Bruce Packard examines the sharp rise in UK gilt yields and what it signals for inflation, equities and investor sentiment. He also explores the AI disruption debate through the lens of CCT, RMV, RWS.

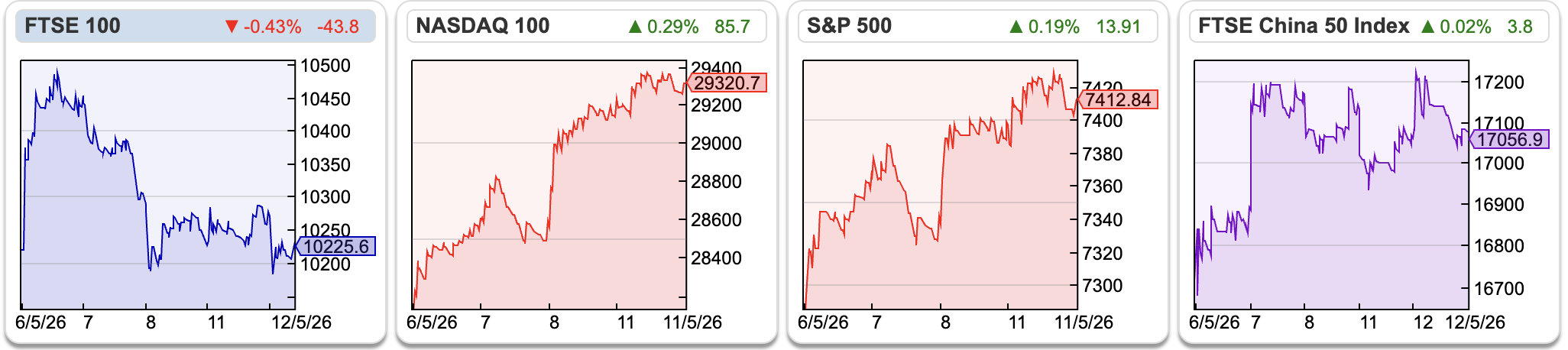

The FTSE 100 was flat over the last 5 days, remaining above the 10,000 level at 10,225. US markets have been much stronger, with the Nasdaq100 up +6% and S&P500 +3%. Brent was $107 per barrel, up +7% after Donald Trump rejected Tehran’s offer to end hostilities in the Gulf.

The FTSE 100 was flat over the last 5 days, remaining above the 10,000 level at 10,225. US markets have been much stronger, with the Nasdaq100 up +6% and S&P500 +3%. Brent was $107 per barrel, up +7% after Donald Trump rejected Tehran’s offer to end hostilities in the Gulf.

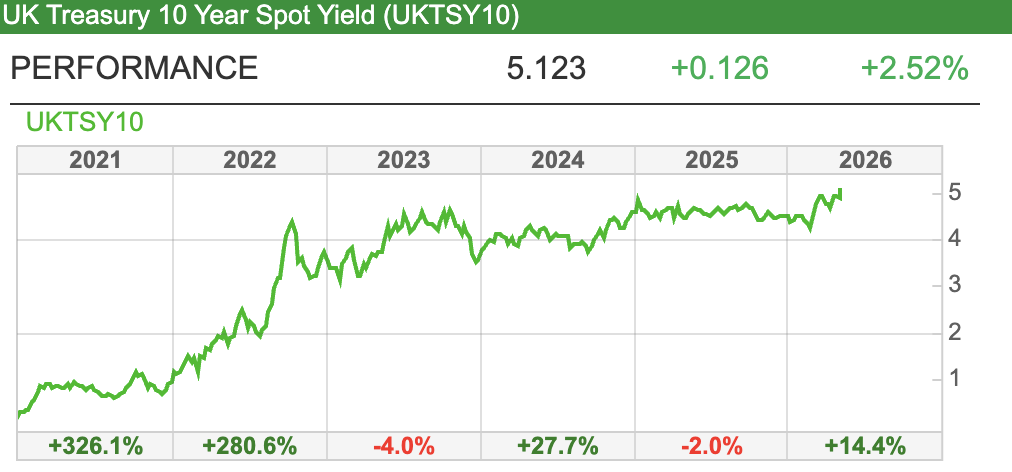

The UK 10 year government bond yield (ShareScope ticker UKTSY10) has broken above the 5% level, versus a historic low of just 7 basis points in August 2020. 7bp to lend to the UK government for 10 years! One of the main buyers of gilts back then was the Bank of England (Quantitative Easing), which is now being reversed and the Central Bank continues to sell down their position at a yield above 5%.

To be fair, the Central Bank’s stated intent was not to make profits, but to prevent a deflationary spiral. However, by using tax payers’ money to suppress Government borrowing costs, there was a wealth transfer from younger generations of workers to the property owning older generation. That’s not sustainable and we are now dealing with the consequences.

To be fair, the Central Bank’s stated intent was not to make profits, but to prevent a deflationary spiral. However, by using tax payers’ money to suppress Government borrowing costs, there was a wealth transfer from younger generations of workers to the property owning older generation. That’s not sustainable and we are now dealing with the consequences.

ShareScope also shows the steepness of the yield curve, the difference between the 2 year and 10 year gilts below. The curve was inverted for much of 2023 and 2024 (2 year yields above 10 year yields) often taken to be a signal of a coming recession. The recent “bear steepening” shows gilt investors are now more worried about persistent inflation.

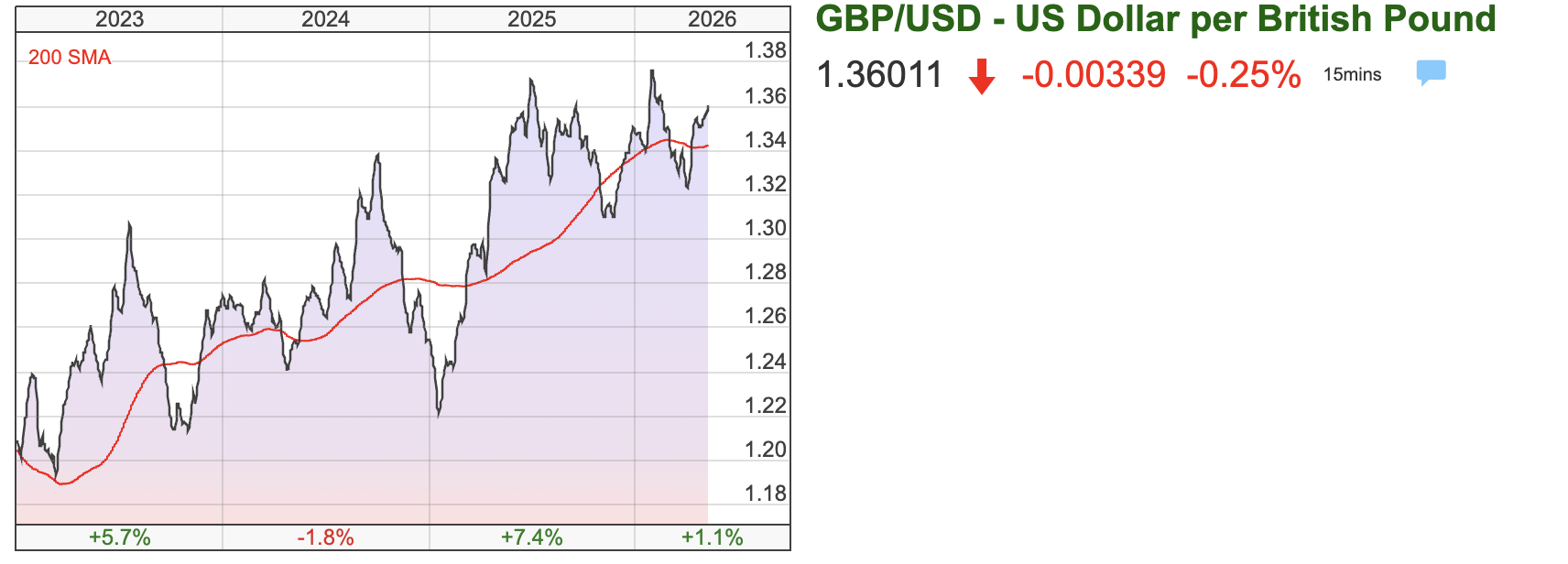

These trends may turn out to be a positive for both the pound and owners of UK equities, as the investment case here looks attractive on a relative basis, particularly compared to UK property and US equities. While gilts have been weak, sterling has been strengthening (chart below).

AXX has also rebounded strongly, +16% since the end of March and is now trading above short and long term moving averages. Thus I may have been too cautious, having sold Arcontech, Andrews Sykes and half of my Duke Capital, to tidy up my portfolio and raise cash to reinvest in the summer. Let’s wait and see.

AXX has also rebounded strongly, +16% since the end of March and is now trading above short and long term moving averages. Thus I may have been too cautious, having sold Arcontech, Andrews Sykes and half of my Duke Capital, to tidy up my portfolio and raise cash to reinvest in the summer. Let’s wait and see.

This week I look at a couple of investment cases responding to the threat of Agentic AI: i) Rightmove’s AGM trading statement and ii) RWS the language translation services group that has made a small acquisition. I begin with Character Group’s significantly ahead of expectations guidance for FY Aug.

Character Group H1 Feb, FY Aug significantly above market expectations

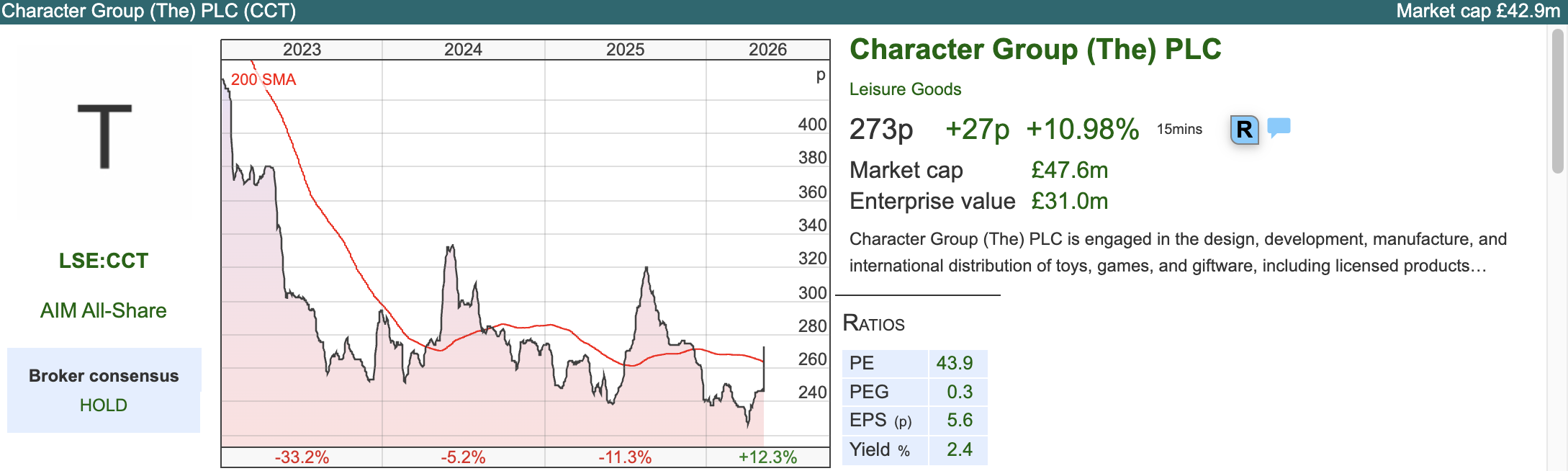

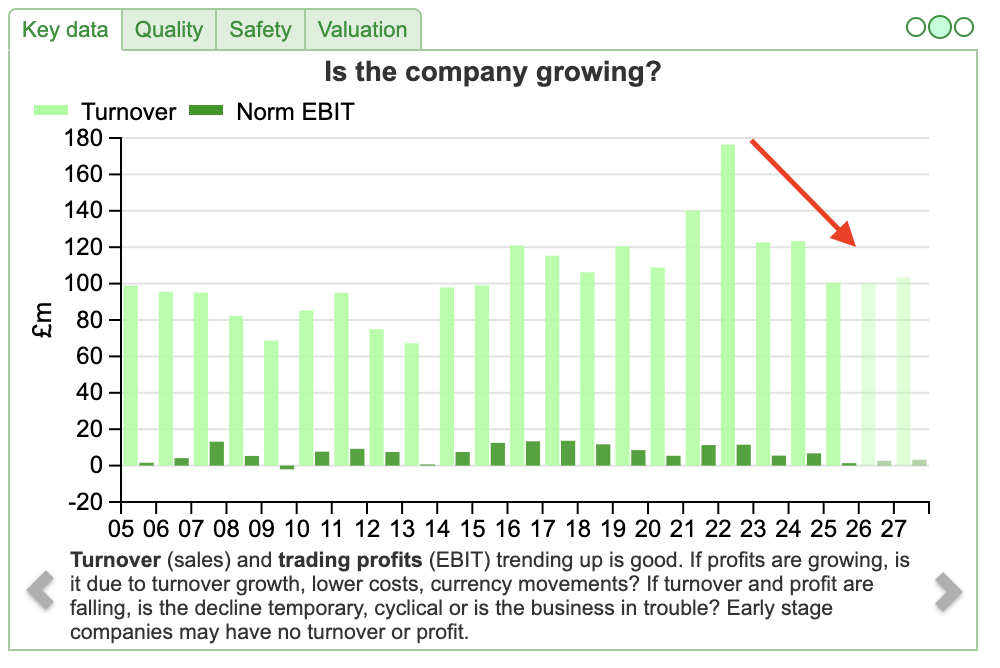

This toy and games maker has faced a difficult couple of years, through no fault of their own. First they lost the Peppa Pig manufacturing contract, when Entertainment One (owner of the IP and trademark) was bought by Hasbro. More recently they’ve been a victim of the cost of living pressure (household disposable income eroded by rising inflation and borrowing costs) then on top of that Donald Trump’s tariffs, as they manufacture toys in China and sell into the USA. Revenue fell from £176m FY Aug 2022 to £100m FY Aug 2025, as the red arrow on the ShareScope chart below shows.

This toy and games maker has faced a difficult couple of years, through no fault of their own. First they lost the Peppa Pig manufacturing contract, when Entertainment One (owner of the IP and trademark) was bought by Hasbro. More recently they’ve been a victim of the cost of living pressure (household disposable income eroded by rising inflation and borrowing costs) then on top of that Donald Trump’s tariffs, as they manufacture toys in China and sell into the USA. Revenue fell from £176m FY Aug 2022 to £100m FY Aug 2025, as the red arrow on the ShareScope chart below shows.

That said, the shares have bounced more than +20% from their April low, so perhaps we are beginning to see a recovery?

That said, the shares have bounced more than +20% from their April low, so perhaps we are beginning to see a recovery?

H1 Feb PBT ex FX currency gains was up +14%, to £2.4m, despite H1 Feb revenues falling -9% to £48m. The H1 comparisons are particularly tough, as the previous H1 was before Trump’s tariffs. They have always operated with a conservative balance sheet, and net cash was £14m at the Feb half year. Inventory is less than £10m, so they’re not sitting on unsold stock. I had wrongly believed they no longer had any rights to make Peppa Pig, but reading the commentary they mention the arrival of Peppa’s baby sister Evie. They are still making Peppa complementary and adjacent toys, but Hasbro has in-sourced the core Peppa Pig manufacturing.

Property: Management are currently leasing out their warehouse in Lancashire and have written a call option, allowing the tenant to buy the property for just under £10m at the completion of the letting before the end of the current financial year end (August).

Outlook: Despite the H1 revenue decline, management suggest FY Aug results will be “significantly above current market expectations.” Within that, FY Aug revenue is likely to be flat, but helped by a well received product portfolio, an improved gross margin and a currency tail wind, should mean an encouraging performance despite tough markets. Allenby have raised FY Aug PBT by two thirds, from £3m to £5m.

Valuation: The shares are trading on a PER of 12x Allenby’s upgraded FY Aug 2026F adj EPS estimate and 5x EV/EBITDA the same year. There are no FY Aug 2027F forecasts yet though, suggesting management don’t feel particularly confident in the outlook for next year.

Opinion: The group has navigated the difficult environment reasonably well, and hopefully better times are ahead. During the pandemic ROCE peaked at mid 20’s, so I can see that the recovery could have further to go if the current positive trends are sustainable. That said, they don’t own their own Intellectual Property, so they are very unlikely to be the “next Games Workshop”, EBIT margin is currently just over 1%. I don’t own any, but imagine this could rebound at some point.

Opinion: The group has navigated the difficult environment reasonably well, and hopefully better times are ahead. During the pandemic ROCE peaked at mid 20’s, so I can see that the recovery could have further to go if the current positive trends are sustainable. That said, they don’t own their own Intellectual Property, so they are very unlikely to be the “next Games Workshop”, EBIT margin is currently just over 1%. I don’t own any, but imagine this could rebound at some point.

Rightmove AGM Trading statement

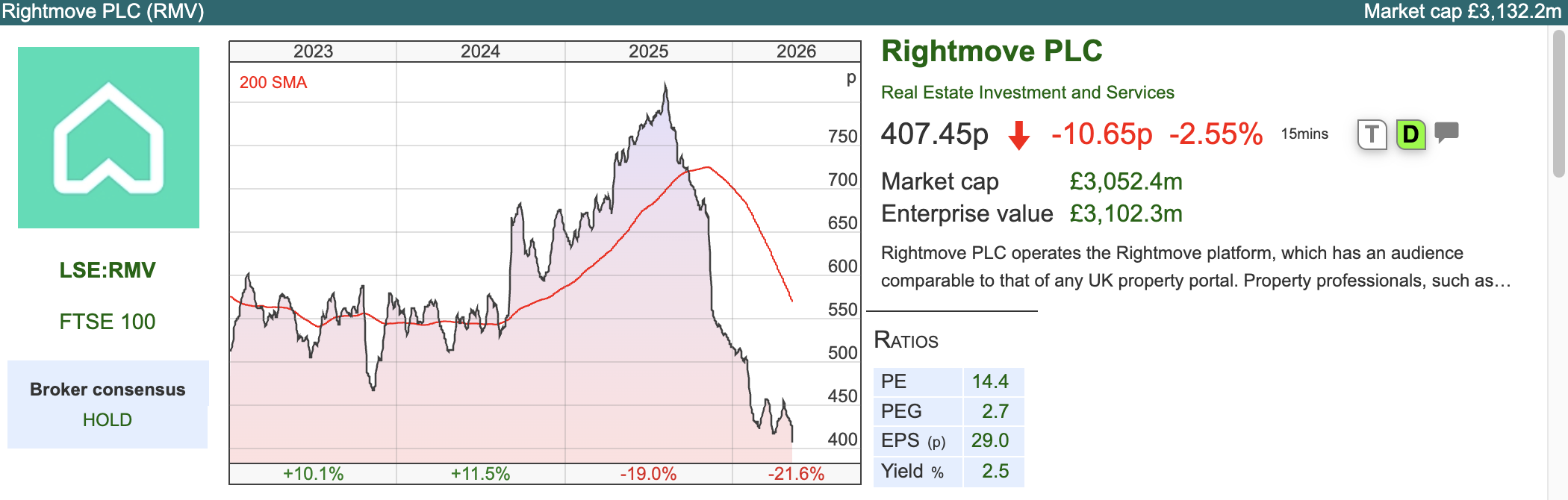

Investors have been worrying for several years that this property advertising portal has been enjoying unsustainably high profitability. When I last wrote about the group in early 2024, RMV RoCE was 300% and Nasdaq-listed CoStar had bought OntheMarket, hoping to invest and disrupt Rightmove’s business model. That threat has not yet had an impact as ShareScope’s quality indicators, which show that Rightmove’s 2025 RoCE was 323% and EBIT margin remained close to 70%.

Investors have been worrying for several years that this property advertising portal has been enjoying unsustainably high profitability. When I last wrote about the group in early 2024, RMV RoCE was 300% and Nasdaq-listed CoStar had bought OntheMarket, hoping to invest and disrupt Rightmove’s business model. That threat has not yet had an impact as ShareScope’s quality indicators, which show that Rightmove’s 2025 RoCE was 323% and EBIT margin remained close to 70%.

Then in late 2024 REA Group, the Australian property group 62% owned by Rupert Murdoch’s News Corp, made an unsolicited approach, culminating in a final bid at 780p (346p in cash and the rest in REA Group paper). The Rightmove board unanimously rejected this proposal, believing that it materially undervalued the company.

Then in late 2024 REA Group, the Australian property group 62% owned by Rupert Murdoch’s News Corp, made an unsolicited approach, culminating in a final bid at 780p (346p in cash and the rest in REA Group paper). The Rightmove board unanimously rejected this proposal, believing that it materially undervalued the company.

Then the shares fell -16% in November last year, when management said they would spend £18m (£12m expensed through the P&L and £6m of capitalised investment added to the balance sheet) on software development and other intangible spend to defend their “moat”. That compares to £290m of PBT FY Dec 2025.

This year there’s been a court case, where estate agents (who pay Rightmove to advertise properties on the platform) say RMV are abusing its dominant market position by charging estate agents excessive fees. This case is being backed by Innsworth Advisors, the litigation finance arm of Paul Singer’s Elliot hedge fund. The headline cost of redress is suggested at £1.5bn. The shares have roughly halved from their mid 2025 peak of 827p.

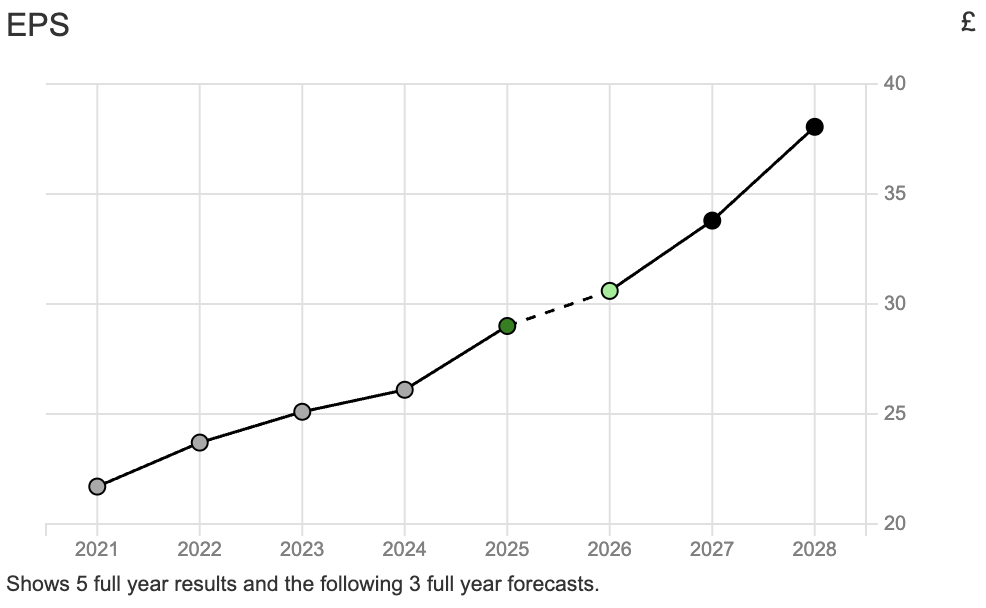

Outlook: All that background, plus a weak UK property market and Rightmove AGM statement last week reiterated revenue growth guidance of +8 to +10%. Underlying EPS growth is expected to be at least +5%, and ShareScope Forecast tab shows consistently rising EPS into the foreseeable future.

Outlook: All that background, plus a weak UK property market and Rightmove AGM statement last week reiterated revenue growth guidance of +8 to +10%. Underlying EPS growth is expected to be at least +5%, and ShareScope Forecast tab shows consistently rising EPS into the foreseeable future.

Valuation: The shares are trading on PER of 12x Dec 2027 and 9x EV/EBITDA. That’s obviously well below the historic valuation multiple investors were prepared to pay, however Rightmove is still on over 6x price to sales. For comparison, WISE a platform that’s following a different strategy of sharing the benefits of network effects with customers (via lower prices) is on 5x sales, but a PER of 27x.

Valuation: The shares are trading on PER of 12x Dec 2027 and 9x EV/EBITDA. That’s obviously well below the historic valuation multiple investors were prepared to pay, however Rightmove is still on over 6x price to sales. For comparison, WISE a platform that’s following a different strategy of sharing the benefits of network effects with customers (via lower prices) is on 5x sales, but a PER of 27x.

Opinion: I think I will put RMV in the “too hard” pile for now. There’s an obvious disconnect between continuing rising EPS forecasts and a share price that has collapsed on understandable, but hard to quantify, fears of disruption. The disruption fear is that AI Agents will be able execute multi-step workflows, thus RMV’s “moat” could be threatened. A couple of months ago I posted this Substack piece in the ShareScope chat feature.

I think the share price is almost certainly “wrong”. If the platform is about to collapse, we should start seeing it in the next 6-12 months and the shares are overvalued. If the forecasts are delivered and the court case dismissed, then the shares are almost certainly undervalued. Therein lies the opportunity for amateur investors, who might be able to enter/exit the investment case ahead of the professional fund managers.

I think the share price is almost certainly “wrong”. If the platform is about to collapse, we should start seeing it in the next 6-12 months and the shares are overvalued. If the forecasts are delivered and the court case dismissed, then the shares are almost certainly undervalued. Therein lies the opportunity for amateur investors, who might be able to enter/exit the investment case ahead of the professional fund managers.

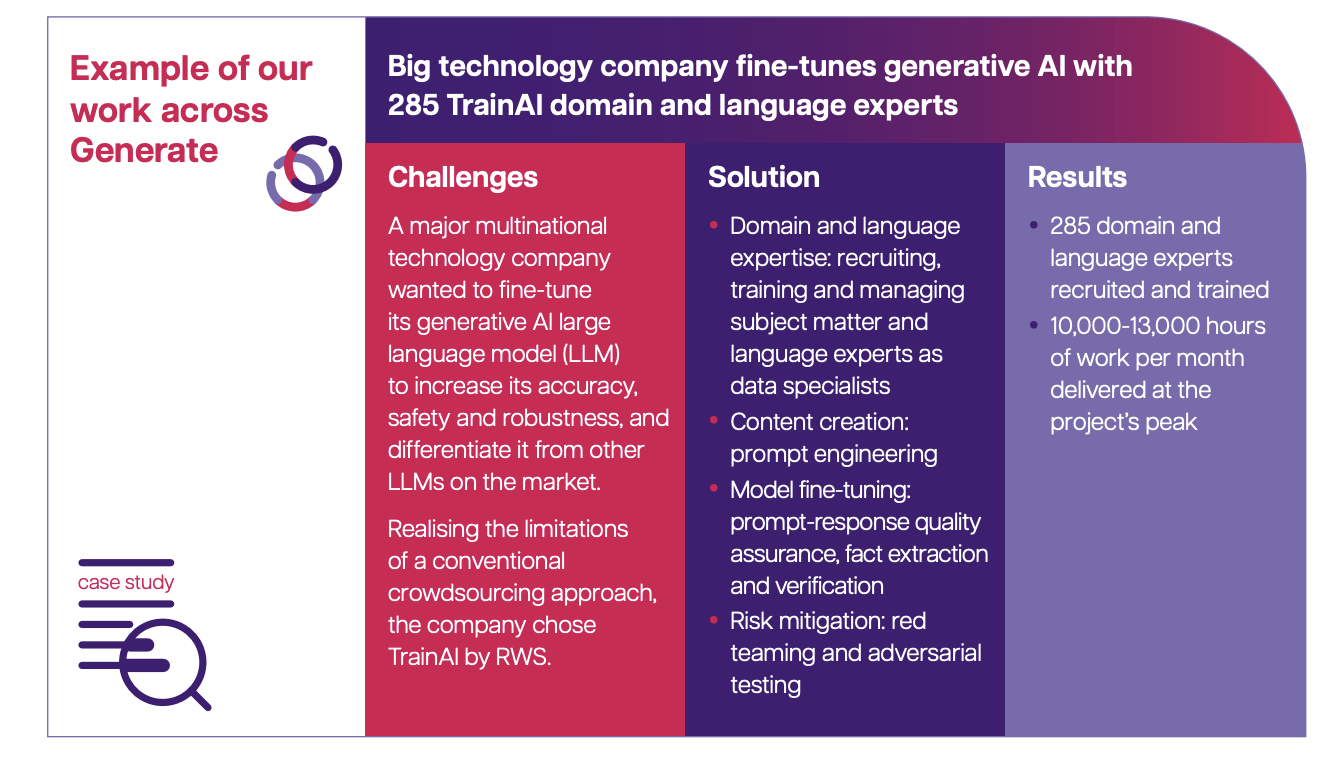

RWS to acquire Obviously

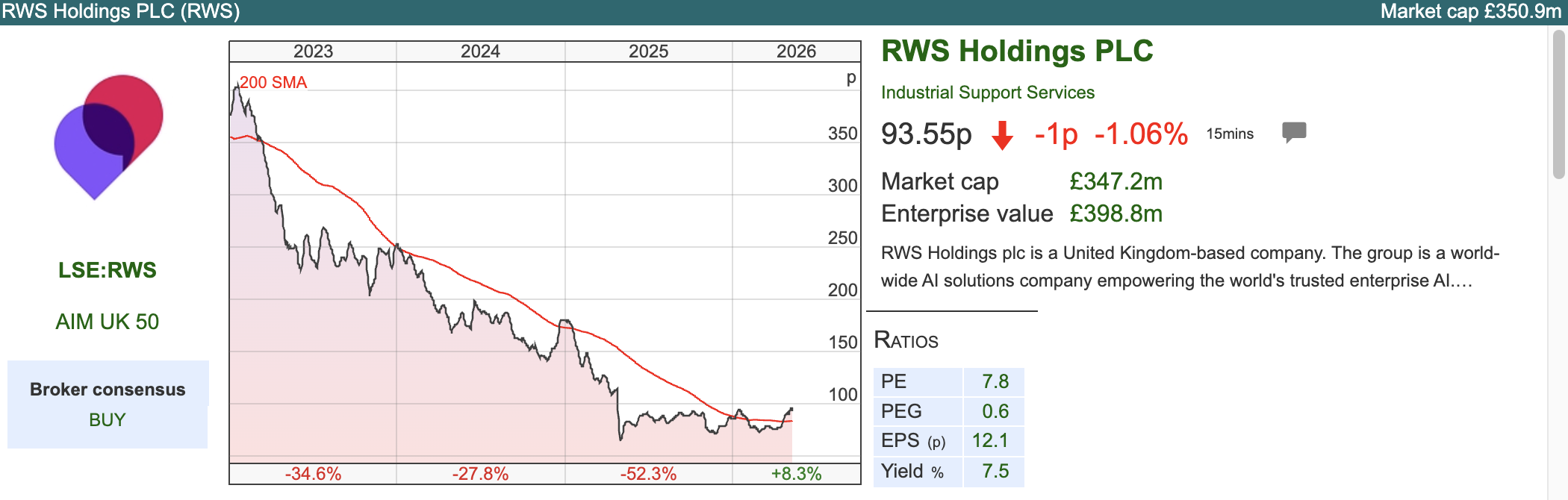

This language translation group has had a torrid time since November 2022, when OpenAI released their first version of ChatGPT to the public and LLMs became the focus of investor attention. I notice RWS management have changed how they describe themselves from “the world’s leading language services and technology group” in 2021 to instead be “a global AI solutions company empowering the world’s most trusted enterprise AI”.

This language translation group has had a torrid time since November 2022, when OpenAI released their first version of ChatGPT to the public and LLMs became the focus of investor attention. I notice RWS management have changed how they describe themselves from “the world’s leading language services and technology group” in 2021 to instead be “a global AI solutions company empowering the world’s most trusted enterprise AI”.

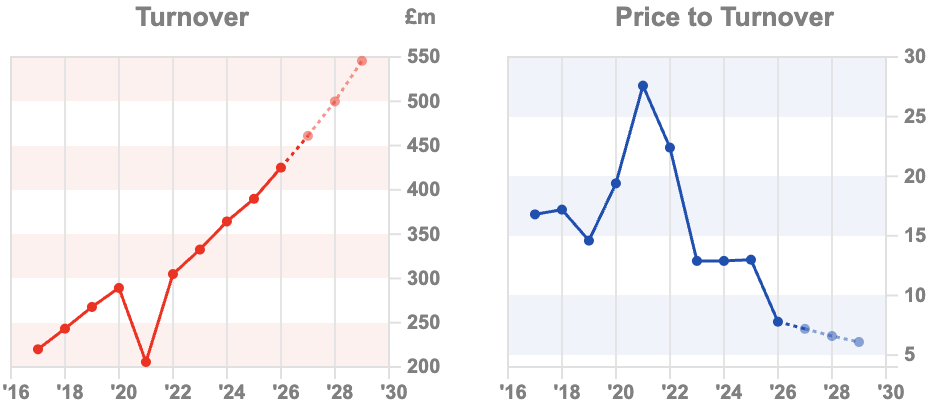

From a peak of £750m in FY Sept 2022 revenue has declined every year by around £20m. Nonetheless, the chart is suggesting that performance has stabilised, the group is now forecast to see a return to revenue growth (+3%) from the £690m reported FY Sept 2025. The group is also forecast to generate a whisker under £70m PBT FY Sept 2026F. The dividend is around 2x covered and yield is over 8%.

Last week they announced they would buy Obviously Group, who help companies manage and protect their Intellectual Property. Brand integrity effectively means scanning the internet for copyright, infringements, counterfeits and copycat products. Management think that if this deal goes ahead, their Total Addressable Market (TAM) could increase by c£2bn, as they can go into trademark and brand protection. RWS already has a division called “Protect” and they think they’ll take more market share of this existing market.

Last week they announced they would buy Obviously Group, who help companies manage and protect their Intellectual Property. Brand integrity effectively means scanning the internet for copyright, infringements, counterfeits and copycat products. Management think that if this deal goes ahead, their Total Addressable Market (TAM) could increase by c£2bn, as they can go into trademark and brand protection. RWS already has a division called “Protect” and they think they’ll take more market share of this existing market.

The acquisition price is £16.5m, rising to £40m total consideration if EBITDA performance hurdles are achieved. That equates to 6.6x headline price to revenues, rising to 16x price revenue if those hurdles are achieved in the following 3 years. So, not a large deal in the context of RWS group, but an indication of management confidence perhaps? RWS highlighted their turnaround plan at the end of last year, highlighting their understanding of fundamental client needs and new opportunities.

RWS suggest that their network of linguists are also subject-matter experts. Large corporations need “Human-in-the-Loop” (HITL) to trust the AI outputs particularly in areas like Life Sciences and Patent Law, where a mistake can costs millions.

Valuation: The shares are trading on 6x Sept 2027 PER. That translates to 3x EV/EBITDA the same year. Note that that ShareScope’s quality indicators are poor though; we’re yet to see evidence of a successful turnaround in the reported historic numbers.

Opinion: I think RWS is an early case study in how to respond to AI disruption. I rate Andrew Brodie, the founder, Chairman and 25% shareholder who took RWS public in 2003, by reversing into a shell at an implied market cap of less than £50m, seeing the group “20 bag” over the next couple of decades. He was also the Non Exec Chairman of Learning Technologies Group, acquired for £800m by US Private Equity at the end of 2024.

Opinion: I think RWS is an early case study in how to respond to AI disruption. I rate Andrew Brodie, the founder, Chairman and 25% shareholder who took RWS public in 2003, by reversing into a shell at an implied market cap of less than £50m, seeing the group “20 bag” over the next couple of decades. He was also the Non Exec Chairman of Learning Technologies Group, acquired for £800m by US Private Equity at the end of 2024.

There’s been a recent sell-off of enterprise technology stocks over fears of AI disruption, and translation services was an early victim of this a couple of years ago. So, even if you are wary of backing this turnaround, I think it’s worth paying attention to. We’re seeing an entrepreneurial management team engage with the threat and try to respond. I have no position, but the chart says the investment case might have found a support level.

There’s been a recent sell-off of enterprise technology stocks over fears of AI disruption, and translation services was an early victim of this a couple of years ago. So, even if you are wary of backing this turnaround, I think it’s worth paying attention to. We’re seeing an entrepreneurial management team engage with the threat and try to respond. I have no position, but the chart says the investment case might have found a support level.

Some thoughts from Benedict Evans.

I’ll leave you with some thoughts from Ben Evans. Ben was a telco’s analyst in the TMT bubble, but then pivoted to work for Andreessen Horowitz, the Venture Capital firm. He publishes a weekly tech round-up, with 200K subscribers, which has been going for almost 15 years.

“If a given model can make something “96% accurate” in a given domain, is that good or bad? In some domains, no human will be able to tell the difference, but in others that 4% could get someone killed. In principle, GenML models make something that looks like what you asked for, but they do not, in principle, make something that is what you asked for. So where is that useful and where is it dangerous? Extending this, I suspect there are a lot of use cases in the middle where the answer is ‘helpful, but I’ll need to check (and you can learn from what I check)’ – rather like asking an intern to produce a document for you.”

He first published that in January 2023. I think it holds up well 3.5 years later, and could be a useful framework for thinking about the investment case in RWS, Craneware, Future, LSEG, MONY, Next 15, RELX, RMV, YouGov and all the other stocks that have been sold-off over fears of AI disruption.

Bruce Packard

@bruce_packard

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Bi-Weekly Market Commentary | 13/05/2026 |CCT, RMV, RWS | Signals from the UK gilt market

Bruce Packard examines the sharp rise in UK gilt yields and what it signals for inflation, equities and investor sentiment. He also explores the AI disruption debate through the lens of CCT, RMV, RWS.

The UK 10 year government bond yield (ShareScope ticker UKTSY10) has broken above the 5% level, versus a historic low of just 7 basis points in August 2020. 7bp to lend to the UK government for 10 years! One of the main buyers of gilts back then was the Bank of England (Quantitative Easing), which is now being reversed and the Central Bank continues to sell down their position at a yield above 5%.

ShareScope also shows the steepness of the yield curve, the difference between the 2 year and 10 year gilts below. The curve was inverted for much of 2023 and 2024 (2 year yields above 10 year yields) often taken to be a signal of a coming recession. The recent “bear steepening” shows gilt investors are now more worried about persistent inflation.

These trends may turn out to be a positive for both the pound and owners of UK equities, as the investment case here looks attractive on a relative basis, particularly compared to UK property and US equities. While gilts have been weak, sterling has been strengthening (chart below).

This week I look at a couple of investment cases responding to the threat of Agentic AI: i) Rightmove’s AGM trading statement and ii) RWS the language translation services group that has made a small acquisition. I begin with Character Group’s significantly ahead of expectations guidance for FY Aug.

Character Group H1 Feb, FY Aug significantly above market expectations

H1 Feb PBT ex FX currency gains was up +14%, to £2.4m, despite H1 Feb revenues falling -9% to £48m. The H1 comparisons are particularly tough, as the previous H1 was before Trump’s tariffs. They have always operated with a conservative balance sheet, and net cash was £14m at the Feb half year. Inventory is less than £10m, so they’re not sitting on unsold stock. I had wrongly believed they no longer had any rights to make Peppa Pig, but reading the commentary they mention the arrival of Peppa’s baby sister Evie. They are still making Peppa complementary and adjacent toys, but Hasbro has in-sourced the core Peppa Pig manufacturing.

Property: Management are currently leasing out their warehouse in Lancashire and have written a call option, allowing the tenant to buy the property for just under £10m at the completion of the letting before the end of the current financial year end (August).

Outlook: Despite the H1 revenue decline, management suggest FY Aug results will be “significantly above current market expectations.” Within that, FY Aug revenue is likely to be flat, but helped by a well received product portfolio, an improved gross margin and a currency tail wind, should mean an encouraging performance despite tough markets. Allenby have raised FY Aug PBT by two thirds, from £3m to £5m.

Valuation: The shares are trading on a PER of 12x Allenby’s upgraded FY Aug 2026F adj EPS estimate and 5x EV/EBITDA the same year. There are no FY Aug 2027F forecasts yet though, suggesting management don’t feel particularly confident in the outlook for next year.

Rightmove AGM Trading statement

Then the shares fell -16% in November last year, when management said they would spend £18m (£12m expensed through the P&L and £6m of capitalised investment added to the balance sheet) on software development and other intangible spend to defend their “moat”. That compares to £290m of PBT FY Dec 2025.

This year there’s been a court case, where estate agents (who pay Rightmove to advertise properties on the platform) say RMV are abusing its dominant market position by charging estate agents excessive fees. This case is being backed by Innsworth Advisors, the litigation finance arm of Paul Singer’s Elliot hedge fund. The headline cost of redress is suggested at £1.5bn. The shares have roughly halved from their mid 2025 peak of 827p.

Opinion: I think I will put RMV in the “too hard” pile for now. There’s an obvious disconnect between continuing rising EPS forecasts and a share price that has collapsed on understandable, but hard to quantify, fears of disruption. The disruption fear is that AI Agents will be able execute multi-step workflows, thus RMV’s “moat” could be threatened. A couple of months ago I posted this Substack piece in the ShareScope chat feature.

RWS to acquire Obviously

From a peak of £750m in FY Sept 2022 revenue has declined every year by around £20m. Nonetheless, the chart is suggesting that performance has stabilised, the group is now forecast to see a return to revenue growth (+3%) from the £690m reported FY Sept 2025. The group is also forecast to generate a whisker under £70m PBT FY Sept 2026F. The dividend is around 2x covered and yield is over 8%.

The acquisition price is £16.5m, rising to £40m total consideration if EBITDA performance hurdles are achieved. That equates to 6.6x headline price to revenues, rising to 16x price revenue if those hurdles are achieved in the following 3 years. So, not a large deal in the context of RWS group, but an indication of management confidence perhaps? RWS highlighted their turnaround plan at the end of last year, highlighting their understanding of fundamental client needs and new opportunities.

RWS suggest that their network of linguists are also subject-matter experts. Large corporations need “Human-in-the-Loop” (HITL) to trust the AI outputs particularly in areas like Life Sciences and Patent Law, where a mistake can costs millions.

Valuation: The shares are trading on 6x Sept 2027 PER. That translates to 3x EV/EBITDA the same year. Note that that ShareScope’s quality indicators are poor though; we’re yet to see evidence of a successful turnaround in the reported historic numbers.

Some thoughts from Benedict Evans.

I’ll leave you with some thoughts from Ben Evans. Ben was a telco’s analyst in the TMT bubble, but then pivoted to work for Andreessen Horowitz, the Venture Capital firm. He publishes a weekly tech round-up, with 200K subscribers, which has been going for almost 15 years.

“If a given model can make something “96% accurate” in a given domain, is that good or bad? In some domains, no human will be able to tell the difference, but in others that 4% could get someone killed. In principle, GenML models make something that looks like what you asked for, but they do not, in principle, make something that is what you asked for. So where is that useful and where is it dangerous? Extending this, I suspect there are a lot of use cases in the middle where the answer is ‘helpful, but I’ll need to check (and you can learn from what I check)’ – rather like asking an intern to produce a document for you.”

He first published that in January 2023. I think it holds up well 3.5 years later, and could be a useful framework for thinking about the investment case in RWS, Craneware, Future, LSEG, MONY, Next 15, RELX, RMV, YouGov and all the other stocks that have been sold-off over fears of AI disruption.

Bruce Packard

@bruce_packard

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.