As volatility returns, Value investing is beginning to reassert itself over Growth. Bruce Packard examines the shift, covering MWE, CLX and STX.

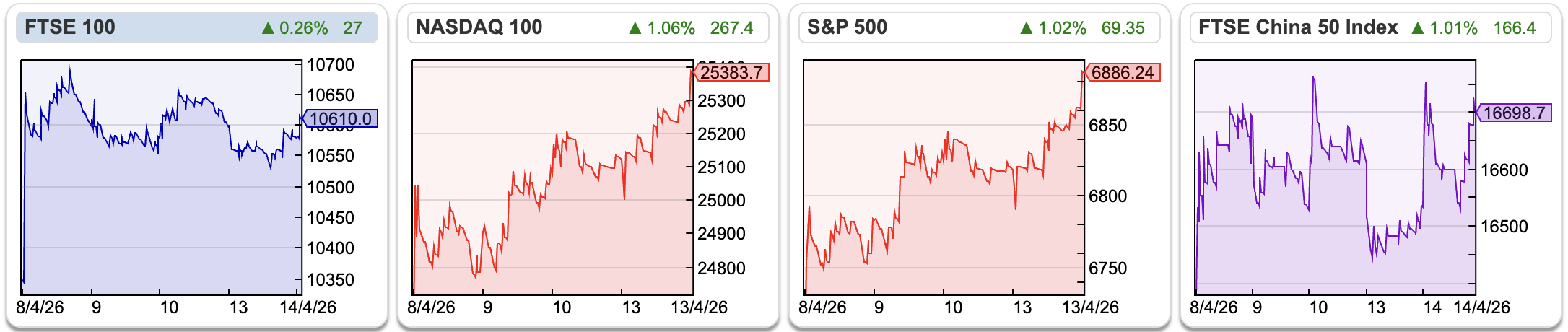

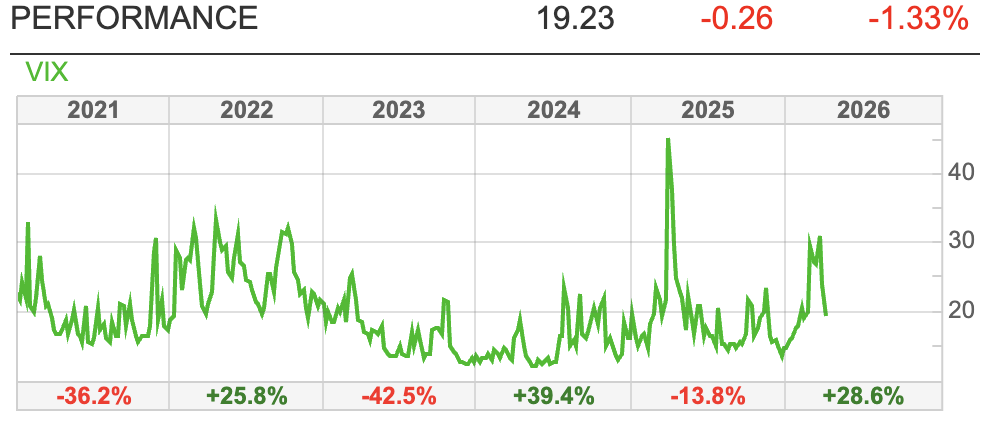

The FTSE 100 rose +2.3% to 10,610 over the last 5 trading days. The Nasdaq100 and S&P500 were up even more strongly, +5.0% and +4.2% respectively. The Vix has fallen below 20. So there’s been a “risk on” rally, without the Straits of Hormuz re-opening. I remain cautious for now, trying to sell my more illiquid, underperforming positions to raise cash to reinvest in the summer/autumn.

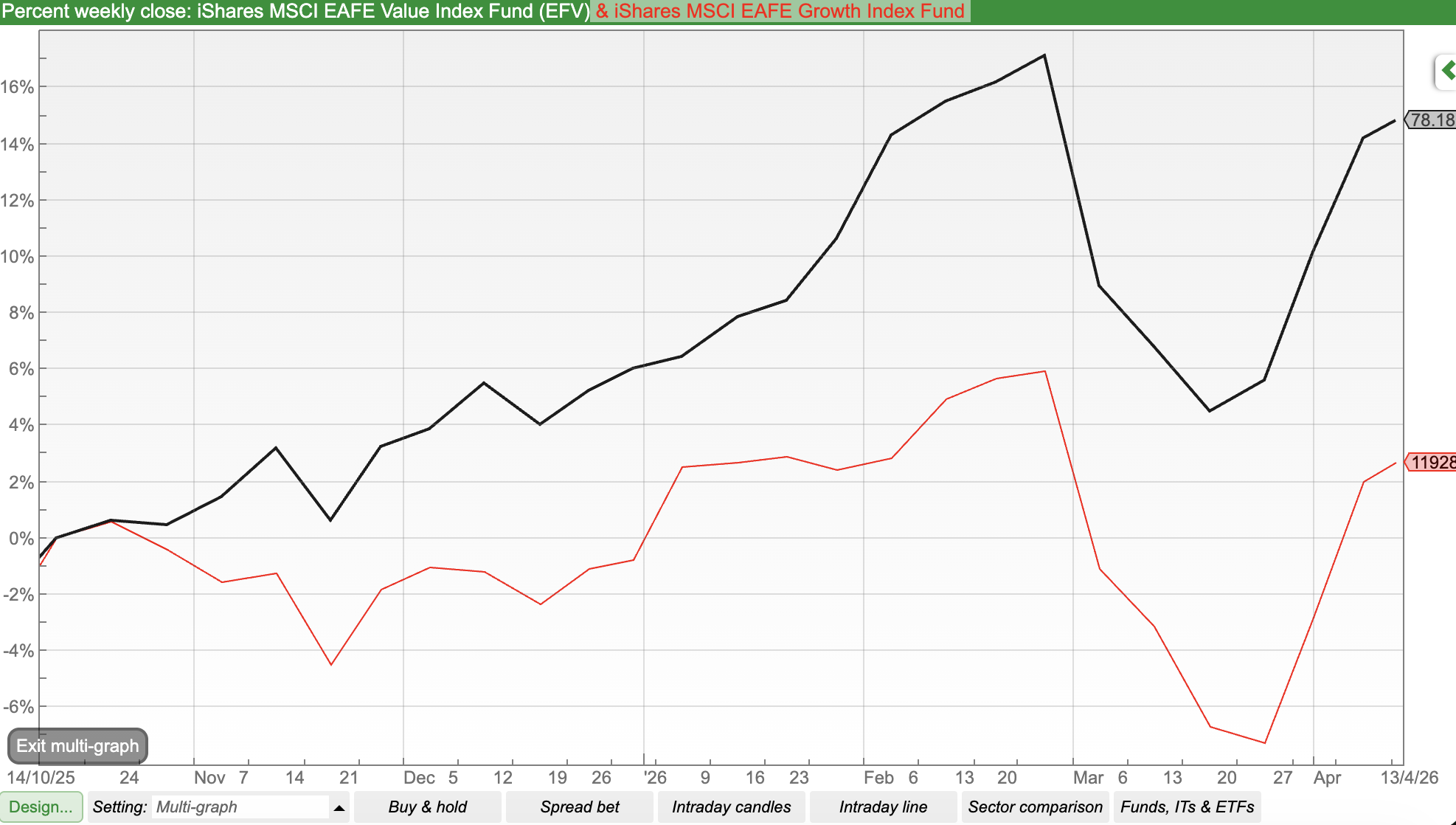

I mostly invest in individual UK shares, but one benefit of ShareScope that I find very useful is the ability to look at various commodities (oil, copper) and ETF indices (MSCI World, TLT 20+ Year US Govt Bond). Below are a couple of charts comparing the MSCI EAFE (Europe, Australasia, and the Far East – that is, developed markets outside the USA) Growth versus Value over different timescales. I show the six month graph, showing that Value (in black) has begun to outperform Growth (in red) then further below the long term chart.

I mostly invest in individual UK shares, but one benefit of ShareScope that I find very useful is the ability to look at various commodities (oil, copper) and ETF indices (MSCI World, TLT 20+ Year US Govt Bond). Below are a couple of charts comparing the MSCI EAFE (Europe, Australasia, and the Far East – that is, developed markets outside the USA) Growth versus Value over different timescales. I show the six month graph, showing that Value (in black) has begun to outperform Growth (in red) then further below the long term chart.

I’m keen to avoid US markets at the moment because I) they’re expensive II) I believe the military adventurism in the Gulf/Trump’s tariffs/AI bubble etc could be the catalyst for US equity market underperformance. Mike Howell has also flagged that liquidity (which fuels the US bull market) is beginning to decline.

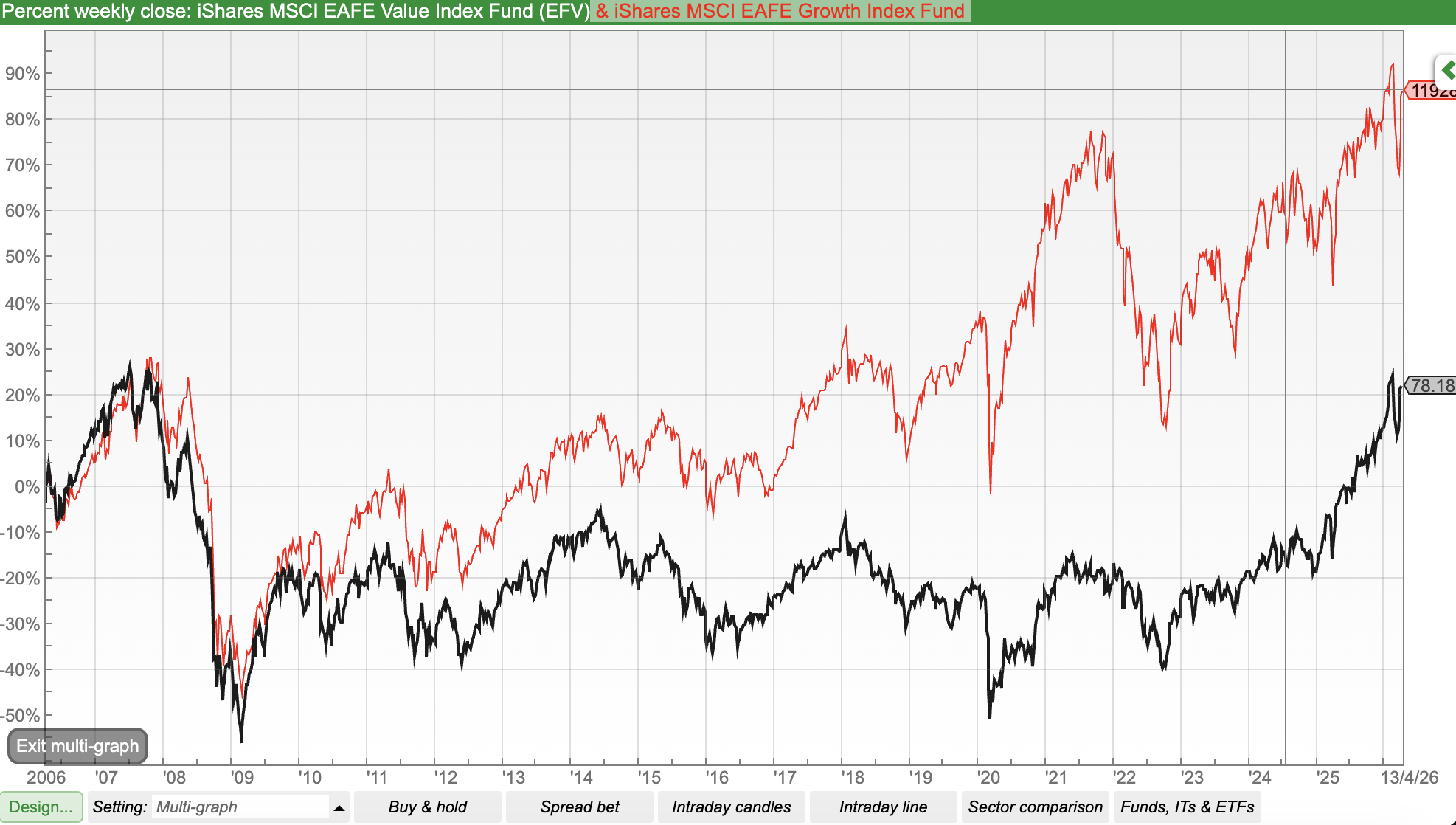

Instead I think the swing from outperformance to underperformance of Growth investing is an interesting theme that UK investors could gain from. Below is the 20 year chart of the same indices, which shows Growth doing very well in the low interest rate, Q.E. market regime, but then Value catching up as inflation returned and interest rates normalised and Central Banks began Q.T..

An irony of Q.E. and low interest rate polices is that they were adopted by Central Bankers because of low growth in developed market economies, and yet these drove the outperformance of Growth investing. Now we are in a stagflationary and volatile environment, Value has begun to outperform.

An irony of Q.E. and low interest rate polices is that they were adopted by Central Bankers because of low growth in developed market economies, and yet these drove the outperformance of Growth investing. Now we are in a stagflationary and volatile environment, Value has begun to outperform.

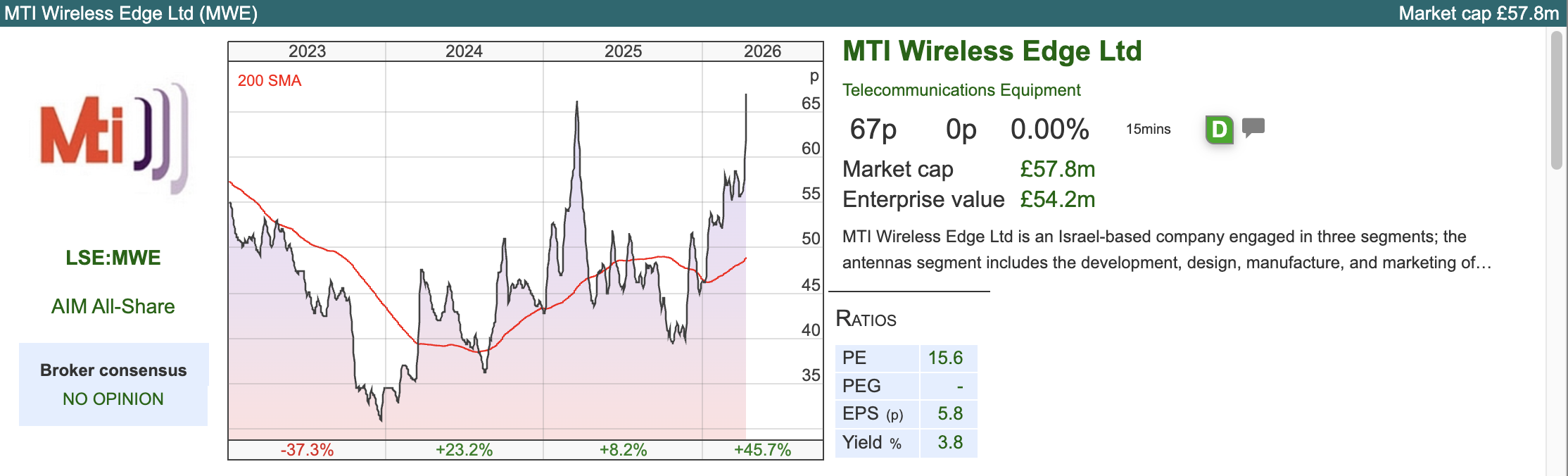

This week I look at two telco equipment companies: MTI Wireless, the Israeli headquartered radio antenna firm, currently announcing contract wins and Calnex Solutions, which also is benefitting from a pick up in capex spending related to defence and data centres. Plus Shield Therapeutics, which has a novel treatment for iron deficiency, previously the share price disappointed but the chart shows it’s now above the 200 day moving.

MTI Wireless Edge Contract Wins

This Israeli headquartered radio frequency company has benefited from increased defence spending, winning orders equivalent to over 10% of FY Dec 2025 annual revenues (which were $52m). They give a split of the orders, i) $2.2m contract to supply communications infrastructure to the Israeli Ministry of Defence; ii) a $1.9m contract to supply military antennas to an international defence company; iii) a US$0.5m contract for military antennas from a local defence company; and iv) additional orders $1.3m again for a defence company. Then at the start of this week, they put out another RNS saying that their antenna division has yet another order for $2m for a local defence company.

This Israeli headquartered radio frequency company has benefited from increased defence spending, winning orders equivalent to over 10% of FY Dec 2025 annual revenues (which were $52m). They give a split of the orders, i) $2.2m contract to supply communications infrastructure to the Israeli Ministry of Defence; ii) a $1.9m contract to supply military antennas to an international defence company; iii) a US$0.5m contract for military antennas from a local defence company; and iv) additional orders $1.3m again for a defence company. Then at the start of this week, they put out another RNS saying that their antenna division has yet another order for $2m for a local defence company.

Looking back the FY Dec results, which cam out a month ago, the Antenna’s division is just under a third of group revenue. It was growing at +11% per year, but military antennas was growing at +50%, and represented around half (so 15% of group) of the division. The other divisions are Water Control & Management, just over a third of revenue, which manages water irrigation for agriculture and was growing at +10%. The third division is Distribution & Professional Consulting Services, which contains MTI Summit and PSK brands, also selling into the defence sector, around 80% of revenue (a quarter of group revenue).

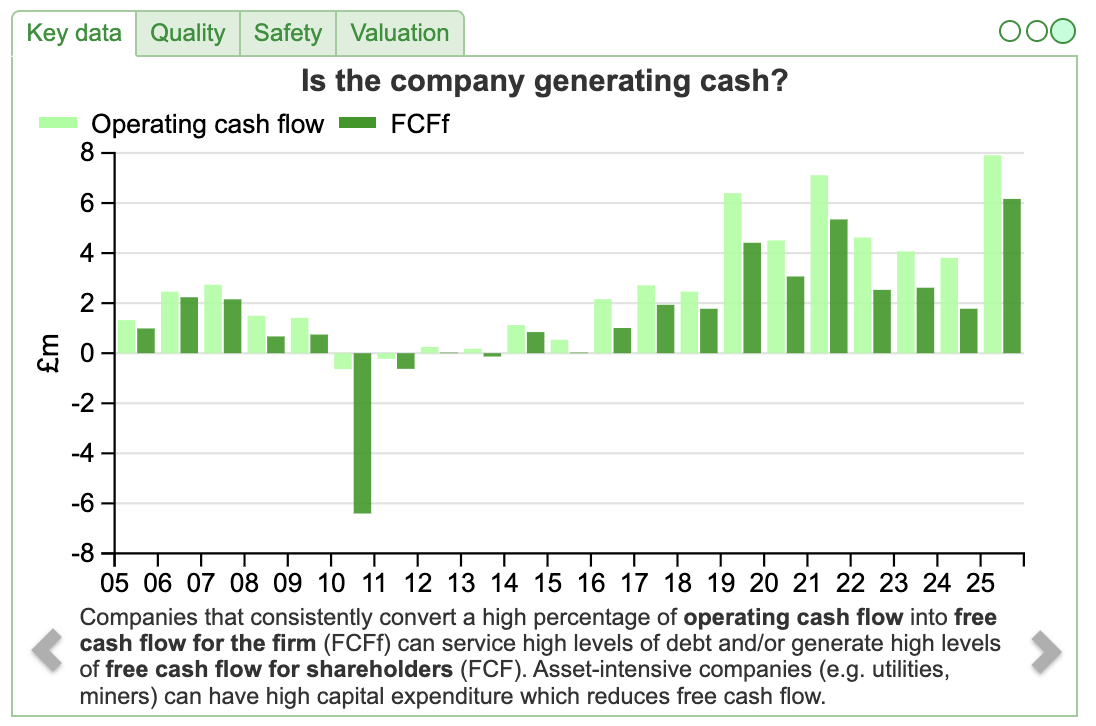

I am normally wary of Israeli groups listed on AIM, but this has been listed on AIM since 2006, which is reassuring. ShareScope also shows (above) that there’s a long history of Free Cash Flow generation too. There are a couple of large blocks of shareholders, including the Borowitz family who own a third. As the founder, Zvi Borowitz died a few months ago, this may create an overhang.

I am normally wary of Israeli groups listed on AIM, but this has been listed on AIM since 2006, which is reassuring. ShareScope also shows (above) that there’s a long history of Free Cash Flow generation too. There are a couple of large blocks of shareholders, including the Borowitz family who own a third. As the founder, Zvi Borowitz died a few months ago, this may create an overhang.

Outlook: Shore Capital, their broker, published a research note after the announcement, but didn’t upgrade EPS forecasts ($c5.8 FY Dec 2026F and $c6.0 FY Dec 2027F). It is early in the year, so perhaps we should see upward pressure on forecasts in a couple of months, or the Water Control division is struggling.

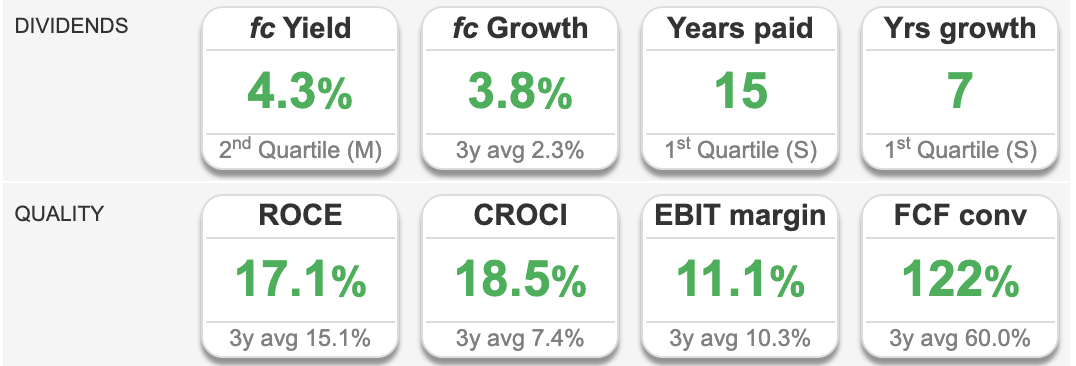

Valuation: The shares are trading on 15x Dec 2026F, dropping to 14x the following year. The EV/EBITDA is 9x 2026F. ShareScope’s quality indicators are positive.

Opinion: I like it. Good track record of profitable growth trading on a reasonable multiple. The one negative is that the shares are up almost +50% YTD, so it’s possible that were chasing the investment case higher when profitability is close to a cyclical peak and there’s potentially a large block of shares that might be sold. The valuation isn’t expensive though, and there does seem to be upward pressure on forecasts, with all the contract win announcements.

Opinion: I like it. Good track record of profitable growth trading on a reasonable multiple. The one negative is that the shares are up almost +50% YTD, so it’s possible that were chasing the investment case higher when profitability is close to a cyclical peak and there’s potentially a large block of shares that might be sold. The valuation isn’t expensive though, and there does seem to be upward pressure on forecasts, with all the contract win announcements.

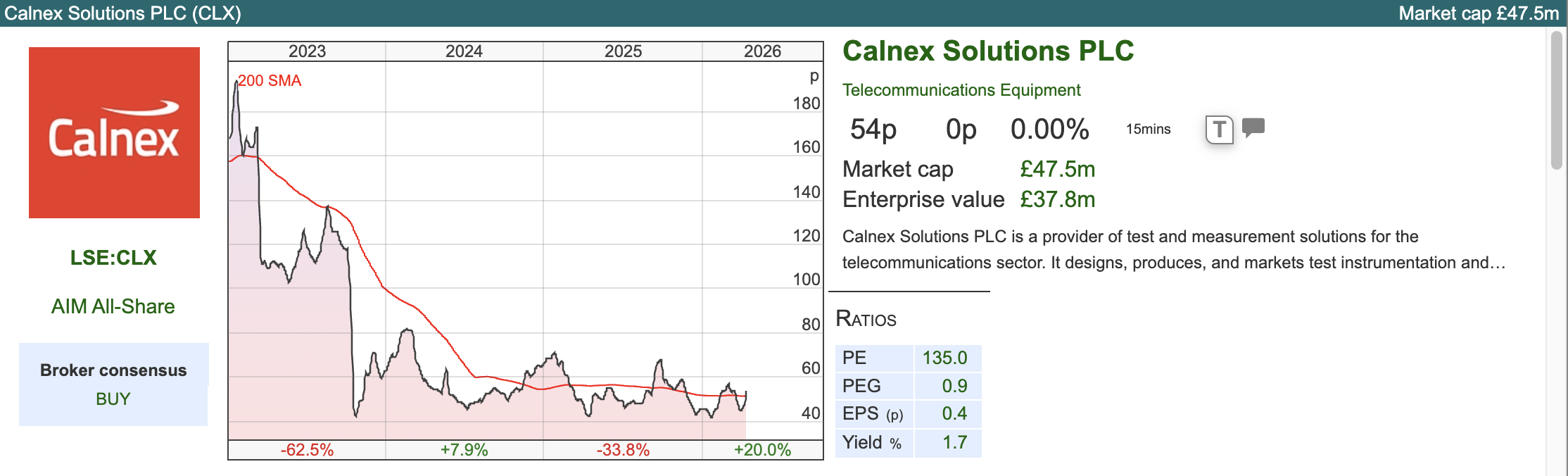

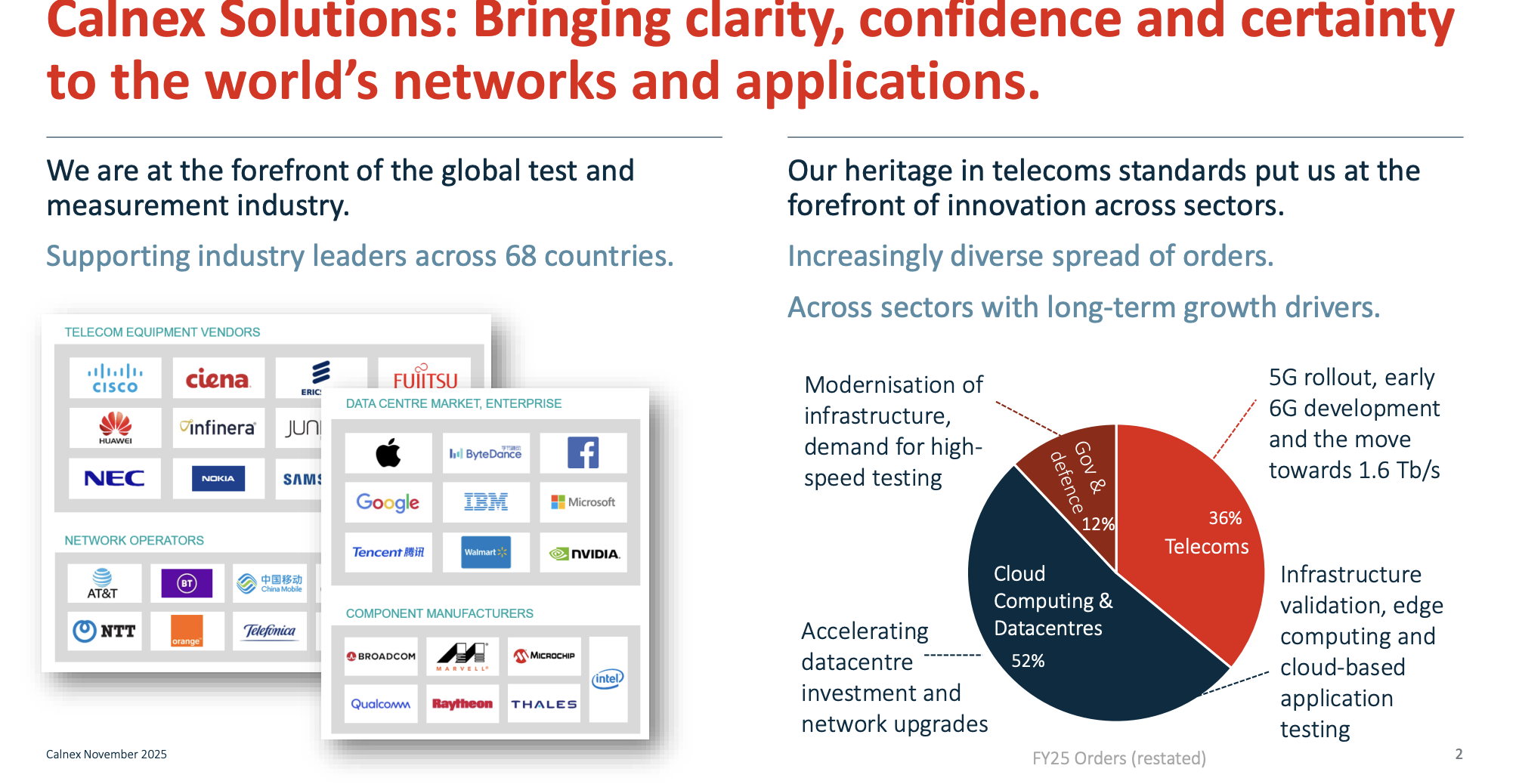

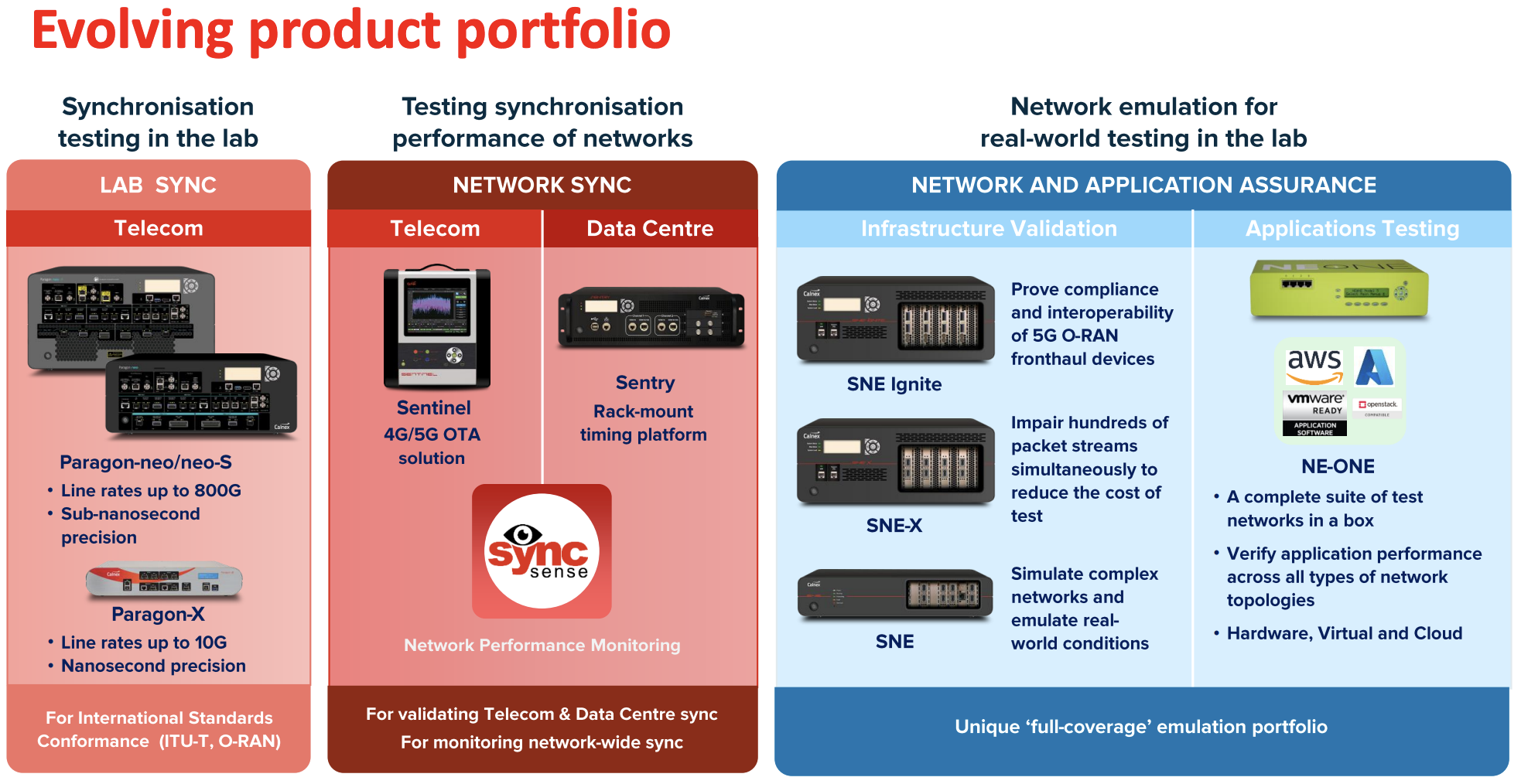

Calnex Solutions FY Mar 2026F Ahead Trading Update

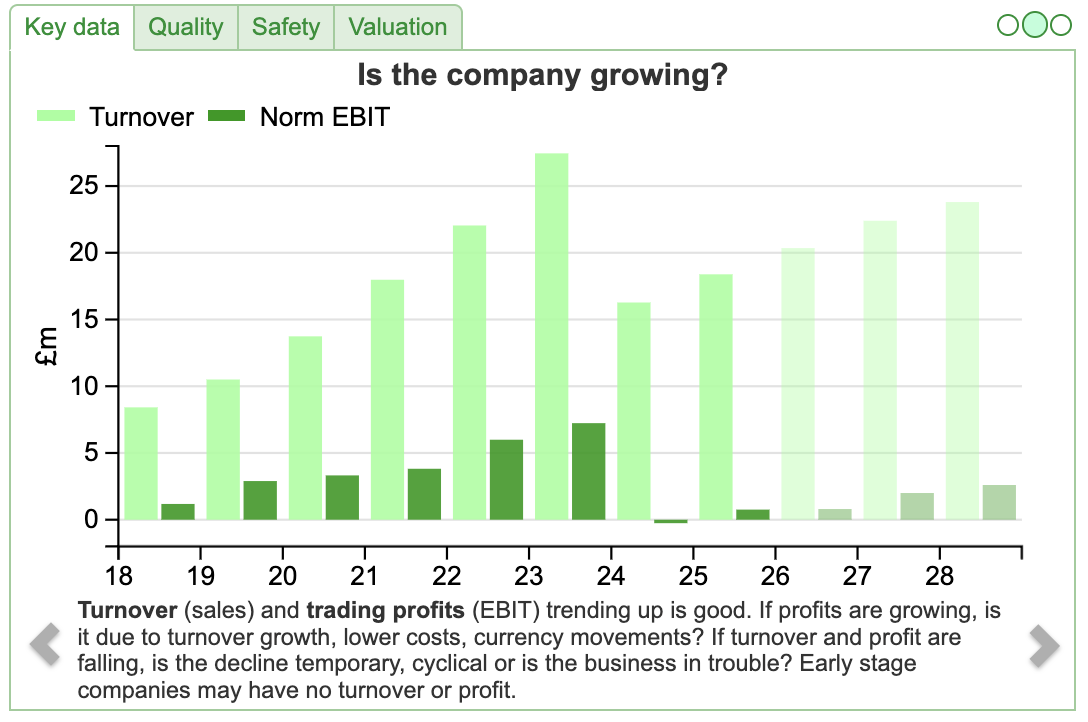

This telecoms equipment testing group was a 2020 IPO, doing well through the pandemic then coming unstuck with a nasty profit warning in late 2023. Maynard did flag that a simple comparison between the profitability reported within Calnex’s flotation document and the profitability reported within the original accounts filed at Companies House revealed some notable discrepancies.

That was a useful red flag. To be clear, window dressing the financial numbers for the IPO didn’t cause the 2023 profit warning, as customers took a more cautious approach to capex decisions. Instead Maynard’s article highlighted poor voluntary disclosure choices by management that were an early indicator that the investment case had been somewhat finessed for public markets. The situation now seems to have improved, with Calnex’s reporting a “slightly ahead” RNS for FY Mar 2026F, +19% revenue growth to £22m and improved profitability. Net cash is £9m.

Outlook: The RNS mentions a couple of Calnex products that could benefit from all the investment going into AI datacentres, suggesting that they are well placed for growth. Cavendish, their broker, have increased their FY Mar 2026F EPS forecast by 60% to 1.06p. They’ve also introduced Mar 2027F and 2028F forecasts, implying +19% and +54% EPS growth.

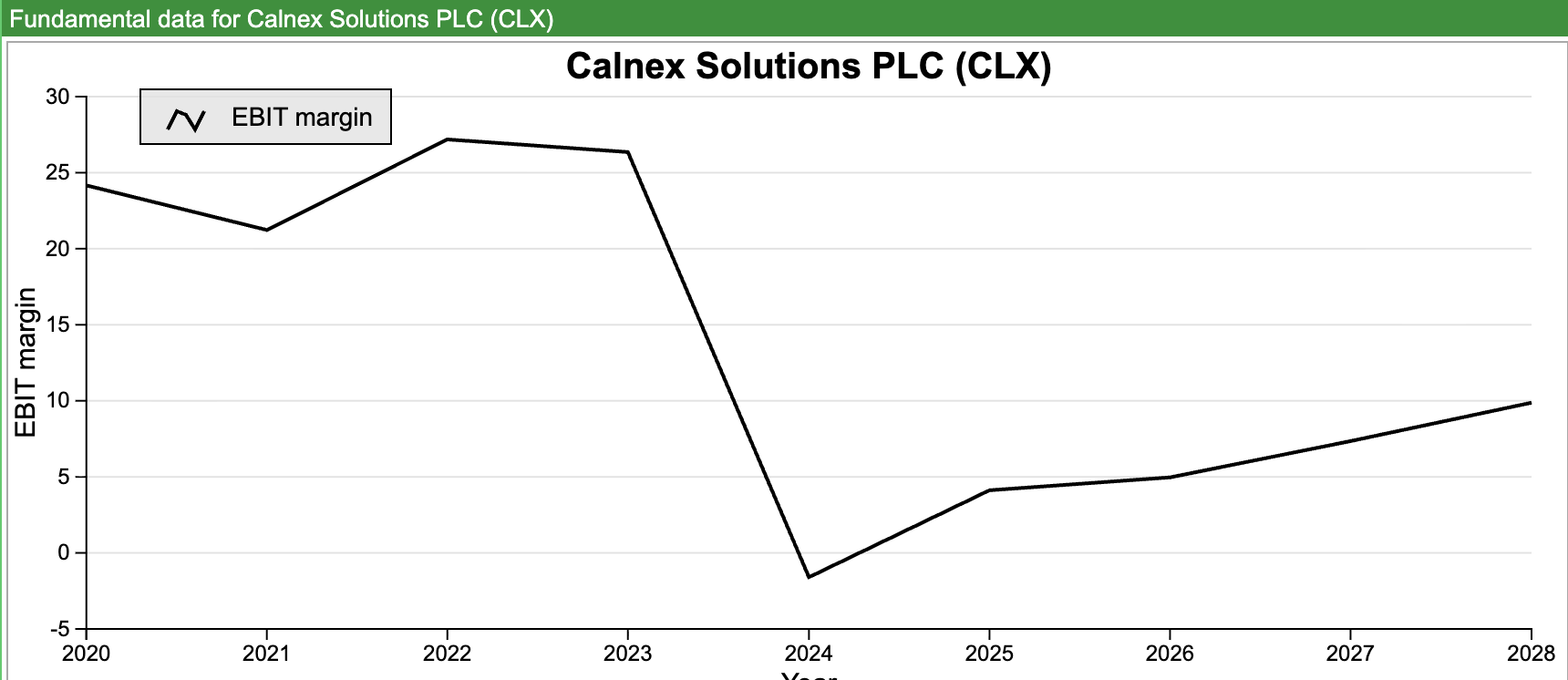

Valuation: The shares are trading on a PER of 47x Mar 2027F, falling to 30x 2028F. On those kind of numbers you could argue that the recovery is already priced in. ShareScope shows that historically the EBIT margin was around 25% though, whereas it only recovers to 10% during the forecast period. If we assume that the margin can recover to the 2020-23 average, then the PER multiple is in the low teens.

Valuation: The shares are trading on a PER of 47x Mar 2027F, falling to 30x 2028F. On those kind of numbers you could argue that the recovery is already priced in. ShareScope shows that historically the EBIT margin was around 25% though, whereas it only recovers to 10% during the forecast period. If we assume that the margin can recover to the 2020-23 average, then the PER multiple is in the low teens.

Opinion: This looks to be in an exciting area, benefiting from AI datacentres and also defence spending. There seems to be good visibility over the next couple of years, but presumably capex spending might slow at some point, so I’m not sure what multiple investors should be willing to pay. Yet another pandemic era IPO that has disappointed, but now worth revisiting the investment case and worth a second look?

Shield Therapeutics FY Dec 2025 Results

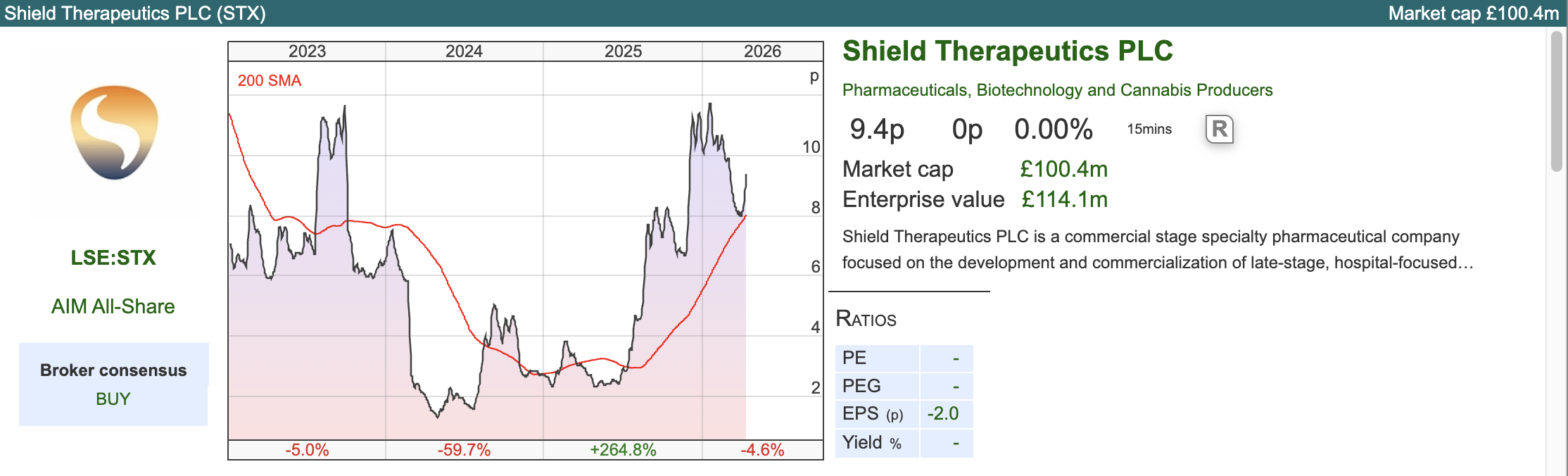

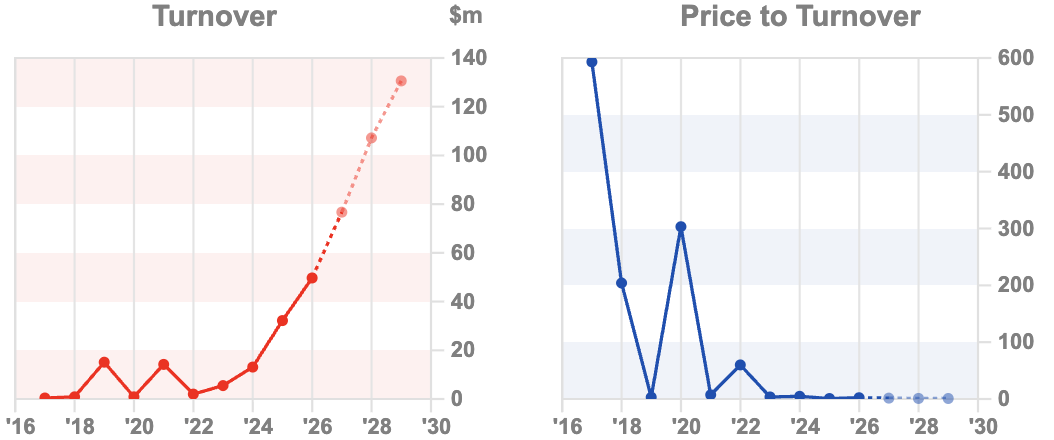

This pharma group has a product ACCRUFeR® that is a treatment for iron deficiency. It did very well 10-bagging just before the pandemic, because it had a good story. The potential market size is $2.3bn for treating iron deficiency, so you can see why investors were excited. Financial results then disappointed and the share price fell -99%. More recently Michael Taylor flagged the chart 6-12 months ago as being in the early stages of a recovery, which was a good call. Last week the group announced ACCRUFeR® record prescription volumes, increased average net selling prices, and record revenues of $49m FY Dec 2025.

This pharma group has a product ACCRUFeR® that is a treatment for iron deficiency. It did very well 10-bagging just before the pandemic, because it had a good story. The potential market size is $2.3bn for treating iron deficiency, so you can see why investors were excited. Financial results then disappointed and the share price fell -99%. More recently Michael Taylor flagged the chart 6-12 months ago as being in the early stages of a recovery, which was a good call. Last week the group announced ACCRUFeR® record prescription volumes, increased average net selling prices, and record revenues of $49m FY Dec 2025.

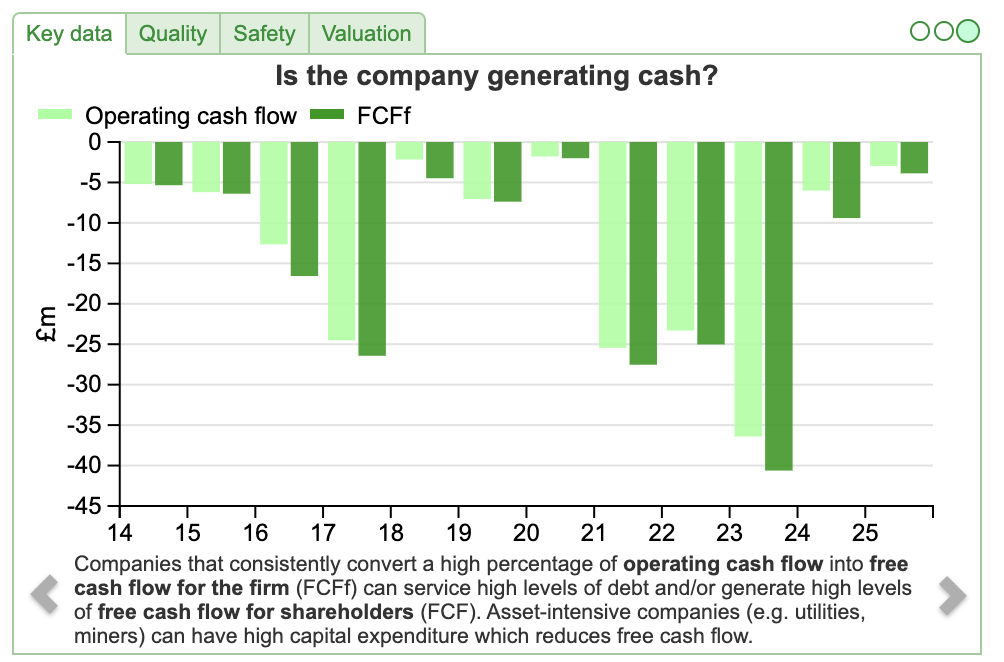

That $49m represents +54% sales growth versus the previous year. The group is still loss making, $17m (down from $26m FY Dec 2024). If anything those loses understate financial performance, as management capitalise some R&D expense on to their balance sheet ($19m of intangible assets), which reduces the costs expensed through the p&l. Sharescope shows that the company hasn’t been generating cash, yet the FCFf and Operating cash flow have improved from deeply negative in the last couple of years towards breakeven. Hopefully that improving trend can continue into the future.

Management raised $12m of equity in December 2024 at 3p, mostly from AOP, a Vienna headquartered healthcare stock with revenues of over €250m. AOP currently owns 54% of the shares, so they might make an offer to buy out the minorities now performance has improved. Tedi Sagi had a similar percentage holding in KAPE, using UK investors to fund the growth and then declaring that AIM was undervaluing the company (not least because Kape was persistently issuing new shares and Tedi was a majority shareholder!) and then taking the VPN/cyber security private on a PER multiple of around 5x. I think this situation is different, but wanted to flag that as a risk to the Shield investment case.

Management raised $12m of equity in December 2024 at 3p, mostly from AOP, a Vienna headquartered healthcare stock with revenues of over €250m. AOP currently owns 54% of the shares, so they might make an offer to buy out the minorities now performance has improved. Tedi Sagi had a similar percentage holding in KAPE, using UK investors to fund the growth and then declaring that AIM was undervaluing the company (not least because Kape was persistently issuing new shares and Tedi was a majority shareholder!) and then taking the VPN/cyber security private on a PER multiple of around 5x. I think this situation is different, but wanted to flag that as a risk to the Shield investment case.

Annoyingly STX doesn’t report a net debt figure. The highlight $11.6m of cash at the end of Dec last year, rising to $12.4m end of March this year. However there’s $30m of loans and milestone financing, which implies net debt of $18.5m. Worth noting the +63% jump in payables to $37.4m in the current liabilities. So although cashflow was positive in Q4 last year and Q1 this year and this doesn’t look like it’s going to run out of money, some of that was $4.8m positive working capital movement which isn’t sustainable.

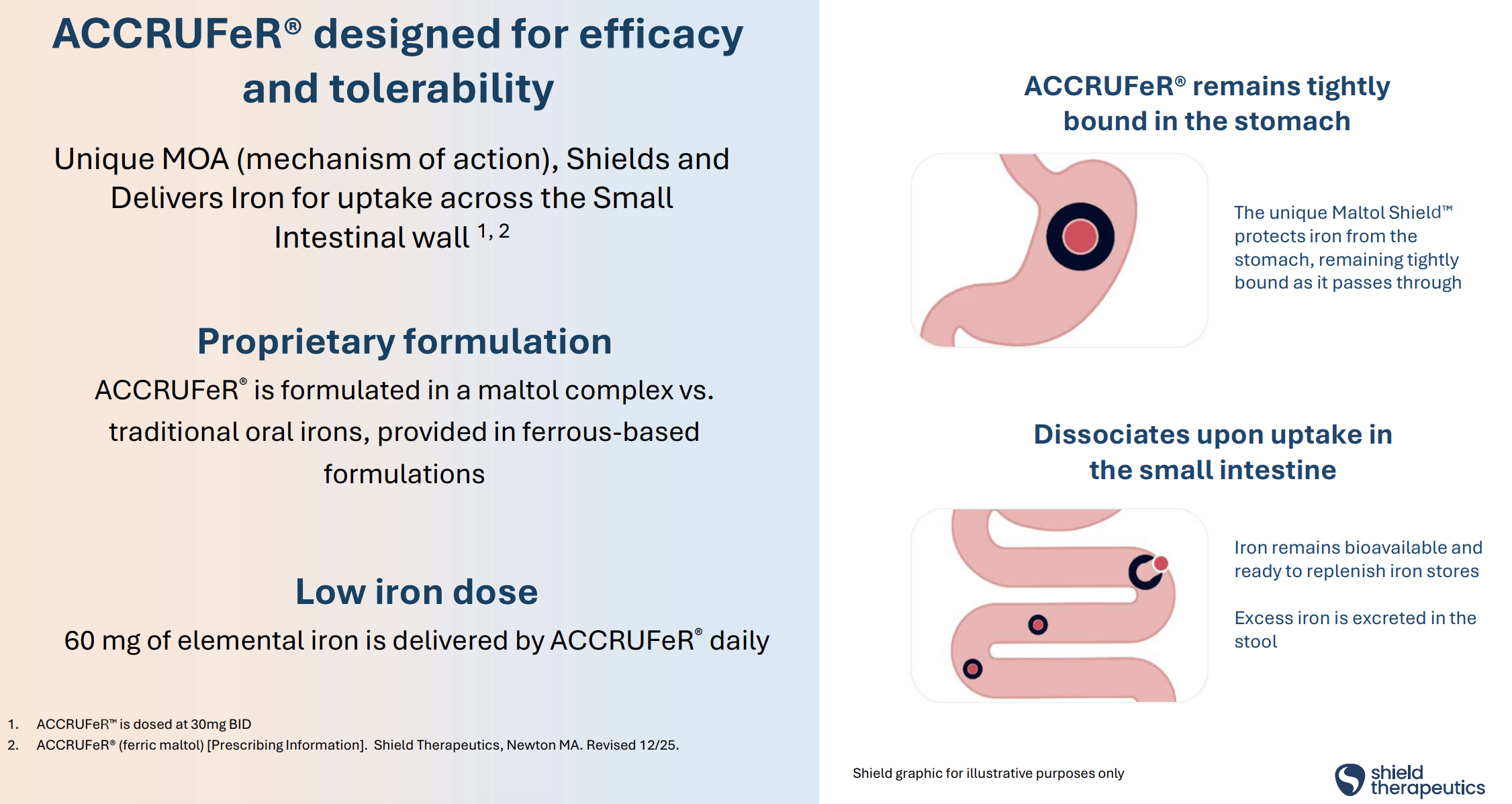

Iron Deficiency: I had an aunt who was advised by her doctor to drink a pint of Guinness a day to treat iron deficiency. That’s now been debunked as a treatment (great marketing though!) 14m individuals diagnosed with the deficiency in the US, probably another 10m undiagnosed. The body lacks the iron to make haemoglobin, which carries oxygen around your body, resulting in tiredness, pale skin, shortness of breath and brain fog. You would think simple tablets containing iron would counter this, however up to 60% of patients develop gastrointestinal (ie stomach) problems. Shield Therapeutics ACCRUFeR® is much better tolerated across the small intestinal wall.

Iron Deficiency: I had an aunt who was advised by her doctor to drink a pint of Guinness a day to treat iron deficiency. That’s now been debunked as a treatment (great marketing though!) 14m individuals diagnosed with the deficiency in the US, probably another 10m undiagnosed. The body lacks the iron to make haemoglobin, which carries oxygen around your body, resulting in tiredness, pale skin, shortness of breath and brain fog. You would think simple tablets containing iron would counter this, however up to 60% of patients develop gastrointestinal (ie stomach) problems. Shield Therapeutics ACCRUFeR® is much better tolerated across the small intestinal wall.

ACCRUFeR®is approved by the FDA in the USA for patients 10 years old and over. Regulatory approval has been granted in Korea, they are making progress in China and phase II trials in Japan and a partnership with Norgine in Europe.

ACCRUFeR®is approved by the FDA in the USA for patients 10 years old and over. Regulatory approval has been granted in Korea, they are making progress in China and phase II trials in Japan and a partnership with Norgine in Europe.

Outlook: Cavendish, their broker, have revenue growing +60% in FY Dec 2026F, but the group still making a $5m adj PBT loss. The company hasn’t given them enough confidence to forecast further out than that.

Valuation: The shares are trading on 1.4x Dec 2026F sales. I’m not sure what margin we might expect the group to make as the business scales, but that p/sales multiple doesn’t look demanding. Sharescope also has EV/EBITDA Dec 2026F of 7x, which also seems like an attractive entry point for a rapidly growing company with large Total Addressable Market (TAM).

Opinion: Still rather speculative, but I think this could continue to reward shareholders. You’re never going to call the bottom on these type of situations. However, there’s plenty still go for, despite the shares bouncing strongly from their low below 2p two years ago. I think the investment case makes sense as part of a diversified portfolio.

Bruce Packard

@bruce_packard

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Bi-Weekly Market Commentary | 15/04/2026 | MWE, CLX, STX | Value in volatile times

As volatility returns, Value investing is beginning to reassert itself over Growth. Bruce Packard examines the shift, covering MWE, CLX and STX.

The FTSE 100 rose +2.3% to 10,610 over the last 5 trading days. The Nasdaq100 and S&P500 were up even more strongly, +5.0% and +4.2% respectively. The Vix has fallen below 20. So there’s been a “risk on” rally, without the Straits of Hormuz re-opening. I remain cautious for now, trying to sell my more illiquid, underperforming positions to raise cash to reinvest in the summer/autumn.

I’m keen to avoid US markets at the moment because I) they’re expensive II) I believe the military adventurism in the Gulf/Trump’s tariffs/AI bubble etc could be the catalyst for US equity market underperformance. Mike Howell has also flagged that liquidity (which fuels the US bull market) is beginning to decline.

Instead I think the swing from outperformance to underperformance of Growth investing is an interesting theme that UK investors could gain from. Below is the 20 year chart of the same indices, which shows Growth doing very well in the low interest rate, Q.E. market regime, but then Value catching up as inflation returned and interest rates normalised and Central Banks began Q.T..

This week I look at two telco equipment companies: MTI Wireless, the Israeli headquartered radio antenna firm, currently announcing contract wins and Calnex Solutions, which also is benefitting from a pick up in capex spending related to defence and data centres. Plus Shield Therapeutics, which has a novel treatment for iron deficiency, previously the share price disappointed but the chart shows it’s now above the 200 day moving.

MTI Wireless Edge Contract Wins

Looking back the FY Dec results, which cam out a month ago, the Antenna’s division is just under a third of group revenue. It was growing at +11% per year, but military antennas was growing at +50%, and represented around half (so 15% of group) of the division. The other divisions are Water Control & Management, just over a third of revenue, which manages water irrigation for agriculture and was growing at +10%. The third division is Distribution & Professional Consulting Services, which contains MTI Summit and PSK brands, also selling into the defence sector, around 80% of revenue (a quarter of group revenue).

Outlook: Shore Capital, their broker, published a research note after the announcement, but didn’t upgrade EPS forecasts ($c5.8 FY Dec 2026F and $c6.0 FY Dec 2027F). It is early in the year, so perhaps we should see upward pressure on forecasts in a couple of months, or the Water Control division is struggling.

Valuation: The shares are trading on 15x Dec 2026F, dropping to 14x the following year. The EV/EBITDA is 9x 2026F. ShareScope’s quality indicators are positive.

Calnex Solutions FY Mar 2026F Ahead Trading Update

This telecoms equipment testing group was a 2020 IPO, doing well through the pandemic then coming unstuck with a nasty profit warning in late 2023. Maynard did flag that a simple comparison between the profitability reported within Calnex’s flotation document and the profitability reported within the original accounts filed at Companies House revealed some notable discrepancies.

That was a useful red flag. To be clear, window dressing the financial numbers for the IPO didn’t cause the 2023 profit warning, as customers took a more cautious approach to capex decisions. Instead Maynard’s article highlighted poor voluntary disclosure choices by management that were an early indicator that the investment case had been somewhat finessed for public markets. The situation now seems to have improved, with Calnex’s reporting a “slightly ahead” RNS for FY Mar 2026F, +19% revenue growth to £22m and improved profitability. Net cash is £9m.

Outlook: The RNS mentions a couple of Calnex products that could benefit from all the investment going into AI datacentres, suggesting that they are well placed for growth. Cavendish, their broker, have increased their FY Mar 2026F EPS forecast by 60% to 1.06p. They’ve also introduced Mar 2027F and 2028F forecasts, implying +19% and +54% EPS growth.

Opinion: This looks to be in an exciting area, benefiting from AI datacentres and also defence spending. There seems to be good visibility over the next couple of years, but presumably capex spending might slow at some point, so I’m not sure what multiple investors should be willing to pay. Yet another pandemic era IPO that has disappointed, but now worth revisiting the investment case and worth a second look?

Shield Therapeutics FY Dec 2025 Results

That $49m represents +54% sales growth versus the previous year. The group is still loss making, $17m (down from $26m FY Dec 2024). If anything those loses understate financial performance, as management capitalise some R&D expense on to their balance sheet ($19m of intangible assets), which reduces the costs expensed through the p&l. Sharescope shows that the company hasn’t been generating cash, yet the FCFf and Operating cash flow have improved from deeply negative in the last couple of years towards breakeven. Hopefully that improving trend can continue into the future.

Annoyingly STX doesn’t report a net debt figure. The highlight $11.6m of cash at the end of Dec last year, rising to $12.4m end of March this year. However there’s $30m of loans and milestone financing, which implies net debt of $18.5m. Worth noting the +63% jump in payables to $37.4m in the current liabilities. So although cashflow was positive in Q4 last year and Q1 this year and this doesn’t look like it’s going to run out of money, some of that was $4.8m positive working capital movement which isn’t sustainable.

Outlook: Cavendish, their broker, have revenue growing +60% in FY Dec 2026F, but the group still making a $5m adj PBT loss. The company hasn’t given them enough confidence to forecast further out than that.

Valuation: The shares are trading on 1.4x Dec 2026F sales. I’m not sure what margin we might expect the group to make as the business scales, but that p/sales multiple doesn’t look demanding. Sharescope also has EV/EBITDA Dec 2026F of 7x, which also seems like an attractive entry point for a rapidly growing company with large Total Addressable Market (TAM).

Opinion: Still rather speculative, but I think this could continue to reward shareholders. You’re never going to call the bottom on these type of situations. However, there’s plenty still go for, despite the shares bouncing strongly from their low below 2p two years ago. I think the investment case makes sense as part of a diversified portfolio.

Bruce Packard

@bruce_packard

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.