Bruce Packard explores how soaring energy prices ultimately failed to translate into stronger performance for renewable energy funds, and considers what investors can learn from this when assessing the future of AI and space infrastructure investment. Companies covered include Kainos Group (KNOS), Keller Group (KLR) and Diaceutics (DXRX).

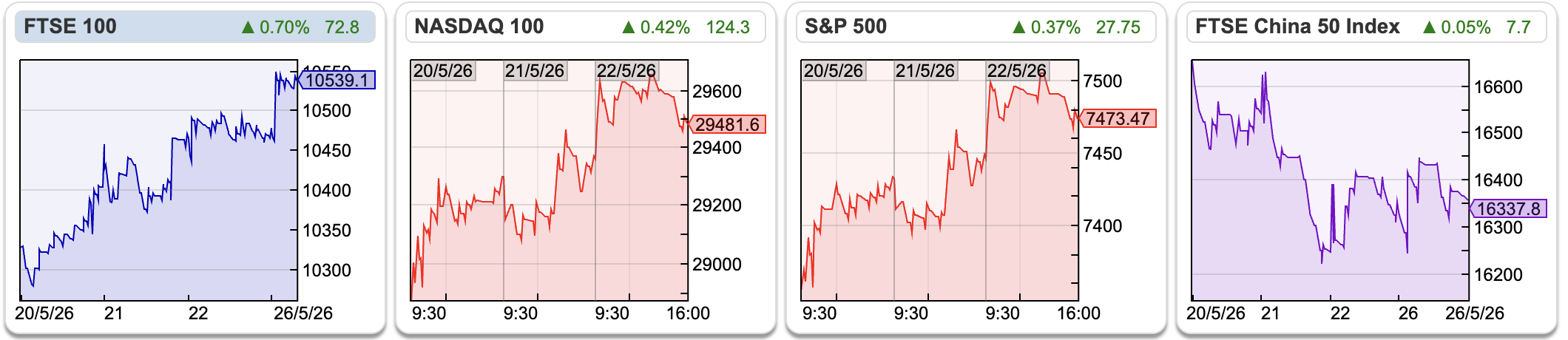

The FTSE 100 rose +2.1% to 10,539 in the last 5 trading days. The Nasdaq100 and S&P500 were up around +1%, while the FTSE China 50 fell -1.4%. Since Donald Trump commenced hostilities with Iran the FTSE China 50 has fallen -4%, along with the Mumbai Indian exchange and CAC 40 in Paris, the worst performing countries. European Natural Gas (EGAS) fell -5% over the last 5 trading days, but is still up +50% since the end of February. Brent Crude fell -10% and is now $96 per barrel, as newspaper headlines suggest that Iran and the USA are approaching a compromise to re-open the Straits of Hormuz.

The FTSE 100 rose +2.1% to 10,539 in the last 5 trading days. The Nasdaq100 and S&P500 were up around +1%, while the FTSE China 50 fell -1.4%. Since Donald Trump commenced hostilities with Iran the FTSE China 50 has fallen -4%, along with the Mumbai Indian exchange and CAC 40 in Paris, the worst performing countries. European Natural Gas (EGAS) fell -5% over the last 5 trading days, but is still up +50% since the end of February. Brent Crude fell -10% and is now $96 per barrel, as newspaper headlines suggest that Iran and the USA are approaching a compromise to re-open the Straits of Hormuz.

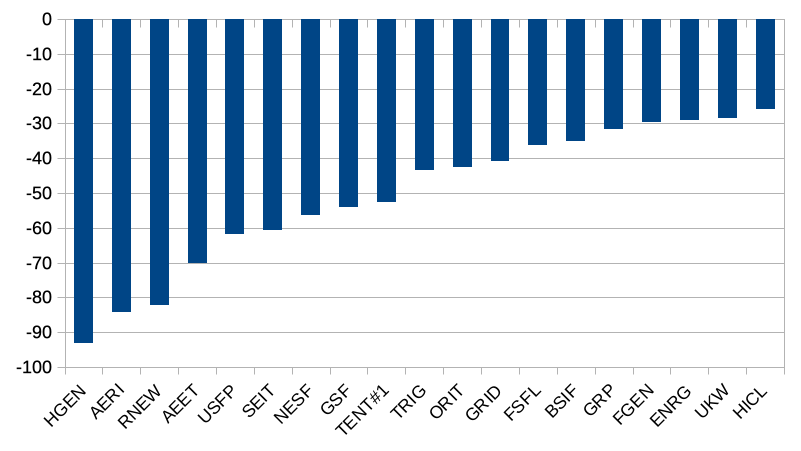

One counter intuitive aspect of energy cost rises that I wanted to flag, is just how badly UK listed Renewables Energy Infrastructure Funds (REIFs) have performed since Putin invaded Ukraine. Below is a chart showing that even the best performing funds, such as HICL and Greencoat UK Wind are down by over -25% since Feb 2022. Solar panel funds like Bluefield Solar Income Fund (BSIF) and Foresight Solar Fund (FSFL) have fared worse, down by almost -40%. Next Energy Solar Fund (NESF) and battery funds like Gore Street Energy Storage (GSF) are down by around -55%. Hydrogen One (HGEN) fell -95% as hydrogen infrastructure is capitally intensive and the returns are uncertain (sound familiar?). The shares were delisted last month.

Since Donald Trump began hostilities against Iran, performance has improved for Greencoat Renewables (GRP) +17% and Octopus Renewables Infrastructure (ORIT) +13%, but these are still down -30% to -40% over the longer term horizon in the chart above.

This can serve as a reminder that investing is not about predicting the future. If you had had perfect foresight that Putin would invade Ukraine, and the Labour governments would be keen to encourage investment in renewables as a source of energy independence, then the REIFs might have seemed like an obvious way to play this theme. The reality was that their business models suffered more from rising interest rates than they gained from rising energy costs.

Instead of trying to predict the future, the red flags with the REIF sector were murky accounting, unconsolidated balance sheets, fair value assets and indecipherable cashflow statements. I took a position in NESF when the dividend yield hit 13%, thinking a cut was probably priced in – that turned out to be a mistake as the yield was over 17% before being cut in half.

There could also be a parallel with investing in today’s hot themes of Artificial Intelligence or Space. I am sure that the world will look very different in a couple of decades time, but I’m sceptical of the investment case in both OpenAI and SpaceX IPOs. OpenAI has a lot of customers, but its unclear how it can generate enough cashflow to justify the mooted valuation and announced infrastructure spend. SpaceX is an odd mix of Twitter/X and LEO satellites, priced on over 100x sales. There’s a quote from Scott McNealy, of Sun Microsystems in 2002, following the implosion of the TMT bubble, complaining that 10x sales was an absurdly high valuation for a tech infrastructure company.

Voting for the Investors’ Chronicle/FT annual Celebration of Investment awards 2026 is now open. As always, we would be extremely grateful to receive your vote in the Best Investment Software and Data Tool Provider category. Voting should only take a couple of minutes. Click here to vote.

This week I look at Kainos FY Mar results, which like many other enterprise software groups has strong forecast revenue growth, but has experienced a de-rating over AI fears. Similarly, Diaceutics a medical database platform, has seen strongly rising revenue growth while experiencing de-rating. I also look at Keller, the geo-technical building contractor, which seems to be benefiting from excitement over US datacenter build out.

I’m looking forward to seeing many readers at the Mello investor conference in Chiswick at the start of June. Please do come along and say “hello”.

Kainos FY Mar 2026 Results

Like Craneware, which I wrote about a couple of months ago, this is another enterprise software group that has been sold-off due to concerns over AI Agents. Kainos reported FY Mar revenue up +17% to £431m. Statutory PBT was up +19% to £58m, however that y-o-y comparison was helped by £8.4m of restructuring costs in the previous year, without which PBT growth was just +2%. Management explain that following a series of large contract wins, they have had to increase the use of contractors, where costs quadrupled to £18.5m, while third-party supplier costs doubled to £30m. So despite being an IT group, the gross margin was 46% and revenue growth has not converted into underlying profit growth.

Like Craneware, which I wrote about a couple of months ago, this is another enterprise software group that has been sold-off due to concerns over AI Agents. Kainos reported FY Mar revenue up +17% to £431m. Statutory PBT was up +19% to £58m, however that y-o-y comparison was helped by £8.4m of restructuring costs in the previous year, without which PBT growth was just +2%. Management explain that following a series of large contract wins, they have had to increase the use of contractors, where costs quadrupled to £18.5m, while third-party supplier costs doubled to £30m. So despite being an IT group, the gross margin was 46% and revenue growth has not converted into underlying profit growth.

Digging a little deeper, the group gross margin is a composite of very different activities:

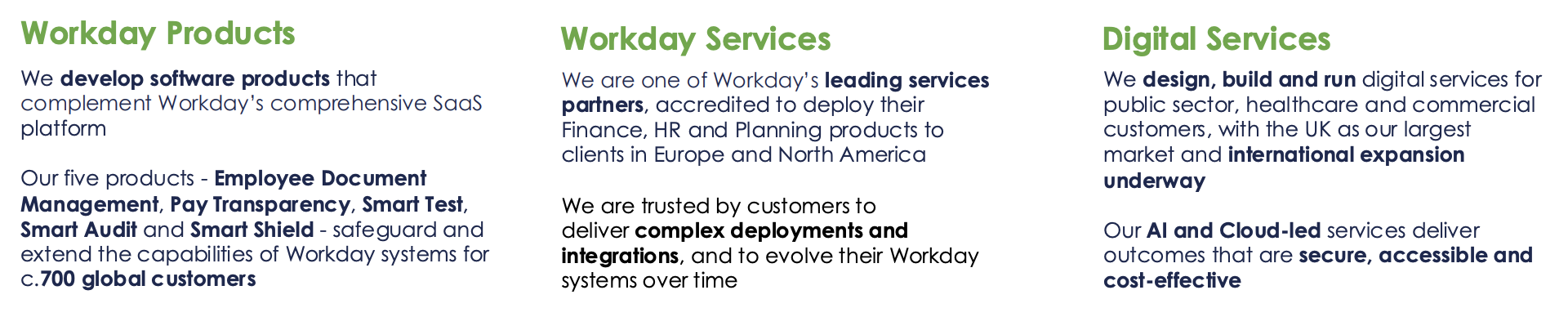

Kainos implements Workday Products, an ERP software package, which generates a stable gross margin of 78%. Once the software is developed, the marginal cost to implement for the next customer is close to zero, so it ought to be an attractive, scaleable business. Revenues in that division grew +15% to £81m. Digital Services, where revenues grew +23% to £241m, has a gross margin of 36% and involves custom software engineering where the economics don’t scale as attractively. Finally there’s also Workday Services, where revenue increase +9% to £108m, but the gross margin fell 6% to 46%, as a result of higher staff costs.

Kainos implements Workday Products, an ERP software package, which generates a stable gross margin of 78%. Once the software is developed, the marginal cost to implement for the next customer is close to zero, so it ought to be an attractive, scaleable business. Revenues in that division grew +15% to £81m. Digital Services, where revenues grew +23% to £241m, has a gross margin of 36% and involves custom software engineering where the economics don’t scale as attractively. Finally there’s also Workday Services, where revenue increase +9% to £108m, but the gross margin fell 6% to 46%, as a result of higher staff costs.

Balance sheet: There’s £53m of goodwill and other intangible assets on the balance sheet, compared to shareholders’ equity of £100m. Net cash fell to £89m, but that was mainly a result of the £56m share buyback, cash conversion remains healthy at close to 100%. Deferred income in current liabilities rose +31% to £60m – that’s very positive as represents cash that clients have paid, but can’t yet be booked as revenue.

Outlook: There are some positive statements about the opportunities AI creates. More concretely, they highlight the healthy sales pipeline and say for FY Mar 2027F, Workday Products, should achieve £100m of ARR by the end of 2026. That would actually represent a slowdown from the +23% just reported to £89m though. They also talk about further growth in the other divisions, without committing to anything definitive though.

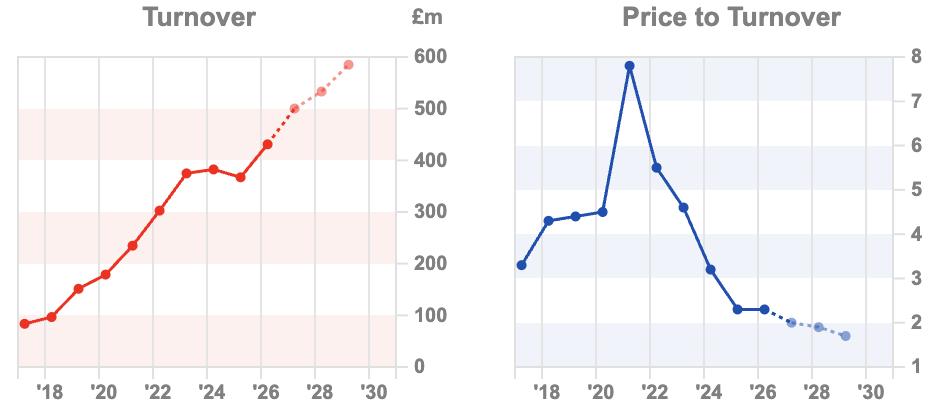

Valuation: The shares are trading on a PER of 18x Mar 2027F, dropping to 16x the following year. On an EV/EBITDA basis they’re on 11.5x, dropping to 9.8x in Mar 2028F. The forecast price to sales multiple is 2.1x. I seem to be posting a number of these type of charts, showing consistently growing revenue but de-rating of price/revenue. Other recent examples include Rightmove, Bango, Calnex, Shield Therapeutics, YouGov and Craneware.

Opinion: Not what I was expecting to see. I thought we might see growth slowing, but instead there’s no problem with the top line, instead this looks like a group where management are coping with large contract wins and having to hire outside help. Historically this has been a high RoCE group, shareholders just need to be sure that the benefits of contract wins are not going to external help to implement projects. More generally I think all of these groups like Kainos, Craneware and GB Group are looking much better value than a few years ago, so I think it’s a sector worth trying to understand.

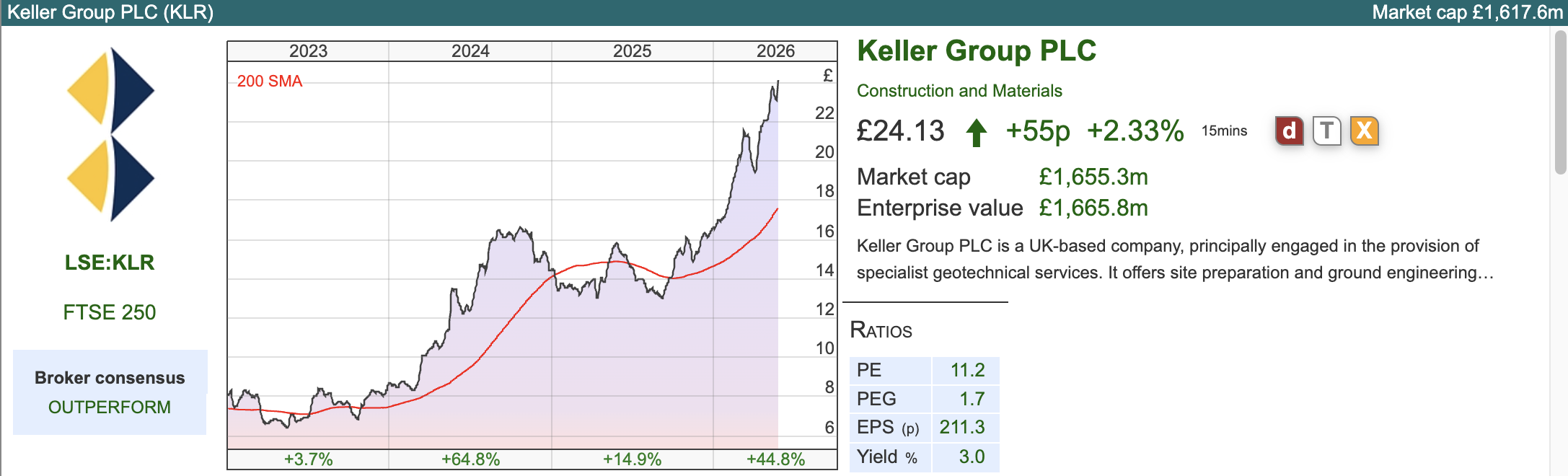

Keller AGM Trading Update

This geotechnical contractor with a December year end issued an inline trading update. In their FY 2025 Annual Report they mentioned AI data centre build out as a case study. North America is currently 59% of group revenue.

This geotechnical contractor with a December year end issued an inline trading update. In their FY 2025 Annual Report they mentioned AI data centre build out as a case study. North America is currently 59% of group revenue.

Last week’s RNS says that their order book has strengthened to c£1.7bn at the end of April 2026 (versus £1.5bn Dec 2025) meaning that management has good visibility of future opportunities across all divisions.

Last week’s RNS says that their order book has strengthened to c£1.7bn at the end of April 2026 (versus £1.5bn Dec 2025) meaning that management has good visibility of future opportunities across all divisions.

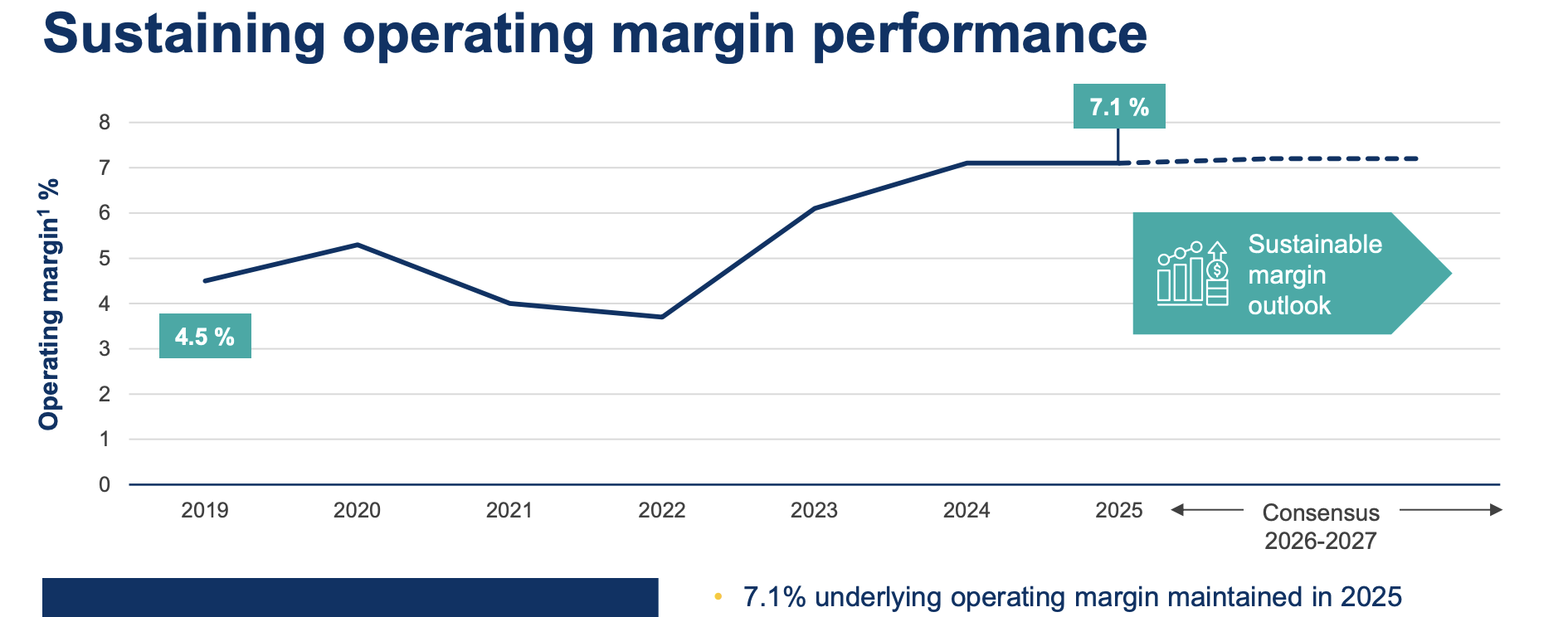

ShareScope shows FY Dec 2026F revenue is forecast to grow +2% to £3.1bn and +3% the following year. Yet the share price is up +45% YTD, suggesting investors are expecting that growth rate to be beaten. Bear in mind though that there is some exposure to the Middle East, plus US residential sector which continues to be weak. The group’s underlying operating margin is currently above 7%, well above the average achieved since 2019, as this slide from the FY results shows.

Naturally management suggest that the margin outlook is sustainable, in which case a RoCE of around 20% also looks viable.

Valuation: The shares are trading on 10.5x PER Dec 2026F, falling to 9.5x the following year. That translates to 5x EV/EBITDA, which seems undemanding, as long as the margin is sustainable and revenue doesn’t collapse when all the datacenter work is completed.

Opinion: Tricky one. Momentum is strong and I can see UK investors are keen to find ways to benefit from the AI boom and data centre build out. The investment case looks attractive for now, but I tend to invest with a 3-5 year time horizon, on which basis I would be more cautious. I think the time to buy it was 2024, when I last wrote about the stock, when I pointed out that the share price was benefiting from increased infrastructure spending, but that I would sell on the first signs of trouble. So far, no trouble has emerged, but I think if I re-visit the investment case in May 2028, I’d be surprised if increased energy and material costs had not weakened the investment case. So, not for me but if you have shorter time horizons, then don’t let me stand in your way.

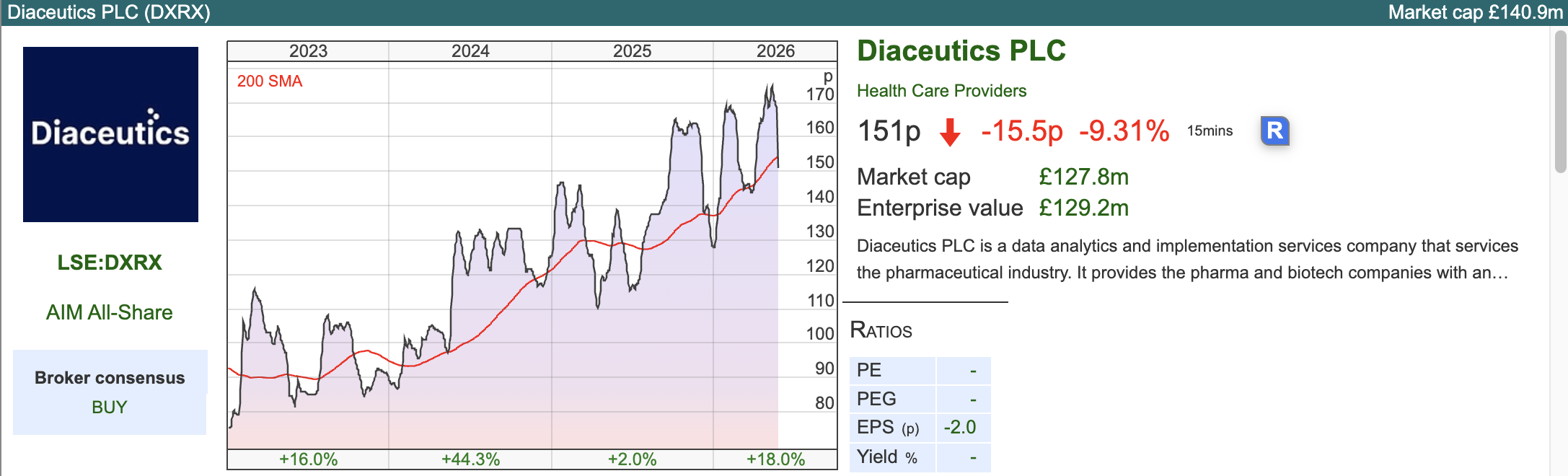

Diaceutics FY Dec 2025 Results

This group starts with a black mark against it, having only now released FY Dec 2025 results. To be fair, they did put out a trading statement in mid January with the headline numbers, but if large, global FTSE 100 groups can get their results out in 2-3 months, you have to question the finance director of a £130m market cap company releasing their FY Dec results at the end of May.

This group starts with a black mark against it, having only now released FY Dec 2025 results. To be fair, they did put out a trading statement in mid January with the headline numbers, but if large, global FTSE 100 groups can get their results out in 2-3 months, you have to question the finance director of a £130m market cap company releasing their FY Dec results at the end of May.

Keeping an open mind though, revenue grew +24% on a constant currency basis to £38m. That has meant a swing from £1.9m loss before tax last year to just over £300K PBT. Cash fell -42% to £7.3m, but that should be adequate to fund growth now that the group is profitable.

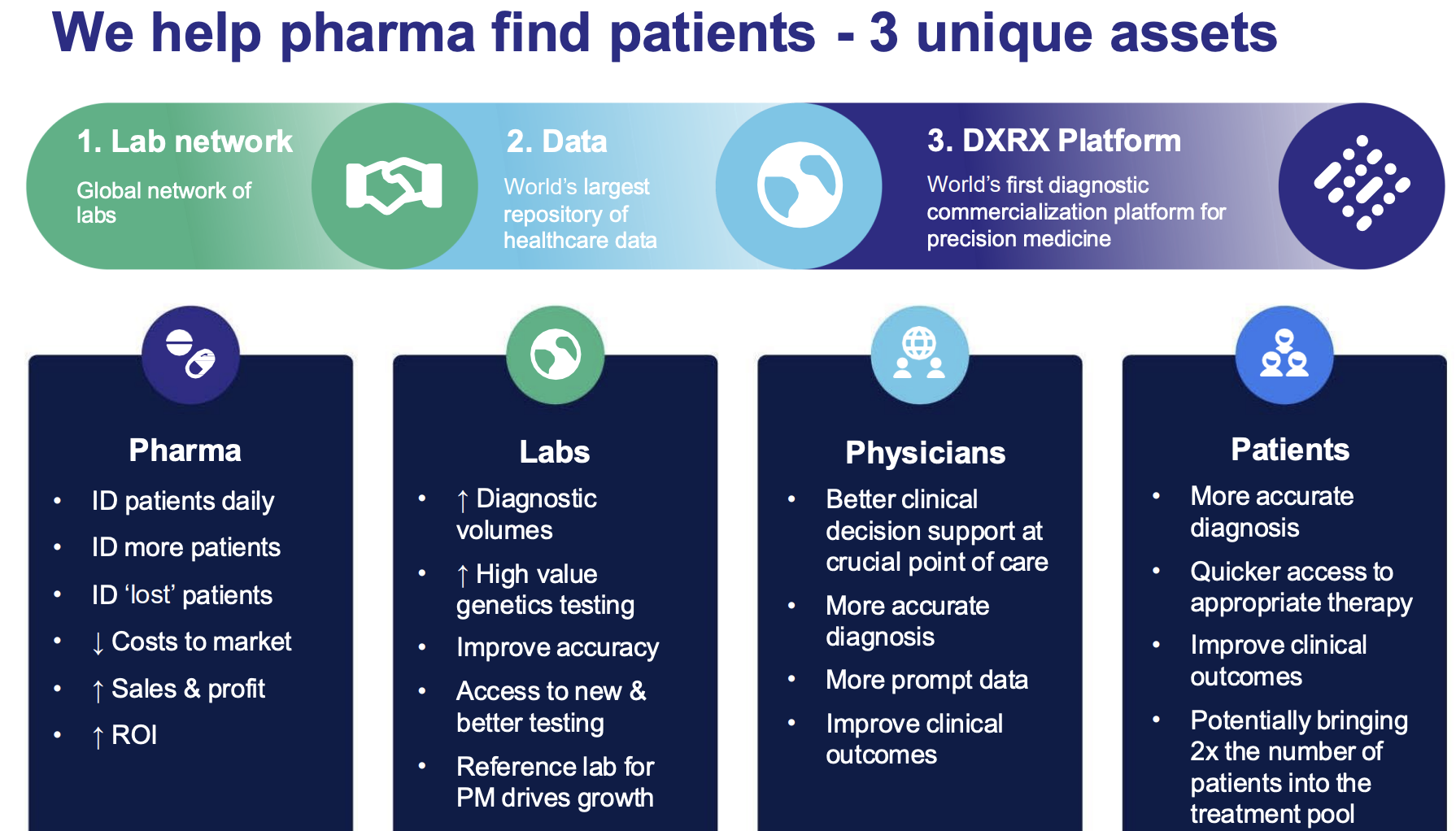

The group describes itself as “a leading technology and solutions provider to the pharma and biotech industry”. The commentary mentions “precision medicine”, which means using biomarker tests to see whether a patient is eligible for targeted therapies that have already been developed by the pharma industry. When a pharmaceutical company develops a “precision medicine” drug (common in cancer/oncology), the biggest commercial challenge isn’t then selling the drug—it’s finding the specific patients who the drug will be most effective treatment for.

So this is a medical database business, and they specifically mention “the operating leverage inherent in our platform model”. Indeed, I did a word count and the word “platform” appears 64 times in this week’s RNS. Below is a slide from their analyst presentation, like many other software/database groups, they suggest AI is an enabler that deepens their “moat”.

So this is a medical database business, and they specifically mention “the operating leverage inherent in our platform model”. Indeed, I did a word count and the word “platform” appears 64 times in this week’s RNS. Below is a slide from their analyst presentation, like many other software/database groups, they suggest AI is an enabler that deepens their “moat”.

Outlook: They say that Q1 2026 revenue growth has slowed to +15%, while ongoing enhancements to the DXRX platform are delivering operational leverage, which would imply improving margins. Management also reiterate that they are on track for FY Dec 2026F targets, with Sharescope showing +24% revenue growth forecast this year, and +21% next year.

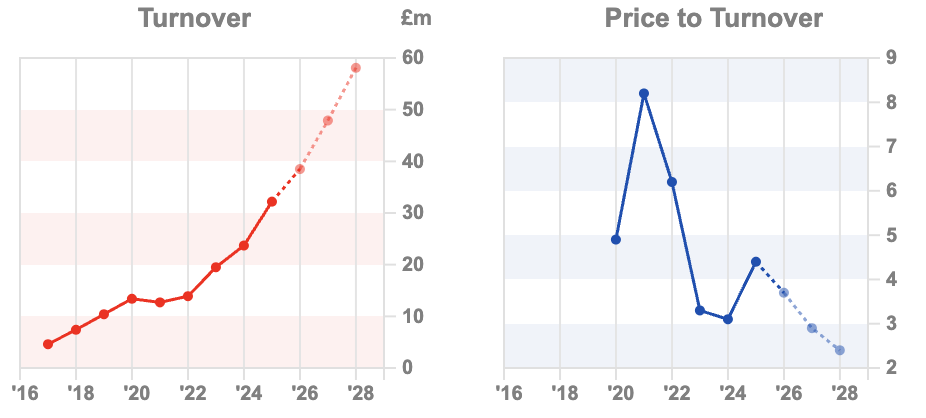

Valuation: The shares are trading on a PER of over 300x this year, but that drops to 35x in 2027F as revenue continues to grow and the margin improves. The EV/EBITDA is forecast to be 9x in 2027F and the price/sales drops below 2.5x (versus 3.7x 2025A). This is another group with Sharescope showing compounding turnover growth while price/turnover has de-rated from over 8x during the pandemic to below 2.5x in two years’ time.

Opinion: I think that this could be a genuine platform business, with high margin recurring revenue but I would need to understand why growth has slowed in the early part of this year. Presumably that disappointment led to the shares falling -11% on the morning of the RNS. The analyst presentation suggests that although they are focused on oncology currently, “Precision for All” could next be applied to immunology, cardiology, nephrology, rare diseases and neurology. So this seems like a good story, Growth at a Reasonable Price (GARP), but in a sector few understand well and that seeing significant disruption from AI.

Bruce Packard

@bruce_packard

Bruce owns shares in Next Energy Solar Fund

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Bi-Weekly Market Commentary | 27/05/2026 |KNOS, KLR, DXRX | Energy costs and renewables

Bruce Packard explores how soaring energy prices ultimately failed to translate into stronger performance for renewable energy funds, and considers what investors can learn from this when assessing the future of AI and space infrastructure investment. Companies covered include Kainos Group (KNOS), Keller Group (KLR) and Diaceutics (DXRX).

One counter intuitive aspect of energy cost rises that I wanted to flag, is just how badly UK listed Renewables Energy Infrastructure Funds (REIFs) have performed since Putin invaded Ukraine. Below is a chart showing that even the best performing funds, such as HICL and Greencoat UK Wind are down by over -25% since Feb 2022. Solar panel funds like Bluefield Solar Income Fund (BSIF) and Foresight Solar Fund (FSFL) have fared worse, down by almost -40%. Next Energy Solar Fund (NESF) and battery funds like Gore Street Energy Storage (GSF) are down by around -55%. Hydrogen One (HGEN) fell -95% as hydrogen infrastructure is capitally intensive and the returns are uncertain (sound familiar?). The shares were delisted last month.

Since Donald Trump began hostilities against Iran, performance has improved for Greencoat Renewables (GRP) +17% and Octopus Renewables Infrastructure (ORIT) +13%, but these are still down -30% to -40% over the longer term horizon in the chart above.

This can serve as a reminder that investing is not about predicting the future. If you had had perfect foresight that Putin would invade Ukraine, and the Labour governments would be keen to encourage investment in renewables as a source of energy independence, then the REIFs might have seemed like an obvious way to play this theme. The reality was that their business models suffered more from rising interest rates than they gained from rising energy costs.

Instead of trying to predict the future, the red flags with the REIF sector were murky accounting, unconsolidated balance sheets, fair value assets and indecipherable cashflow statements. I took a position in NESF when the dividend yield hit 13%, thinking a cut was probably priced in – that turned out to be a mistake as the yield was over 17% before being cut in half.

There could also be a parallel with investing in today’s hot themes of Artificial Intelligence or Space. I am sure that the world will look very different in a couple of decades time, but I’m sceptical of the investment case in both OpenAI and SpaceX IPOs. OpenAI has a lot of customers, but its unclear how it can generate enough cashflow to justify the mooted valuation and announced infrastructure spend. SpaceX is an odd mix of Twitter/X and LEO satellites, priced on over 100x sales. There’s a quote from Scott McNealy, of Sun Microsystems in 2002, following the implosion of the TMT bubble, complaining that 10x sales was an absurdly high valuation for a tech infrastructure company.

Voting for the Investors’ Chronicle/FT annual Celebration of Investment awards 2026 is now open. As always, we would be extremely grateful to receive your vote in the Best Investment Software and Data Tool Provider category. Voting should only take a couple of minutes. Click here to vote.

This week I look at Kainos FY Mar results, which like many other enterprise software groups has strong forecast revenue growth, but has experienced a de-rating over AI fears. Similarly, Diaceutics a medical database platform, has seen strongly rising revenue growth while experiencing de-rating. I also look at Keller, the geo-technical building contractor, which seems to be benefiting from excitement over US datacenter build out.

I’m looking forward to seeing many readers at the Mello investor conference in Chiswick at the start of June. Please do come along and say “hello”.

Kainos FY Mar 2026 Results

Digging a little deeper, the group gross margin is a composite of very different activities:

Balance sheet: There’s £53m of goodwill and other intangible assets on the balance sheet, compared to shareholders’ equity of £100m. Net cash fell to £89m, but that was mainly a result of the £56m share buyback, cash conversion remains healthy at close to 100%. Deferred income in current liabilities rose +31% to £60m – that’s very positive as represents cash that clients have paid, but can’t yet be booked as revenue.

Outlook: There are some positive statements about the opportunities AI creates. More concretely, they highlight the healthy sales pipeline and say for FY Mar 2027F, Workday Products, should achieve £100m of ARR by the end of 2026. That would actually represent a slowdown from the +23% just reported to £89m though. They also talk about further growth in the other divisions, without committing to anything definitive though.

Valuation: The shares are trading on a PER of 18x Mar 2027F, dropping to 16x the following year. On an EV/EBITDA basis they’re on 11.5x, dropping to 9.8x in Mar 2028F. The forecast price to sales multiple is 2.1x. I seem to be posting a number of these type of charts, showing consistently growing revenue but de-rating of price/revenue. Other recent examples include Rightmove, Bango, Calnex, Shield Therapeutics, YouGov and Craneware.

Opinion: Not what I was expecting to see. I thought we might see growth slowing, but instead there’s no problem with the top line, instead this looks like a group where management are coping with large contract wins and having to hire outside help. Historically this has been a high RoCE group, shareholders just need to be sure that the benefits of contract wins are not going to external help to implement projects. More generally I think all of these groups like Kainos, Craneware and GB Group are looking much better value than a few years ago, so I think it’s a sector worth trying to understand.

Keller AGM Trading Update

ShareScope shows FY Dec 2026F revenue is forecast to grow +2% to £3.1bn and +3% the following year. Yet the share price is up +45% YTD, suggesting investors are expecting that growth rate to be beaten. Bear in mind though that there is some exposure to the Middle East, plus US residential sector which continues to be weak. The group’s underlying operating margin is currently above 7%, well above the average achieved since 2019, as this slide from the FY results shows.

Naturally management suggest that the margin outlook is sustainable, in which case a RoCE of around 20% also looks viable.

Valuation: The shares are trading on 10.5x PER Dec 2026F, falling to 9.5x the following year. That translates to 5x EV/EBITDA, which seems undemanding, as long as the margin is sustainable and revenue doesn’t collapse when all the datacenter work is completed.

Opinion: Tricky one. Momentum is strong and I can see UK investors are keen to find ways to benefit from the AI boom and data centre build out. The investment case looks attractive for now, but I tend to invest with a 3-5 year time horizon, on which basis I would be more cautious. I think the time to buy it was 2024, when I last wrote about the stock, when I pointed out that the share price was benefiting from increased infrastructure spending, but that I would sell on the first signs of trouble. So far, no trouble has emerged, but I think if I re-visit the investment case in May 2028, I’d be surprised if increased energy and material costs had not weakened the investment case. So, not for me but if you have shorter time horizons, then don’t let me stand in your way.

Diaceutics FY Dec 2025 Results

Keeping an open mind though, revenue grew +24% on a constant currency basis to £38m. That has meant a swing from £1.9m loss before tax last year to just over £300K PBT. Cash fell -42% to £7.3m, but that should be adequate to fund growth now that the group is profitable.

The group describes itself as “a leading technology and solutions provider to the pharma and biotech industry”. The commentary mentions “precision medicine”, which means using biomarker tests to see whether a patient is eligible for targeted therapies that have already been developed by the pharma industry. When a pharmaceutical company develops a “precision medicine” drug (common in cancer/oncology), the biggest commercial challenge isn’t then selling the drug—it’s finding the specific patients who the drug will be most effective treatment for.

Outlook: They say that Q1 2026 revenue growth has slowed to +15%, while ongoing enhancements to the DXRX platform are delivering operational leverage, which would imply improving margins. Management also reiterate that they are on track for FY Dec 2026F targets, with Sharescope showing +24% revenue growth forecast this year, and +21% next year.

Valuation: The shares are trading on a PER of over 300x this year, but that drops to 35x in 2027F as revenue continues to grow and the margin improves. The EV/EBITDA is forecast to be 9x in 2027F and the price/sales drops below 2.5x (versus 3.7x 2025A). This is another group with Sharescope showing compounding turnover growth while price/turnover has de-rated from over 8x during the pandemic to below 2.5x in two years’ time.

Opinion: I think that this could be a genuine platform business, with high margin recurring revenue but I would need to understand why growth has slowed in the early part of this year. Presumably that disappointment led to the shares falling -11% on the morning of the RNS. The analyst presentation suggests that although they are focused on oncology currently, “Precision for All” could next be applied to immunology, cardiology, nephrology, rare diseases and neurology. So this seems like a good story, Growth at a Reasonable Price (GARP), but in a sector few understand well and that seeing significant disruption from AI.

Bruce Packard

@bruce_packard

Bruce owns shares in Next Energy Solar Fund

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.