Richard considers modest executive pay at Alfa Financial Software and Quartix, and recent share purchases by FDM directors.

5 Strikes

Eighteen companies have published annual reports and passed my minimum quality filter since my last update.

|

Name |

TIDM |

Prev AR |

Strikes |

# Strikes |

|---|---|---|---|---|

|

EKF |

EKF Diagnostics |

27/4/26 |

? CROCI – Growth ? ROCE |

2 |

|

BILN |

Billington |

24/4/26 |

? Holdings – CROCI – Growth ? ROCE |

3 |

|

WINK |

M Winkworth |

24/4/26 |

– Holdings – Growth |

2 |

|

SQZ |

Serica Energy |

24/4/26 |

? Holdings ? Acquisitions – CROCI – Growth – ROCE – Shares |

X |

|

ENQ |

EnQuest |

23/4/26 |

? Acquisitions – Debt – Growth – ROCE ? Shares |

4 |

|

SAA |

M&C Saatchi |

23/4/26 |

– CROCI – Debt – Growth – ROCE – Shares |

X |

|

JDG |

Judges Scientific |

22/4/26 |

? Acquisitions – Debt – Growth |

2 |

|

NBB |

Norman Broadbent |

22/4/26 |

– CROCI – Growth – ROCE |

3 |

|

BAG |

Barr (AG) |

21/4/26 |

? Acquisitions ? Growth |

1 |

|

SAG |

Science |

21/4/26 |

? Growth |

1 |

|

STVG |

STV |

21/4/26 |

– Holdings – CROCI – Debt – Growth ? ROCE – Shares |

X |

|

FEVR |

Fevertree Drinks |

20/4/26 |

– CROCI – Growth |

2 |

|

FRES |

Fresnillo |

17/4/26 |

– CROCI ? Growth – ROCE |

3 |

|

MER |

Mears |

17/4/26 |

? Holdings – CROCI – Debt – Growth ? ROCE |

4 |

|

BOY |

Bodycote |

16/4/26 |

– Holdings ? Debt – Growth ? ROCE |

3 |

|

NXT |

Next |

16/4/26 |

– Debt |

1 |

|

CAML |

Central Asia Metals |

15/4/26 |

– Growth ? ROCE |

2 |

|

29/04/2026 |

||||

Quality was thin though. After momentarily considering their financial track records, three shares completely struck out, and only eight achieved less than three strikes. They will be considered for long-term investment, but not today, because I am working through a backlog.

I am also revisiting shares that I have already introduced as new information comes to light. Alfa Financial Software is one of them…

Alfa Financial Software [- Growth] and Quartix [? ROCE]

Maynard has done a deep dive on Alfa. It reveals an unusual executive remuneration setup that’s got me thinking.

The bombshell in Maynard’s article was that Alfa’s executive chairman and chief executive are paid close to the National Living Wage, although two other executives are paid more.

The executives’ decision to limit their pay in 2021, was prompted by a desire to be aligned with other shareholders. Since Alfa’s chairman owns 52% of the shares and the chief executive owns 2.6%, they will do well, like us, if the company prospers.

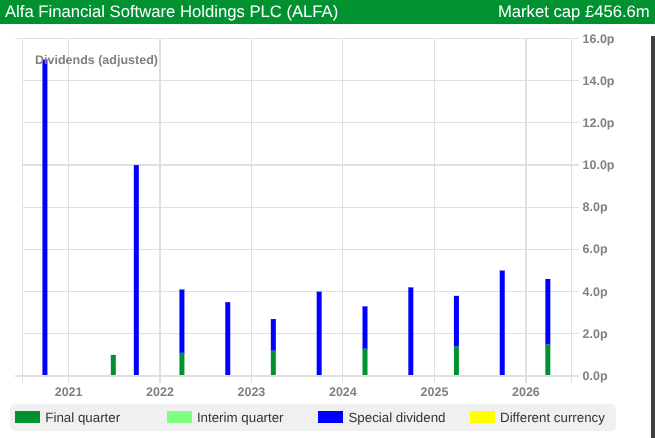

Certainly a steady stream of special dividends has provided them with an income:

Source: ShareScope

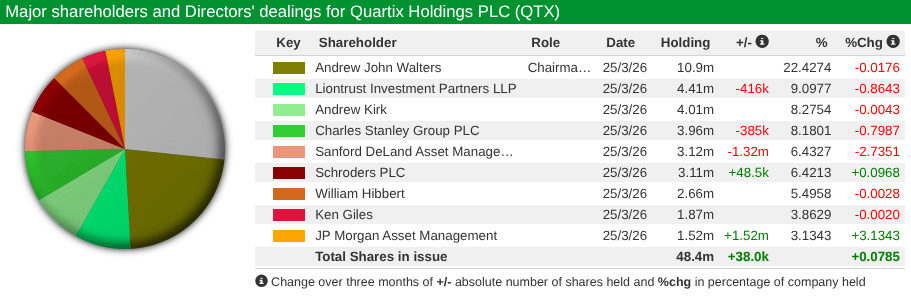

This situation reminds me of Quartix, where the company’s part-time chief executive and founder has taken home £50,000 a year in recent years.

Like the two Alfa executives, he has chosen not to receive bonuses or pension pay. Like them, dividends are a big source of income for him because he is a major shareholder:

While shareholder alignment is wonderful, the nit picking part of my brain also wonders whether it is sustainable. At some point these executives must hang up their boots and more standard executive pay may be required to recruit replacements.

This happened at Quartix in 2021, when chief executive Andy Walters retired. Quartix recruited a more typical board adding significantly to costs. Strategic missteps, principally a botched acquisition, presaged the exit of the newly recruited board, the return of the founder and the restoration of profitability.

A difficulty arises when we compare the profitability of businesses like Alfa and Quartix with businesses that pay more typical remuneration to executives. If we were to double the cost of Alfa’s board, say, so the two executives on the National Living Wage were paid more than the others (befitting their seniority), the cost of the board would increase from £2m to £4m.

Alfa earned £40m in profit (EBIT) last year, so £2m of additional board costs probably would not have a big impact on the financial metrics we use to compare businesses, like Return on Capital Employed and the valuation ratio EV:EBIT.

The less profitable the business, the greater the potential for a low-cost board to flatter our perception of the quality of the business itself. Quartix earned £8m of adjusted EBIT in 2025, a record for the company.

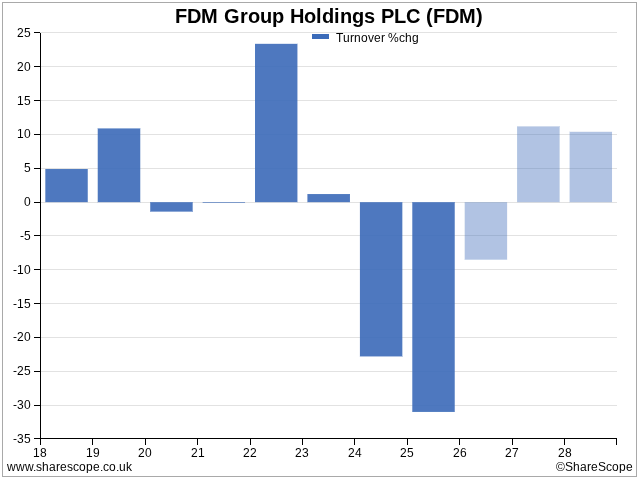

FDM [- Growth]

FDM only has one strike for growth. It’s a big one, though. So big I am considering introducing the concept of a double strike [–]. Turnover fell by more than 20% in 2024 and more than 30% in 2025. It has more than halved since it peaked at £334m in 2023.

Profit has collapsed, even on an adjusted basis. Six years ago in 2019, adjusted operating profit was just over £55m, in 2025 it was less than £14m.

This is not the consistency we look for in a long-term investment, but two things have drawn my attention to FDM.

The first is share transactions by executives, which encourages me to think speculatively that the company might be about to turn a corner. FDM executives have bought as the share price has plumbed new depths.

In April, founder Rod Flavell and his wife Sheila Flavell, also FDM’s chief executive and chief operating officer, bought shares worth more than £300,000. A day later, the spouse of the chief financial officer bought £50,000 worth of shares.

Founded by Rod Flavell and his previous wife Jacqueline Flavell in 1991, FDM has quite a complicated history. It listed on the main market in 2014, but had previously been listed on AIM. In 2010, Rod and Sheila Flavell took it private.

With the share price at new lows, history would be repeated if the firm delists at a lowball price again. That seems unlikely though. The combined holdings of the Flavells amount to about 14% of the shares, nowhere near the 75% vote required to delist voluntarily.

The thing that brings me back to FDM every year is the company’s silence on the threat of Artificial Intelligence.

FDM recruits entry level technical consultants and business analysts, trains them up and hires them out on fixed term contracts. If fears that AI is replacing entry level software jobs are true, FDM ought to be the canary in the coalmine.

In its latest annual report, FDM explains the fall in turnover using broadbrush terms like “difficult market conditions”. It references macroeconomic and geopolitical uncertainty. Previously, it has also claimed that customers are often reluctant to take on permanent staff in economic slow downs, creating the “potential for an increase in demand” for temporary consultants.

I cannot find any mention of a negative impact on the deployment of consultants specifically due to the adoption of AI in the annual report. But customers are demanding AI skills, because the company is training its recruits so it can take advantage of the opportunity.

Whether the opportunity is greater than the threat that customers are developing these skills internally is another question. Judging by the trades, management may think it is, and traders may be more sceptical.

Richard Beddard

Contact Richard Beddard by email: richard@beddard.net, web: beddard.net

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

How can I keep a check on your portfolio?

Hi John, this link will take you to all of my articles in interactive investor: https://www.ii.co.uk/authors/richard-beddard

Most weeks I write about companies in the portfolio or candidates for inclusion. The first week of the month is different. This article is a Share Sleuth portfolio update. It includes details of any trades made in the portfolio during the month, and also its performance. The next Share Sleuth article is imminent. You should be able to read it on Saturday. The last one is here: https://www.ii.co.uk/analysis-commentary/share-sleuth-why-i-ignored-trading-nudge-ii538697

Hope that helps.

Thanks Richard Always a fascinating read.

Thanks Jas