Loads more companies pass 5 Strikes this week as the flood of annual reports continues. Richard looks at what software companies are saying about the AI threat, and reconsiders ConvaTec (CTEC) as its strategy evolves.

5 Strikes

21 companies published annual reports in the last two weeks or so and passed my minimum quality filter:

| Name | TIDM | Prev AR | Strikes | # Strikes |

|---|---|---|---|---|

| GRG | Greggs | 13/4/26 | – Holdings – CROCI – Debt | 3 |

| PAGE | Page | 13/4/26 | – Holdings? CROCI – Debt – Growth – ROCE | 2 |

| FDM | FDM | 10/4/26 | – Growth | 1 |

| HILS | Hill & Smith | 10/4/26 | – Holdings ? Acquisitions | 1 |

| MACF | Macfarlane | 10/4/26 | – Holdings – Debt ? Growth | 2 |

| SVS | Savills | 9/4/26 | – Holdings – CROCI ? Growth ? ROCE | 2 |

| APTD | Aptitude Software | 8/4/26 | – Holdings ? Acquisitions – Growth | 2 |

| CCC | Computacenter | 8/4/26 | 0 | |

| IGG | IG | 8/4/26 | – Holdings – Growth | 2 |

| SPX | Spirax | 8/4/26 | – Holdings – Debt ? Growth | 2 |

| BBY | Balfour Beatty | 2/4/26 | – Holdings ? CROCI ? Growth – ROCE | 2 |

| KGF | Kingfisher | 2/4/26 | – Holdings – Debt – Growth – ROCE | 4 |

| MSLH | Marshalls | 2/4/26 | – Holdings – Growth – ROCE – Shares | 4 |

| TPFG | Property Franchise Group | 1/4/26 | – Holdings ? Acquisitions – Shares | 3 |

| FRAN | Franchise Brands | 31/3/26 | ? Acquisitions – Debt – ROCE – Shares | 3 |

| IMI | IMI | 31/3/26 | ? Holdings – Debt ? Growth | 1 |

| CKN | Clarkson | 30/3/26 | ? Growth – ROCE | 1 |

| RMV | Rightmove | 30/3/26 | – Holdings | 1 |

| RWA | Robert Walters | 27/3/26 | – Holdings – CROCI – Growth – ROCE | 4 |

| ROR | Rotork | 27/3/26 | – Holdings ? Growth | 1 |

| VTY | Vistry | 27/3/26 | – Holdings ? Acquisitions – CROCI ? Growth – ROCE – Shares | 4 |

| Click here for our 5 Strikes explainer | 15/04/2026 | |||

Having briefly scrutinised their financial track records in Sharescope, 14 of them achieved less than three strikes. I will get around to writing more about them, but not this time.

Due to the large numbers of companies publishing annual reports, I am still writing up promising investment candidates from lists in previous articles.

And I’m still thinking about some of the major issues facing investors now…

AI interlude

I received a surprise in my inbox recently. A marketing email from Cerillion. Beddard Telecoms must have inadvertently signed up when digging for info on the company earlier this year. Luckily I didn’t nuke the email on sight.

Since the sell off in software companies, information providers, and broker style intermediaries in February, it is clear investors are worrying that increasingly capable looking AI will usurp these businesses.

Yet in the communications I’ve seen from companies I follow, the threat of AI is barely mentioned, relegated to a generic sentence or two in the risk report (here’s looking at you, Softcat and Auto Trader). AI is portrayed as an opportunity for these businesses to serve customers better, and code more efficiently.

Investors need help to understand the risks, because if the worst case for these businesses comes true their existence could be in doubt. Even if they believe there is no risk from AI, we need them to explain why.

Alfa Financial Software impressed me by tackling the issue head on in the main body of its annual report.

On Cerillion’s blog Dominic Smith, the company’s marketing director, writes that AI cannot do what Cerillion does. Cerillion is a Software as a Service company. It provides billing and charging software for telecom companies.

Smith says AI cannot do charging and billing because it is probabilistic, which means the same inputs will produce slightly different outcomes. In most business contexts this is not a big deal: “If an AI agent drafts slightly different wording in a contract summary or marketing email, no harm is done…”

But billing is not a game of Numberwang, where random numbers are arbitrarily declared correct.”

Financial systems require fixed rules and reproducible results (this is one of Alfa’s arguments too – it provides software for lessors).

Cerillion’s customers are Communications Service Providers (CSPs), an umbrella term that includes telecoms companies, virtual network operators and broadband providers.

What sounds like a fairly simple process, billing, is the culmination of millions of chargeable events every day, across different systems (text, voice, data, and broadband for example). The bill is determined by rules relating to pricing, discounts, bundling and tax for example. Small inaccuracies compound, he says, and regulators punish billing inaccuracies. I am sure customers don’t like them either.

AI can help configure and optimise systems, explain bills, analyse problems, and automate some of the human activity required by the platform, but it cannot replace the billing software itself. Indeed, he says AI must be integrated safely, so that it cannot interfere with the software.

This strikes me as a similar argument to the one being made in defence of information providers like RELX. AI can make it easier to access the data, like it can make it easier to use deterministic software, but without high quality data or deterministic software it is unreliable. In some contexts, that is not acceptable.

In a recent FT column, the chief executive of SAP, the giant German enterprise software company, wrote that AI models do not know “how a manufacturer sequences parts across a global supply chain, or how a bank reconciles thousands of transactions against regional regulation. That knowledge is not learnt from the internet – it is encoded in enterprise software.”

These arguments may be self-serving, but they also ring true. That said, we could all be surprised by how AI does, or does not, change things in the future.

ConvaTec [? holdings – Debt ? Growth ? ROCE]

Last time, I introduced ConvaTec. Days later the company announced the evolution of its strategy, now dubbed “Accelerate”.

I feared the company might go all in on acquisitions, a rapid and sometimes unsustainable way to grow. ConvaTec’s old strategy, FISBE, stood for Focus Innovate Simplify Build Execute, all ambitions I could get behind.

Under FISBE ConvaTec focused on four categories relating to chronic care: Advanced Wound Care (for example dressings), Ostomy Care (for example Last time), Continence Care (for example catheters), and Infusion Care (infusion sets).

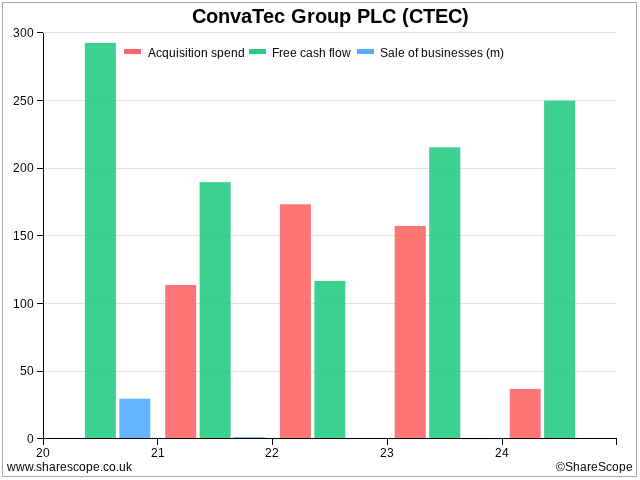

The FISBE strategy did not specifically mention acquisitions, but while it was guiding ConvaTec between 2020 and 2025 the company made several. Between 2021 and 2023 it spent most of its free cash flow on seven businesses, six of them mostly in Continence Care. The biggest by far was an Advanced Wound Care business (Triad Life Sciences).

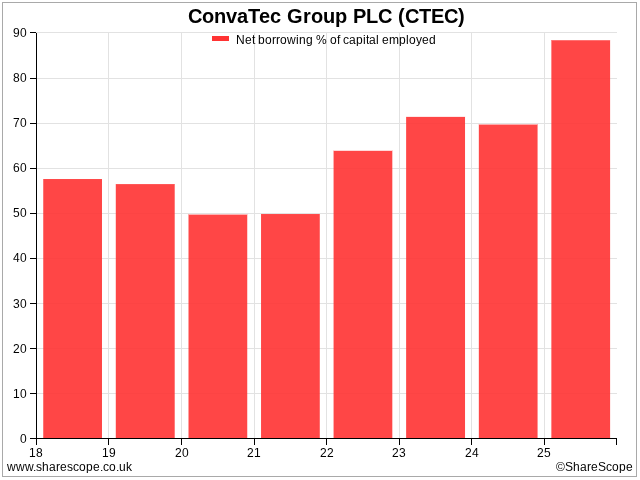

In the process it amassed more debt than I am comfortable with (it already had more than I am comfortable with!):

The Accelerate strategy does not specifically mention acquisitions either. ConvaTec plans to work more closely with customers, innovate with new technology, simplify and speed up operations, and develop a culture of purpose and performance. It’s a refinement of FISBE.

These are boring buzzwords that can be hard for outsiders to evaluate, but they are also things confident self reliant companies do well.

ConvaTec must ease off on the acquisitions, reduce debt, and keep growing profitably if it is to convince me it is one of them.

Richard Beddard

Contact Richard Beddard by email: richard@beddard.net, web: beddard.net

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Great point about the SAP CEO’s view on enterprise software. It’s easy to forget that ‘knowledge’ isn’t just scraped from the web; it’s encoded in decades of process rules. Looking forward to your deeper dive into the other 14 companies that passed your quality filter!

Hi ia. Thanks for your comment! I agree, the whole thing about probability v determinism was a fascinating rabbit hole to run down. Regarding the 14 other companies, there are more than that now. They’re mounting up. But that’s a great position to be in. I look forward to writing about them.