AIM has fallen through key moving average support levels, suggesting it may be time to trim portfolios and cut low conviction or losing positions. Companies covered NESF, TCAP and CBG.

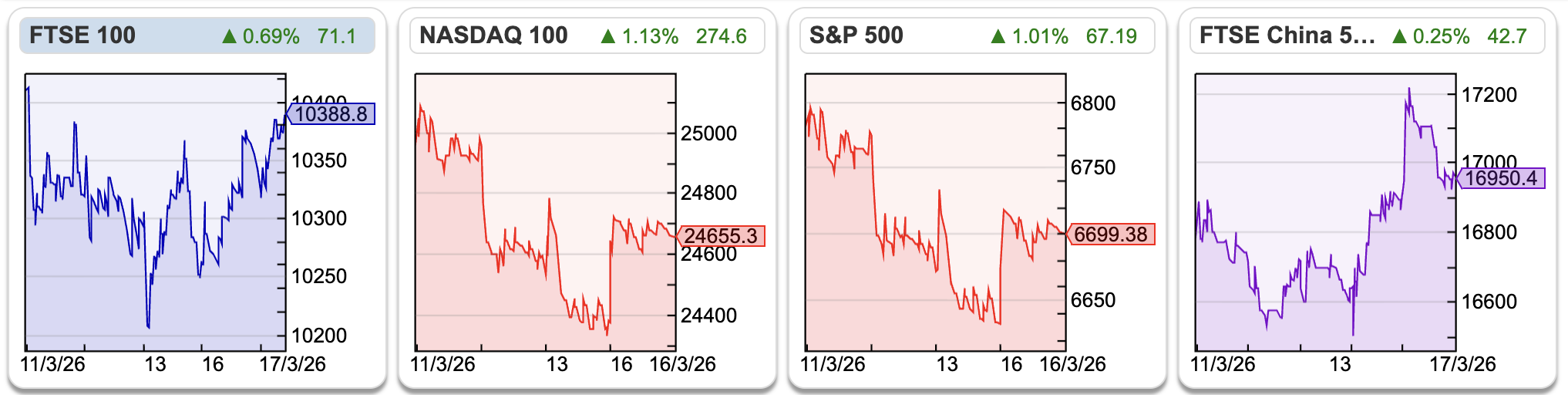

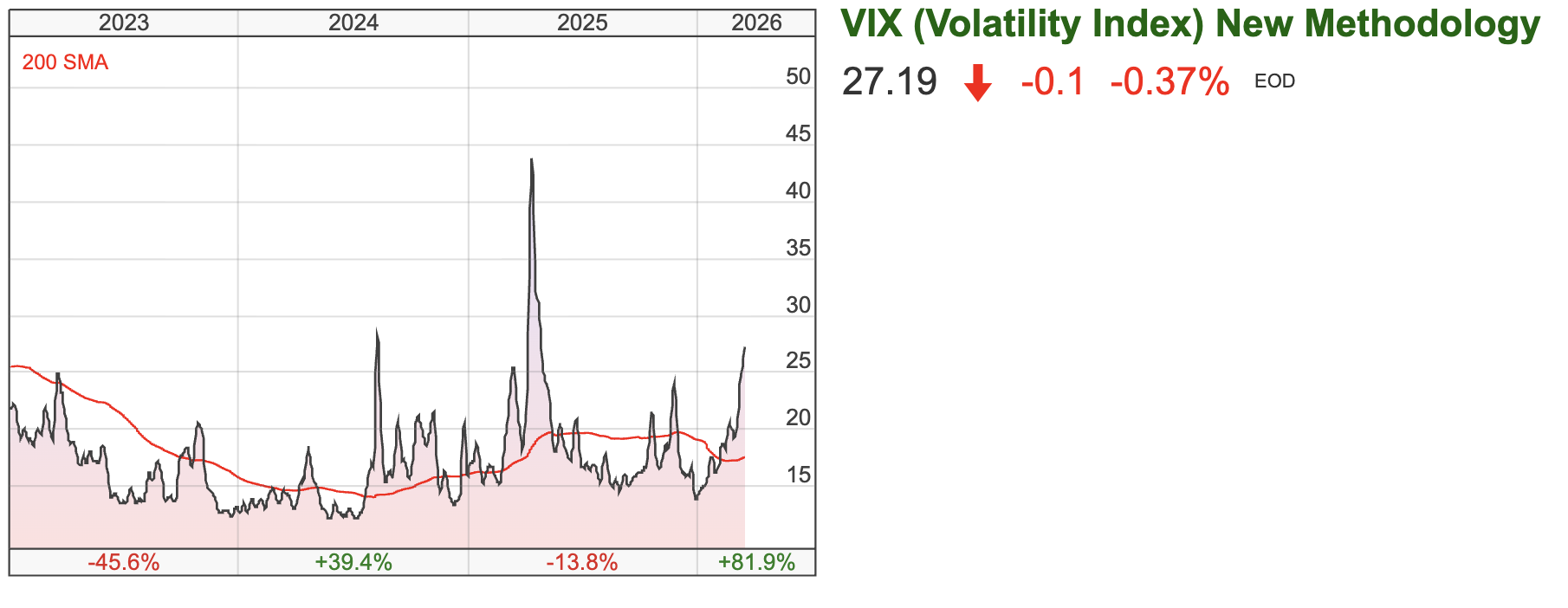

The FTSE 100 was flat over the last 5 days, currently 10,388 – but with some significant daily swings. The peak at the end of Feb was 10,900 and the trough 10,200 on the 9th March. There’s little clarity on how US/Israel attacks on Iran ends.. Brent crude is $104 per barrel, +62% YTD but below its $120 conflict high. The VIX is currently at 27, up +82% YTD but still well below the 44 level that it peaked at during Trump’s tariff announcements a year ago.

The FTSE 100 was flat over the last 5 days, currently 10,388 – but with some significant daily swings. The peak at the end of Feb was 10,900 and the trough 10,200 on the 9th March. There’s little clarity on how US/Israel attacks on Iran ends.. Brent crude is $104 per barrel, +62% YTD but below its $120 conflict high. The VIX is currently at 27, up +82% YTD but still well below the 44 level that it peaked at during Trump’s tariff announcements a year ago.

I haven’t done any buying or selling since the violence started. I do need to cut down on my positions, as over the last few years I’ve accumulated too many “low conviction ideas” and my portfolio has ballooned to 40 stocks. The AXX has fallen below its 200 day moving average and the 64/16 (blue/red lines) day has crossed over, so selling some losers seems like my next step.

I haven’t done any buying or selling since the violence started. I do need to cut down on my positions, as over the last few years I’ve accumulated too many “low conviction ideas” and my portfolio has ballooned to 40 stocks. The AXX has fallen below its 200 day moving average and the 64/16 (blue/red lines) day has crossed over, so selling some losers seems like my next step.

David has announced the dates for the London Mello event in June: Tues 2nd & Wed 3rd June, at The Clayton Hotel & Conference Centre, Chiswick, London. I’ve booked my flight, so hopefully see many of you there.

David has announced the dates for the London Mello event in June: Tues 2nd & Wed 3rd June, at The Clayton Hotel & Conference Centre, Chiswick, London. I’ve booked my flight, so hopefully see many of you there.

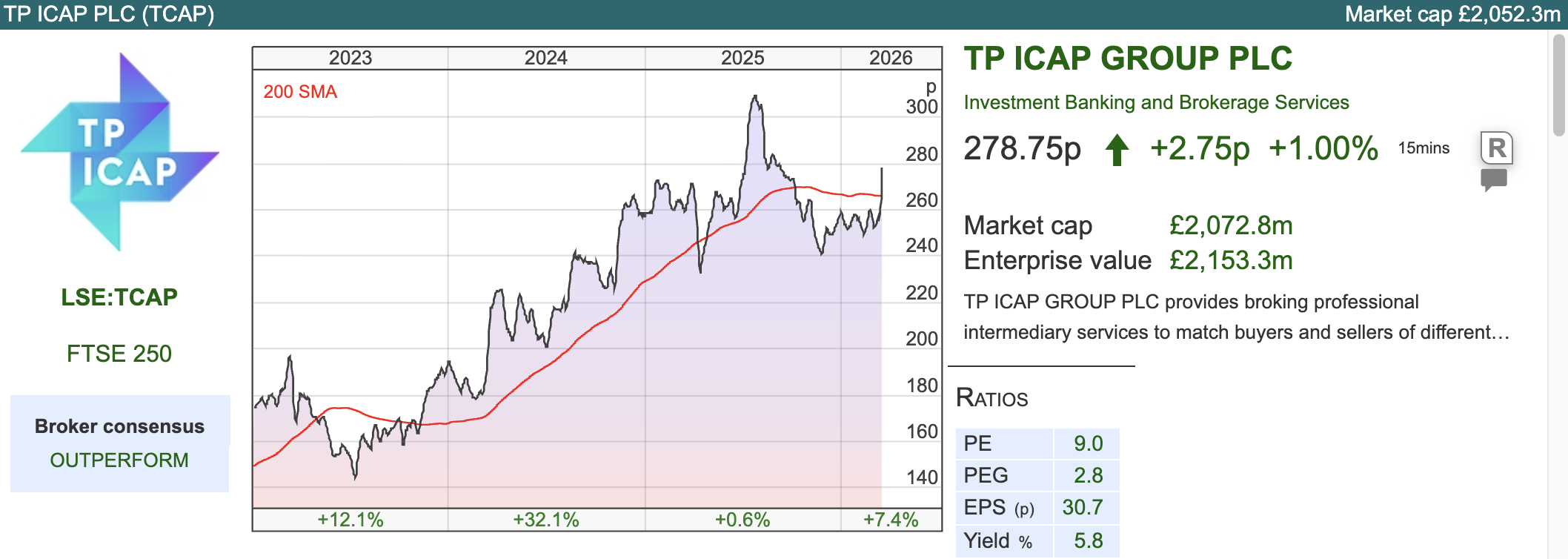

This week I look at solar fund NESF, which announced a dividend cut last week and Close Brothers which has come under attack from short seller Viceroy. But I start with TP ICAP the interdealer broker.

TP ICAP FY Dec 2025 Results

This interdealer broker ought to benefit from volatility, as customers seek to hedge or take advantage of market moves. The group reported FY Dec 2025 up +4% to £2.35bn and statutory PBT was up +7% to £230m. There’s an £80m buyback announced with management pointing out that since H1 2023 they have returned £600m to shareholders in buybacks and dividends.

This interdealer broker ought to benefit from volatility, as customers seek to hedge or take advantage of market moves. The group reported FY Dec 2025 up +4% to £2.35bn and statutory PBT was up +7% to £230m. There’s an £80m buyback announced with management pointing out that since H1 2023 they have returned £600m to shareholders in buybacks and dividends.

They reported a cash balance of £903m, down -15% versus the previous year, “primarily driven by a working capital outflow”. TCAP is a trading business that needs to operate with substantial cash in order for counterparties to trade, they were also carrying gross debt of £802m at the year end. They explain the large swing in working capital as:

“Approximately half of the year-on-year movement reflects changes in net settlement balances that are temporary and reversed immediately after the year end. Other working capital outflows are principally driven by the increase in trade receivable balances due to significant trading activity in December 2025 compared with the prior year, adverse movements in other receivables and creditor balances as well as some provision utilisation.” Capex was £74m driven by investment in technology and “strategic facilities investments.” On the call management said that profits should convert into 100% cash over a 3 year cycle.

I note there’s a “below the line” charge of £53m, mainly from FX translation. That’s around a quarter of the statutory PBT figure, given the TP ICAP is in the trading business, I’m not convinced we should ignore such a large item, as the group suffers from dollar weakness. Management said that at the current spot rates they anticipate a £9-10m FX headwind to 2026 adjusted EBIT.

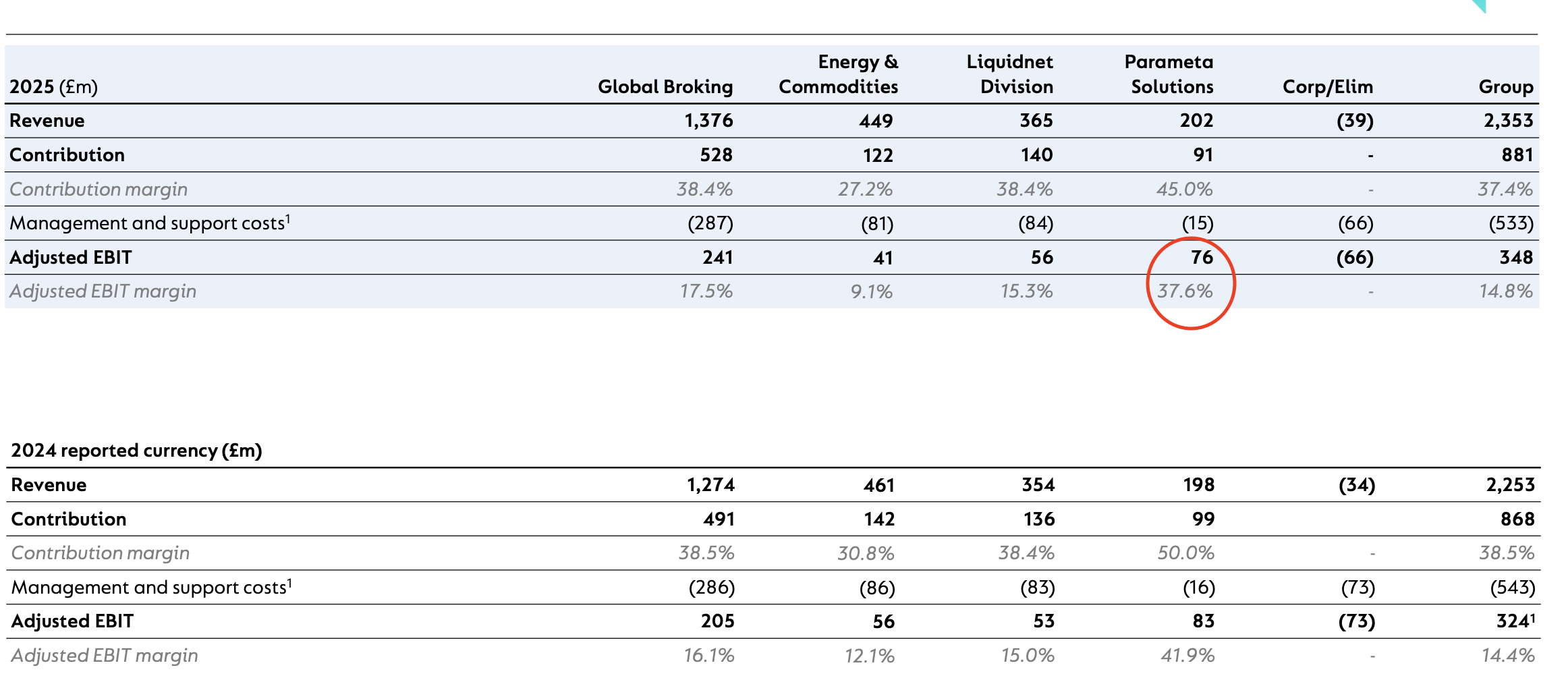

Parameta: Activist investor Jason Hughes encouraged the group to look at realising value from their Parameta data business. An IPO in New York has been anticipated, but they say conditions remain challenging – try telling that to Elon Musk who thinks he can float SpaceX at a $1.5trillion in June when the planets Jupiter and Venus align. Parameta achieved +5% revenue growth on a constant currency basis (+2% reported). Parameta’s EBIT declined -6% to £76m as management invested to grow the business, however the EBIT margin was still an eye catching 38% (group adj EBIT margin 14.8%). Management were asked about the risk from AI, but said that as their data is proprietary (ie not publicly available) AI was more of an opportunity that a threat.

Instead, the driver of results seems to be a reinvigoration of the core Global Broking business (around 60% of group revenue, with an adj EBIT margin of 17.5%) which grew +10% on a constant currency basis, with particular strength in Rates, Credit and Equities.

Instead, the driver of results seems to be a reinvigoration of the core Global Broking business (around 60% of group revenue, with an adj EBIT margin of 17.5%) which grew +10% on a constant currency basis, with particular strength in Rates, Credit and Equities.

Outlook: They say 2026 has started well with supportive market conditions, despite the FX headwind they expect to achieve FY Dec 2026F EBIT (Sharescope consensus forecast £362m – TCAP says the range is £347m to £370m in a footnote), so in effect, a +2.7% upgrade on a constant currency basis.

Valuation: The shares are trading on 8x PER Dec 2026F and 2027F. That seems about right given Sharescopes Quality indicators reflect the favourable trading conditions (RoCE and CRoCI is above the 3 year average) but even so returns are only just double digits.

Opinion: This is no longer as cheap as it was, but I am happy to continue holding. It’s pleasing to see the core Global Broking business doing well, even as Parameta the higher margin data business slows. That shows the group is well diversified – they’ve also been hiring in Energy & Commodities (just under 20% of group revenue) which has been well timed, as that’s likely to see significant activity in the coming months.

Opinion: This is no longer as cheap as it was, but I am happy to continue holding. It’s pleasing to see the core Global Broking business doing well, even as Parameta the higher margin data business slows. That shows the group is well diversified – they’ve also been hiring in Energy & Commodities (just under 20% of group revenue) which has been well timed, as that’s likely to see significant activity in the coming months.

I should have taken a larger position when I bought in 2022. I emailed a friend who had worked in FX options, who had TCAP as a counterparty and knew traders there. Both my friend and his contact were dismissive of the investment case when TCAP shares were trading close to £1 – which I think goes to show that even brokers can be clueless about the investment case in their own organisations.

Next Energy Solar Dividend Cut (Strategic Update)

This is one I got wrong. I bought into the story because I thought that NESF, the over indebted solar panels infrastructure fund, would benefit from falling interest rates, selling off assets and rising energy prices. All those things happened, but management have still cut the dividend! Management had also announced a £20m share buyback, but only achieved £11.5m, due to bouncing up against debt limits (the group’s policy is that net debt can not exceed 50% of Gross Asset Value).

This is one I got wrong. I bought into the story because I thought that NESF, the over indebted solar panels infrastructure fund, would benefit from falling interest rates, selling off assets and rising energy prices. All those things happened, but management have still cut the dividend! Management had also announced a £20m share buyback, but only achieved £11.5m, due to bouncing up against debt limits (the group’s policy is that net debt can not exceed 50% of Gross Asset Value).

Last week the group announced a new dividend policy, paying out 75% of operating free cashflow post debt servicing, which equates to 4.0p to 4.6p per share (down from 8.47p FY Mar 2026). That means a dividend c. 10% yield on the current price at 1.3x cover. Management have cut the dividend without explaining to their investors what’s gone wrong. Cavendish, who write “paid for” research, refer to grid outages and cannibalisation – I think the basic problem is that although solar power is “cheap”, solar funds sell power at a discount because they generate power when it isn’t needed (noon on a sunny summer day). You would think that this would be obvious – but the NESF share price has fallen from over 120p in summer 2022 (a few months after Putin invaded Ukraine) to just below 45p currently. The Labour government intends to triple UK solar capacity, but it’s not clear who funds this and why investors should back new solar projects when the existing funds are trading at 40%-50% discounts to NAV.

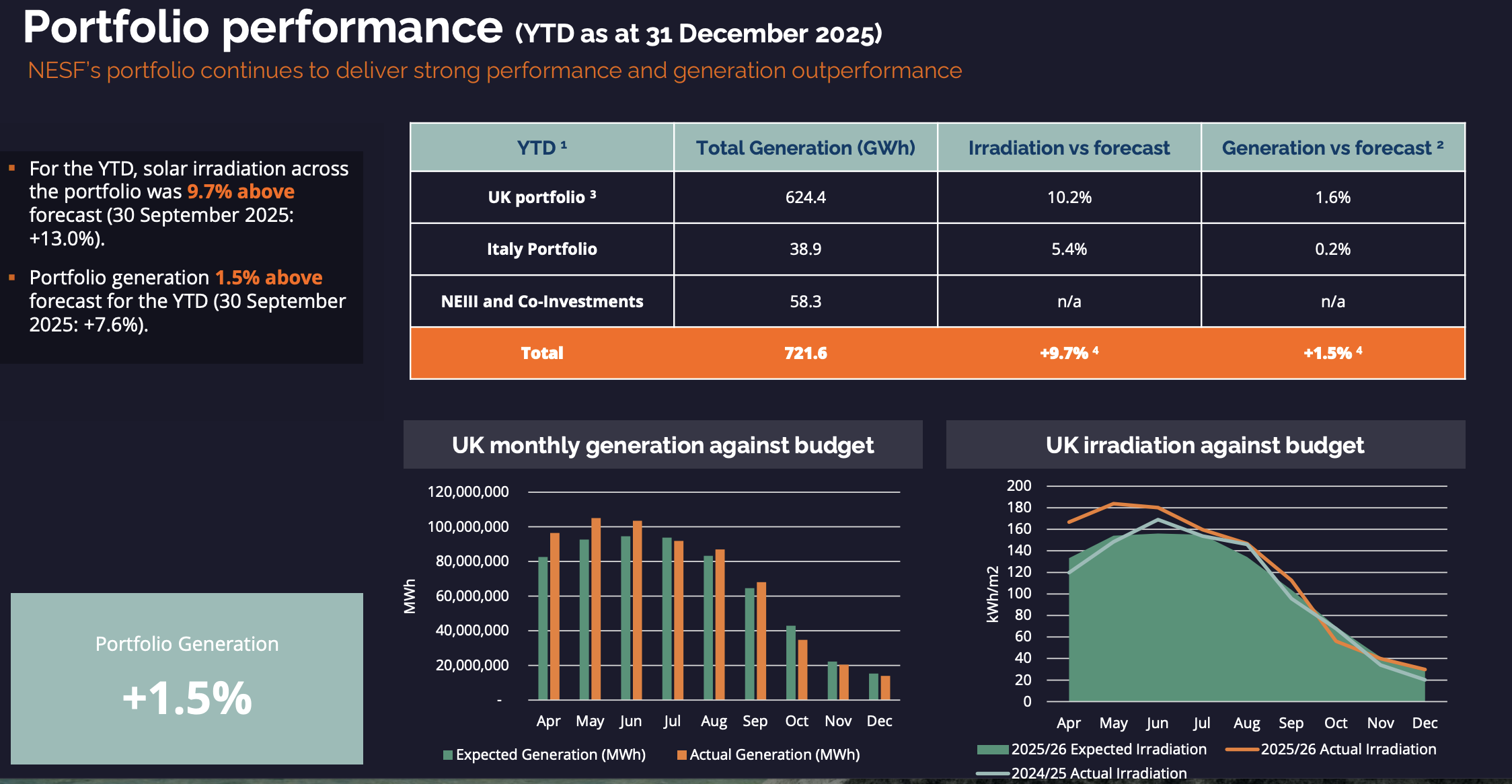

The dividend cut, buyback pause and NAV discount come at a time when NESF has been enjoying more solar irradiation than budgeted (+10% above forecast), as the slide below shows.

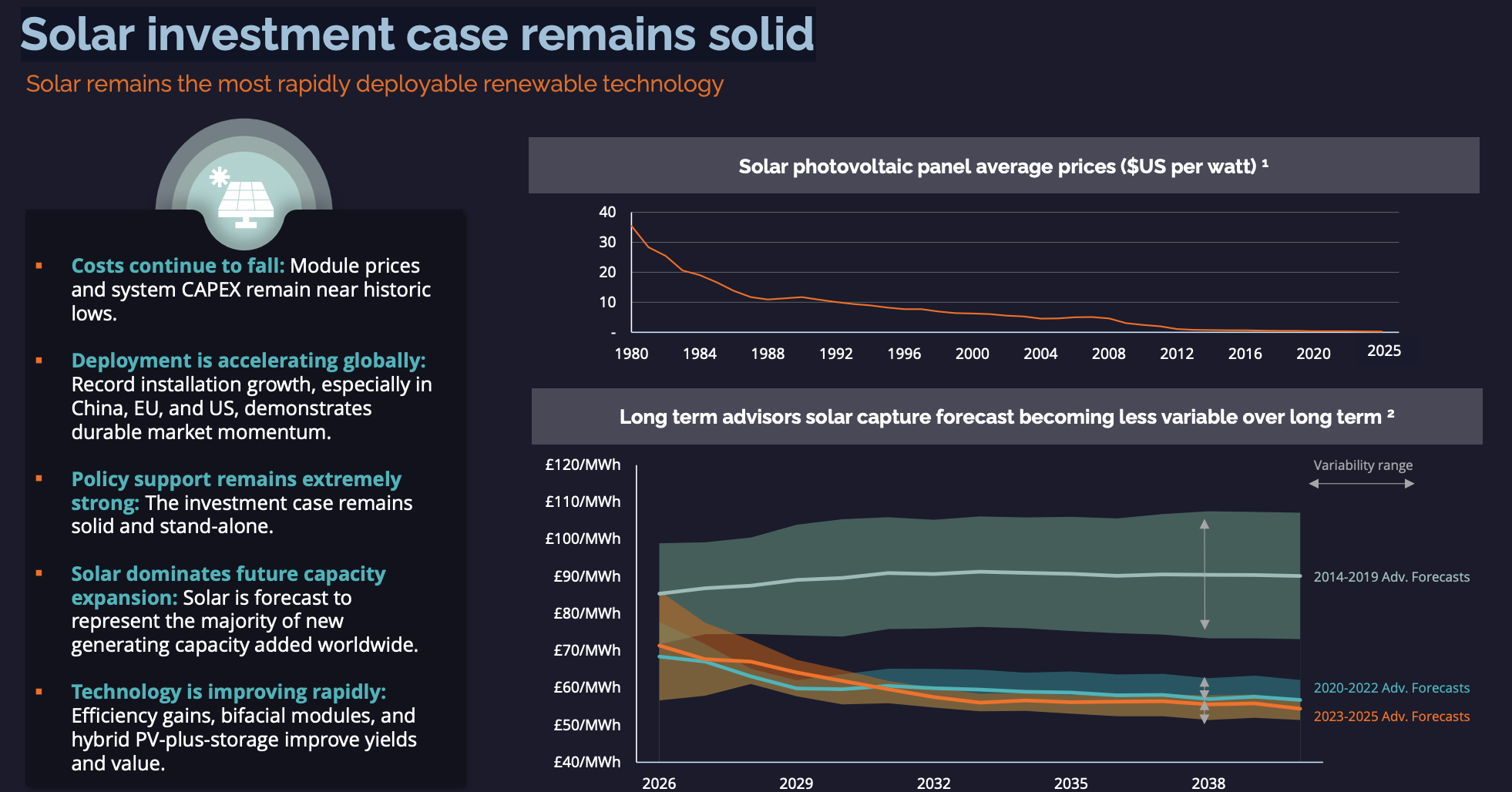

From this I think we can conclude that management have made hopelessly optimistic electricity pricing assumptions. They don’t say that though! Management do seem to have a sense of humour, with one slide headed “Solar investment case remains solid” after their investors have seen a >60% decline in the share price and the discount to NAV has widened to almost 50%.

From this I think we can conclude that management have made hopelessly optimistic electricity pricing assumptions. They don’t say that though! Management do seem to have a sense of humour, with one slide headed “Solar investment case remains solid” after their investors have seen a >60% decline in the share price and the discount to NAV has widened to almost 50%.

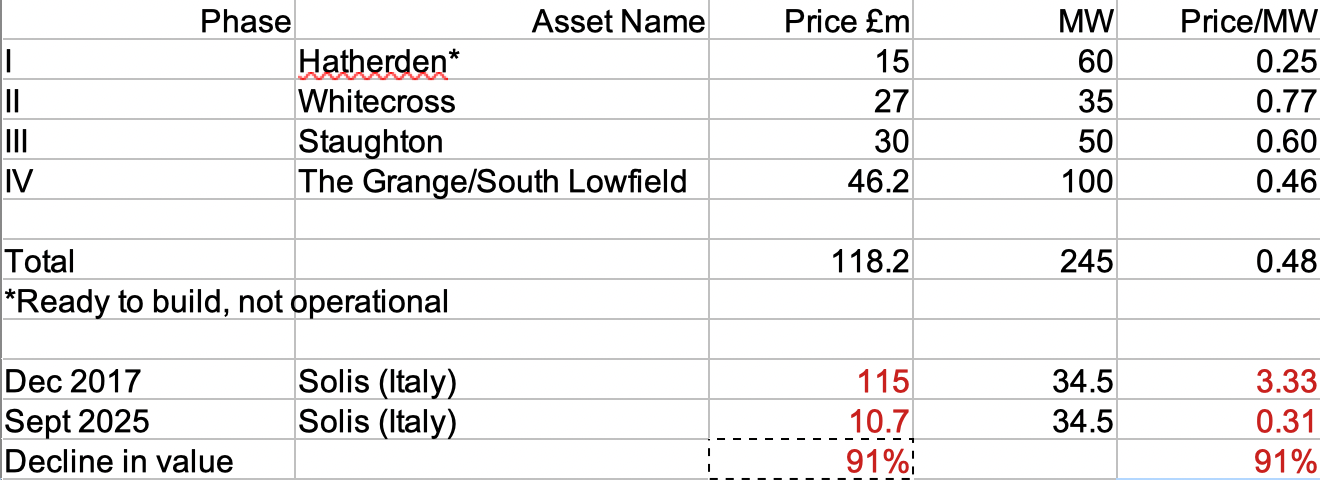

Disposals: In April 2023, NESF announced a “Capital Recycling Programme” which was effectively selling off 245MW of solar capacity. My experience of the banking crisis was that banks sell good assets to achieve prices close to their fair value accounting marks. Toxic assets remain on the balance sheet, to avoid the humiliation of selling at a distressed valuation – this is not how professional management are supposed to behave (cut your losses, run your winners!)

NESF have helpfully disclosed the prices they have sold their assets for, but curiously they haven’t drawn attention to the Solis portfolio (acquired in Italy Dec 2017 for £115m) which has declined in value by 90% according to their own disclosure. So I have helpfully added that to the bottom of the table. The CRP will be extended by selling up to a further 120MW of solar assets.

NESF reported £1.14 billion of invested capital, yet total assets on the balance sheet are well below that level, at £771 million. The reason for the divergence is that management report their financial results on a non-consolidated basis. The group then makes investments in solar panels through special purpose vehicles, which are off the balance sheet. It’s hard to escape the impression that disclosure is deliberately opaque to mask the disappointing cash returns on invested capital.

NESF reported £1.14 billion of invested capital, yet total assets on the balance sheet are well below that level, at £771 million. The reason for the divergence is that management report their financial results on a non-consolidated basis. The group then makes investments in solar panels through special purpose vehicles, which are off the balance sheet. It’s hard to escape the impression that disclosure is deliberately opaque to mask the disappointing cash returns on invested capital.

Valuation: The Dec 2025 NAV was 85p, so the shares are currently trading at around a 50% discount. In reality, I think that reveals investors don’t trust the disclosure, as does the 10% dividend yield on the slashed dividend.

Opinion: My instinct is that the bad news is in the price, but I’m put off by the voluntary disclosure. I cut half my position when the shares briefly rebounded above 75p in summer 2025. I should have been more aggressive. I don’t understand how the government can encourage investment to treble capacity when the existing solar funds have been such disastrous investments.

This also strikes me as showing the limitations of “paid for” research. It’s not Cavendish’s or Quoted Data’s fault, because as NESF are paying for the research, the analyst will parrot the same narrative as management. But that doesn’t help investors, Board’s don’t decide to cut dividends merely because share prices trade at a discount to NAV, the operating cashflow must have disappointed. Yet there’s very little explanation, which suggests that there could be other nasty surprises if management assumptions prove too optimistic yet again.

Close Brothers H1 Jan 2026 and short attack

Fraser Perring’s Viceroy published a short attack on Close Brothers at the start of this week, arguing that the bank was understating provisions from historic car loans mis-selling. The following day CBG released H1 Jan results, showing a H1 Jan £65.5m statutory loss on continuing operations, but a Core Equity Tier 1 ratio of 14.3%. Management said they are “confident that this leaves us well placed to absorb a range of potential outcomes from the FCA’s proposed motor finance commission redress scheme.”

Fraser Perring’s Viceroy published a short attack on Close Brothers at the start of this week, arguing that the bank was understating provisions from historic car loans mis-selling. The following day CBG released H1 Jan results, showing a H1 Jan £65.5m statutory loss on continuing operations, but a Core Equity Tier 1 ratio of 14.3%. Management said they are “confident that this leaves us well placed to absorb a range of potential outcomes from the FCA’s proposed motor finance commission redress scheme.”

Viceroy had a major success against Wirecard, but also have been wrong on occasions (South African lender Capitec). Viceroy suggest that Close Brothers’ redress exposure ranges from £572m to £1.2bn, well above its current £300m provision (which hasn’t been raised from Oct last year). Viceroy’s base case indicates that equity-holders will be “substantially wiped out”. I’d recommend reading Viceroy’s full note here, their argument is that applying average industry assumptions to Close Brothers book is too benign, as CBG was more aggressive with Discretionary Commission Arrangements (DCA) than other lenders, so will be forced to pay out higher customer redress than industry averages.

Naturally CBG management put out a statement saying they “strongly disagree” with the report but in the H1 Jan results do warn that the “ultimate cost to the group could be materially higher or lower than the provision taken and remains subject to further clarity from the FCA on the scope and design of any redress scheme.”

Next steps: Theres a FCA consultation process ongoing, with the details of the final redress scheme published in a couple of weeks (late March).

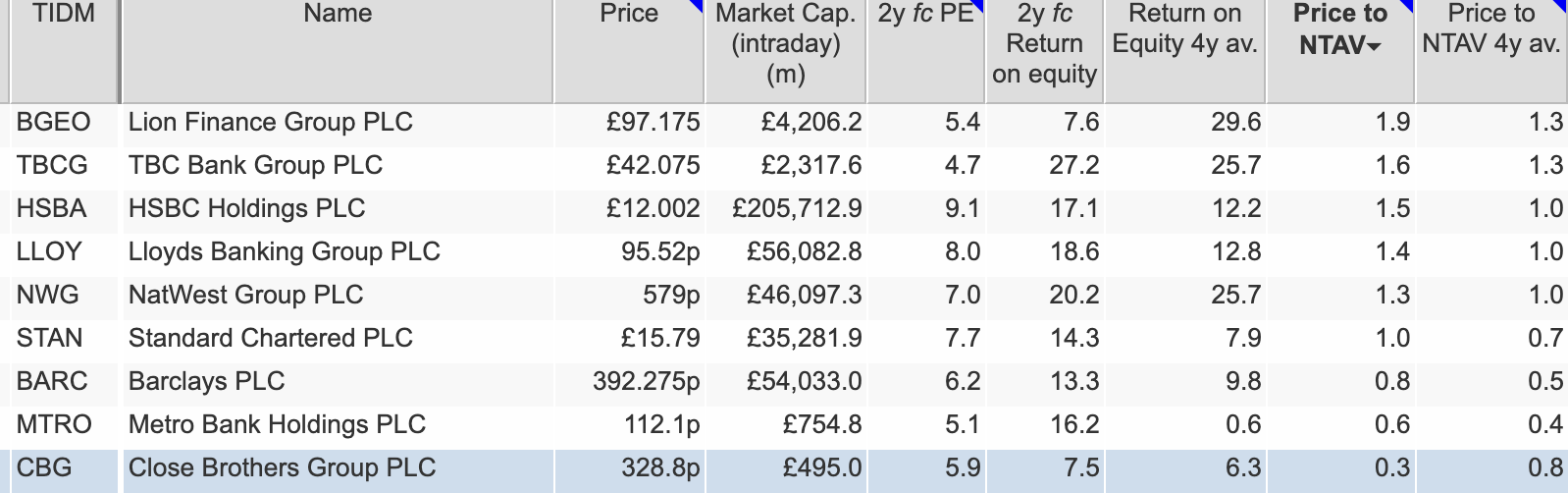

Valuation: CBG trades on Price/NTAV of 0.3x (half the level of Metro Bank, the next lowest, and well below historic levels). CBG is currently the cheapest bank on the London market, even as the rest of the sector has re-rated higher due to a more favourable interest rate environment (HSBC and LLOY are currently on around 1.5x P/NTAV, around a 50% premium to their 4 year average P/NTAV).

Opinion: It’s hard for me to imagine that regulatory action could wipe out shareholders of a bank. The FCA should be more interested in financial stability so they would be reluctant to make the bank sector “uninvestable” yet again. At the very least I would expect CBG to be able to earn its way out of problems over time.

Banks fail because everyone rushes to take their deposits out (Credit Suisse, Northern Rock etc). Close Brothers’ customer deposits did fall -11% to £7.9bn in H1 Jan, but management point out retail deposits have grown from 27% (Jul 2022) financial year to account for 54% (H1 Jan 2026) of total funding. Only 19% of total deposits are available on demand (ie can be withdrawn immediately) and 47% have at least three months to maturity.

So I will stick with my investment here. The FCA publish the rules soon enough, fingers crossed.

Bruce Packard

@bruce_packard

Bruce owns shares in TCAP, NESF and Close Brothers

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Bi-Weekly Market Commentary | 18/03/2026 | NESF, TCAP, CBG | Volatility Rising

AIM has fallen through key moving average support levels, suggesting it may be time to trim portfolios and cut low conviction or losing positions. Companies covered NESF, TCAP and CBG.

This week I look at solar fund NESF, which announced a dividend cut last week and Close Brothers which has come under attack from short seller Viceroy. But I start with TP ICAP the interdealer broker.

TP ICAP FY Dec 2025 Results

They reported a cash balance of £903m, down -15% versus the previous year, “primarily driven by a working capital outflow”. TCAP is a trading business that needs to operate with substantial cash in order for counterparties to trade, they were also carrying gross debt of £802m at the year end. They explain the large swing in working capital as:

“Approximately half of the year-on-year movement reflects changes in net settlement balances that are temporary and reversed immediately after the year end. Other working capital outflows are principally driven by the increase in trade receivable balances due to significant trading activity in December 2025 compared with the prior year, adverse movements in other receivables and creditor balances as well as some provision utilisation.” Capex was £74m driven by investment in technology and “strategic facilities investments.” On the call management said that profits should convert into 100% cash over a 3 year cycle.

I note there’s a “below the line” charge of £53m, mainly from FX translation. That’s around a quarter of the statutory PBT figure, given the TP ICAP is in the trading business, I’m not convinced we should ignore such a large item, as the group suffers from dollar weakness. Management said that at the current spot rates they anticipate a £9-10m FX headwind to 2026 adjusted EBIT.

Parameta: Activist investor Jason Hughes encouraged the group to look at realising value from their Parameta data business. An IPO in New York has been anticipated, but they say conditions remain challenging – try telling that to Elon Musk who thinks he can float SpaceX at a $1.5trillion in June when the planets Jupiter and Venus align. Parameta achieved +5% revenue growth on a constant currency basis (+2% reported). Parameta’s EBIT declined -6% to £76m as management invested to grow the business, however the EBIT margin was still an eye catching 38% (group adj EBIT margin 14.8%). Management were asked about the risk from AI, but said that as their data is proprietary (ie not publicly available) AI was more of an opportunity that a threat.

Outlook: They say 2026 has started well with supportive market conditions, despite the FX headwind they expect to achieve FY Dec 2026F EBIT (Sharescope consensus forecast £362m – TCAP says the range is £347m to £370m in a footnote), so in effect, a +2.7% upgrade on a constant currency basis.

Valuation: The shares are trading on 8x PER Dec 2026F and 2027F. That seems about right given Sharescopes Quality indicators reflect the favourable trading conditions (RoCE and CRoCI is above the 3 year average) but even so returns are only just double digits.

I should have taken a larger position when I bought in 2022. I emailed a friend who had worked in FX options, who had TCAP as a counterparty and knew traders there. Both my friend and his contact were dismissive of the investment case when TCAP shares were trading close to £1 – which I think goes to show that even brokers can be clueless about the investment case in their own organisations.

Next Energy Solar Dividend Cut (Strategic Update)

Last week the group announced a new dividend policy, paying out 75% of operating free cashflow post debt servicing, which equates to 4.0p to 4.6p per share (down from 8.47p FY Mar 2026). That means a dividend c. 10% yield on the current price at 1.3x cover. Management have cut the dividend without explaining to their investors what’s gone wrong. Cavendish, who write “paid for” research, refer to grid outages and cannibalisation – I think the basic problem is that although solar power is “cheap”, solar funds sell power at a discount because they generate power when it isn’t needed (noon on a sunny summer day). You would think that this would be obvious – but the NESF share price has fallen from over 120p in summer 2022 (a few months after Putin invaded Ukraine) to just below 45p currently. The Labour government intends to triple UK solar capacity, but it’s not clear who funds this and why investors should back new solar projects when the existing funds are trading at 40%-50% discounts to NAV.

The dividend cut, buyback pause and NAV discount come at a time when NESF has been enjoying more solar irradiation than budgeted (+10% above forecast), as the slide below shows.

Disposals: In April 2023, NESF announced a “Capital Recycling Programme” which was effectively selling off 245MW of solar capacity. My experience of the banking crisis was that banks sell good assets to achieve prices close to their fair value accounting marks. Toxic assets remain on the balance sheet, to avoid the humiliation of selling at a distressed valuation – this is not how professional management are supposed to behave (cut your losses, run your winners!)

NESF have helpfully disclosed the prices they have sold their assets for, but curiously they haven’t drawn attention to the Solis portfolio (acquired in Italy Dec 2017 for £115m) which has declined in value by 90% according to their own disclosure. So I have helpfully added that to the bottom of the table. The CRP will be extended by selling up to a further 120MW of solar assets.

Valuation: The Dec 2025 NAV was 85p, so the shares are currently trading at around a 50% discount. In reality, I think that reveals investors don’t trust the disclosure, as does the 10% dividend yield on the slashed dividend.

Opinion: My instinct is that the bad news is in the price, but I’m put off by the voluntary disclosure. I cut half my position when the shares briefly rebounded above 75p in summer 2025. I should have been more aggressive. I don’t understand how the government can encourage investment to treble capacity when the existing solar funds have been such disastrous investments.

This also strikes me as showing the limitations of “paid for” research. It’s not Cavendish’s or Quoted Data’s fault, because as NESF are paying for the research, the analyst will parrot the same narrative as management. But that doesn’t help investors, Board’s don’t decide to cut dividends merely because share prices trade at a discount to NAV, the operating cashflow must have disappointed. Yet there’s very little explanation, which suggests that there could be other nasty surprises if management assumptions prove too optimistic yet again.

Close Brothers H1 Jan 2026 and short attack

Viceroy had a major success against Wirecard, but also have been wrong on occasions (South African lender Capitec). Viceroy suggest that Close Brothers’ redress exposure ranges from £572m to £1.2bn, well above its current £300m provision (which hasn’t been raised from Oct last year). Viceroy’s base case indicates that equity-holders will be “substantially wiped out”. I’d recommend reading Viceroy’s full note here, their argument is that applying average industry assumptions to Close Brothers book is too benign, as CBG was more aggressive with Discretionary Commission Arrangements (DCA) than other lenders, so will be forced to pay out higher customer redress than industry averages.

Naturally CBG management put out a statement saying they “strongly disagree” with the report but in the H1 Jan results do warn that the “ultimate cost to the group could be materially higher or lower than the provision taken and remains subject to further clarity from the FCA on the scope and design of any redress scheme.”

Next steps: Theres a FCA consultation process ongoing, with the details of the final redress scheme published in a couple of weeks (late March).

Valuation: CBG trades on Price/NTAV of 0.3x (half the level of Metro Bank, the next lowest, and well below historic levels). CBG is currently the cheapest bank on the London market, even as the rest of the sector has re-rated higher due to a more favourable interest rate environment (HSBC and LLOY are currently on around 1.5x P/NTAV, around a 50% premium to their 4 year average P/NTAV).

Opinion: It’s hard for me to imagine that regulatory action could wipe out shareholders of a bank. The FCA should be more interested in financial stability so they would be reluctant to make the bank sector “uninvestable” yet again. At the very least I would expect CBG to be able to earn its way out of problems over time.

Banks fail because everyone rushes to take their deposits out (Credit Suisse, Northern Rock etc). Close Brothers’ customer deposits did fall -11% to £7.9bn in H1 Jan, but management point out retail deposits have grown from 27% (Jul 2022) financial year to account for 54% (H1 Jan 2026) of total funding. Only 19% of total deposits are available on demand (ie can be withdrawn immediately) and 47% have at least three months to maturity.

So I will stick with my investment here. The FCA publish the rules soon enough, fingers crossed.

Bruce Packard

@bruce_packard

Bruce owns shares in TCAP, NESF and Close Brothers

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.