ME Group issued a profit warning the other week and its shares now trade close to their 52-week low. Maynard Paton reviews the photobooth operator’s diversification into washing machines, its family-run boardroom and some slapdash financial reporting.

Shares trading close to their 52-week lows can often provide lucrative buying opportunities for contrarian investors.

In particular, promising companies that appear temporarily out of favour can generate very worthwhile returns as and when profits recover and the market re-rates the share price.

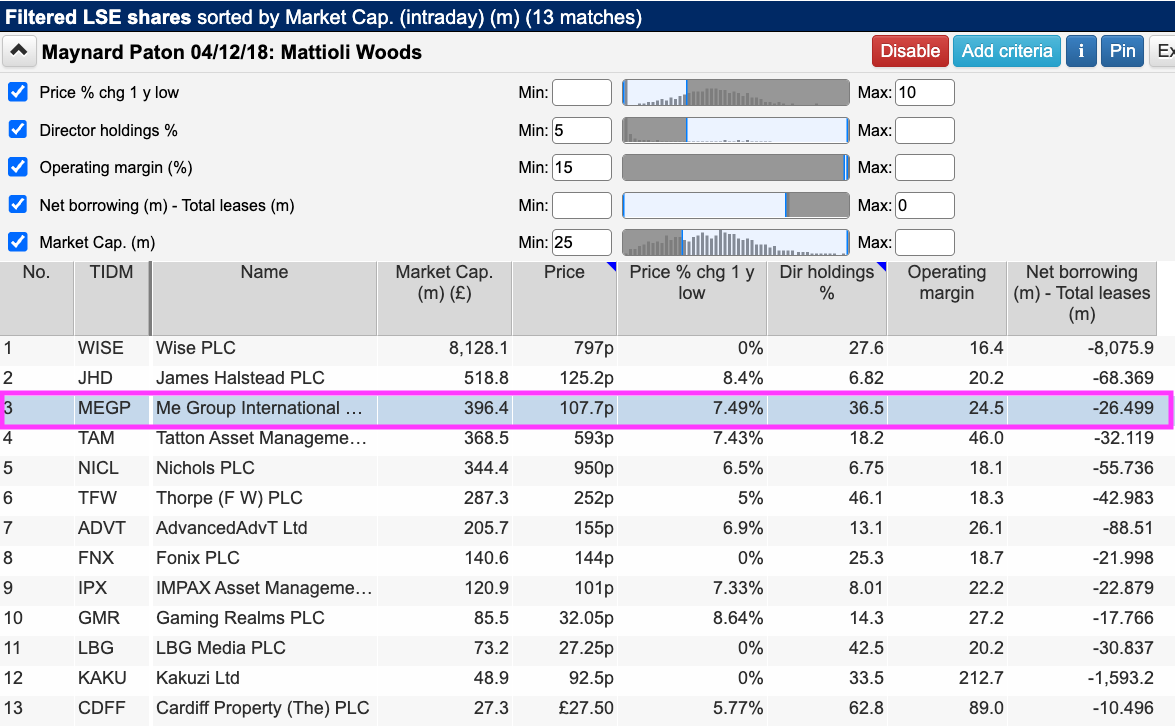

The other day ShareScope revealed some 458 names trading within 10% of their 52-week lows, with further filtering to find only ‘promising companies’ narrowing the list down to 13:

(You can run this screen for yourself by selecting the “Maynard Paton 04/12/18: Mattioli Woods” filter within ShareScope’s marvellous Filter Library. My instructions show you how.)

The exact screening criteria I redeployed were:

- A share price within 10% of its 52-week low;

- Director ownership of at least 5%;

- An operating margin of 15% or more;

- Net borrowings less total leases of no more than 0 (i.e. a net cash position excluding IFRS 16 lease obligations), and;

- A minimum market cap of £25m.

Among the shortlisted shares were James Halstead, Tatton Asset Management, Fonix and Impax Asset Management.

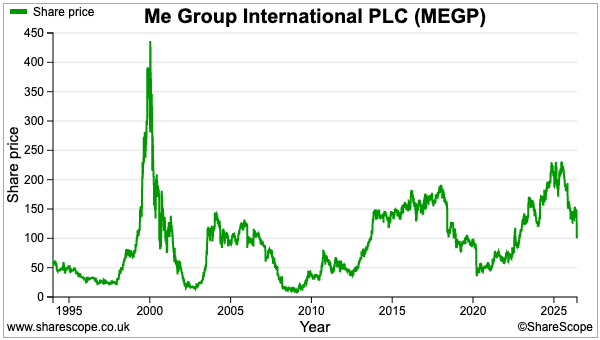

I selected ME Group because this company has for years popped up on my various ShareScope filters and coverage had become very overdue. A recent profit warning meanwhile established a new 52-week low at 100p:

Let’s take a closer look.

Introducing ME Group

“Back in 1981, I had the idea of express photo processing. At that time it took around a week to develop a photo using enormous machines. I did not know anything about developing photos, so we started with the idea for a completely innovative system, which was really successful. We showcased it for the first time at the Photography Show in Paris, in November 1981. Everyone laughed, thinking it was a joke.

We worked with an American factory in Somerset and with [our] Grenoble factory to manufacture 1,000 minilabs a month, made to order. Back then, the minilabs were selling at $50,000 each. We reduced the [photo processing] time from 8 days to one hour then to just 30 minutes.”

So recounted Serge Crasnianski during this Youtube interview about how he led the development of the world’s first photo ‘minilab‘ and established the concept of ‘one hour photo processing’.

The success of Mr Crasnianski’s minilabs — and before that his automatic key-cutting machines — eventually led to his business, KIS Photo Industrie, taking a 20% stake in Photo-Me International during 1990.

Photo-Me then merged with KIS during 1994 to take advantage of the latter’s new digital photobooths. Photo-Me launched is first photobooth during 1954 and, following government approval during 1966, the group’s booths have been synonymous with passport photos ever since:

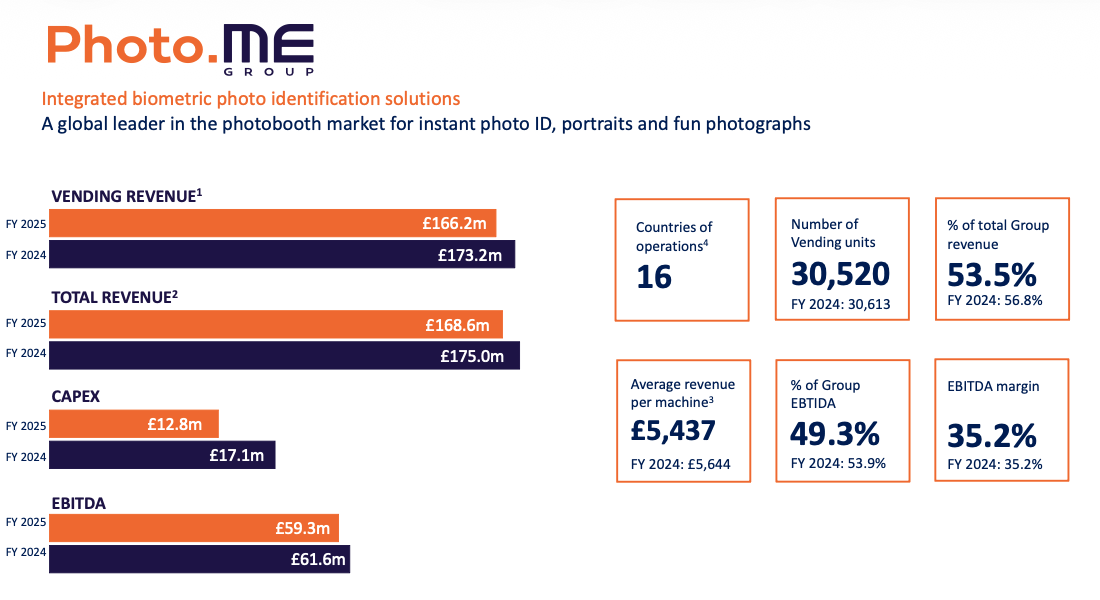

Following various acquisitions throughout the last three decades (and changing its name from Photo-Me to ME Group during 2022), the business today operates more than 30,000 photobooths throughout the UK, Europe and Asia:

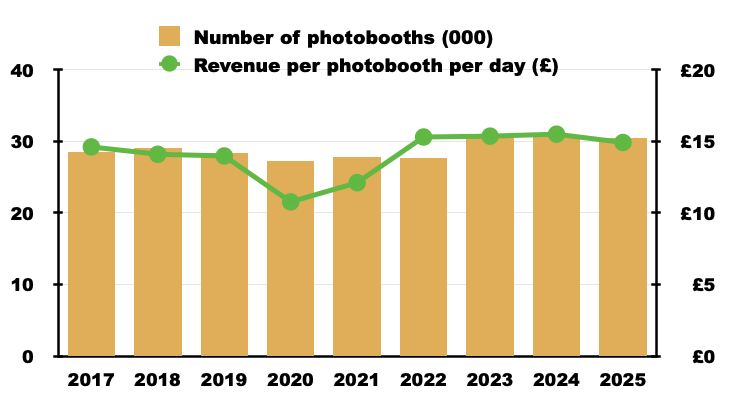

Perhaps emphasising how photobooths have long since passed their heyday, vending revenue per booth last year was approximately £5,400 — equivalent to less than £15 a day. Aside from the pandemic, revenue per booth has stayed at approximately £15 a day since at least 2017:

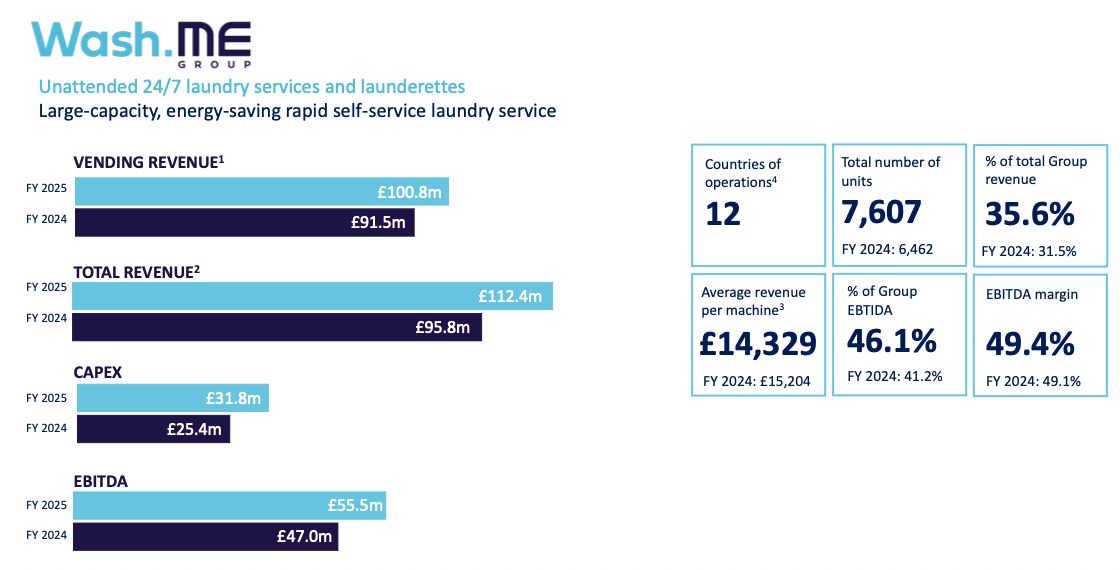

ME’s photobooth division is accompanied by a laundry division, which operates large-capacity outdoor washing machines and has become a rather surprising money-spinner:

This testimonial outlines why some people prefer to use an outdoor washing machine.

“Our baby groups use the machine every week and they will often arrive early to get the first go. They find it invaluable, as they get their washing done during class. We have other customers who own Airbnbs who are regular users as they can claim back their washing through their business. People regularly use the machine to wash large items such as duvets and rugs with positive comments about how fresh and clean the washing smells.

[The machines] have brought more people here and worked well with the on-site diner as people will get food and drink while they wait for their washing. People are also using the machine now because you can get three washing loads done in 40 minutes and people are saving on their own electricity.“

This independent reviewer meanwhile was “impressed with how my clothes were left smelling, feeling and looking“, although she was less impressed by the £10 cost.

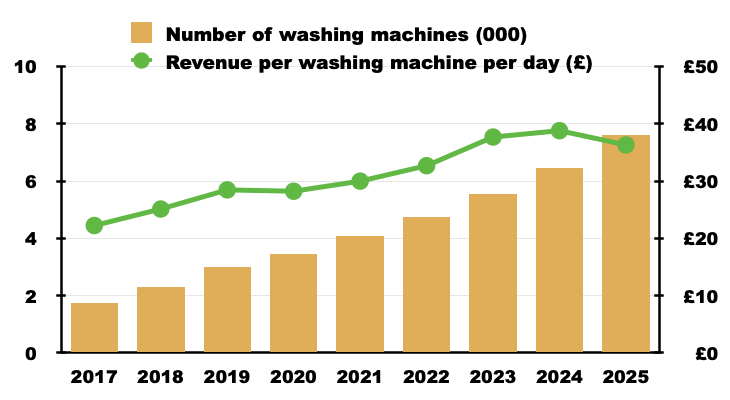

The laundry service was launched during 2012 and last year had reached more than 7,600 machines at supermarkets, petrol stations and other retail areas:

Vending revenue per washing machine last year was approximately £13,300 or £36 a day. I calculate revenue per washing machine has improved by more than 60% since 2017:

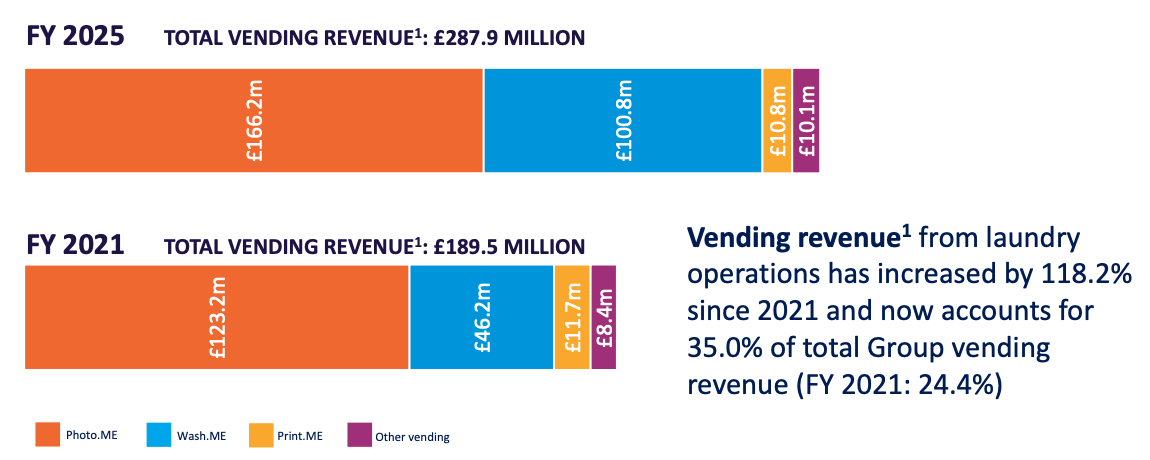

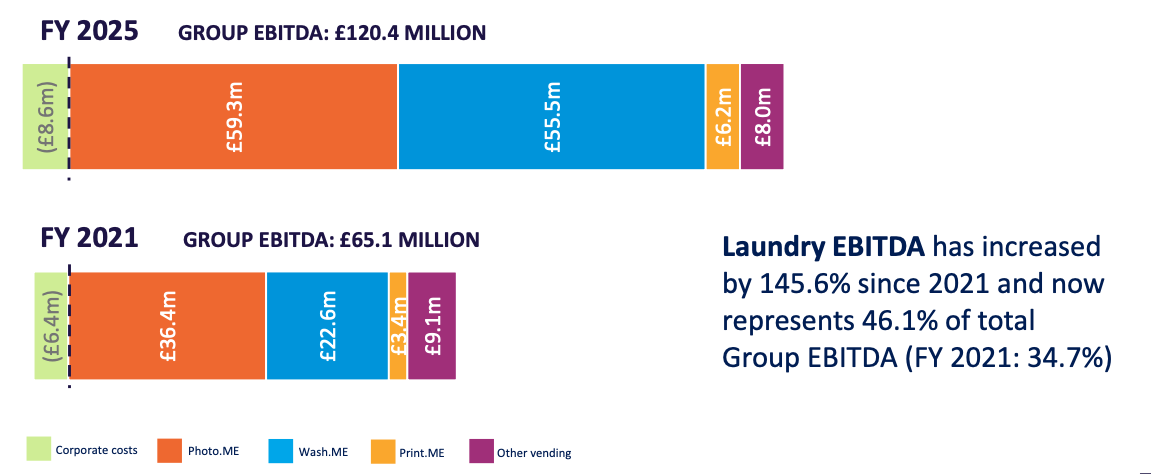

The bulk of ME’s revenue remains attributable to photobooths…

…but profitability (via Ebitda) has become more finely balanced between photobooths and washing machines:

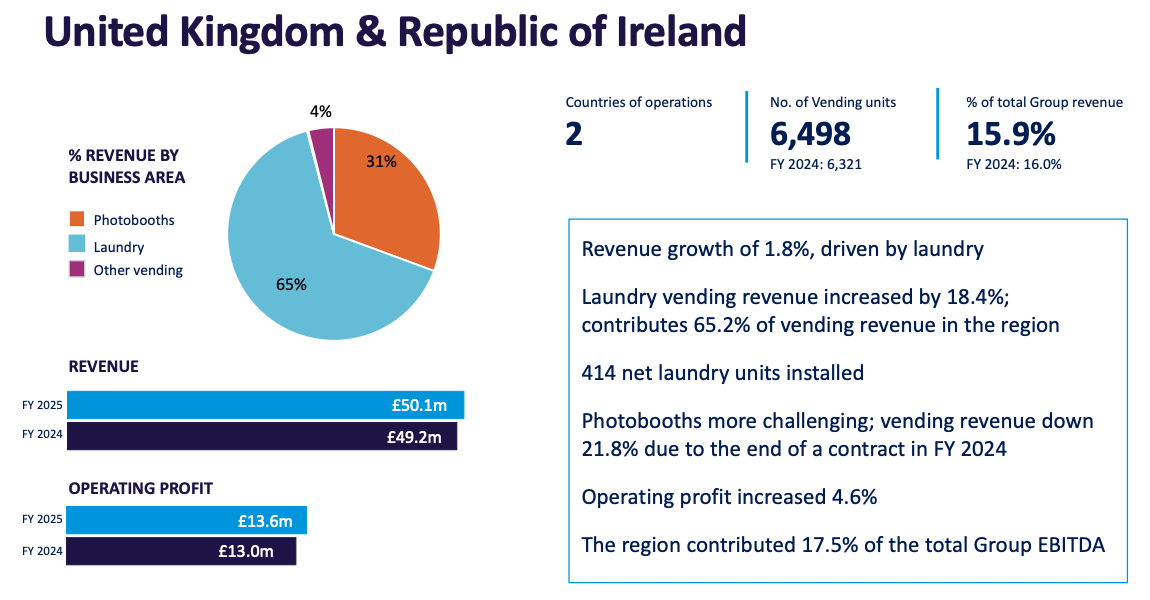

I was surprised to learn two-thirds ME’s UK revenue is now supported by the washing machines:

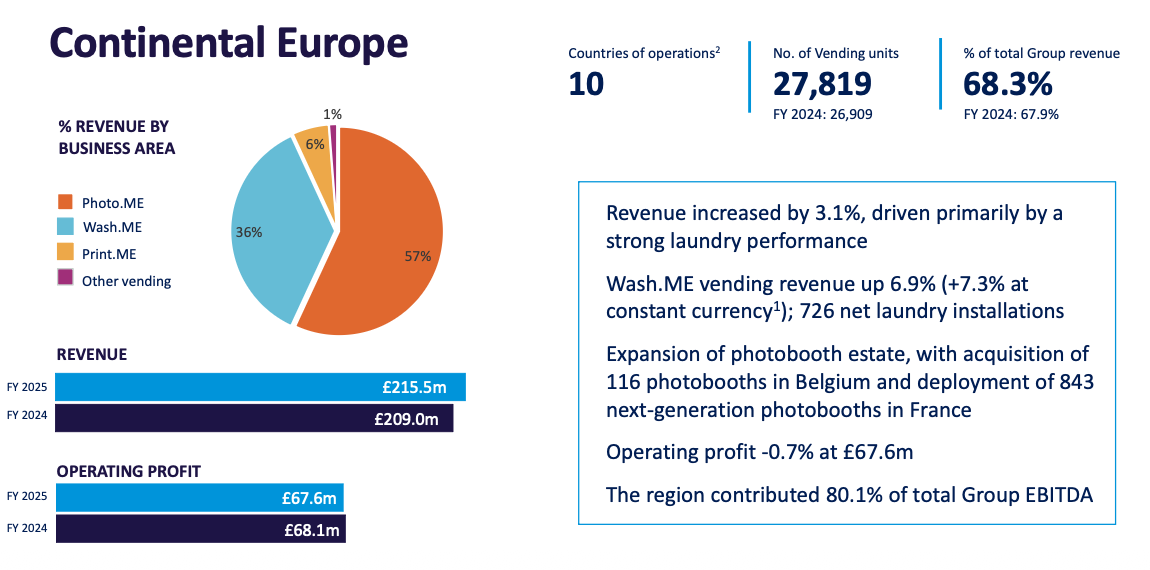

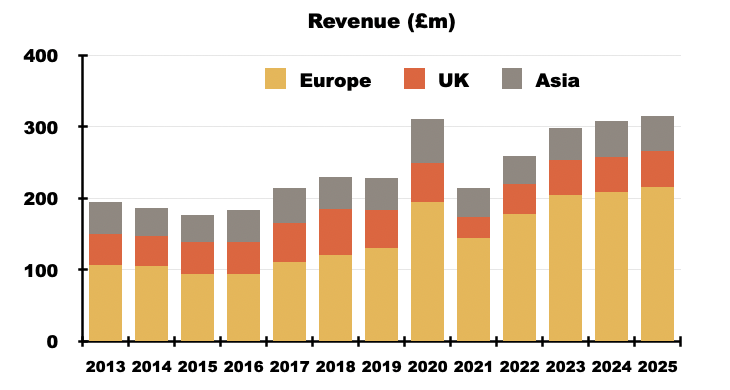

Two-thirds of group revenue is earned in Europe:

European income has in fact doubled since 2013:

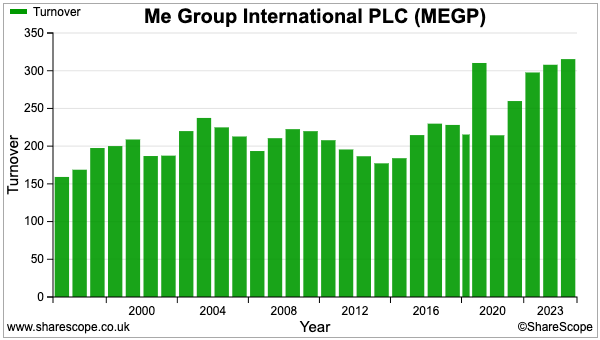

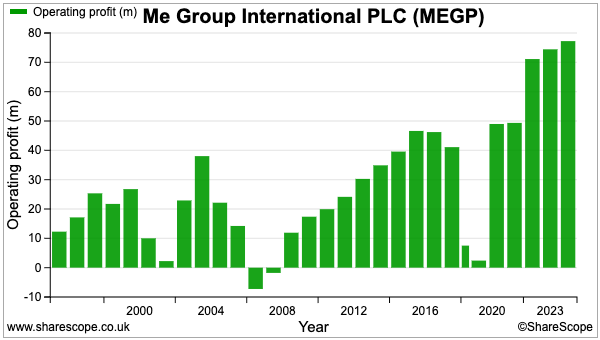

Following the KIS merger during 1994, total revenue has advanced from £172 million to £315 million…

…while operating profit has climbed from £18 million to £77 million:

Progress has not been straightforward, with a mix of greater competition, customer problems, technical transitions, difficult contracts, regulatory changes, failed projects, equipment write-downs and operating restructures causing very haphazard profits during the Noughties. The pandemic then blighted the group during 2020.

A profit warning the other week knocked 27% off the shares and seemingly reiterated ME’s wobbly earnings history. The recent 108p price trades at a level first witnessed during 1999(!) and supports a £396 million market cap.

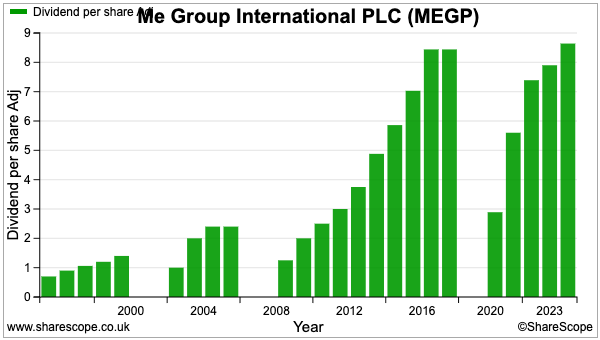

The earnings ups and downs are reflected by the dividend disappearing three times:

Mind you, ME has paid five specials (2013: 3p; 2014: 2p; 2016: 2.81p; 2022: 6.5p, and; 2023: 0.6p) to help make up for the absent ordinaries.

Prior-year restatements

Any commentary on ME’s accounts must start with the group’s slapdash approach to financial reporting. Recent years have suffered numerous prior-year restatements.

For example, the 2025 accounts revealed a £9 million error calculating the 2024 cash balance:

“Correction of prior period error – cash in transit

The opening balance of cash and cash equivalents at 1 November 2024 has been restated by a reduction of £8,689,000 to correct an error in the prior year financial statements. The adjustment is to correct an error in the calculation of the value of cash in transit held in the Group’s vending machines at the reporting date. A corresponding adjustment has been made to decrease the balance of trade and other payables by the same value (note 27)…“

The 2024 accounts meanwhile revealed a £22 million mix-up within property, plant and equipment:

“The balances of cost and depreciation for land and buildings, photobooth and vending machines and plant, machinery, furniture, fixtures & motor vehicles as at 31 October 2022 and 31 October 2023 have been restated to correct classification errors in the prior year property, plant and equipment note…

The impact on cost balances at 31 October 2023 was: land and buildings increase of £22,002,000; photobooth and vending machines reduction of £1,218,000; and plant, machinery, furniture, fixtures & motor vehicles reduction of £20,784,000.“

The 2024 accounts also owned up to a £4 million miscalculation of held-for-sale assets:

“The opening balance of property held for sale at 1 November 2023 has been restated by £4,362,000 to correct an error in the prior year financial statements.“

The 2023 accounts in turn corrected a £4 million mistake to the value of intangibles:

“The balance of prepayments at 1 November 2022 has been restated by a reduction of £3,783,000 to correct an error in the prior year financial statements. The adjustment represents the value of capitalised development work in progress which had previously been reported in prepayments but has now been reclassified to other intangible assets.“

The 2022 accounts included a ticking off from the auditor about ME’s goodwill calculations:

“We identified a number of audit adjustments and internal control recommendations to strengthen the group’s approach to goodwill recognition and impairment assessments that were shared with the Audit Committee.“

Rather alarmingly, the 2021 accounts had included the same ticking off:

“We identified a number of audit adjustments and internal control recommendations to strengthen the group’s approach to goodwill recognition and impairment assessments that were shared with the Audit Committee.“

And the 2020 accounts included an £11 million rejig of intangible assets…

“Intangible assets including goodwill represented £41.8m at 30 April 2019 and £32.7m at 31 October 2020. In the 18-month period to 31 October 2020, in accordance with IFRS 3 – Business Combinations, the group remeasured the value of intangibles arising from the acquisition of a subsidiary in April 2019 with the allocation of £10.5m from goodwill to Other intangible assets.”

…that prompted another comment from the auditor.

“Through the above procedures, we identified the need to restate the opening balance due to the correction of a prior year error, being the requirement under IFRS 3 to recognise a measurement period adjustment“

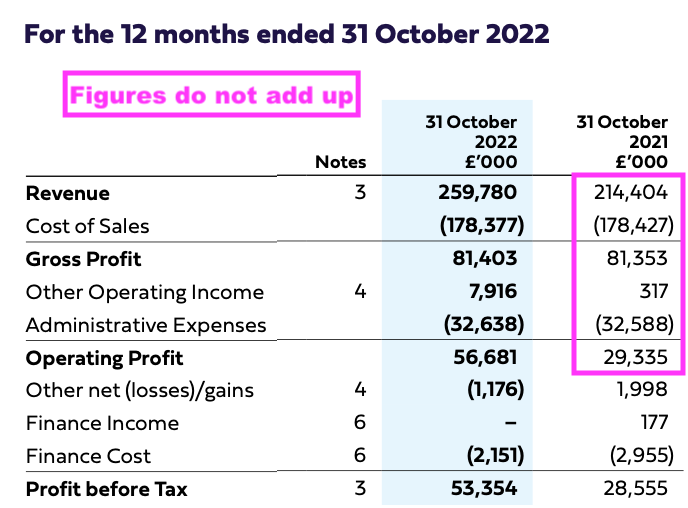

As well as restatements, ME has occasionally confused shareholders with typographical errors. The 2022 accounts for instance provided completely wrong figures within the comparative 2021 income statement:

Suffice to say, ME’s financials are not the easiest to follow and I am not surprised the 2025 results were delayed by three weeks because the auditor required more time to double-check the figures.

The delay meant MEGP missed the FCA’s four-month reporting deadline and the group’s shares had to be temporarily suspended.

ME said at the time it was “naturally displeased and disappointed… and is working with Forvis Mazars to make sure that the audit is completed as soon as possible.”

But to be fair to the auditor, ME had initially planned to publish its 2025 accounts on the day of the FCA’s four-month deadline, and the group’s history of accounting errors always risked extra audit work and subsequent delays.

Financials

The restatements and reclassifications sadly mean the following ShareScope charts may not be entirely accurate.

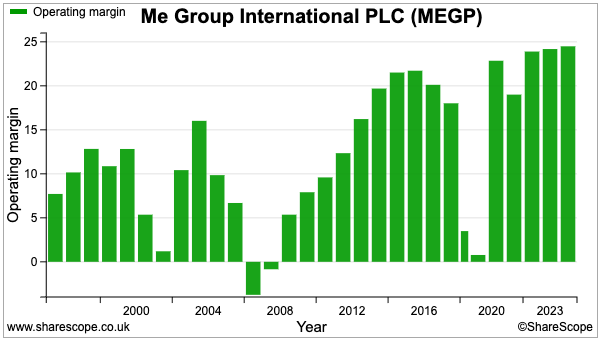

But as my initial filtering suggested, ME does apparently enjoy a decent operating margin. Approximately 24% has been registered for the last three years:

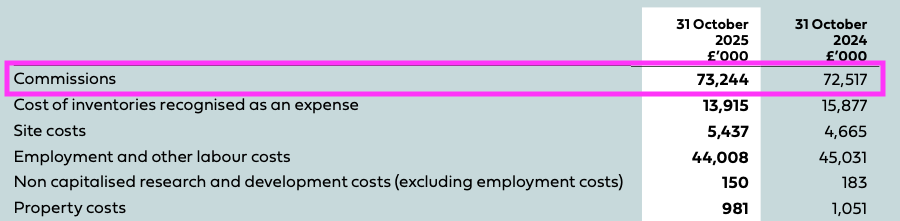

ME’s largest expense is commissions. Last year some £73 million — equivalent to 25% of group vending revenue — was shared among the site owners:

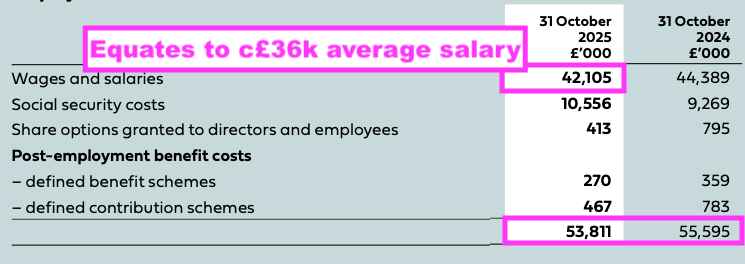

Another significant cost is the workforce. During 2025, £54 million was spent on 1,143 employees:

An average salary of roughly £36k does not seem a lot given ME’s history of technical innovation and its “in-house R&D team of 50+ engineers“. A fair number of ME’s staff are in fact deemed part-time and presumably undertake more mundane roles.

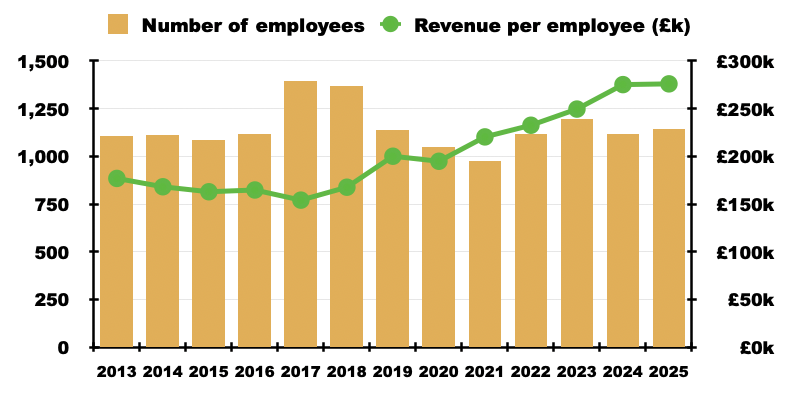

Workforce productivity has certainly improved. The headcount back in 2013 was also around 1,100, and revenue per employee has advanced from £177k to £276k since that time:

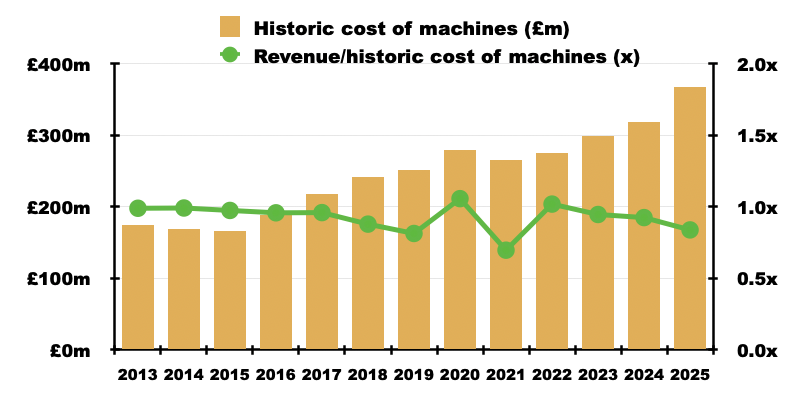

The productivity of ME’s vending machines has unfortunately not demonstrated such an obvious improvement.

The historic cost of the group’s photobooths, washing machines and other self-service equipment has doubled since 2013 to £368m:

But vending revenue divided by that historic cost has bobbed around the 0.9x mark throughout most of that time.

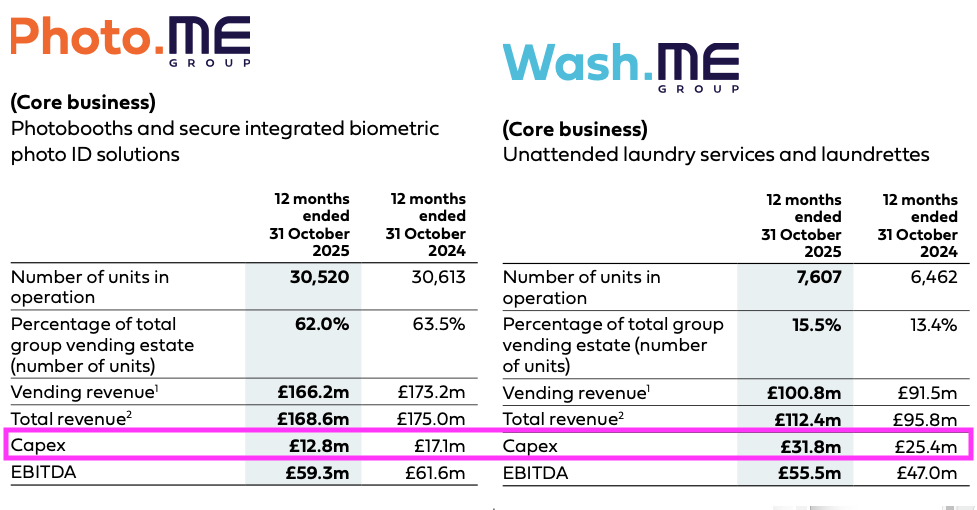

Further analysis can be gleaned from ME’s annual reports, which divulge the level of capital expenditure incurred by the photobooth and washing-machine divisions:

I calculate ME has incurred aggregate photobooth capex of £77 million since 2018, which in turn has lifted photobooth vending revenue by just £14 million — a return of 18%.

In contrast, I calculate ME has incurred aggregate laundry capex of £161 million since 2018, which in turn has lifted laundry vending revenue by £87 million — a return of 54%.

I get the impression the economics of the washing machines are much more attractive than the economics of the photobooths. Indeed, 5,587 additional washing machines since 2017 gives capex per new unit of £27k, while 1,979 additional photobooths since 2017 gives a much higher capex per new unit of £39k.

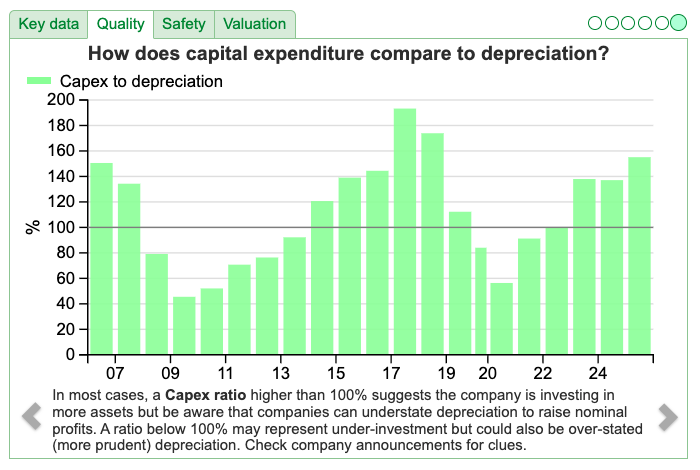

Note that the capex on all the new machines has often exceeded the depreciation charged against reported profits:

During the last ten years for example, aggregate capex of £361 million compares to aggregate depreciation of £308 million. The £53 million difference is not insignificant when aggregate operating operating profit during the same time is £485 million.

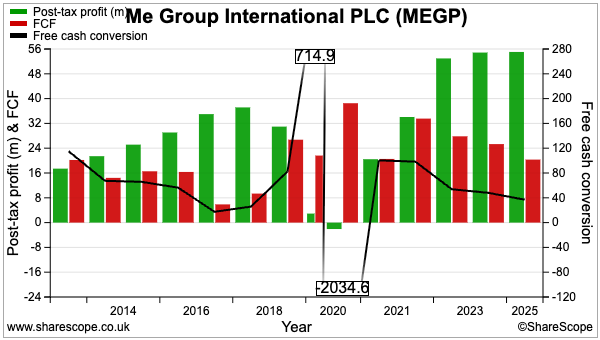

The gap between capex and depreciation explains why earnings have often converted at less than 60% into free cash:

Just so you know, the accounting useful life of the vending machines ranges from three to ten years:

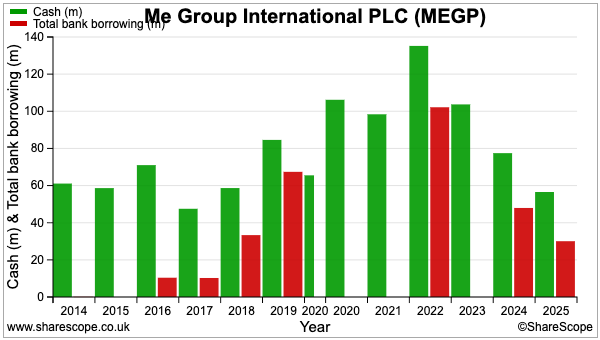

Despite all the capex, the balance sheet remains net-cash positive:

At the last count, bank borrowings were £30 million and looked under control given cash was £56 million and interest was charged at fixed rates up to a maximum of only 1.57%. Note that ME recently earmarked up to £18 million of its cash to support a share buyback.

Boardroom

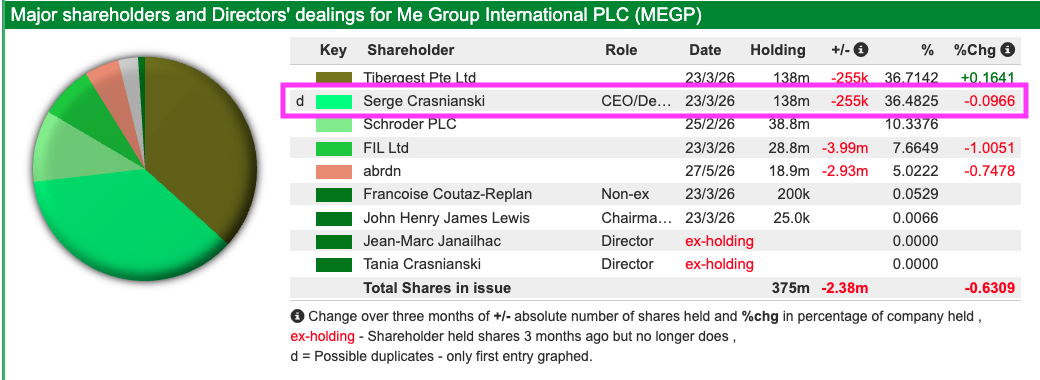

The aforementioned Serge Crasnianski remains ME’s prime executive and largest shareholder.

After joining the board initially as a non-exec during 1990, he became an executive following the 1994 KIS merger and then chief executive during 1998.

His leadership was interrupted during 2007 by unhappy shareholders, who effectively ousted Mr Crasnianski after witnessing 2005 earnings of £23 million slump to only £8 million.

But his board absence was short-lived, as one of the unhappy shareholders sold its 10% stake to a non-exec that paved the way for Mr Crasnianski to rejoin the board during 2009. By 2010 Mr Crasnianski had fallen out with ME’s proposed chief executive and has led ME ever since.

Mr Crasnianski’s desire to keep charge of ME is supported by his shareholding. He and his close relatives currently boast a 36% stake worth almost £150 million:

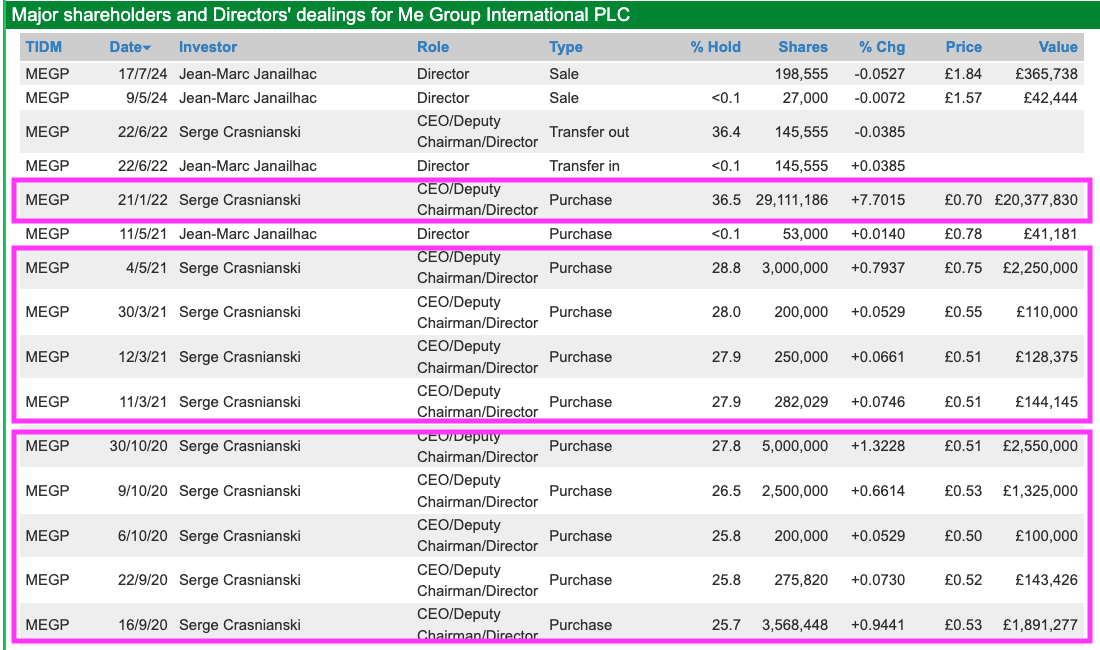

Recent years have encouragingly witnessed Mr Crasnianski allocate significant sums on ME shares. He spent £20 million during 2022 at 70p, £3 million during 2021 at an average 71p and £9 million during 2020 at an average 50p:

However, Mr Crasnianski now appears to be seeking an exit. A statement this time last year confirmed the group was “evaluating various strategic options to enhance shareholder value” and that “one of the options being considered involves seeking potential offerors for the Company“.

Six months of “engagement with several interested parties” sadly did not result in an offer that would “be in the best interests of all the Company’s shareholders“. Given the shares have since fallen from around 160p to the recent 108p, a suitable third-party bid would still appear very elusive.

Mr Crasnianski is accompanied on the board by his son Vladimir, who acts as deputy chief executive, and his daughter Tania, who serves as a non-exec after a few years holding a executive role.

This family-controlled board unsurprisingly incurs various corporate-governance transgressions. The 2025 annual report lists eleven best-practice contraventions, including not holding annual director re-elections, not responding to 20% protest votes and not replacing non-execs after the standard nine years.

Mr Crasnianski turns 84 next month and, absent any outside bid, I suppose ME will remain a family-controlled venture…

…although Mr Crasnianski’s children will have extremely large shoes to fill when their father eventually retires. Mr Crasnianski trained as a nuclear physicist, started KIS aged only 20, boasts more than 100 patents to his name…

…and has a particular “demanding” style of management (this 1985 Forbes article is extremely enlightening). He also seems very unconcerned about the aforementioned run of accounting errors.

For the record, ME’s finance director sits one rung below the main board and has been responsible for the group’s financial reporting since 2018:

Valuation and verdict

A trading update the other week revealed a “softening in revenue” during April that was “largely attributable to a shift in consumer spending patterns driven by lower consumer confidence due to the ongoing conflict in the Middle East.”

First-half revenue was said to have advanced only 2% as demand for official photo IDs subsided due to “ongoing travel uncertainty“. Demand for the washing machines was meanwhile “impacted… by a decline in consumer spending“.

The Middle East explanation for April’s “softening in revenue” did not seem entirely convincing, given the Iran conflict began at the end of February and annual results published on 23rd March had previously said 2026 trading was in line with expectations.

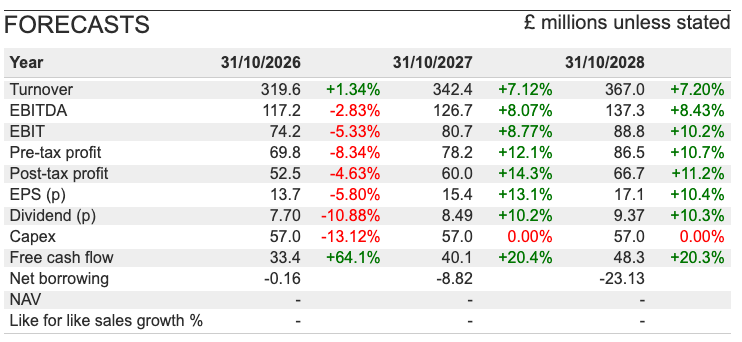

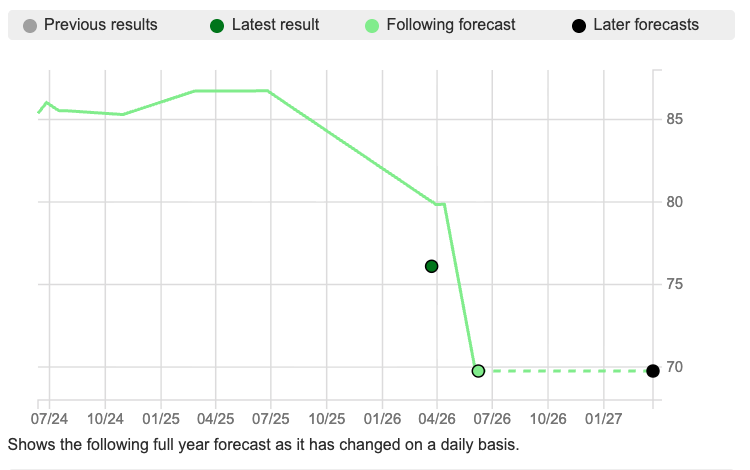

ME now expects a 2026 pre-tax profit of between £69 million and £74 million. Brokers anticipate £70 million versus £78 million for 2025:

Brokers had previously forecast an £80 million 2026 profit, while this time last year £85 million was being touted:

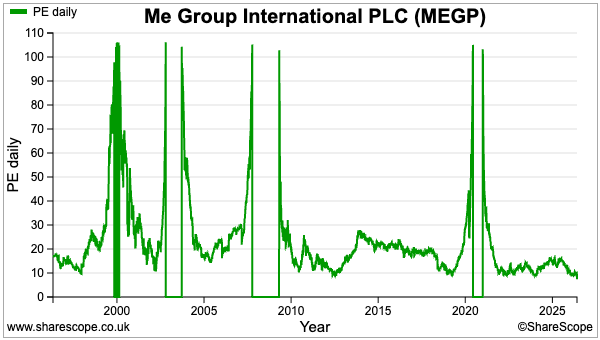

Earnings predictions of 13.7p per share support a multiple of less than 8, which is hardly expensive but does seem to match previous P/E lows:

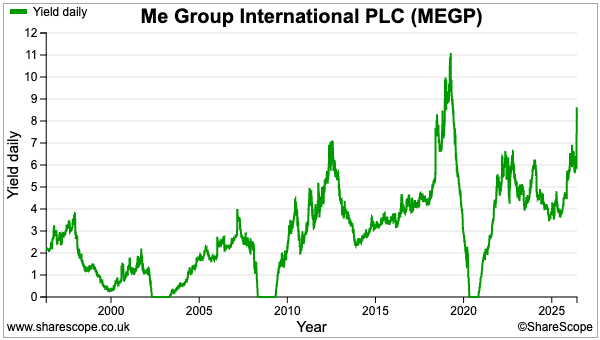

This year’s dividend is expected to suffer an 11% reduction to 7.7p per share, which in turn supports an 8% yield:

While the shares appear very inexpensive, clearly the economics of the group are not great if a 2% improvement to first-half sales (and perhaps 1% for the full year) is expected to translate into an £8 million lower annual profit.

The worry of course is what ME describes as the “uncertainty in the macroeconomic landscape” continues throughout the rest of 2026 and beyond.

I had not imagined usage of the washing machines in particular to be that sensitive to world events, but ME’s dividend going missing during the dot-com crash, the banking crash and the Covid crash does imply a certain vulnerability to downturns.

That vulnerability undoubtedly explains why the shares now trade close to that 52-week low and support a valuation that may well tempt contrarian investors to back Mr Crasnianski for another recovery.

I am quite sure any revival will be dependent entirely on the laundry division, given the photobooths appear to be a much more mature business and the group’s mishmash of other machines — including pizza-vending chalets — barely register in the accounts. I am also not sure whether Mr Crasnianski has a final money-spinning invention currently in the works.

After Mr Crasnianski terminated the bid discussions last year when the shares were north of 160p, I suppose he must believe the price offers substantial upside potential at the recent 108p. Could Mr Crasnianski therefore one day take ME private?

After all, Mr Crasnianski did purchase significant chunks of the group between 2020 and 2022 at prices up to 71p…

…and his attitude towards financial-reporting accuracy in particular does seem best suited away from the public markets.

Until next time, I wish you safe and healthy investing with ShareScope.

Maynard Paton

Disclosure: Maynard does not own shares in ME Group.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.