £50,000. In the US, net assets might be referred to as net worth and is an estimate of what might be left over if all the assets were sold and all the liabilities were paid off.

On the other side of the balance sheet, there is the £50,000 that John inherited and invested in the business which is shown as share capital.

In a real company, the total equity is made up of the initial share capital put into it by its owners plus reserves.

The most significant reserve is retained profits – profits that have been earned but not paid out to shareholders. This is zero in John’s case because the business hasn’t made any profits yet. So shareholders’ funds are £50,000 – the same as net assets.

How new transactions affect a balance sheet

Every financial transaction a company makes will affect the balance sheet. But it will still always balance. I’m going to show you a couple of examples to show you how this works out in practice.

John spends some money

John decides to spend some money on the house to make it more appealing to potential tenants. He spends £5,000 on furniture and a new central heating system. This is how the balance sheet evolves after he has done this.

| Before | Furniture + CH | After | |

|---|---|---|---|

| Non-Current Assets (House) | £100,000 | £5,000 | £105,000 |

| Current Assets (Cash) | £10,000 | -£5,000 | £5,000 |

| Total Assets | £110,000 | 0 | £110,000 |

| Mortgage | £60,000 | £60,000 | |

| Total Liabilities | £60,000 | £60,000 | |

| Share Capital | £50,000 | £50,000 | |

| Other Reserves | £0 | £0 | |

| Total Equity | £50,000 | £50,000 | |

| Total Liabilities + Total Equity | £110,000 | £110,000 | |

| Net Assets (Total Assets minus Total Liabilities) | £50,000 | £50,000 |

Again, the balance sheet balances and the net assets and equity are still £50,000. All that has happened is that the cash balance has gone down by the £5,000 spent by John and the fixed assets number has gone up by the same amount to reflect the money that has been spent on furniture and the central heating system.

No new money has come into the business, nor has any profit been made so the total equity number is unchanged at £50,000.

John makes a profit

John soon finds some tenants and after a year he finds he has made a profit of £5,000 after he has paid out all his expenses and paid any taxes owed. He decides to retain this profit in the business instead of paying himself a dividend.

This profit has an impact on both net assets and total equity. Net assets increase by £5,000 to reflect the cash going into the business. Total Equity increases by the same amount to reflect the profits retained. Again the balance sheet balances with net assets and total equity of £55,000.

| John’s Balance Sheet | Before | Profit | After |

|---|---|---|---|

| Non-Current Assets (House) | £105,000 | £105,000 | |

| Current Assets (Cash) | £5,000 | £5,000 | £10,000 |

| Total Assets | £110,000 | £115,000 | |

| Mortgage | £60,000 | £60,000 | |

| Total Liabilities | £60,000 | £60,000 | |

| Share Capital | £50,000 | £50,000 | |

| Retained Profit | £5,000 | ||

| Other Reserves | £0 | £0 | |

| Total Equity | £50,000 | £55,000 | |

| Total Liabilities + Total Equity | £110,000 | £115,000 | |

| Net Assets (Total Assets minus Total Liabilities) | £50,000 | £55,000 |

You can see an example of a balance sheet in ShareScope below.

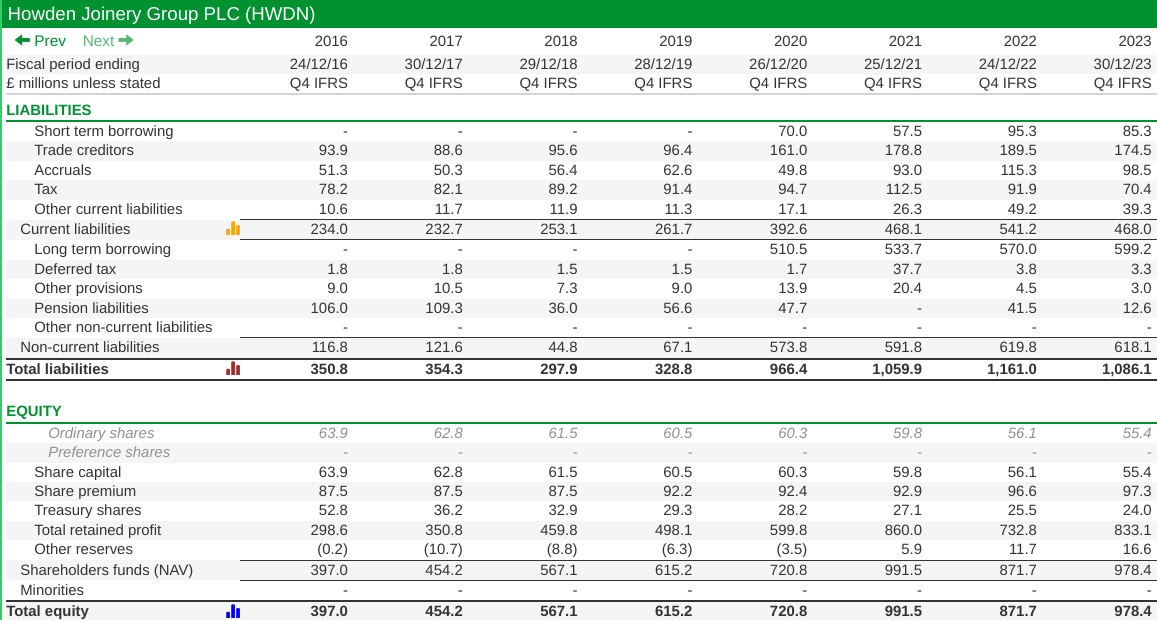

The balance sheet of Howden Joinery plc:

All balance sheets work on the same basic principles. It’s just the number of transactions that go into them which is different.

In short, assets are what a company owns. Liabilities are what it owes. Equity is the value of the shareholder’s stake in the business since it began trading. This is equal to the amount of money they have invested plus any profits that have been retained in the company. It is also the same as the company’s total assets less its total liabilities or net assets.

Below is Howden Joinery’s balance sheet as you will find in ShareScope. It is split into three parts:

- Assets

- Liabilities

- Equity

I’ll now explain the main terms within it starting with assets.

Current assets

Current assets are assets that are expected to be turned into cash within one year of the balance sheet date. The main types of current assets are as follows:

Stock and work in progress (WIP)

Stock (called inventories in the US) is generally defined as goods held for resale. Work-in-progress is goods that are part finished. Raw materials used to make goods may also be included within stock and work-in-progress. Howden Joinery was holding £382.8m of stock and work-in-progress at its last balance sheet date of 30 December 2023.

Debtors

Debtors are amounts of money that are owed to the company.

Sometimes in ShareScope, it is not possible to separately disclose the different types of debtors. However, in most cases, the biggest type of debtor for a company is known as a trade debtor. This is money owed to it by customers for goods and services that have been sold or provided but where the cash has not been received. The most common way a trade debtor is created is by selling goods or services on credit.

Howden had £194.5m of debtors at its 2023 balance sheet date, of which trade debtors were £159.5m. This should end up as cash that flows into the company’s coffers during the next year.

There is of course a risk, normally very small, that some customers do not pay their bills and a bad debt is realised and the money will have to be written off.

Prepayments

Prepayments are created when a company pays for services in advance but has not yet received them. This might be something like paying for stock which has not been delivered or a bill that has been paid in advance.

They are treated as an asset because they are effectively owed to the company. Howden had prepayments of £39m at its last balance sheet date.

Securities and cash

A company may decide to put some surplus money into bonds or shares to earn a higher return than cash in a bank account. These are classified as securities. Howden did not have any money invested in securities at its last balance sheet date.

Cash doesn’t need any explanation. Howden’s last annual balance sheet had a cash balance of £282.8m.

Non-current assets

These are assets that are intended for continued use in the business in order to generate revenues and profit and are not for sale. They are usually divided into three main categories:

- Intangible assets

- Tangible assets

- Investments

Intangible assets

These are assets that you can’t physically touch. They include things such as:

- Brands

- Patents

- Trademarks

- Publishing titles

- Goodwill – the amount paid over net asset value when buying another company

Intangible assets can be bought by a company or developed within it. They are not always easy to value and there are rules for how these are presented on a balance sheet. The values you will see are net values after a charge known as amortisation has been deducted.

Amortisation is a cost of using an intangible asset which is incurred each year that companies are required to charge against their revenues which in turn reduces their profits. This annual expense is meant to match the cost of the intangible assets against the revenues that they generate over their remaining useful lives.

For example, if a company had an intangible asset with an original cost of £10 million that had a life of ten years and would be worth nothing after that, a company might choose to evenly charge £1m per year in amortisation (known as a straight line method of amortisation).

Some businesses such as pharmaceuticals, computer software or consumer goods companies can have very large intangible assets on their balance sheets.

Howden Joinery did not have a large amount of intangible assets at the end of 2023. They totalled £43.5m of which £12.4m is goodwill – telling the reader that Howden has bought some businesses in the past.

Tangible assets

These are physical assets that you can touch. They are used in a business over a number of years often to make goods that are to be sold. The most common tangible assets are:

- Land and buildings

- Plant and machinery

- Motor vehicles

- Fixtures and fittings

The figures you will see on the balance sheet are what are known as their net book values. These are calculated by taking the original cost of the asset less the amount of accumulated depreciation.

Depreciation is a very important number in a company’s financial statements. It is similar to amortisation and is charged against the value of an asset over its estimated useful life. It can be interpreted in different ways such as the loss of value of an asset or an estimate of the annual amount of money that a company needs to spend in order to maintain the asset in its original condition.

Howden has a lot of tangible assets totalling £1104.8m and they are by far the biggest part of its balance sheet’s total assets of £2064.5m.

Investments

This figure will include the value of stakes in other companies (where the ownership stake is 50% or less) known as joint ventures and associates. It will also include long-term investments in shares or bonds.

At its last balance sheet date, Howden did not have any investments.

Now let’s have a look at Howden’s liabilities and equity.

Current liabilities

These are liabilities that the company usually has to pay within one year of the balance sheet date. They can include:

- Bank loans

- Tax owed

- Trade creditors – amounts owed to suppliers

- Accruals – an estimate of an amount for goods and services used but where no bill has been received.

Howden had £468m of current liabilities at its last balance sheet date, with trade creditors making up the biggest part. We can also see that the company owed £70.4m in taxes, had £85.3m in borrowings that had to be repaid within a year and £98.5m of accruals.

Non-current liabilities

These are liabilities due after one year. The most common items in this category are:

- Long-term borrowings

- Deficits of Final Salary Pension Schemes

- Provisions – amounts set aside for future costs based on a decision already taken. e.g. demolition of a factory site.

- Deferred tax – tax payable in future years

All these total just over £618m for Howden with virtually all of it accounted for by borrowings.

Howden’s total liabilities added up to £1086.1m at its 2023 balance sheet date. Take this number away from the £2064.5m of total assets and there is £978.4m of net assets left over.

Equity

This is the sum of share capital plus reserves. The main items of equity are:

- Share capital – there are different kinds of share capital. The most common type is ordinary shares. The value of share capital is the number of shares that have been issued multiplied by a nominal or par value. Howden had £55.4m of share capital at the end of 2023.

- Share premium – the amount above par value paid for a share. In Howden’s case, this is £97.3m. If you add this number to the share capital number, you will get the total amount of equity that has been invested by shareholders in the company. For Howden, this is £152.7m

- Treasury shares – This is the value of previously issued shares that have been repurchased by the company. It reduces the amount of shareholders’ equity. In Howden’s case, the reduction is £24m. The treasury shares are often held by the company to reward employees with bonuses or share investment schemes and are usually excluded from earnings per share (EPS) calculations and do not receive dividends.

- Retained profits – profits that have been made by the company that haven’t been paid out as dividends to shareholders. Howden had £833m of retained profits at the end of 2023.

- Minority interests – refer to the value of equity of a company’s businesses not owned by the parent company – in this case Howden Joinery. It is very common for companies to own majority stakes such as 90% of a business, but the 10% owned by others is disclosed as a minority interest in the equity section of the balance sheet and reduces the total equity attributable to shareholders. Howden didn’t have any minority interests on its last balance sheet date.

In very basic terms, the total equity of a company amounts to the amount of money paid in by shareholders (share capital + share premium) plus all the retained profits. In 2023, this figure was £978m for Howden. As a balance sheet must balance, this is equal to the value of its net assets which is the same number.

Total Assets also equal the value of total liabilities and total equity of £2068.5m.

All these numbers in the balance sheet help to explain a company’s financial position. As for what they mean for you as an investor, I’ll tell you in the next chapter.

Next: Chapter 3 – Analysing balance sheets

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.