Six shares pass 5 strikes this time. Richard takes a closer look at Morgan Sindall, which achieved no strikes. The building contractor and property developer is a complex business, as demonstrated by its loss-making Muse subsidiary.

5 Strikes

Since my last update, 11 shares have published annual reports and passed my minimum quality filter. Six of them achieved less than three strikes when I scrutinised their numbers.

| Name | TIDM | Prev AR | Strikes | # Strikes |

|---|---|---|---|---|

| BMY | Bloomsbury Publishing | 19/6/26 | – Growth | 1 |

| MTO | Mitie | 19/6/26 | ? Acquisitions ? CROCI – Debt – Growth ? ROCE – Shares | 5 |

| CMCX | CMC Markets | 16/6/26 | – CROCI – Growth ? ROCE | 3 |

| TAM | Tatton Asset Management | 16/6/26 | 0 | |

| PAY | PayPoint | 11/6/26 | – Holdings – Debt – Growth | 3 |

| QQ. | QinetiQ | 10/6/26 | ? Holdings ? Acquisitions ? Growth – ROCE | 2 |

| OXIG | Oxford Instruments | 9/6/26 | – Holdings – Growth | 2 |

| PETS | Pets at Home | 9/6/26 | – Holdings ? Growth | 1 |

| AUTO | Autotrader | 8/6/26 | 0 | |

| RS1 | RS | 8/6/26 | – Holdings ? Acquisitions ? Debt – Growth | 3 |

| AAZ | Anglo Asian Mining | 2/6/26 | – CROCI ? Debt – Growth – ROCE | 3 |

| Click here for our 5 Strikes explainer | 23/06/2026 | |||

The six 5 Strikes winners are Bloomsbury Publishing [- Growth], Tatton Asset Management [No strikes], Oxford Instruments [- Holdings – Growth], Pets at Home [- Holdings ? Growth], and Autotrader [No strikes].

They join my research list, which is all the shares that have achieved less than three strikes so far in 2026. It is included at the end of this article.

I am researching the shares with the fewest strikes first. Next on the list is Morgan Sindall.

Morgan Sindall [No strikes]

Morgan Sindall is a rarity. There are no significant blemishes in its numbers. I examined the construction company last year and concluded that it is a complicated collection of businesses.

The company says its superpower is the way its business units support each other, but I think its superpower is one of the units: Fit Out.

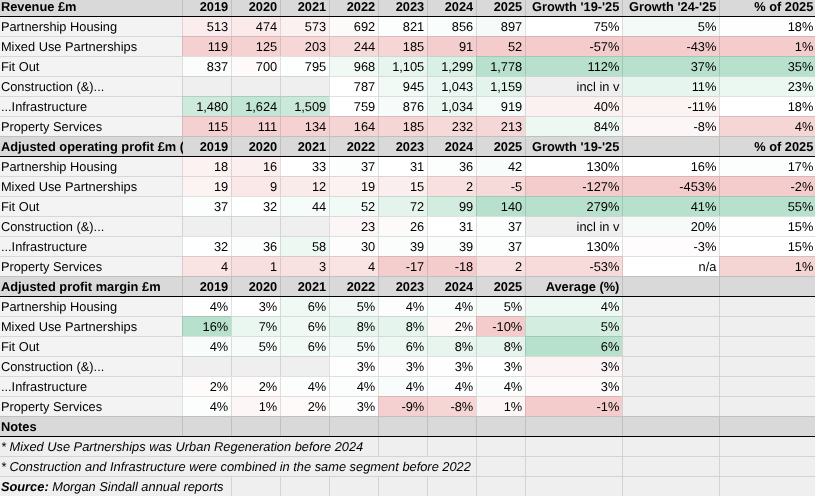

To reacquaint us with Morgan Sindall, I have updated the segmental analysis. It exposes Morgan Sindall’s complexity and helps us understand how it performed in the year to December 2025.

Just so we know what we are talking about, here’s a brief description of each business unit:

Partnership Housing, which trades as Lovell, and Mixed Use Partnerships which trades as Muse, are property developers. They invest in land, materials, and work in progress and earn revenue as properties are developed for customers or sold.

Through these subsidiaries, Morgan Sindall partners with local authorities, landowners and housing associations. Partnership Housing primarily builds homes. Mixed Use Partnerships regenerates urban areas with new homes, offices, shops and amenities.

Partnership shares risk and requires less capital than buying and banking land like many developers do. However once Morgan Sindall is developing a project it still requires capital to buy land and build on it.

This capital comes from Morgan Sindall’s cash generative contracting businesses: Fit out, Construction, and Infrastructure. The company depicts a virtual circle, because these business units are often employed for the building.

Fit Out is Overbury and Morgan Lovell. Primarily they refurbish and build new office interiors. Morgan Sindall Construction builds exteriors. Much of its work is for the public sector. Morgan Sindall Infrastructure and BakerHicks are civil engineering businesses that work on road, rail, aviation, energy and industrial projects.

Morgan Sindall Property Services repairs and maintains residential property for local authorities. Due to cost inflation it lost money in 2023 and 2024, but it made a tiny profit in 2025. Since it only accounts for 4% of revenue I am focusing on the more consequential parts of the business today.

The table shows revenue, adjusted operating profit and adjusted profit margin from 2019 to 2025. For each of the three metrics it uses a colour scale to show which of Morgan Sindall’s six business units achieved the best number (green), which were average (white) and which achieved the worst number (pink).

For example, the smallest businesses by revenue throughout the period were Mixed Use Partnerships and Property Services. Construction and Infrastructure started out the biggest but in 2022 it was divided in two, and Fit Out emerged as the biggest division.

The growth of Fit Out should not be underestimated. Since 2019 it has grown revenue by 112%. It has grown more than any other division and contributed 35% of total revenue, also more than any other in 2025.

Turning to profit, Fit Out’s performance is even more impressive. Adjusted operating profit has increased 279%, contributing more than half (60%) of total adjusted operating profit. This is because the division’s profit margin has increased from 4% to 8%. It was the most profitable division in 2025, and on average between 2019 and 2025.

The two questions in my mind are the sustainability of Fit Out’s extraordinary growth, and the suitability of the property development businesses as beneficiaries of Fit Out’s excess cash.

Slowing growth

In 2024 the company anticipated a slow down in Fit Out’s growth. Since the pandemic it has benefitted as employers have redesigned offices to accommodate flexible working practices, make them more attractive to employees and improve energy efficiency.

Morgan Sindall expected growth to moderate in 2025, but actually it accelerated.

The annual report, though, dampens our enthusiasm: “…the division is expected to have another strong year in 2026, with profits lower than 2025 but still significantly above the top end of the medium-term target range.”

In a subsequent trading update Morgan Sindall changed its mind again, and put a number on the medium term target range: “[Fit Out] Profits are now expected to be significantly ahead of previous expectations and further exceed the top-end of its Medium-Term Target of £80m – £100m.”

As my table shows, Fit Out profit in 2025 was £140 million, so a medium-term target of £80m to £100m is quite a come down even if Fit Out beats it in 2026.

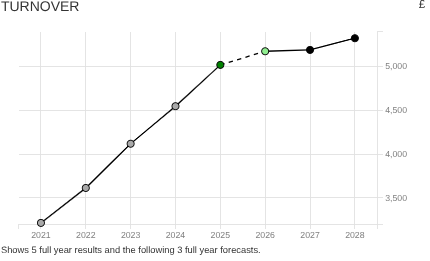

Fit Out has been the main driver of growth, which is why the consensus of 7 analysts in ShareScope is much lower growth in future:

Source: ShareScope Financials > Forecasts

Risky business

Meanwhile losses at Muse (Mixed Use Partnerships) stem from a high level of spending on projects that have yet to start and a low level of project completions. Morgan Sindall says it has been converting bids into partnership agreements, some of which are starting on site this year.

It has also failed to generate the returns it expected from apartment sales in London because people cannot afford London properties.

These developments show that projects take a long time to generate a return and that return is by no means guaranteed.

Although House Partnerships has been a more reliable earner, I am cautious about extrapolating Morgan Sindall’s great financial track record into the future. It could be that 2019-2025 was an unusually propitious time.

I am not dropping Morgan Sindall from my research list though. I am intrigued. The company is confident the projects Muse is just starting may be lucrative in years to come.

In the annual report the company says: “Given the Board’s increased confidence in the long-term prospects for this division, the medium-term target for Mixed Use Partnerships has been increased to generate a return on capital up towards 30%.”

All the 0’s, 1’s and 2’s

So far this year, 67 Shares have passed 5 Strikes. 37 achieved two strikes, 19 achieved 1 strike and 11 achieved no strikes.

These aren’t necessarily good investments. They have performed well in the past, and because their pasts are relatively uncomplicated, they ought to be relatively easy to evaluate.

Forming an opinion on the future requires further analysis, which is why these companies have joined my research list. The shares I have already researched in more detail this year are linked in the table.

Morgan Sindall and Nichols joined the list this time even though they published their annual reports back in March. I am not sure how they evaded me, but I spotted the error in a recent check and have added them back in.

| Name | TIDM | Prev AR | Strikes | # Strikes | Link |

|---|---|---|---|---|---|

| CER | Cerillion | 12/1/26 | 0 | > | |

| HWDN | Howden Joinery | 25/2/26 | ? Holdings | 0 | > |

| PRV | Porvair | 11/3/26 | ? Holdings | 0 | > |

| NICL | Nichols | 23/3/26 | 0 | > | |

| MGNS | Morgan Sindall | 24/3/26 | 0 | ||

| QTX | Quartix | 25/3/26 | ? ROCE | 0 | > |

| CCC | Computacenter | 8/4/26 | 0 | > | |

| FOUR | 4imprint | 14/4/26 | ? Holdings | 0 | > |

| KEYS | Keystone Law | 13/5/26 | 0 | > | |

| AUTO | Autotrader | 8/6/26 | 0 | ||

| TAM | Tatton Asset Management | 16/6/26 | 0 | ||

| BOWL | Hollywood Bowl | 5/1/26 | – Debt | 1 | > |

| MEGP | Me International | 23/3/26 | – Growth ? ROCE | 1 | > |

| ALFA | Alfa Financial Software | 24/3/26 | – Growth | 1 | > |

| GAMA | Gamma Communications | 24/3/26 | ? Acquisitions – Holdings | 1 | |

| INCH | Inchcape | 24/3/26 | – Growth | 1 | |

| ROR | Rotork | 27/3/26 | – Holdings ? Growth | 1 | |

| CKN | Clarkson | 30/3/26 | ? Growth – ROCE | 1 | |

| RMV | Rightmove | 30/3/26 | – Holdings | 1 | |

| IMI | IMI | 31/3/26 | ? Holdings – Debt ? Growth | 1 | |

| FDM | FDM | 10/4/26 | – Growth | 1 | > |

| HILS | Hill & Smith | 10/4/26 | – Holdings ? Acquisitions | 1 | |

| NXT | Next | 16/4/26 | – Debt | 1 | |

| BAG | Barr (AG) | 21/4/26 | ? Acquisitions ? Growth | 1 | |

| SAG | Science | 21/4/26 | ? Growth | 1 | |

| ELCO | Eleco | 9/5/26 | – Holdings ? Growth | 1 | |

| LSC | London Security | 15/5/26 | – Holdings | 1 | |

| W7L | Warpaint London | 22/5/26 | – Shares ? Growth | 1 | |

| PETS | Pets at Home | 9/6/26 | – Holdings ? Growth | 1 | |

| BMY | Bloomsbury Publishing | 19/6/26 | – Growth | 1 | |

| RWS | RWS | 8/1/26 | ? Acquisitions – Growth – ROCE | 2 | > |

| IHP | IntegraFin | 9/1/26 | – CROCI | 2 | |

| RFX | Ramsdens | 15/1/26 | – CROCI ? Growth ? ROCE | 2 | > |

| REL | RELX | 19/2/26 | ? Holdings – Debt ? Growth | 2 | > |

| IHG | InterContinental Hotels | 26/2/26 | ? Holdings – Debt | 2 | |

| DATA | GlobalData | 2/3/26 | ? Acquisitions – Debt ? ROCE | 2 | > |

| GSK | GSK | 6/3/26 | ? Holdings – Debt ? Growth | 2 | |

| MONY | Mony | 9/3/26 | – Holdings ? Growth | 2 | |

| STEM | SThree | 9/3/26 | – Holdings – Growth | 2 | |

| CTEC | ConvaTec | 10/3/26 | ? holdings – Debt ? Growth ? ROCE | 2 | > |

| BNZL | Bunzl | 17/3/26 | ? Holdings – Debt – Growth | 2 | > |

| HIK | Hikma Pharmaceuticals | 18/3/26 | ? Acquisitions – Debt | 2 | |

| YU. | Yu | 18/3/26 | – CROCI ? ROCE | 2 | |

| JSG | Johnson Service | 19/3/26 | – Holdings – Debt | 2 | |

| ITRK | Intertek | 20/3/26 | ? Holdings – Debt ? Growth | 2 | |

| BA. | BAE Systems | 24/3/26 | ? Holdings ? Acquisitions – Debt ? Growth | 2 | > |

| DOM | Domino’s Pizza | 24/3/26 | – Holdings – Debt ? Growth | 2 | |

| LUCE | Luceco | 25/3/26 | ? Acquisitions – Debt ? Growth ? ROCE | 2 | |

| BBY | Balfour Beatty | 2/4/26 | – Holdings ? CROCI ? Growth – ROCE | 2 | |

| APTD | Aptitude Software | 8/4/26 | – Holdings ? Acquisitions – Growth | 2 | |

| IGG | IG | 8/4/26 | – Holdings – Growth | 2 | |

| SPX | Spirax | 8/4/26 | – Holdings – Debt ? Growth | 2 | |

| SVS | Savills | 9/4/26 | – Holdings – CROCI ? Growth ? ROCE | 2 | |

| MACF | Macfarlane | 10/4/26 | – Holdings – Debt ? Growth | 2 | > |

| PAGE | PageGroup | 13/4/26 | – Holdings? CROCI – Debt – Growth – ROCE | 2 | |

| CAML | Central Asia Metals | 15/4/26 | – Growth ? ROCE | 2 | |

| FEVR | Fevertree Drinks | 20/4/26 | – CROCI – Growth | 2 | |

| JDG | Judges Scientific | 22/4/26 | ? Acquisitions – Debt – Growth | 2 | > |

| WINK | M Winkworth | 24/4/26 | – Holdings – Growth | 2 | |

| EKF | EKF Diagnostics | 27/4/26 | ? CROCI – Growth ? ROCE | 2 | |

| IOF | Iofina | 1/5/26 | ? CROCI – ROCE ? Shares | 2 | |

| AEO | Aeorema Communications | 18/5/26 | – CROCI ? Growth ? ROCE | 2 | |

| ASY | Andrews Sykes | 18/5/26 | – Holdings – Growth | 2 | |

| CARD | Card Factory | 21/5/26 | – Holdings – Debt | 2 | |

| ANP | Anpario | 1/6/26 | ? CROCI – Growth ? ROCE | 2 | |

| OXIG | Oxford Instruments | 9/6/26 | – Holdings – Growth | 2 | |

| QQ. | QinetiQ | 10/6/26 | ? Holdings ? Acquisitions ? Growth – ROCE | 2 | |

| Click here for our 5 Strikes explainer | 23/06/2026 | ||||

Richard Beddard

Contact Richard Beddard by email: richard@beddard.net, web: beddard.net

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.