The lead executives at Alfa Financial Software were paid just £29k last year to match the London Living Wage. Maynard Paton links the commendable remuneration to the run of eleven special dividends declared by this high-margin, high-ROE business.

Can you imagine company directors working for £14.80 an hour?

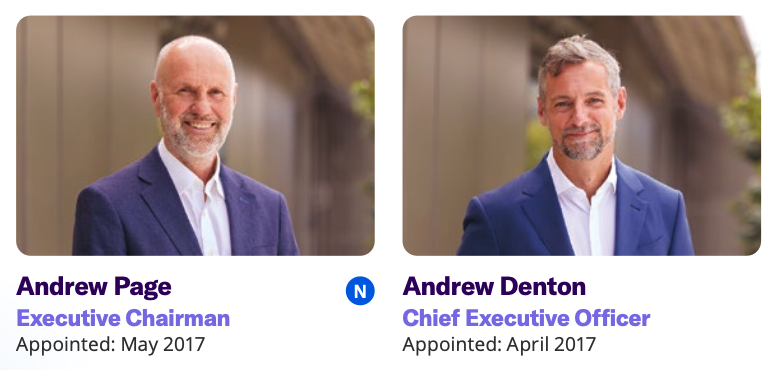

If not, then say hello to Andrew Page and Andrew Denton, the two primary executives of Alfa Financial Software.

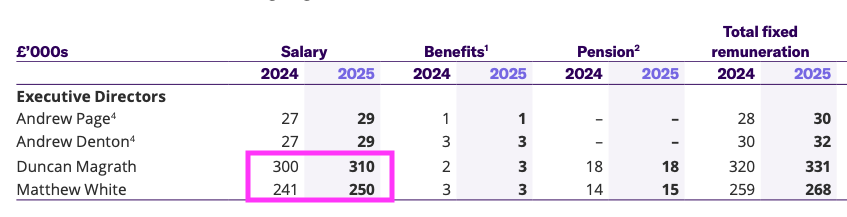

Last year both men collected salaries of just £29k after each committed to being paid only the London Living Wage. Alfa’s 2025 annual report confirmed:

“The Chairman and CEO will continue to have their salaries aligned to the London Living Wage and will receive an increase of 6.6%, marginally below the rate announced by the London Living Wage Foundation of 6.9%. Both have also chosen to waive any variable incentive award or pension contribution for 2026. As significant shareholders, they have expressed a clear preference for their remuneration to remain closely aligned with that of other shareholders.”

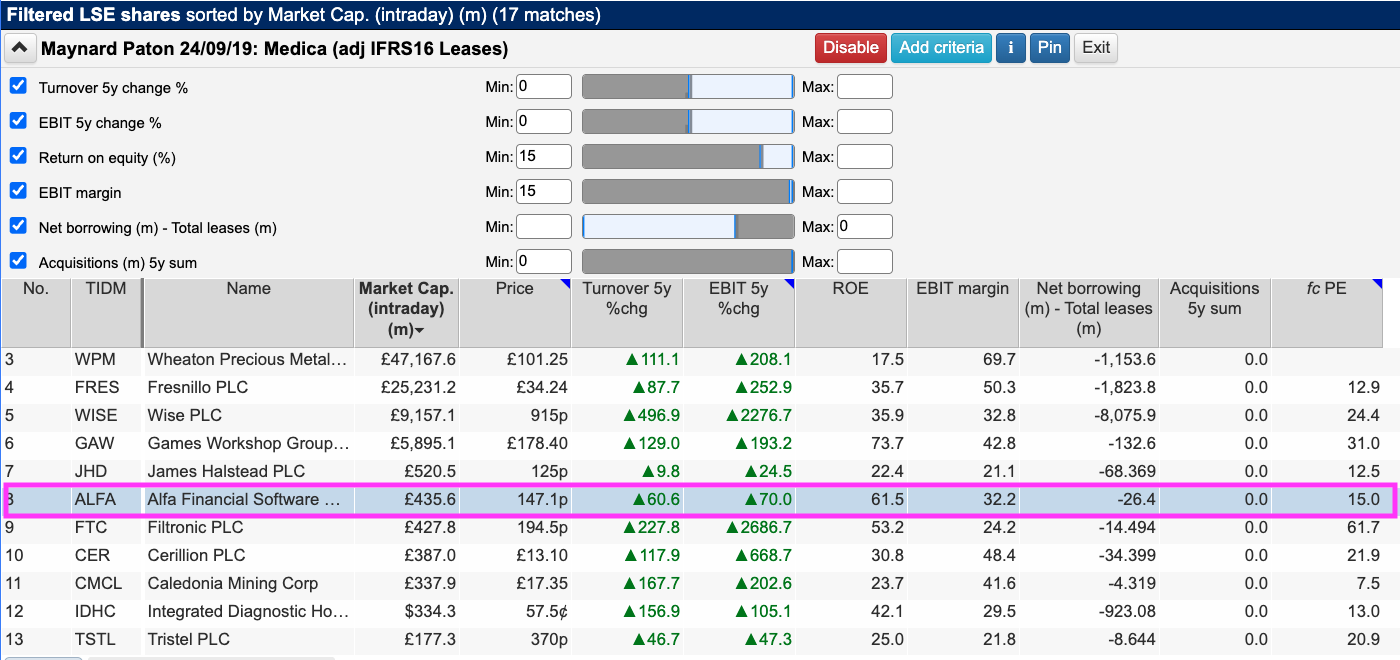

I discovered this commendable remuneration after pinpointing Alfa during one of my regular ShareScope searches.

Alfa appeared on an old ShareScope screen that sought respectable companies that had expanded without acquisition:

(You can run this screen for yourself by selecting the “Maynard Paton 24/09/19: Medica” filter within ShareScope’s amazing Filter Library. My instructions show you how.)

This screen’s filter criteria demanded:

- Positive five-year turnover and operating profit growth;

- A minimum of 15% for both operating margin and return on equity (ROE);

- Net bank borrowing of no more than zero (i.e. a net cash position), and;

- A five-year acquisition spend of zero.

I selected Alfa because the share was also highlighted by three other ShareScope filters (here, here and here), which suggested the company’s combination of organic growth, high margins, robust ROE, net cash, significant director shareholdings and reasonable valuation was very worthy of further investigation.

Plus there are two executives on just £29k salaries working at a business that last year reported a £40 million profit.

Let’s take a closer look.

Introducing Alfa Financial Software

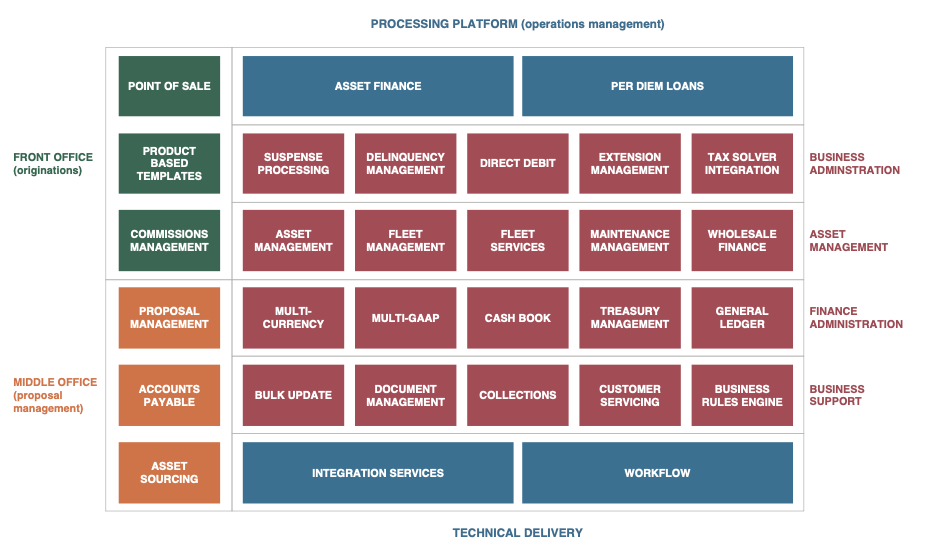

Alfa develops what it claims to be the “world’s leading asset-finance software“.

The business was started by Andrew Page, Ian Hargrave and Justin Cooper during 1990 and won its first client — what was then Hambros Bank — during 1992.

Alfa’s software helps banks and other lenders manage all their different loan, lease and hire-purchase products. Retail car finance is probably the most common product handled by Alfa’s systems, but I believe customers can provide finance for anything from photocopiers to aeroplanes.

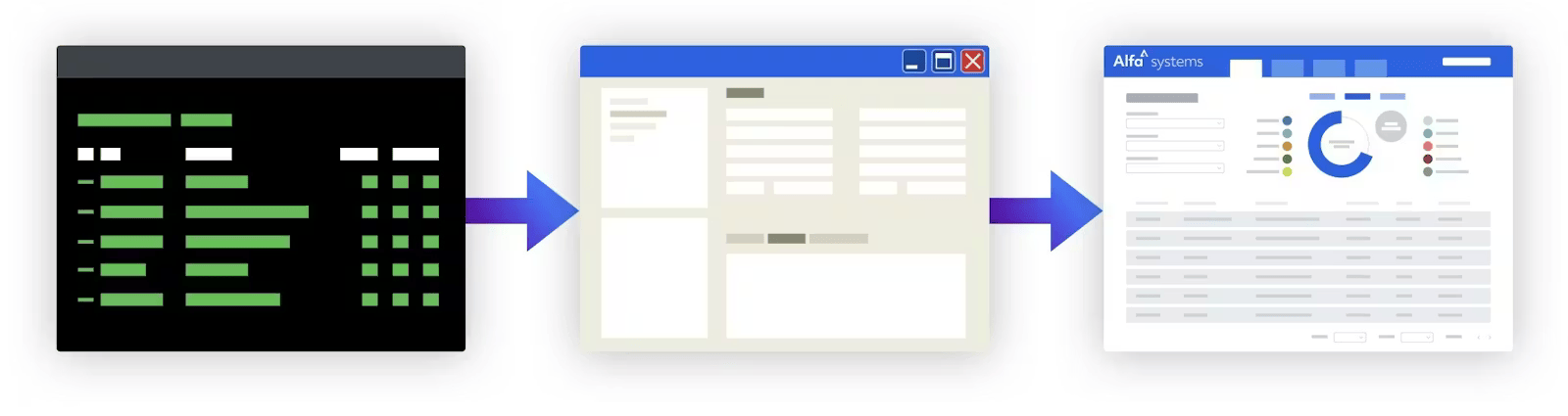

Asset-finance software serves — at least according to Alfa — an “extremely complex” industry that demands all sorts of particular regulatory, accounting and workflow requirements. The diagram below from Alfa’s flotation document outlines the system structure:

New customers have apparently been attracted by Alfa’s purpose-built ‘platform’ system versus ‘legacy’ alternatives that have shown to lack flexibility and functionality.

Alfa’s website says the software is “trusted by the world’s most progressive finance providers“, and name-checks quoted UK lenders Lloyds Bank, Close Brothers and Paragon. Also listed on the website are the financial-services arms of Mercedes and Toyota. Last year almost three-quarters of revenue was earned from outside the UK:

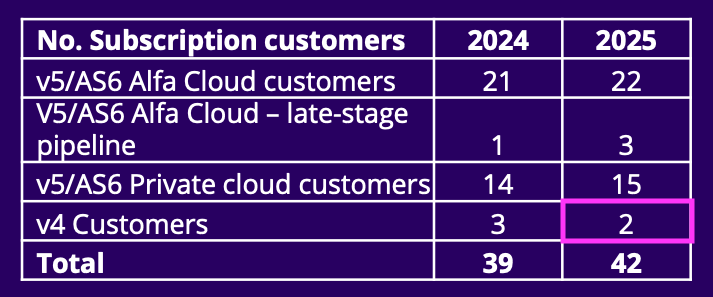

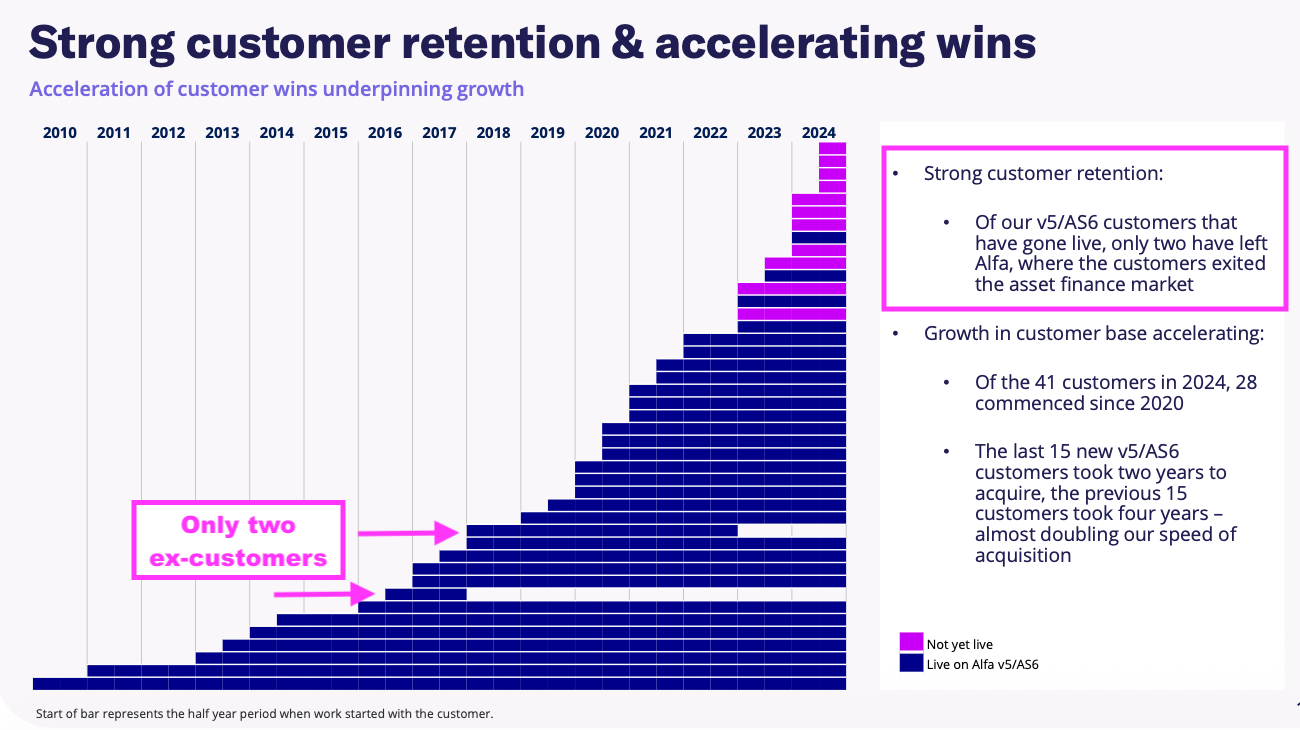

Some 42 customers now pay Alfa subscription revenues although two clients remain on version 4 of Alfa’s software:

Version 4 was introduced during 2003 and was succeeded by version 5 during 2010 and by version 6 during 2024. I suppose clients still using version 4 underlines the longevity of Alfa’s systems, although the two non-adopters may emphasise the glacial pace at which the asset-finance industry upgrades its software.

The benefit of a protracted ‘upgrade cycle’ is client loyalty. Alfa claims only two customers have ceased their version 5 usage:

Of those two leavers, one exited the asset-finance industry entirely while the other was acquired by another Alfa customer. The chart above shows Alfa’s customer wins accelerating; the latest 15 customers took two years to acquire, versus four years for the previous 15.

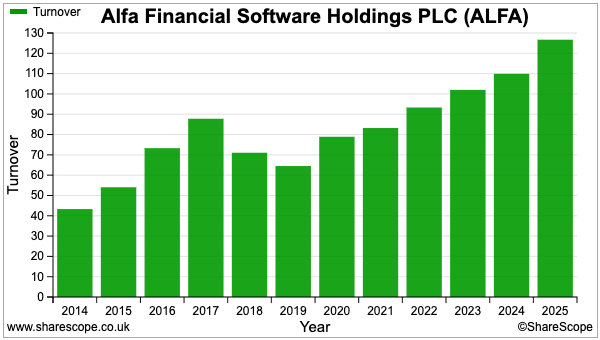

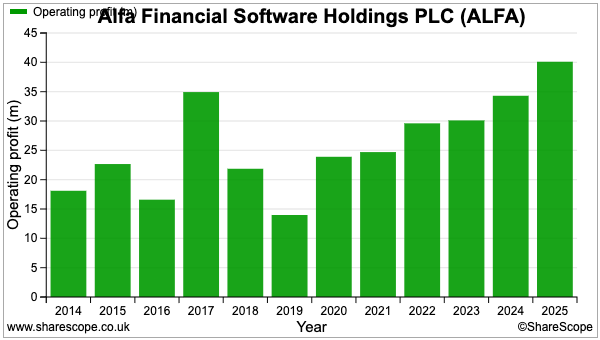

The extra clients have helped pushed revenue to £127 million and operating profit to £40 million:

The reduction to revenue and profit during 2018 and 2019 was due to major customers pausing or postponing the implementation of Alfa’s software…

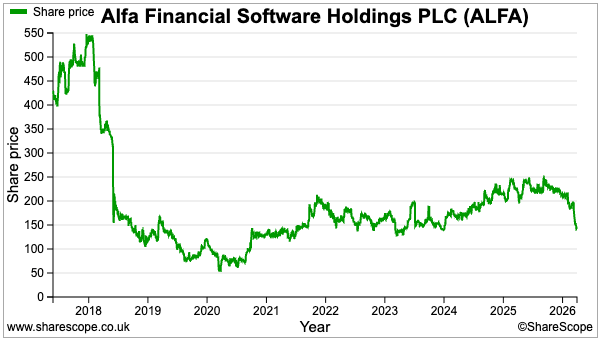

…and, as the share price shows, the resultant profit warning did not go down well with the stock market:

Alfa floated on the main market at 325p during 2017 and the recent 147p share price supports a £436 million market cap.

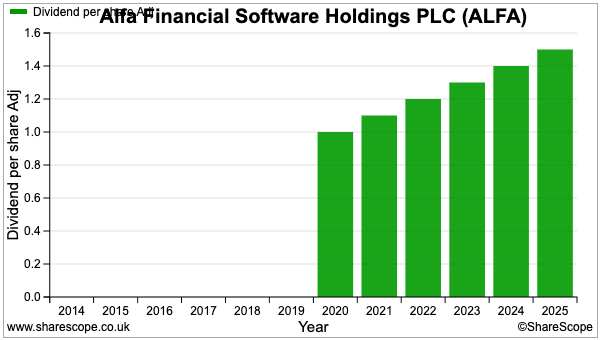

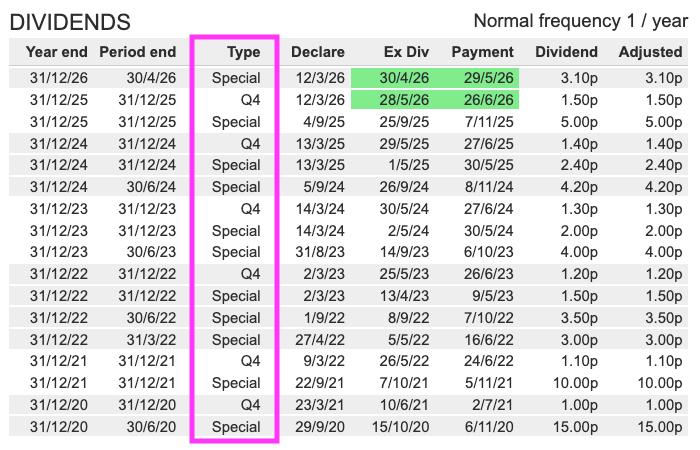

Alfa’s dividend has not yet suffered any setbacks:

Note how the group’s payout record has been bolstered by no less than eleven specials:

The specials tot up to 53.7p per share versus just 7.5p per share from all of the ordinaries. Alfa says it will “consider” special dividends when it has “excess capital” and reckons this approach allows the company to “maintain optionality around the availability of funds for possible future investment“.

Revenue profile

With the benefit of hindsight, Alfa’s 325p flotation price — and the then very racy 40x near-term P/E — was always vulnerable to any problems.

The group’s flotation document spotlighted the concentrated nature of the customer base. The top ten customers at the time supported at least 79% of revenue:

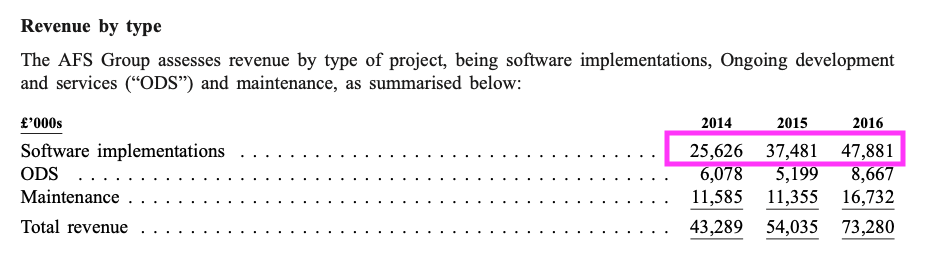

“In the years ended 31 December 2014, 2015 and 2016, the Group had 29 clients, 27 clients and 28 clients, respectively. Over the same period, the top ten clients in terms of revenue (the composition of which varied from period to period) together in each year accounted for 79%, 86% and 90% of the Group’s revenue, respectively.”

In fact, the largest three customers during the three years before the flotation supported 46%, 52% and 52% of total revenue:

The flotation document said the revenue concentration reflected the “disproportionate contribution… of clients in the software implementation phase”.

As well as expenses to implement the software, the “software implementation phase” included perpetual licence fees — one-off, upfront and typically sizeable sums the clients then paid to use Alfa’s system.

Software-implementation income represented approximately 65% of group revenue prior to the flotation…

…and clearly Alfa needed a constant flow of new customers within the ‘software implementation phase’ to maintain its pre-flotation progress.

The profit setback of 2018 and 2019 seemed to accelerate Alfa’s transition to cloud-based services and shift from a perpetual-licence structure to the now-common recurring-subscription model.

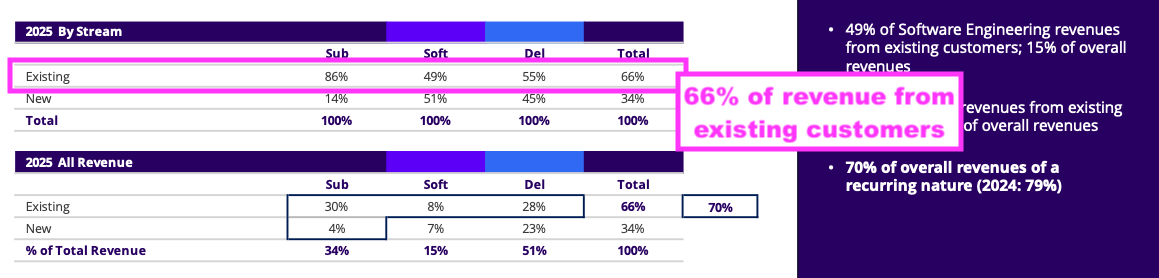

Alfa’s first cloud-based service was sold during 2017 and subscriptions last year supported 34% of revenue while perpetual licenses represented only 2%.

Including revenue from upgrades and certain development work, existing customers contributed 66% to last year’s top line — a proportion of income that the group says is of a “recurring nature“:

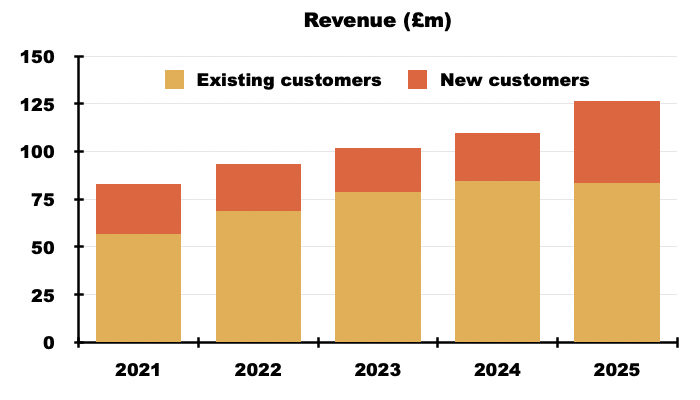

Between 2021 and 2024, revenue from existing customers had increased from £57 million to £85 million… but reduced a fraction to £84 million during 2025:

Revenue from new customers meanwhile had bobbed around £25 million until surging to £43 million last year.

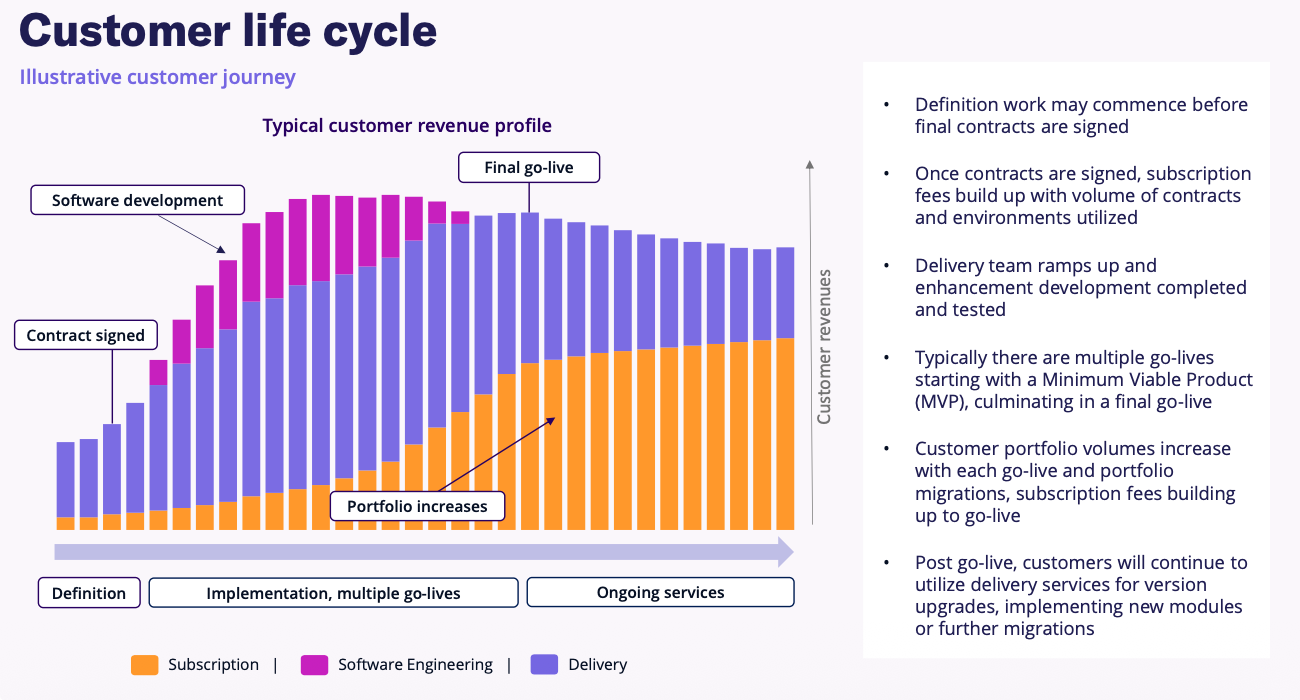

I am hopeful the new customers won last year will continue to contribute significantly to Alfa’s total revenue. The group’s illustrative chart below suggests income from new customers reduces only slightly following the initial implementation:

While Alfa still appears very dependent on new clients for significant growth, at least the transition to subscriptions has lessened the dependence on key accounts.

For example, during 2025 one customer paid £11 million to support 9% of revenue, while back in 2017 one customer paid £20 million to support 23% of revenue. Furthermore, revenue from the top five clients supported 33% of revenue last year versus 61% for 2019.

Financials

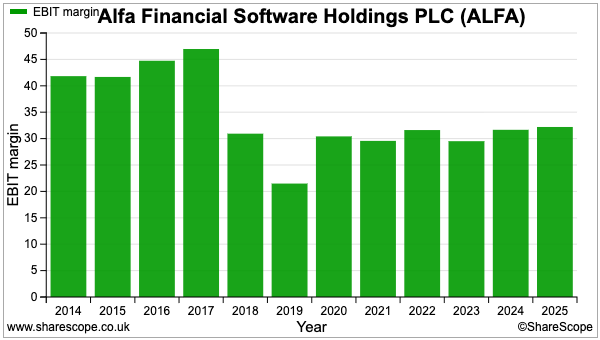

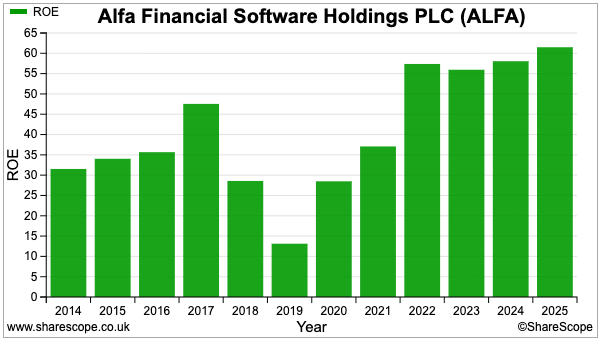

My initial screening had already signalled Alfa’s superior margin and ROE.

Alfa has on average converted a superb 30% of revenue into profit during the last ten years:

The average ROE during the same period is a terrific 42%:

The wonderful ratios imply Alfa enjoys a substantial competitive edge. They also reflect the favourable characteristics enjoyed by many successful software companies, notably:

- Economies of scale through selling the same software to multiple customers, and;

- The ability to operate on relatively minimal amounts of capital (Alfa’s last accounts showed IT equipment worth only £500k — a remarkably low amount for a software business reporting a £40 million profit!).

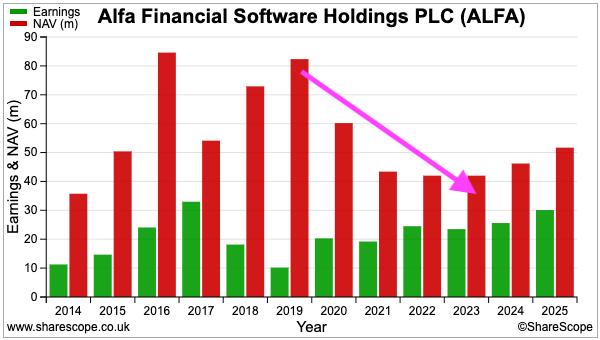

Note that Alfa’s impressive ROE has been achieved in part by reducing its shareholder equity between 2019 and 2023:

The equity reduction is due partly to Alfa distributing its ‘excess’ cash back to shareholders.

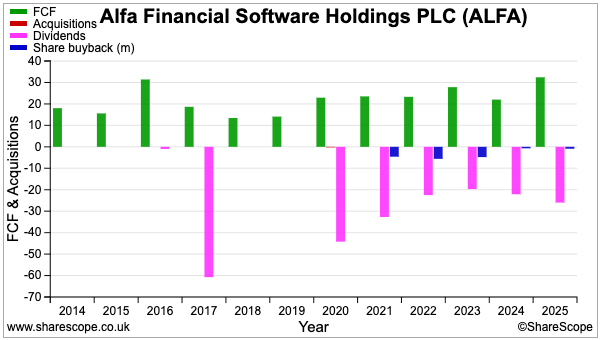

Including those aforementioned eleven special dividends, since 2020 Alfa has handed back £167 million to shareholders versus an aggregate free cash flow of £152 million:

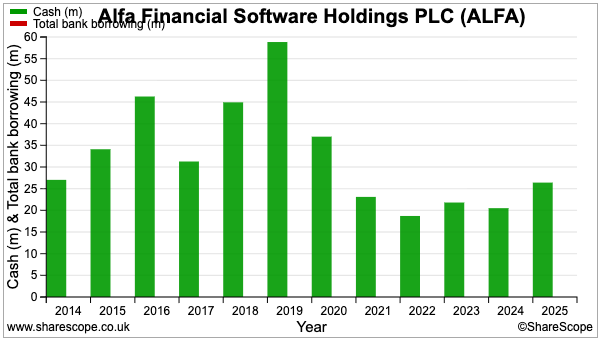

At the last count cash stood at £26 million while bank debt was zero:

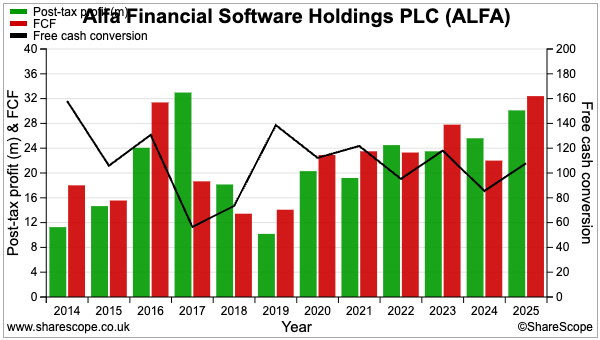

Cash conversion has been extremely acceptable. ShareScope reveals reported earnings have converted into free cash at an average of more than 100% during the last five and ten years:

Alfa says its free cash conversion should remain within the 90-100% range.

My reading of Alfa’s accounts has not unearthed anything obviously untoward, and I particularly welcome the absence of adjusting and exceptional items within the income statement.

However, I did note Alfa has since the flotation capitalised development costs of £12 million that have yet to be charged to reported earnings. I estimate operating profit would on average have been 5-6% lower were all the development costs expensed as incurred.

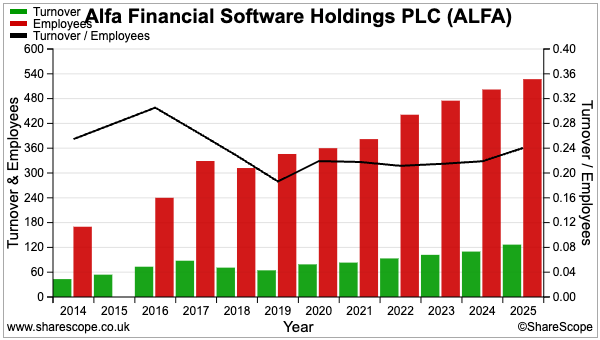

Probably the most disappointing ratio is revenue per employee.

Although this measure advanced to £246k last year, recent workforce productivity remains below the group’s pre-flotation efforts:

I would have imagined the ‘scalability’ of Alfa’s software would allow revenue to grow faster than the headcount.

By far Alfa’s largest expense is employee costs (c50% of revenue, average salary: c£98k), and further margin improvement seems unlikely if extra customers necessitate a commensurate number of extra staff.

Boardroom

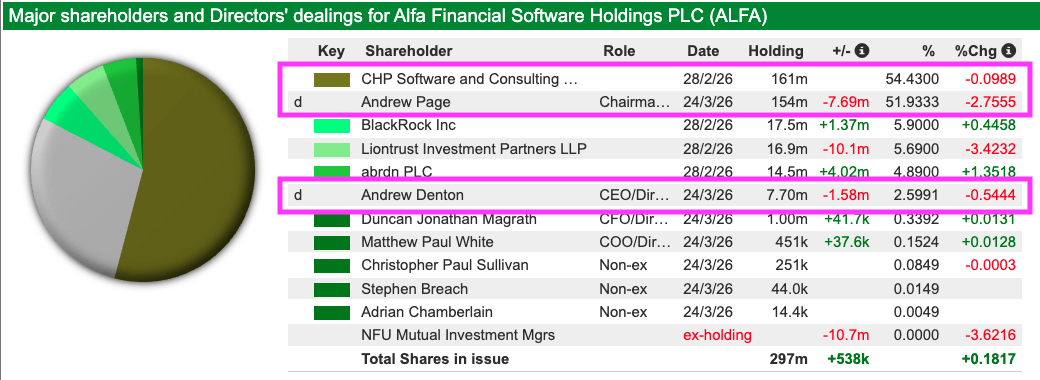

The aforementioned Andrew Page took majority control of Alfa during 2015 and 2016 after his company, CHP Software and Consulting, purchased the 56% combined stakes owned by fellow co-founders Ian Hargrave and Justin Cooper for £54 million.

CHP then sold 28% of its Alfa shareholding at the 2017 flotation and currently retains a 54%/£237 million stake.

ShareScope lists the shareholdings of both CHP and the effective 52%/£226 million stake held by Mr Page through his CHP investment:

Mr Page serves as Alfa’s executive chairman and is accompanied on the board by fellow living-wage director, chief executive Andrew Denton. Mr Denton joined Alfa during 1995, is the minority CHP shareholder and effectively owns a 3%/£11 million Alfa position.

Alfa’s two other executives enjoy much more generous pay packets:

I must add that Messrs Page and Denton did collect £300k-plus salaries up to December 2021, at which point they proposed to earn only the “minimum legal requirement” after expressing “a desire to align their future remuneration with those of the other shareholders“.

I am not quite sure what exactly triggered the decision to earn only the legal minimum, but such severely reduced pay does give the impression the lead executives have a careful eye on wider group salaries and expenditure in general.

Indeed, the large boardroom shareholdings, an eye on costs and the aforementioned run of special dividends do seem to be connected.

Note that Messrs Page and Denton appear open to selling their stakes.

During 2023 and following “a number of unsolicited, non-binding proposals” from EQT, a Swedish private-equity firm, both executives agreed to sell out were Alfa to receive a formal 208p per share bid.

EQT did not table a formal offer, but a few months later, Thomas H Lee Partners, an American private-equity firm, made its own “unsolicited approach“. No potential price was publicly disclosed and Alfa terminated talks a week later.

Just so you know, Messrs Page and Denton did sell 5% of Alfa via CHP during 2024 at 173p (raising £25 million) to “satisfy specific market demand from a single institutional shareholder “.

Mr Page is 63 years old and I do wonder whether he will become more likely to sell down his holding over time. Mr Denton meanwhile is 54 years old and looks set to remain chief executive for the next few years at least.

Valuation and verdict

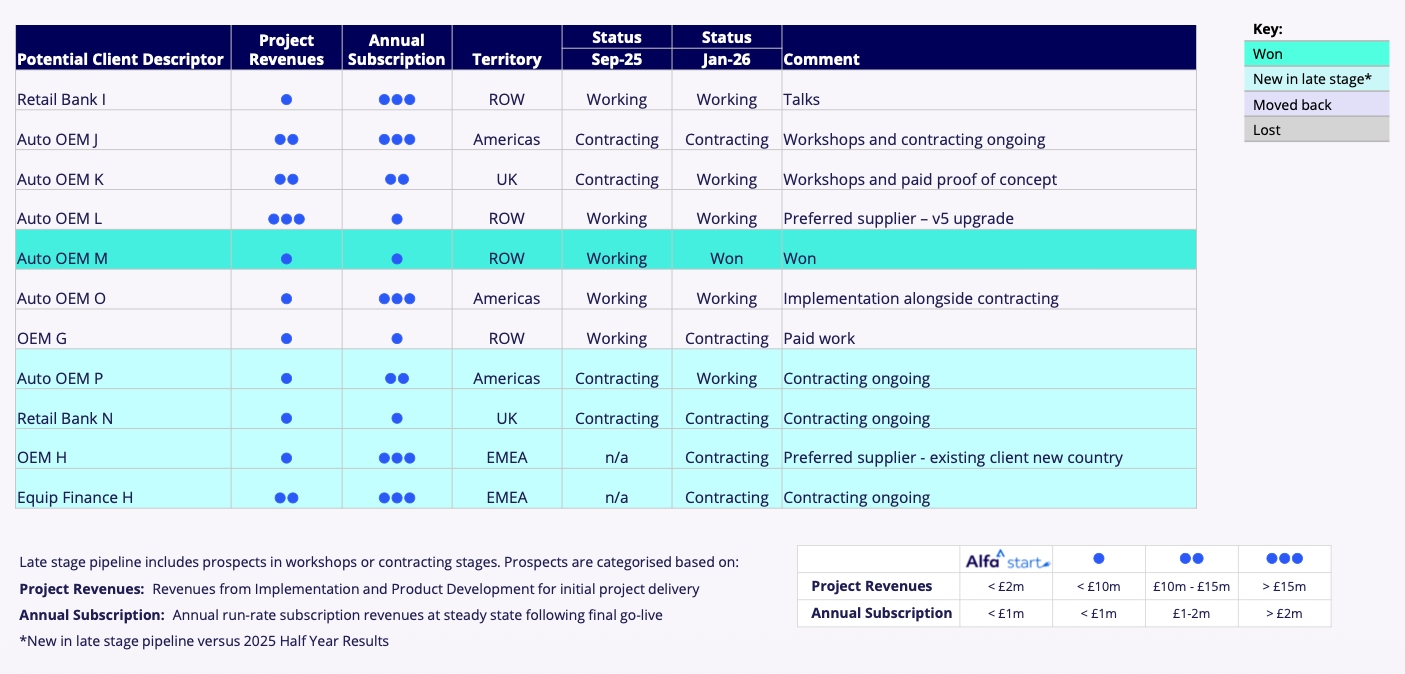

Annual results issued last month showed revenue up 15%, earnings up 17% and a “strong late-stage pipeline” of new customers.

New customers appear vital for Alfa’s future progress and the latest pipeline listed ten active prospects:

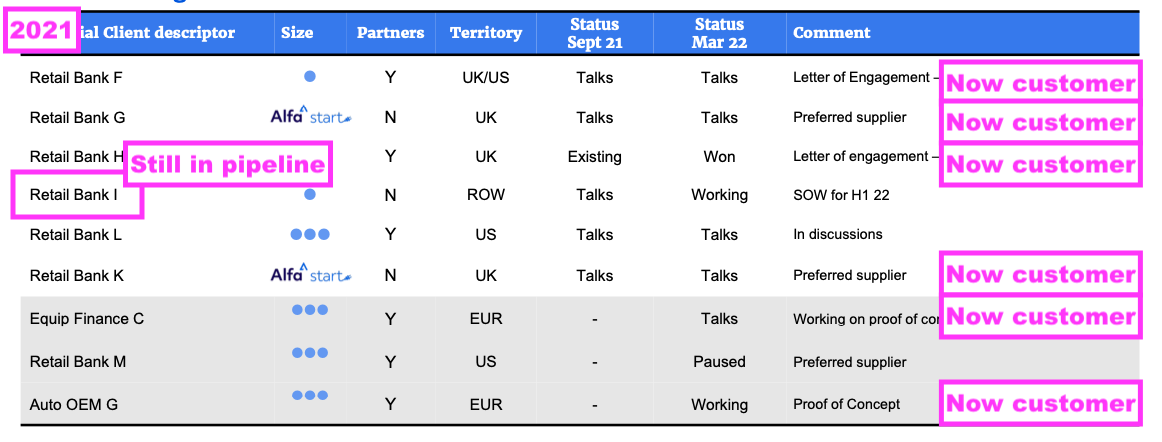

Prospects can take some years to convert into proper customers. Retail Bank I for example has been listed in the late-stage pipeline since 2021:

Although Retail Bank I has not yet converted, six of the other eight prospects from 2021 have become Alfa customers. The other two presumably appointed an alternative supplier.

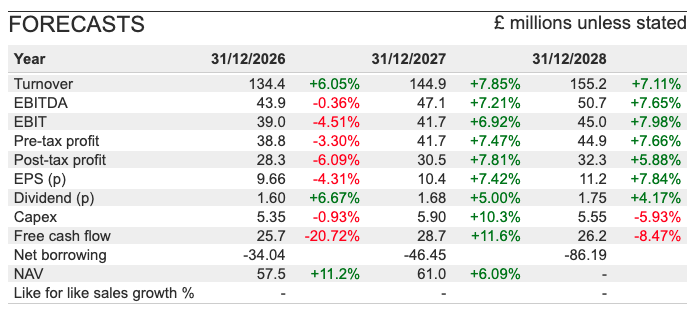

Brokers have translated the late-stage pipeline into the following forecasts:

Alfa’s latest results implied profit for 2026 could be hampered by adverse exchange rates and greater amortisation of the capitalised development costs.

The 2028 projections place the 147p shares on a 13x P/E, which would not appear excessive for a high-margin, high-ROE business that is forecast to expand at a 5-10% annual pace.

Note the 2028 forecasts show net cash having reached £86 million, and I dare say such ‘excess’ cash will in reality be mostly paid out via further special dividends. The extra payouts declared for 2025 came to 8p per share and, if repeated for the next few years, would support a useful 6%-plus ordinary/special income.

I must acknowledge the possible impact of AI on Alfa.

For what it is worth, Alfa first mentioned artificial intelligence within its 2017 annual report…

“Today we are all thinking and talking about digital, artificial intelligence, internet of things and cyber security. The way we did things a couple of years ago will no longer be the way we do it in the future. Demographics and customer priorities are changing and we need to keep listening and changing with them.”

…and today unsurprisingly claims AI will be an “enabler of greater efficiency and customer value” rather than a “disruptor” of the group’s business model.

Alfa believes the implementation of asset-finance software will always be complicated, even for AI:

“Enterprise software implementation projects within highly complex and regulated environments are necessarily huge business change exercises. We see AI increasing implementation efficiency, but not eliminating the process. At Alfa we have an unrivalled track record of delivery of these projects in intricate and interconnected contexts and where competitors consistently struggle. This is a key aspect of our differentiation.”

I suppose customer inertia may also play a part to help ward off AI. After all, two customers remain on version 4, no version 5 customer has yet to switch to an alternative while Retail Bank I has still not signed a full contract after at least four years of late-stage talks.

My best guess is Alfa will cope with any AI onslaught better than most software companies…

…and Messrs Page and Denton will do their utmost to protect their combined £237 million stake… and their living-wage salaries!

Until next time, I wish you safe and healthy investing with ShareScope.

Maynard Paton

Disclosure: Maynard does not own shares in Alfa Financial Software.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Hi Maynard

Thank you for this.

What is your view on actually buying ALFA for yourself? And you reasons, please. (FWIW it is c5% of my family’s portfolio with an average cost of 190p, and I am buying most months)

Regards

Charles

Hi Charles

I write these articles to help readers assess companies for themselves using ShareScope. I raise some salient points and the reader then decides whether or not to research further or dismiss my conjecture. I am not going to tell readers whether to buy, hold or sell, nor I am not going to disclose whether I am likely to buy any share for myself. Given ALFA supports 5% of your family’s portfolio, you should be really telling me what I have missed!!

Maynard