Even as equity markets have rebounded, some early warning indicators are showing consumer sentiment has deteriorated. Companies covered: THG, CCC and BGO.

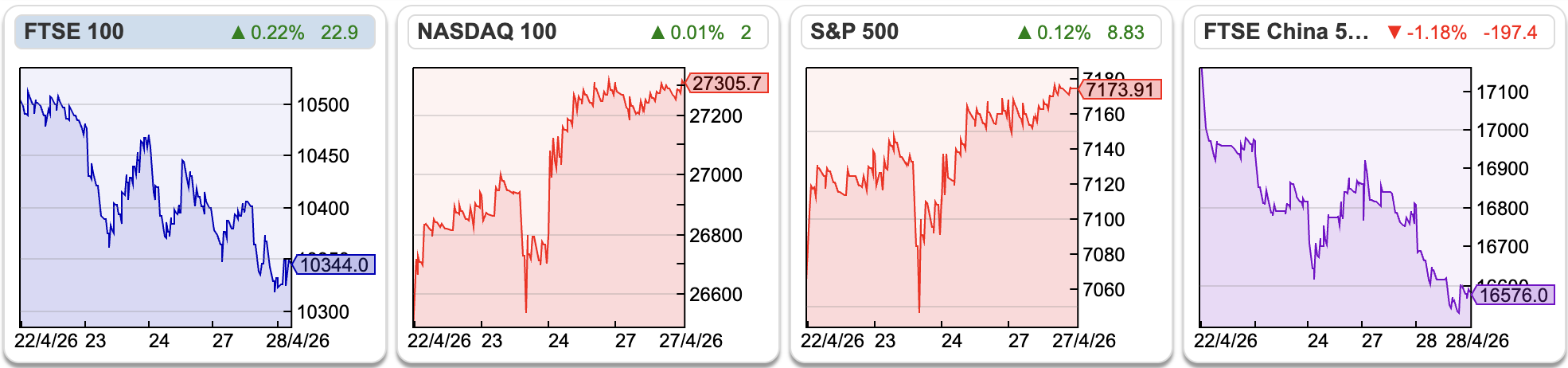

Brent Crude (BR$SP) has risen to $104 per barrel and is now up +47% since 26th February, when hostilities began in Iran. Natural Gas prices have been diverging between the USA and Europe, so I am now following EGAS (Wisdom Tree European Natural Gas Exchange Traded Commodity) +43% since 26th February.

Brent Crude (BR$SP) has risen to $104 per barrel and is now up +47% since 26th February, when hostilities began in Iran. Natural Gas prices have been diverging between the USA and Europe, so I am now following EGAS (Wisdom Tree European Natural Gas Exchange Traded Commodity) +43% since 26th February.

Although US equity markets are not currently showing signs of problems, there are signs of consumer sentiment deteriorating. In the US the University of Michigan Survey of Consumers April reading was 49, much weaker than March and among the softest readings on record. In the UK the April the GfK Consumer Confidence Barometer has fallen for three months in a row. These surveys reflect consumer sentiment (how we feel) and tend to be more forward looking than data points like unemployment, which is a lagging indicator.

Although US equity markets are not currently showing signs of problems, there are signs of consumer sentiment deteriorating. In the US the University of Michigan Survey of Consumers April reading was 49, much weaker than March and among the softest readings on record. In the UK the April the GfK Consumer Confidence Barometer has fallen for three months in a row. These surveys reflect consumer sentiment (how we feel) and tend to be more forward looking than data points like unemployment, which is a lagging indicator.

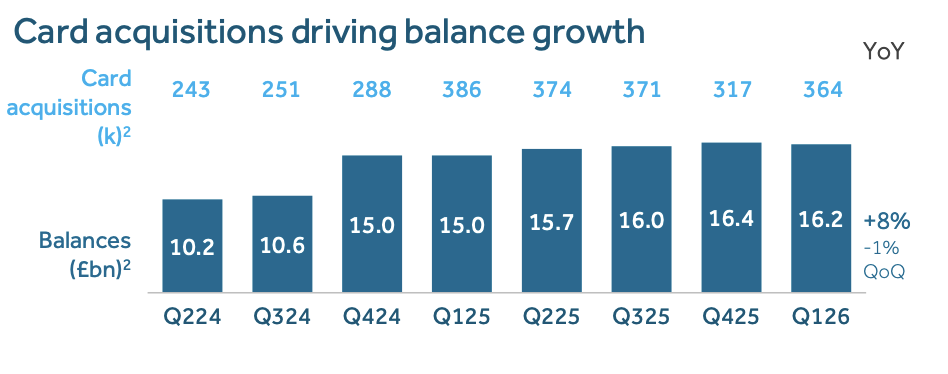

Bear in mind that credit card borrowing is currently growing at +12% in the UK, around 4x the rate of UK mortgage growth. Barclaycard UK, with £16bn of card balances, is the largest credit card company in the UK. Management seem to have taken a step back in Q1 with balances down -1%, perhaps taking their foot off the accelerator as they fear credit quality deterioration in the second half. Barclaycard reveals that in Q1 this year their 30 and 90 day arrears rates are beginning to rise to 0.9% (Q125: 0.7%) and 0.3% (Q125: 0.2%) from a low level.

These indicators are potentially early warning indicators of a more difficult H2. AXX has rebounded strongly +12% since the end of March, and I have taken the opportunity to sell some of my lower conviction and less liquid positions. I could be wrong, I will wait and see for a couple of months.

These indicators are potentially early warning indicators of a more difficult H2. AXX has rebounded strongly +12% since the end of March, and I have taken the opportunity to sell some of my lower conviction and less liquid positions. I could be wrong, I will wait and see for a couple of months.

This week I look at Computacenter’s “comfortably ahead” update and Bango’s diverging revenue growth between Payments and Subscriptions business division, revealed in their FY Dec 2025 results. But I start with THG, the beauty and nutrition brand Q1 March trading update.

THG Q1 March trading update

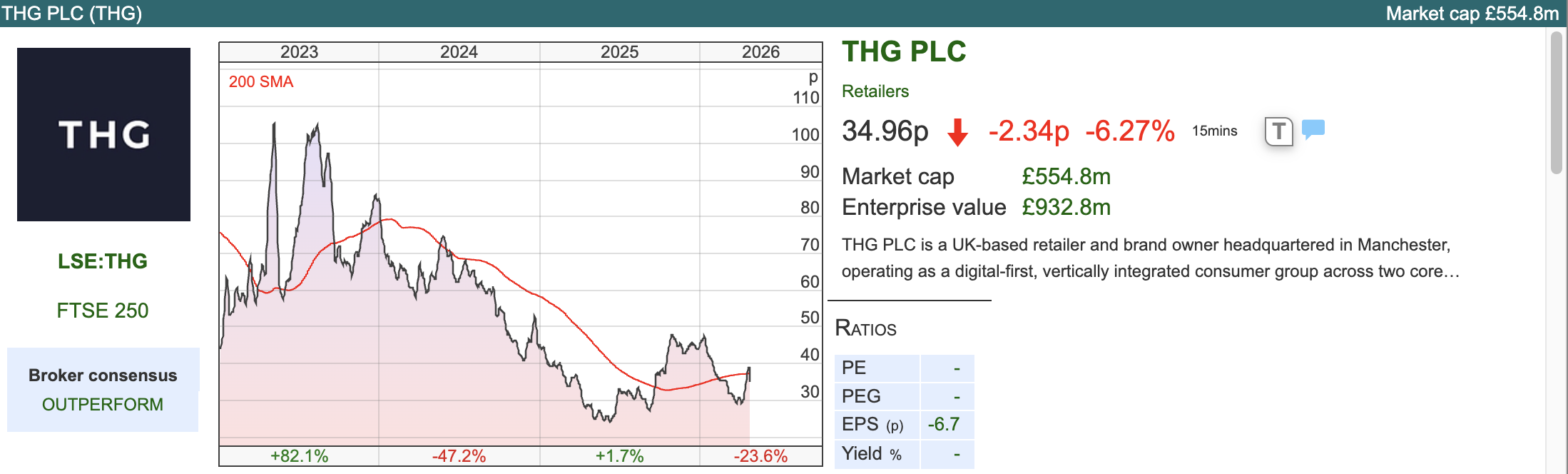

This Manchester headquartered online beauty and nutrition brand was (yet another) 2020 IPO at an over inflated price, subsequently collapsing -95%. Similar to Callnex, which I wrote about earlier this month, I think the chart now may have bottomed, and investors could do worse than fishing in the pool of pandemic era IPO’s that have disappointed, but now stabilised. I wonder why professional fund managers ever backed these investments at the wrong price though; seems like a good argument for using Sharescope to do your own investing.

This Manchester headquartered online beauty and nutrition brand was (yet another) 2020 IPO at an over inflated price, subsequently collapsing -95%. Similar to Callnex, which I wrote about earlier this month, I think the chart now may have bottomed, and investors could do worse than fishing in the pool of pandemic era IPO’s that have disappointed, but now stabilised. I wonder why professional fund managers ever backed these investments at the wrong price though; seems like a good argument for using Sharescope to do your own investing.

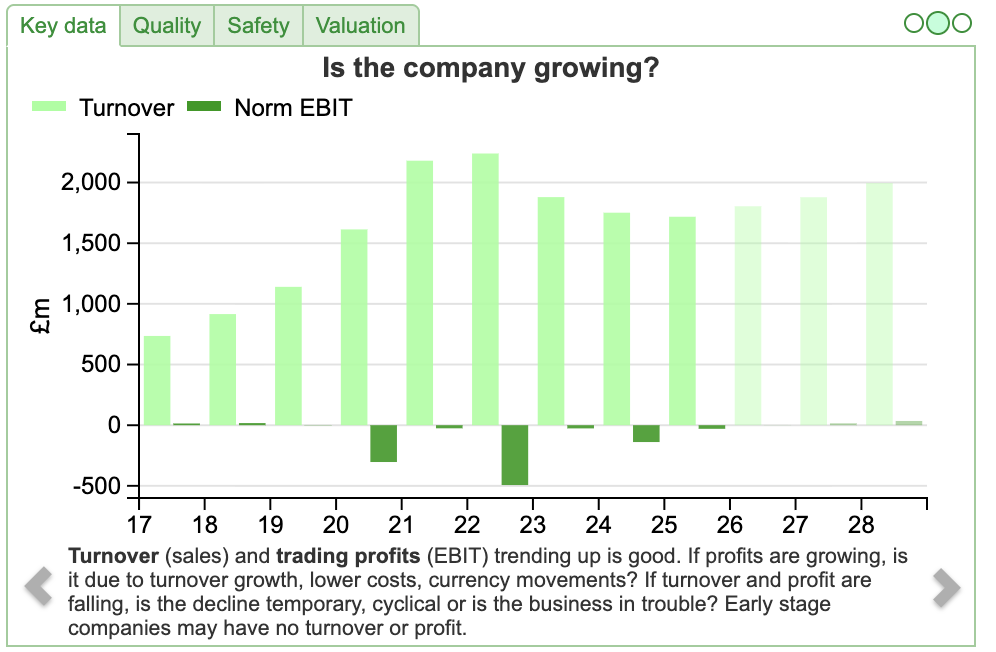

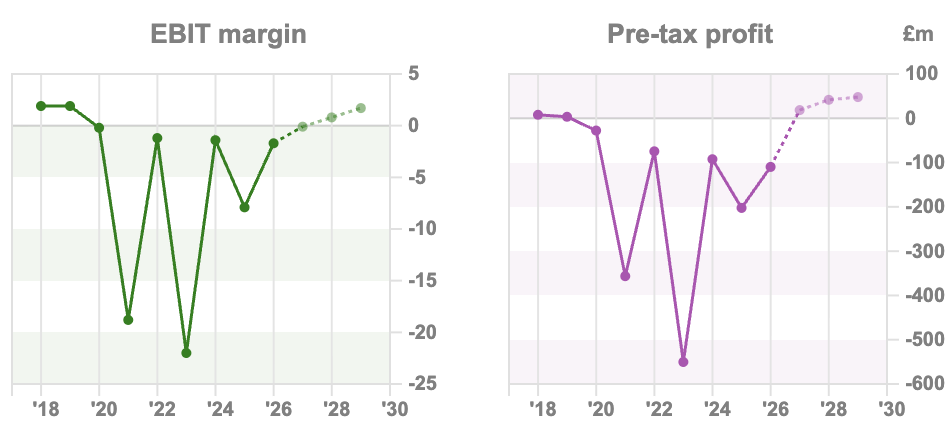

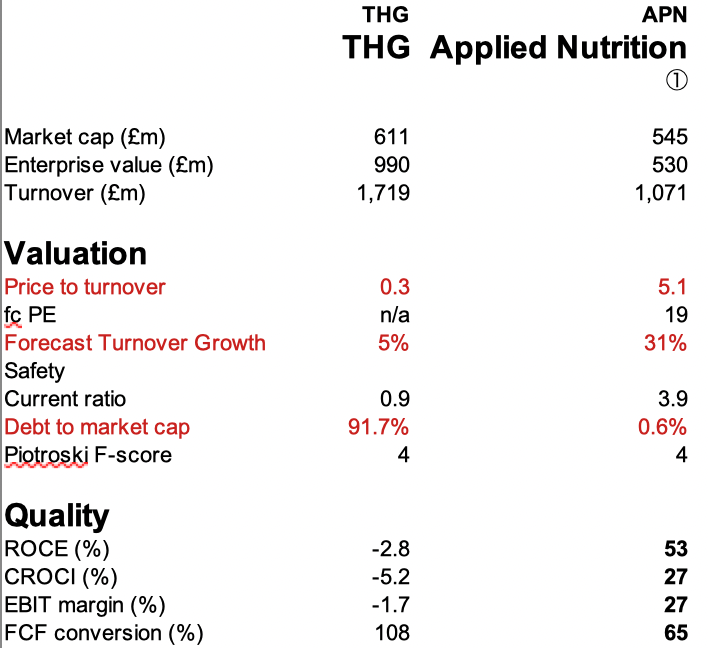

The Beauty division which is just under 60% of group revenue, and includes Lookfantastic, Dermstore and Jessica DeLuca’s Cult Beauty grew +6% on a continuing basis. Nutrition, led by the Myprotein brand, just over 40% of group revenue, grew +9%. Taking a longer term view, Sharescope reveals that revenue peaked at £2.2bn FY Dec 2022, and has declined by -23% to £1.7bn 3 years later. The group has never made a profit as a listed company, but is forecast to now grow the topline at mid single digits and (just about) break even FY Dec 2026F.

There’s plenty of competition in the health and sports nutrition sector, Applied Nutrition expects to grow FY Jul revenue by +30% to £140m, according to ShareScope’s forecast page. Supreme also announced last week a 5 year licensing deal with Carabao, the energy drink brand, who sponsor the Football League Cup (which I remember when it used to be the “Milk Cup”).

There’s plenty of competition in the health and sports nutrition sector, Applied Nutrition expects to grow FY Jul revenue by +30% to £140m, according to ShareScope’s forecast page. Supreme also announced last week a 5 year licensing deal with Carabao, the energy drink brand, who sponsor the Football League Cup (which I remember when it used to be the “Milk Cup”).

THG’s RNS doesn’t mention net debt, but at FY Dec this stood at £364m, or £233m before lease liabilities. At the start of 2025, THG de-merger their loss making e-commerce platform Ingenuity, which was the majority of the Group’s leases. Management raised £90m to fund the “take private” deal, with Matt Moulding the founder/CEO contributing £60m, most of which was a convertible loan and a placing of £30m at 32p per share.

Outlook: FY Dec 2026 guidance of +5% revenue growth with an adj EBITDA margin of 5.7%. They say this is underpinned by continued market share gains in key territories, though APN is growing roughly 6x faster. It is not clear how THG measure market share. Management are fans of adj EBITDA, rather than profit or EPS guidance, so the latter are not available as consensus forecast on THG’s investor relations website.

HMRC tax catalyst: There’s also this fun post by FT Alphaville, suggesting it’s possible that THG has been overpaying VAT on their MyProtein whey powder products. A product designed to build muscle and marketed at gym users should pay standard-rated VAT, but a weight loss product and marketed at slimmers is zero-rated under VAT rules. It’s possible to conceive of a product, with the same ingredients (protein, vitamins etc) but different marketing being treated differently by the tax authorities. A successful claim by the group would result in a cash payment of c.£78m, comprising c.£60m on protein powders and the further c.£18m on certain supplements. Have a read of the blog post and see what you think.

Valuation: ShareScope shows the group trading on 0.3 price/sales and 8x EV/EBITDA Dec 2026F. For comparison, APN trades on 4x price/sales and 13x EV/EBITDA Dec 2026F. I’ve used Sharescope’s “compare” feature, and downloaded the key data points into MS Excel. It strikes me that APN looks better on most profitability metrics, like RoCE and EBIT margin – and the valuation ratios are reflecting that. The question is whether the weak management team at THG can improve performance.

Opinion: The investment case here rests on what you think of the brands, you would expect to see a decent operating margin at some point in the foreseeable future if the brands are valuable. Unlike a B2B SaaS group, whey protein shakes and beauty products are areas where we can test the brands ourselves and ask our friends about their buying behaviour. It’s unscientific, but might just provide some insight that professional fund managers miss. Certainly the institutional investors who put their clients money into THG at the IPO price haven’t covered themselves in glory. I’ll pass on this for now.

Computacenter Q1 Trading “Comfortably Ahead”

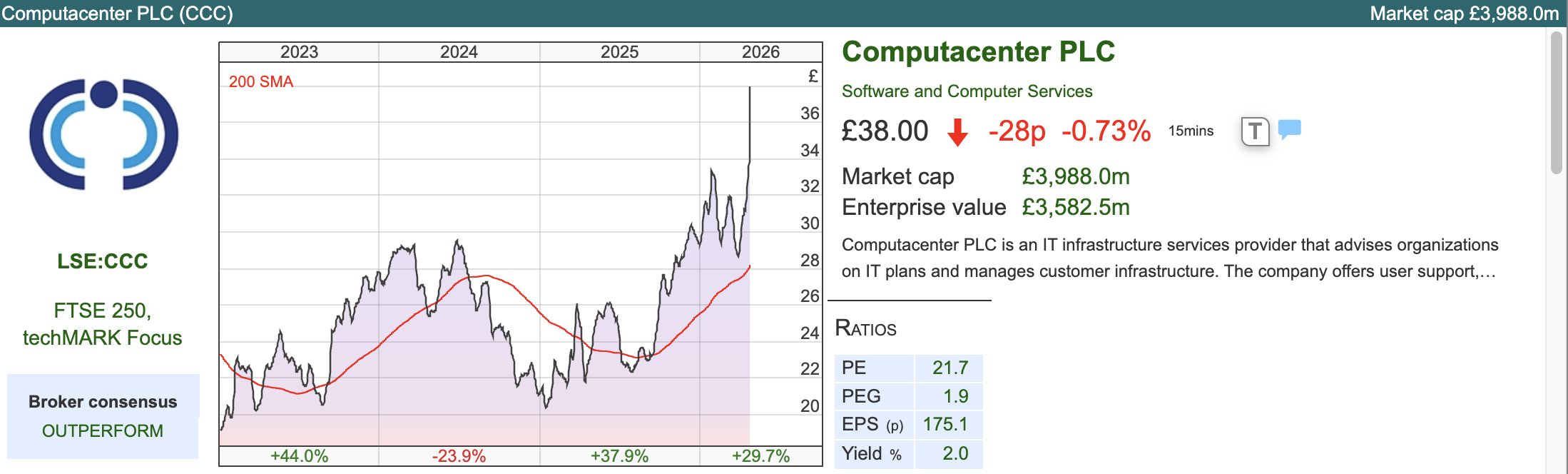

It’s understandable to conflate consistently low margin companies with poor performance. That would be a mistake though, sometimes groups can do very well with high volume, low margin strategies. CCC re-sells technology hardware, with some consultancy and project management. The long term chart (15 years, log scale) reveals that CCC has been a quality compounder, despite EBIT margins oscillating between 3% and 5%. The trend has continued as the share price enjoyed a strong start to 2026, +30% YTD.

It’s understandable to conflate consistently low margin companies with poor performance. That would be a mistake though, sometimes groups can do very well with high volume, low margin strategies. CCC re-sells technology hardware, with some consultancy and project management. The long term chart (15 years, log scale) reveals that CCC has been a quality compounder, despite EBIT margins oscillating between 3% and 5%. The trend has continued as the share price enjoyed a strong start to 2026, +30% YTD.

In one sense, Computacenter is a “middleman”, who theoretically shouldn’t exist because large corporations could just buy their technology direct from vendors; in reality though 70% of corporate IT sales are made through re-sellers. It’s more efficient for Dell or HP to sell their tech to CCC at a discount, then the re-seller invests in the sales relationship and customer support.

In one sense, Computacenter is a “middleman”, who theoretically shouldn’t exist because large corporations could just buy their technology direct from vendors; in reality though 70% of corporate IT sales are made through re-sellers. It’s more efficient for Dell or HP to sell their tech to CCC at a discount, then the re-seller invests in the sales relationship and customer support.

At the FY Dec stage revenue was up +33%, and that momentum has continued into 2026 with Q1 well above management expectations. This was driven by the hyperscalers (in other words Amazon (AWS), Microsoft, Google, Meta, Oracle, and IBM) investing in datacentres, with CCC reporting North American revenue growth +70% last year. Great to see a UK listed group benefitting from the AI “arms race.”

Outlook: Looking to 2026, management now expect a “much stronger” H1 than previously anticipated. For FY Dec 2026F they are sounding a little more cautious. Assuming no significant deterioration to the external backdrop, they are now guiding “comfortably ahead” of FY Dec 2026 adj PBT of £291m (range £284m to £297m).

Valuation: The shares are trading on 19x PER this year, dropping to 18x Dec 2027F. That equates to 0.4x sales (as you would expect for a group with an EBIT margin of close to 3%). On an EV/EBITDA basis they’re on 9x Dec 2026F.

Opinion: The investment case he rests on how long you think the current trend of datacenter buildout is going to last. I’m cautious about H2 generally. Hostilities in the Gulf are taking time to have an effect by we could see higher food prices, corporate capex may also be reduced as we face re-financing of all the corporate bonds issued at much lower rates. Computacenter’s revenue did fall -7% during the pandemic, so I don’t think we should extrapolate recent strong performance too far into the future.

It’s a great company, enjoying a favourable tail wind. The contrarian in me would prefer to buy these type of investments when they’re out of favour. During the pandemic the shares fell below £10 per share, so there maybe better entry points?

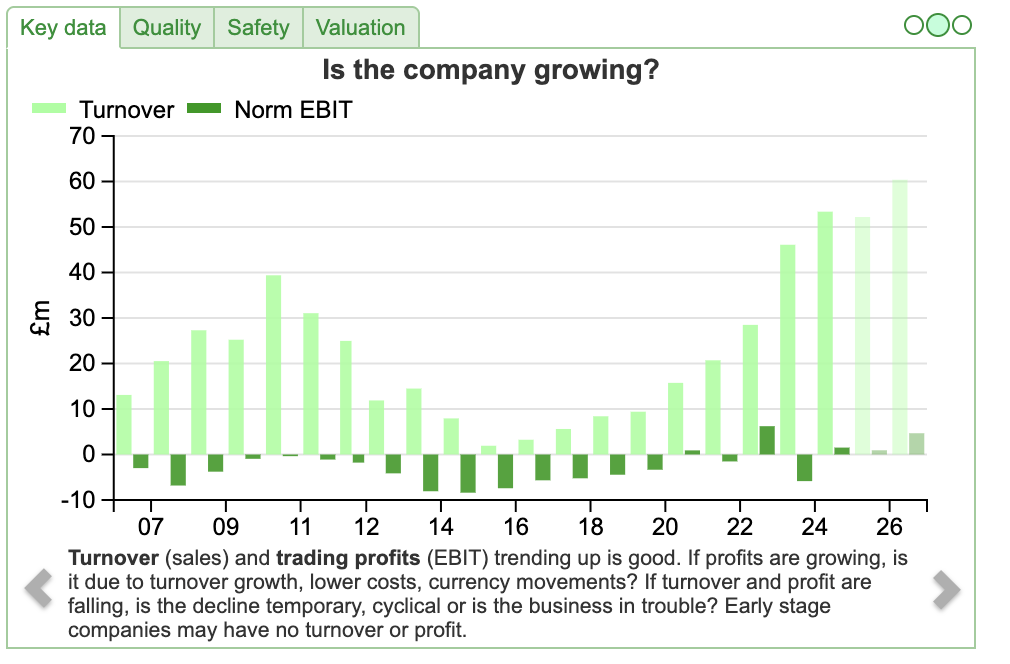

Bango FY Dec 2025 Results

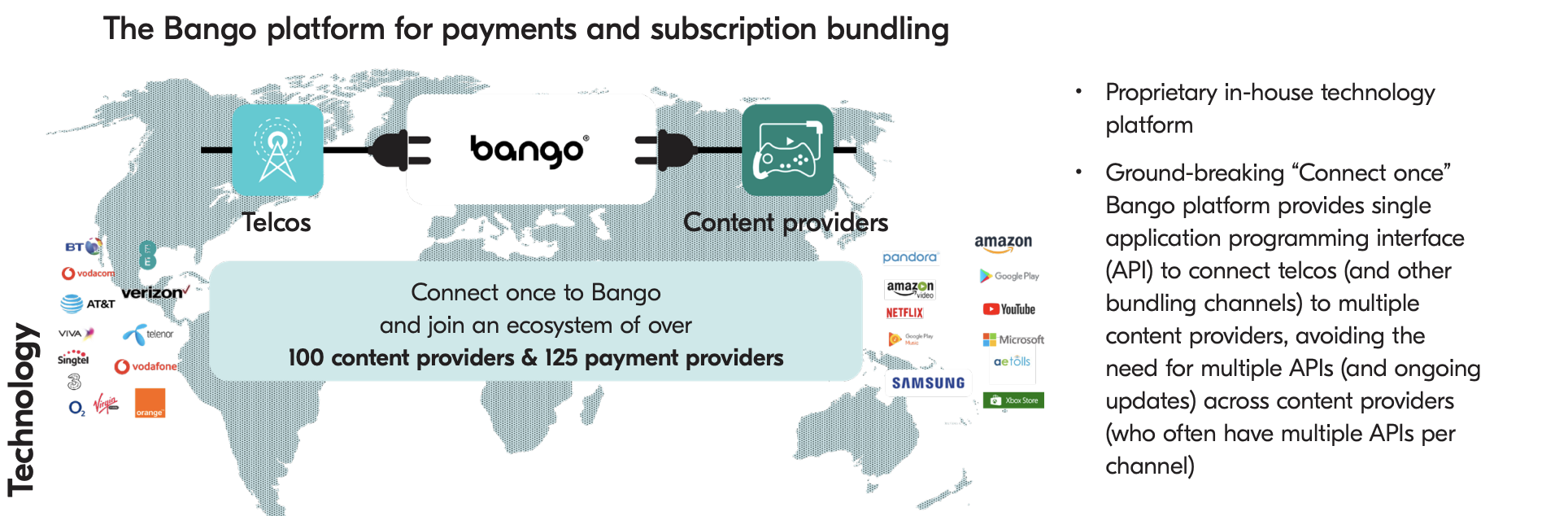

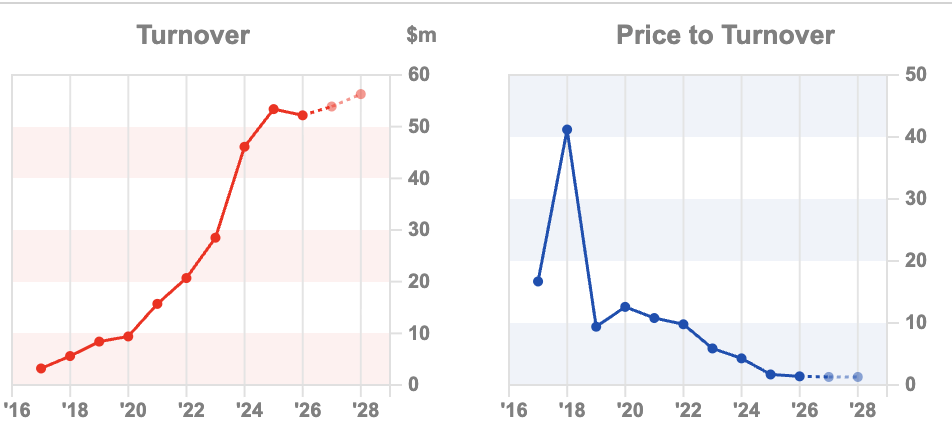

This Direct Carrier Billing (DCB) company, with a long history of losses has been listed on AIM for 20 years. They’ve always had a strong story, about facilitating digital payments through your phone, without a payment card or bank account needed to complete transactions. The revenue growth did eventually come through but that hasn’t helped them to generate profits. I last looked at the group in 2022, and suggested that the valuation of 6x sales for a group with such a poor track record was unattractive, even if revenue was forecast to grow strongly (revenue doubled from 2021 to 2024).

This Direct Carrier Billing (DCB) company, with a long history of losses has been listed on AIM for 20 years. They’ve always had a strong story, about facilitating digital payments through your phone, without a payment card or bank account needed to complete transactions. The revenue growth did eventually come through but that hasn’t helped them to generate profits. I last looked at the group in 2022, and suggested that the valuation of 6x sales for a group with such a poor track record was unattractive, even if revenue was forecast to grow strongly (revenue doubled from 2021 to 2024).

Now the FY Dec 2025 results show revenue growth has stalled: -2% to $52m, and adj EBITDA +7% to $16m. Naturally, no sign of statutory profits on the front page (the p&l shows that losses before tax were $7m), and cashflow from operating activities more than halved from ($19m to $8m). Amply demonstrating why investors should be sceptical of any management team who wish to emphasise adj EBITDA.

Now the FY Dec 2025 results show revenue growth has stalled: -2% to $52m, and adj EBITDA +7% to $16m. Naturally, no sign of statutory profits on the front page (the p&l shows that losses before tax were $7m), and cashflow from operating activities more than halved from ($19m to $8m). Amply demonstrating why investors should be sceptical of any management team who wish to emphasise adj EBITDA.

That’s a disappointing performance, because I had hoped that as the business grew revenue from below $10m in FY Dec 2019, management would be able to demonstrate operational gearing from their “platform”. Despite expanding the gross margin to 84% that was not the case. Similarly, the group has net debt of $9m, up from below $2m Dec 2024 so they can’t continue to fund losses for much longer. Note too that there is $42m of intangible assets on the balance sheet, after the group has capitalised significant R&D spending, double shareholders equity of $21m. So net tangible equity is negative $21m.

Divisional trends: There is a little more to the story though. Management intend to improve disclosure and introduce divisional reporting to help investors understand the trends. The Payments division, just under 60% of group revenue, has adj EBITDA margins of 40% and provides a stable cash generative base. But revenue has declined by -15% in this division in 2025. The Subscription division, just over 40% of group revenue, is a Digital Vending Machine (DVM) which is a bet on consumers are getting “subscription fatigue.” Instead of managing 10 different direct debits, people want to be able to manage (and cancel!) their subscriptions on centralised hub, which Bango provides the plumbing for. Revenue grew +22% in this division in 2025, but has only just reached adj EBITDA breakeven. Management claim high incremental margins and operational gearing – though after 20 years of losses, perhaps we should be a circumspect.

Outlook: The FY results also include a Q1 update. Group revenue for Q1 FY Dec 2026 was up +13% versus Q1 the previous year. Adj EBITDA increased +39%, driven by that revenue growth and the effect of the cost reductions made last year. They note that events in the Gulf have not yet had an impact, but they strike a cautious tone for the rest of the year, while still trying to sound positive about medium term prospects. There was an RNS in January, where management warned that several large DVM opportunities would be delayed from the final quarter of FY Dec 2025 into FY Dec 2026F due to extended customer processes; those deals were not yet signed when the RNS was released at the end of April.

Valuation: Bango is trading on 20x PER Dec 2027F, the price/sales ratio has fallen to 1.3x versus a peak of 40x pre-pandemic. Competitor Boku, also does mobile payments and digital wallets and trades on 18x PER Dec 2027F, 4x sales and EV/EBITDA of 10x the same year. So a higher rating, but also an EBIT margin approaching 20% and RoCE of 15% for Boku, like THG/APN superior profitability track record reflected in higher valuation multiples.

Opinion: You can sense my scepticism towards Bango, but mobile payments still worth following, I think? If the DVM idea really takes off, then it will dominate the investment case. I like the idea in theory, I have too many subscriptions, and I think US tech companies deliberately target the inertia of their customers. Management reported 12 new Digital Vending Machine® (DVM™) last year, and a further 3 wins in Q1 this year, bringing DVM customers to over 40 and active subscriptions +60% to 24m consumers.

So, if Bango has hit on a service that helps consumers and which is hard for competitors to copy then this could really go somewhere. Given past disappointment not a high conviction idea, but just flagging the investment case as having potential.

Bruce Packard

@bruce_packard

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Bi-Weekly Market Commentary | 29/04/2026 |THG, CCC, BGO | Consumers under pressure

Even as equity markets have rebounded, some early warning indicators are showing consumer sentiment has deteriorated. Companies covered: THG, CCC and BGO.

Bear in mind that credit card borrowing is currently growing at +12% in the UK, around 4x the rate of UK mortgage growth. Barclaycard UK, with £16bn of card balances, is the largest credit card company in the UK. Management seem to have taken a step back in Q1 with balances down -1%, perhaps taking their foot off the accelerator as they fear credit quality deterioration in the second half. Barclaycard reveals that in Q1 this year their 30 and 90 day arrears rates are beginning to rise to 0.9% (Q125: 0.7%) and 0.3% (Q125: 0.2%) from a low level.

This week I look at Computacenter’s “comfortably ahead” update and Bango’s diverging revenue growth between Payments and Subscriptions business division, revealed in their FY Dec 2025 results. But I start with THG, the beauty and nutrition brand Q1 March trading update.

THG Q1 March trading update

The Beauty division which is just under 60% of group revenue, and includes Lookfantastic, Dermstore and Jessica DeLuca’s Cult Beauty grew +6% on a continuing basis. Nutrition, led by the Myprotein brand, just over 40% of group revenue, grew +9%. Taking a longer term view, Sharescope reveals that revenue peaked at £2.2bn FY Dec 2022, and has declined by -23% to £1.7bn 3 years later. The group has never made a profit as a listed company, but is forecast to now grow the topline at mid single digits and (just about) break even FY Dec 2026F.

THG’s RNS doesn’t mention net debt, but at FY Dec this stood at £364m, or £233m before lease liabilities. At the start of 2025, THG de-merger their loss making e-commerce platform Ingenuity, which was the majority of the Group’s leases. Management raised £90m to fund the “take private” deal, with Matt Moulding the founder/CEO contributing £60m, most of which was a convertible loan and a placing of £30m at 32p per share.

Outlook: FY Dec 2026 guidance of +5% revenue growth with an adj EBITDA margin of 5.7%. They say this is underpinned by continued market share gains in key territories, though APN is growing roughly 6x faster. It is not clear how THG measure market share. Management are fans of adj EBITDA, rather than profit or EPS guidance, so the latter are not available as consensus forecast on THG’s investor relations website.

HMRC tax catalyst: There’s also this fun post by FT Alphaville, suggesting it’s possible that THG has been overpaying VAT on their MyProtein whey powder products. A product designed to build muscle and marketed at gym users should pay standard-rated VAT, but a weight loss product and marketed at slimmers is zero-rated under VAT rules. It’s possible to conceive of a product, with the same ingredients (protein, vitamins etc) but different marketing being treated differently by the tax authorities. A successful claim by the group would result in a cash payment of c.£78m, comprising c.£60m on protein powders and the further c.£18m on certain supplements. Have a read of the blog post and see what you think.

Valuation: ShareScope shows the group trading on 0.3 price/sales and 8x EV/EBITDA Dec 2026F. For comparison, APN trades on 4x price/sales and 13x EV/EBITDA Dec 2026F. I’ve used Sharescope’s “compare” feature, and downloaded the key data points into MS Excel. It strikes me that APN looks better on most profitability metrics, like RoCE and EBIT margin – and the valuation ratios are reflecting that. The question is whether the weak management team at THG can improve performance.

Opinion: The investment case here rests on what you think of the brands, you would expect to see a decent operating margin at some point in the foreseeable future if the brands are valuable. Unlike a B2B SaaS group, whey protein shakes and beauty products are areas where we can test the brands ourselves and ask our friends about their buying behaviour. It’s unscientific, but might just provide some insight that professional fund managers miss. Certainly the institutional investors who put their clients money into THG at the IPO price haven’t covered themselves in glory. I’ll pass on this for now.

Computacenter Q1 Trading “Comfortably Ahead”

At the FY Dec stage revenue was up +33%, and that momentum has continued into 2026 with Q1 well above management expectations. This was driven by the hyperscalers (in other words Amazon (AWS), Microsoft, Google, Meta, Oracle, and IBM) investing in datacentres, with CCC reporting North American revenue growth +70% last year. Great to see a UK listed group benefitting from the AI “arms race.”

Outlook: Looking to 2026, management now expect a “much stronger” H1 than previously anticipated. For FY Dec 2026F they are sounding a little more cautious. Assuming no significant deterioration to the external backdrop, they are now guiding “comfortably ahead” of FY Dec 2026 adj PBT of £291m (range £284m to £297m).

Valuation: The shares are trading on 19x PER this year, dropping to 18x Dec 2027F. That equates to 0.4x sales (as you would expect for a group with an EBIT margin of close to 3%). On an EV/EBITDA basis they’re on 9x Dec 2026F.

Opinion: The investment case he rests on how long you think the current trend of datacenter buildout is going to last. I’m cautious about H2 generally. Hostilities in the Gulf are taking time to have an effect by we could see higher food prices, corporate capex may also be reduced as we face re-financing of all the corporate bonds issued at much lower rates. Computacenter’s revenue did fall -7% during the pandemic, so I don’t think we should extrapolate recent strong performance too far into the future.

It’s a great company, enjoying a favourable tail wind. The contrarian in me would prefer to buy these type of investments when they’re out of favour. During the pandemic the shares fell below £10 per share, so there maybe better entry points?

Bango FY Dec 2025 Results

That’s a disappointing performance, because I had hoped that as the business grew revenue from below $10m in FY Dec 2019, management would be able to demonstrate operational gearing from their “platform”. Despite expanding the gross margin to 84% that was not the case. Similarly, the group has net debt of $9m, up from below $2m Dec 2024 so they can’t continue to fund losses for much longer. Note too that there is $42m of intangible assets on the balance sheet, after the group has capitalised significant R&D spending, double shareholders equity of $21m. So net tangible equity is negative $21m.

Divisional trends: There is a little more to the story though. Management intend to improve disclosure and introduce divisional reporting to help investors understand the trends. The Payments division, just under 60% of group revenue, has adj EBITDA margins of 40% and provides a stable cash generative base. But revenue has declined by -15% in this division in 2025. The Subscription division, just over 40% of group revenue, is a Digital Vending Machine (DVM) which is a bet on consumers are getting “subscription fatigue.” Instead of managing 10 different direct debits, people want to be able to manage (and cancel!) their subscriptions on centralised hub, which Bango provides the plumbing for. Revenue grew +22% in this division in 2025, but has only just reached adj EBITDA breakeven. Management claim high incremental margins and operational gearing – though after 20 years of losses, perhaps we should be a circumspect.

Outlook: The FY results also include a Q1 update. Group revenue for Q1 FY Dec 2026 was up +13% versus Q1 the previous year. Adj EBITDA increased +39%, driven by that revenue growth and the effect of the cost reductions made last year. They note that events in the Gulf have not yet had an impact, but they strike a cautious tone for the rest of the year, while still trying to sound positive about medium term prospects. There was an RNS in January, where management warned that several large DVM opportunities would be delayed from the final quarter of FY Dec 2025 into FY Dec 2026F due to extended customer processes; those deals were not yet signed when the RNS was released at the end of April.

Valuation: Bango is trading on 20x PER Dec 2027F, the price/sales ratio has fallen to 1.3x versus a peak of 40x pre-pandemic. Competitor Boku, also does mobile payments and digital wallets and trades on 18x PER Dec 2027F, 4x sales and EV/EBITDA of 10x the same year. So a higher rating, but also an EBIT margin approaching 20% and RoCE of 15% for Boku, like THG/APN superior profitability track record reflected in higher valuation multiples.

Opinion: You can sense my scepticism towards Bango, but mobile payments still worth following, I think? If the DVM idea really takes off, then it will dominate the investment case. I like the idea in theory, I have too many subscriptions, and I think US tech companies deliberately target the inertia of their customers. Management reported 12 new Digital Vending Machine® (DVM™) last year, and a further 3 wins in Q1 this year, bringing DVM customers to over 40 and active subscriptions +60% to 24m consumers.

So, if Bango has hit on a service that helps consumers and which is hard for competitors to copy then this could really go somewhere. Given past disappointment not a high conviction idea, but just flagging the investment case as having potential.

Bruce Packard

@bruce_packard

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.