Stepping in for Bruce this week, Jamie Ward looks at effect of Claude AI on SaaS businesses and wonders whether the banking industry can give insights as to the likely path forward for these businesses. He then reviews RELX (REL), the Schroders (SDR) takeover and Renishaw (RSW).

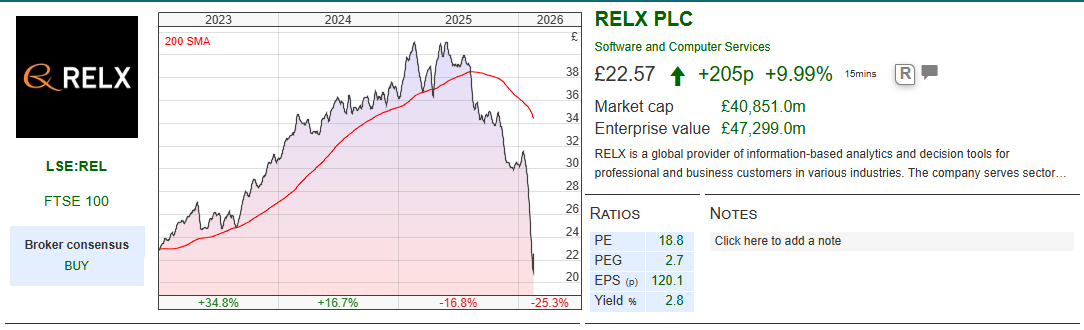

The week before last, Anthropic (maker of the Claude AI) released of a legal automation tool. Parts of stock market had a sharp reaction. This new AI development seeks to automate routine legal tasks and compliance workflows. Its arrival coincided with a significant decline in the share prices of several high-quality British businesses. London Stock Exchange Group, Sage, Experian, and RELX all saw their valuations fall a couple of percent either side of 10% on the day. These movements follow a period of share price disappointment. RELX is now c.50% below its previous highs. Experian has fallen by 40%. Sage and the London Stock Exchange have seen similar pressure.

The fear is that agentic AI software will dismantle the core offerings of these established data and software firms. Investors worry that new technology will simply replace the functions these companies provide. However, this probably overlooks the reality of how deeply these businesses are embedded in their customers’ operations. Extracting a mission-critical software system is not a simple task. Replacing a functional system with a theoretically superior one is a massive risk that most businesses are reluctant to take. It is more probable that these incumbents will integrate AI agents into their own products. Doing so will likely entrench them further into customer workflows rather than making them obsolete.

It’s a bit like the banking sector and current accounts. Most people find the idea of changing their bank account daunting and painful. In a corporate environment, making a major change to software infrastructure is similar to moving bank accounts but on a vastly larger scale. The potential problems associated with switching are complex and fractal. If a business misses even one small detail during a transition, the result can be catastrophic. For companies that rely on mission-critical data, the risk of a botched migration often outweighs the benefits of a new provider.

I volunteer as a treasurer for a local church (two technically), which basically means I look after the bank account and pay the bills etc. We are with Lloyds. It is woeful. We know there are better solutions but the work of getting to the better solution is not worth it. So, I put up with the dreadful service I get at the local branch. The disruption and time required to move accounts are simply too high. I’ve also led a major procurement project for a SaaS system in a large company. It was a hideous experience but had to be done because we were using 1990s technology when we needed to be cutting edge. It was still risky and costly and took months of work and stress.

Within the group of companies mentioned, some appear more exposed than others. One could argue that the London Stock Exchange Group faces the greatest challenge. It does not own a large portion of the data it aggregates and sells. In contrast, Experian owns massive and proprietary databases. This ownership means that AI could actually enhance their competitive position since no one else can train on their data. AI tools require high-quality data to be effective. Consequently, Experian may find that AI makes their data more valuable to their clients.

For a company like Sage, cheaper or even better alternatives have existed for years like Xero or Quickbooks. Nevertheless, customers remain loyal. This is partly because bookkeepers are already trained on Sage systems. The annual cost is relatively low compared to the massive one-off cost and risk of changing systems. Sage will almost certainly integrate AI functionality to make its products more essential. If an agentic mechanism can reduce the manual hours required for finance or customer relationship management, the software becomes even more valuable, not less.

Market sentiment is currently very negative towards these stocks. However, the fundamental reality of customer retention suggests that the threat may be overblown. Markets don’t tend to turn on a sixpence so I wouldn’t bet on any of them recovering soon but they have to worth monitoring. Of course, there will be losers in the AI revolution but I wouldn’t bet on someone vibe-coding embedded SaaS businesses out of existence.

RELX Full Year Results & Buy Back

RELX announced its full year figures for 2025 alongside the continuation of an ongoing share buy scheme. For all the fretting about AI, the update was all very typically RELX. Dull but decent growth, solid margins and a positive outlook. Growth has been improving and management seem to think that trend will continue. The reasons apparently being greater use of decision-making tools driven by technology and its rich dataset. This growth apparently isn’t overly reliant on AI development, but they believe it will help embed the business even more into its customer’s workflow.

There were five acquisitions during the period, which one assumes hasn’t added much growth yet because of annualising. It can be tempting to be a little sniffy when considering acquisition growth but as long as there is a cost discipline (which there is) and they are able to integrate the businesses properly (which there is a good history of), then it can be a worthwhile boost.

Cash returns to shareholders are excellent, and because the shares are so far below the all-time highs, the effect is increased. The dividend yield on the day of the results was 2.9% but more importantly, there is a lot coming back via share buy backs. Last year the company returned £1.5b this way and for 2026, it will return £2.25b. Based on the market cap at time of announcement, this equates another 5.5% on top of the dividend yield. Considering it is generating high single digit growth, this seems very attractive.

Valuation

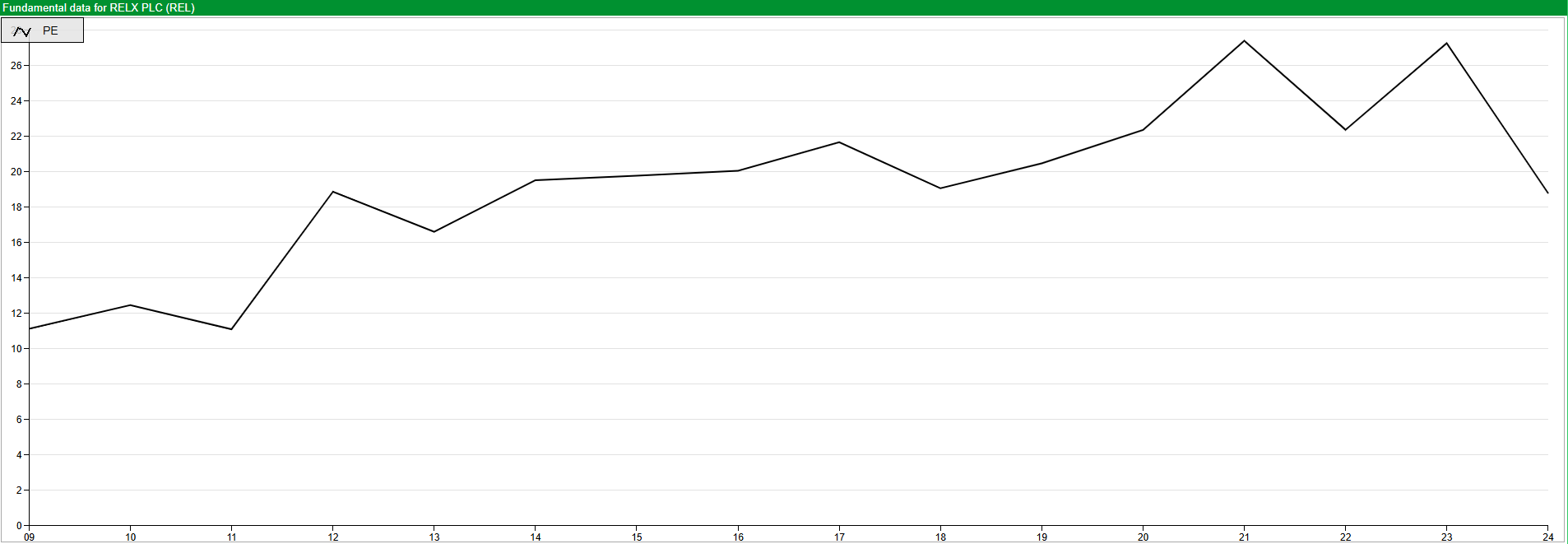

RELX has, deservedly spent much of its history trading over 20x price earnings ratio and occasionally even breaching 30x. For this year, ShareScope is showing forecasted earnings of 141p per share and 154p for the following year, which means it is trading somewhere near to 15x. This is cheap for the stock. On the day of the results the shares popped 10% higher but this was off a price of c. 2000p, which is less than half the level it was just nine months ago.

Opinion

Sentiment can be a pig and even when a company is demonstrably doing well it can a while before markets wake up. RELX is a tremendous business and, as mentioned above, I think the fears of it being replaced by spotty fifteen-year-old vibe-coding a replacement is incredibly unlikely (other demographics of developers are available). That said, I’m not tempted to buy just yet because it’s easy to foresee the market taking fright a couple more times before the reality of the effect of AI sinks in. It’s definitely one to watch though.

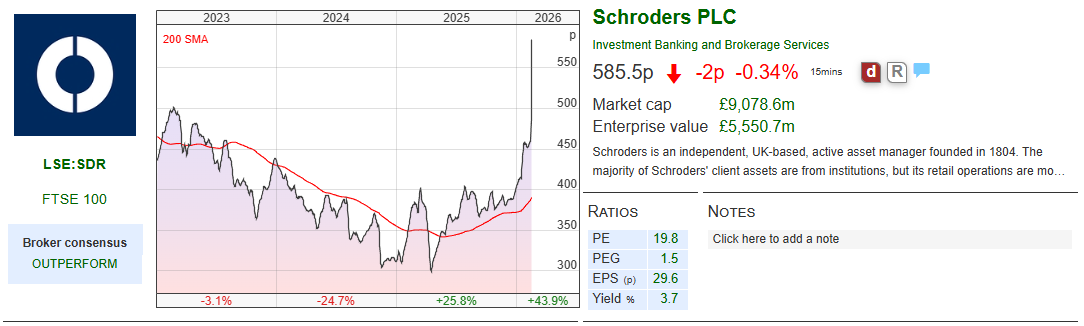

Schroders Take Over

The announced takeover of Schroders was a bit of a surprised. Most in the city hadn’t even heard of Nuveen, the acquirer, until the announcement, despite it apparently employing c. 500 people in London. This marks the thirteenth FTSE350 company to be subject to a takeover approach in as many months. As a major name in investment management, its disappearance is a particularly on-the-nose confirmation of the shrinking London stock market.

Given such as large amount remains held by the Schroders family, one would suppose that they were ultimately on one side of the negotiation with the Schroders board playing a secondary role. This will take the firm out of control of the family after 222 years. Part of the stipulation is for the name to remain, which makes sense; a, it is a well-known brand and b, the Schroders family doubtless see their family history entwined into the Square Mile and would be reluctant to see it disappear.

Valuation

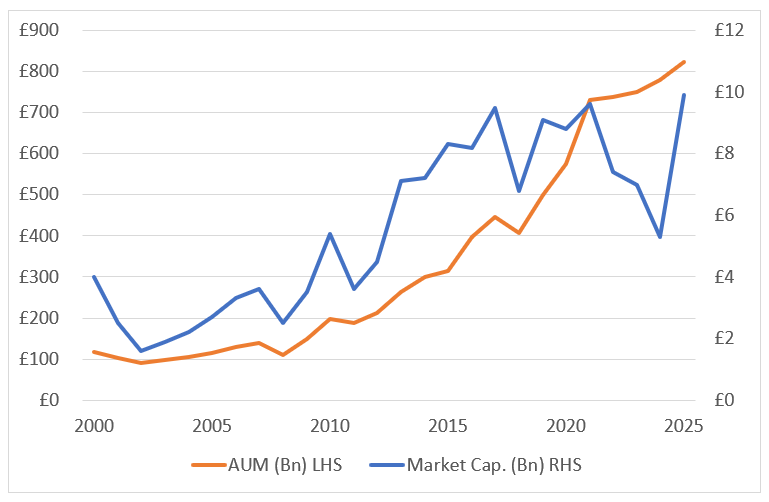

The combined entity will have c. $2.5 trillion under management placing it around number ten in the largest asset management firms globally. Schroders makes up slightly less than half this figure and the takeover price is equivalent to roughly 1.2% of assets under management. Once upon a time, 2% would be the minimum and for really special asset management firms, it could be much higher. But such is the diminishing income proportional to those assets that 1.2% is probably about right and compares to just less than 1% prior to the announcement. The clearest way you can see the destruction of value wrought by regulatory burdens is where it sits compared to history.

Ten years ago, it had the same market capitalisation on less than a third of the assets under management

Opinion

Takeovers in asset management seem to be coming from a position of weakness. The whole sector has been under pressure since a slew of regulations came in in the aftermath of the global financial crisis. The most recent ones being the Assessment of Value and Consumer Duty regulations, which will place even more pressure on fees and force costs even high.

To cope, asset management need to get bigger and bigger to be competitive. There is a dedication to maintain a large London presence – indeed the non-US headquarters (whatever that means in practice). Ultimately, though this only makes sense if Nuveen can strip out duplicated processes and reduce unprofitable products. This means job losses, fund closures/mergers and downsizing.

The glory days of asset management firms being a license to print money are firmly in the rear-view mirror. Whilst I wouldn’t advocate this sector as containing long-term winners, there will be more mergers in the future. If you get lucky, you might own one of the ones that get taken over (as opposed to the one making the takeover), but this isn’t an investment strategy, it is hope. I’d highlight a few potential contenders for being approached but I wouldn’t invest myself, these are: mid-caps with institutional mandates that might be attractive to US bidders like ABRDN (stupid name), M&G (known in the City as Mean & Greedy), Man Group, NinetyOne and Quilter. Smaller companies that are too small to remain competitive in the long run. These include; Liontrust, Brooks McDonald, Jupiter and Ashmore. Long term however, two dead birds, they have four wings but they still cannot fly.

Renishaw – Half Year Figures

Having been in the doldrums for a while, Renishaw released a decent update last week. In recent years, the industrial markets exposed areas have struggled and that remains the case to a degree. But the group level performance was strong with constant currency revenue growth being 11.5%. Operational gearing saw operating profit growth of almost 50%.

Renishaw is a very good business but has a famously short sales visibility. The earnings power is plain to see though with price rises successful put through to entirely offset the effect of tariffs. The outlook was positive with Will Lee (CEO) guiding £132m to £157m in pre-tax profits against market expectations of c. £142m.

Really though, Renishaw could earn a lot more than it does. The company has a large R&D budget and expenses everything it can, which lowers the reported profits significantly. Arguably, this is the correct thing to since some projects have to be written off. Nonetheless, the shares hit almost 7000p in 2021 when it was announced that they would be willing to be acquired by another firm. Investors were excited that the company would be ran for cash flow rather than investment growth. When a takeover didn’t happen the share more than halved and haven’t risen much since.

Valuation

For a cyclical business like Renishaw, enterprise value to capital employed can give a decent steer as to when shares a cheap within the cycle. It has spent much of its history trading in the range of 3x to 3.5x capital employed, implying that the investments that the company make return 3 to 3.5 times their value. At present it is towards the lower end of this band.

There was a period in the run up to the attempted sale where it got to over 5x, but this was partly driven by excitement about additive manufacturing, where the company is carving out a leading niche. It’s clearly not as cheap as it was when the shares were less than 3000p but at 4200p they aren’t obviously expensive if you look beyond the depressed earnings. I would suggest that without a takeover approach, the shares would start to look expensive around 5000p.

Opinion

Renishaw is a great British business but it rarely gets the recognition it deserves. I wrote an obituary in Moneyweek to its founder, David McMurtry last year in which I expressed a desire to see his legacy of investment and innovation continued rather than running the company purely for cash flow. As far as I can tell, his legacy is in place. In the long-term I suspect that is good for shareholders but in the short term a lot of money could be made if it was ran for cash flow. I don’t currently own the shares, although I did when it was lower but I am always interested in the company when the shares become periodically cheap.

Jamie Ward

@JamieCDubya

https://wonderstcks.substack.com/

Jamie owns none of the companies mentioned

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Thank you for an interesting read. I really like RELX.

Renishaw is a long term hold for me.