Bruce looks at OPT, the occupational health group, OMG the cash rich motion sensor company and logistics software group SAAS, which has suffered its own SaaS Apocalypse.

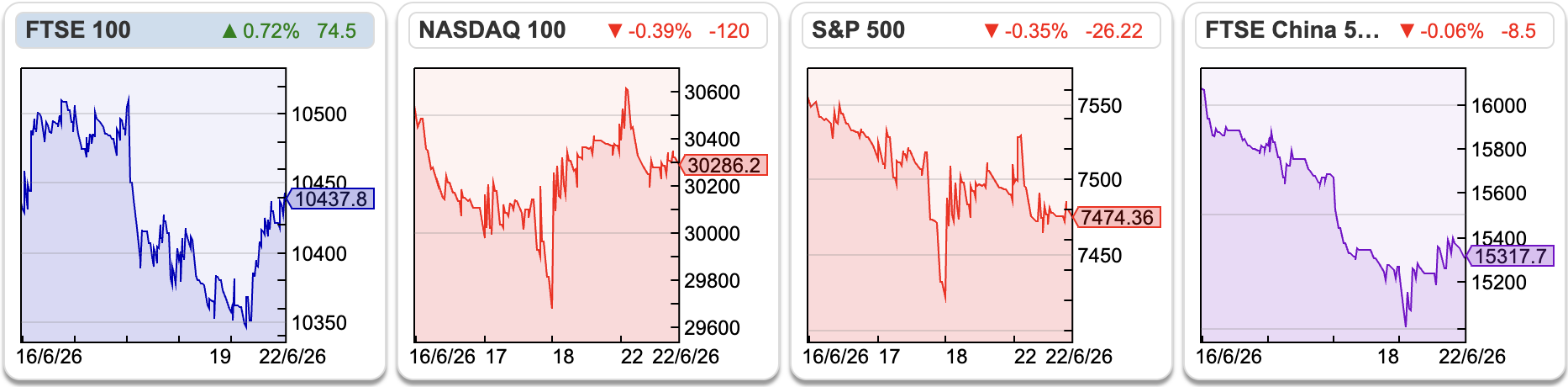

The FTSE 100 was flat over the last 5 trading days at 10,437. Nasdaq100 and S&P500 were +2.1% and +0.5% over the same time period while the FTSE China 50 fell -4.8%. XIN0 is the worst performing index YTD, down -12% while the Nikkei 225 is up +44%, followed by the Nasdaq100 up +21% YTD. Some of that is index composition, with FTSE China 50 consisting of traditional financials, consumer platforms like Meituan and low margin State Owned Enterprises (SOEs) whereas the US and Japanese indices contain groups with pricing power to better cope with the energy price shock from the Straits of Hormuz being closed.

The FTSE 100 was flat over the last 5 trading days at 10,437. Nasdaq100 and S&P500 were +2.1% and +0.5% over the same time period while the FTSE China 50 fell -4.8%. XIN0 is the worst performing index YTD, down -12% while the Nikkei 225 is up +44%, followed by the Nasdaq100 up +21% YTD. Some of that is index composition, with FTSE China 50 consisting of traditional financials, consumer platforms like Meituan and low margin State Owned Enterprises (SOEs) whereas the US and Japanese indices contain groups with pricing power to better cope with the energy price shock from the Straits of Hormuz being closed.

In the UK, Sir Keir Starmer started the week by resigning as Prime Minister. This was widely expected and had limited effects on financial markets. For instance, ShareScope shows UKTSY10 has fallen below 4.8% versus a peak of 5.15% in mid May.

I’m currently reading Katie Prescott’s book: The Curious Case of Mike Lynch: The Improbable Life & Death of a Tech Billionaire. Autonomy was co-founded by Lynch in the 1990’s, and was one of the UK’s original internet darlings, for several years there had been question marks about the accounting but then in 2011 the business was sold to HP for almost $12bn. Roger Phillips who I used to work with at Evolution, was telling anyone who would listen in 2009 that cash conversion seemed curiously low quality for a software group. Derek Brown, my former Head of Research at Seymour Pierce was the Head of Investor Relations when Autonomy was sold, also gets a mention in the book. A year after HP bought the UK group they wrote off $9bn of the goodwill they had paid. Court cases, civic and criminal followed. The story has a tragic end, as Mike Lynch drowned when his yacht, The Bayesian, capsized off the coast of Sicily in 2024.

I’m currently reading Katie Prescott’s book: The Curious Case of Mike Lynch: The Improbable Life & Death of a Tech Billionaire. Autonomy was co-founded by Lynch in the 1990’s, and was one of the UK’s original internet darlings, for several years there had been question marks about the accounting but then in 2011 the business was sold to HP for almost $12bn. Roger Phillips who I used to work with at Evolution, was telling anyone who would listen in 2009 that cash conversion seemed curiously low quality for a software group. Derek Brown, my former Head of Research at Seymour Pierce was the Head of Investor Relations when Autonomy was sold, also gets a mention in the book. A year after HP bought the UK group they wrote off $9bn of the goodwill they had paid. Court cases, civic and criminal followed. The story has a tragic end, as Mike Lynch drowned when his yacht, The Bayesian, capsized off the coast of Sicily in 2024.

Lynch thought that financial analysts who questioned Autonomy’s accounting were “corrupt”. Walking down Piccadilly he suggested one bear could be persuaded to change his “sell” recommendation, blurting out “I’ve got £100m in the bank. Surely we can fix this with a big bag of drugs and a bag of money and a prostitute?” His outburst reveals he never understood the motivation of analysts who questioned the story.

Speaking of boats, in an attempt to recreate the ShareScoping marketing, I have been writing this from my laptop on a boat. Readers will be pleased that I have not included any photos looking into the sunset with my shirt off though.

This week I look at Optima Health, the “corporate wellbeing” outsourcing group, descended from Marlowe’s restructuring. Oxford Metric’s Capital Market’s Day and Microlise, the enterprise software group.

This week I look at Optima Health, the “corporate wellbeing” outsourcing group, descended from Marlowe’s restructuring. Oxford Metric’s Capital Market’s Day and Microlise, the enterprise software group.

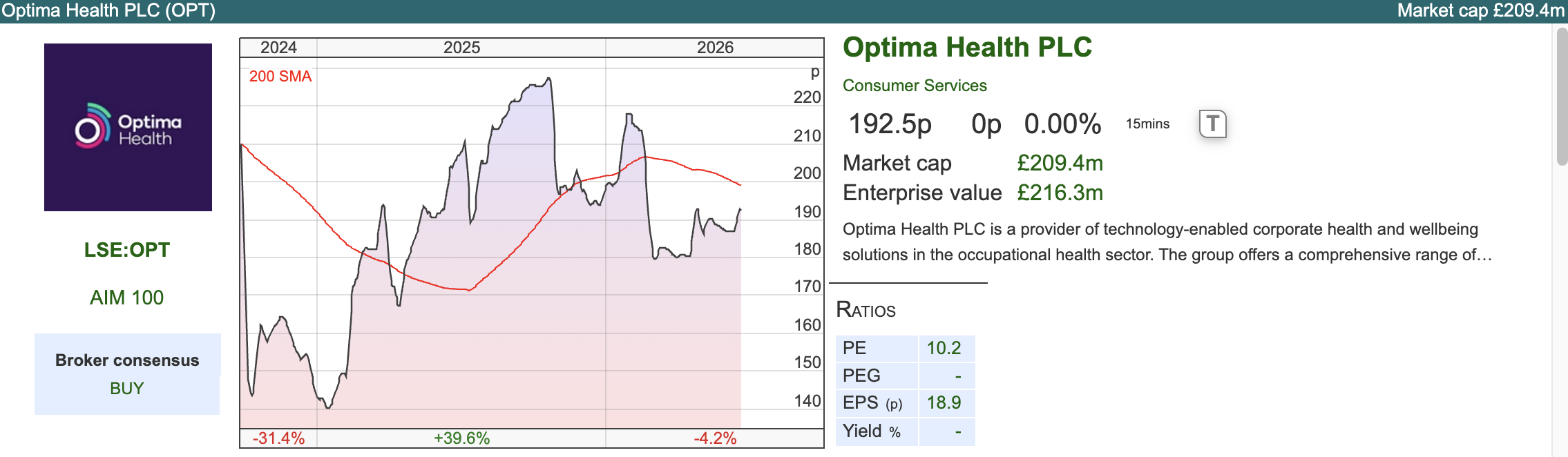

Optima Health FY Mar Trading Update

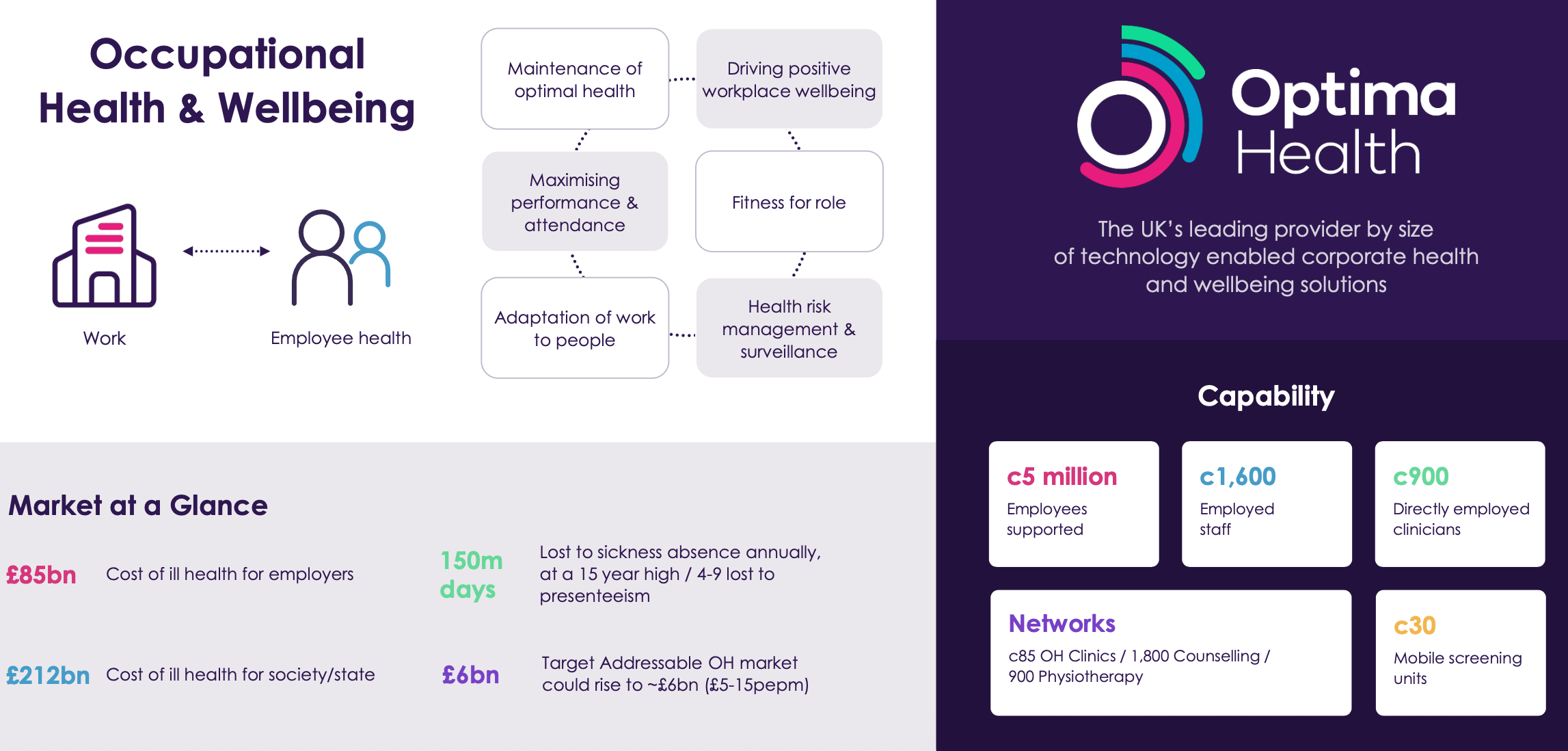

This “corporate wellbeing” group is effectively a B2B outsourcing company that helps large organisations keep track of mandated medical checks for industrial, construction, or transport workers (e.g., lung function, hearing tests, or eye sight tests for train drivers). Lord Ashcroft owns 28%, via his involvement in Marlowe (the safety and regulatory compliance giant from which Optima Health was demerged).

This “corporate wellbeing” group is effectively a B2B outsourcing company that helps large organisations keep track of mandated medical checks for industrial, construction, or transport workers (e.g., lung function, hearing tests, or eye sight tests for train drivers). Lord Ashcroft owns 28%, via his involvement in Marlowe (the safety and regulatory compliance giant from which Optima Health was demerged).

Last week OPT said FY Mar revenue would be up + 15% to £121m (inline) and adj EBITDA approximately 10% ahead of expectations. Normally I would expect a group to publish FY Mar results before the end of June, but Optima has just completed the acquisition of PAM (People Asset Management) Healthcare for £100m total cash consideration, a couple of days before their year end. That equates to 12x EV/historic EBITDA. Net debt was £94m at the end of March, but has fallen since then as they repaid a £30m shareholder bridging loan associated with the deal, using proceeds from an April equity raise (£35m at 175p per share).

Last week OPT said FY Mar revenue would be up + 15% to £121m (inline) and adj EBITDA approximately 10% ahead of expectations. Normally I would expect a group to publish FY Mar results before the end of June, but Optima has just completed the acquisition of PAM (People Asset Management) Healthcare for £100m total cash consideration, a couple of days before their year end. That equates to 12x EV/historic EBITDA. Net debt was £94m at the end of March, but has fallen since then as they repaid a £30m shareholder bridging loan associated with the deal, using proceeds from an April equity raise (£35m at 175p per share).

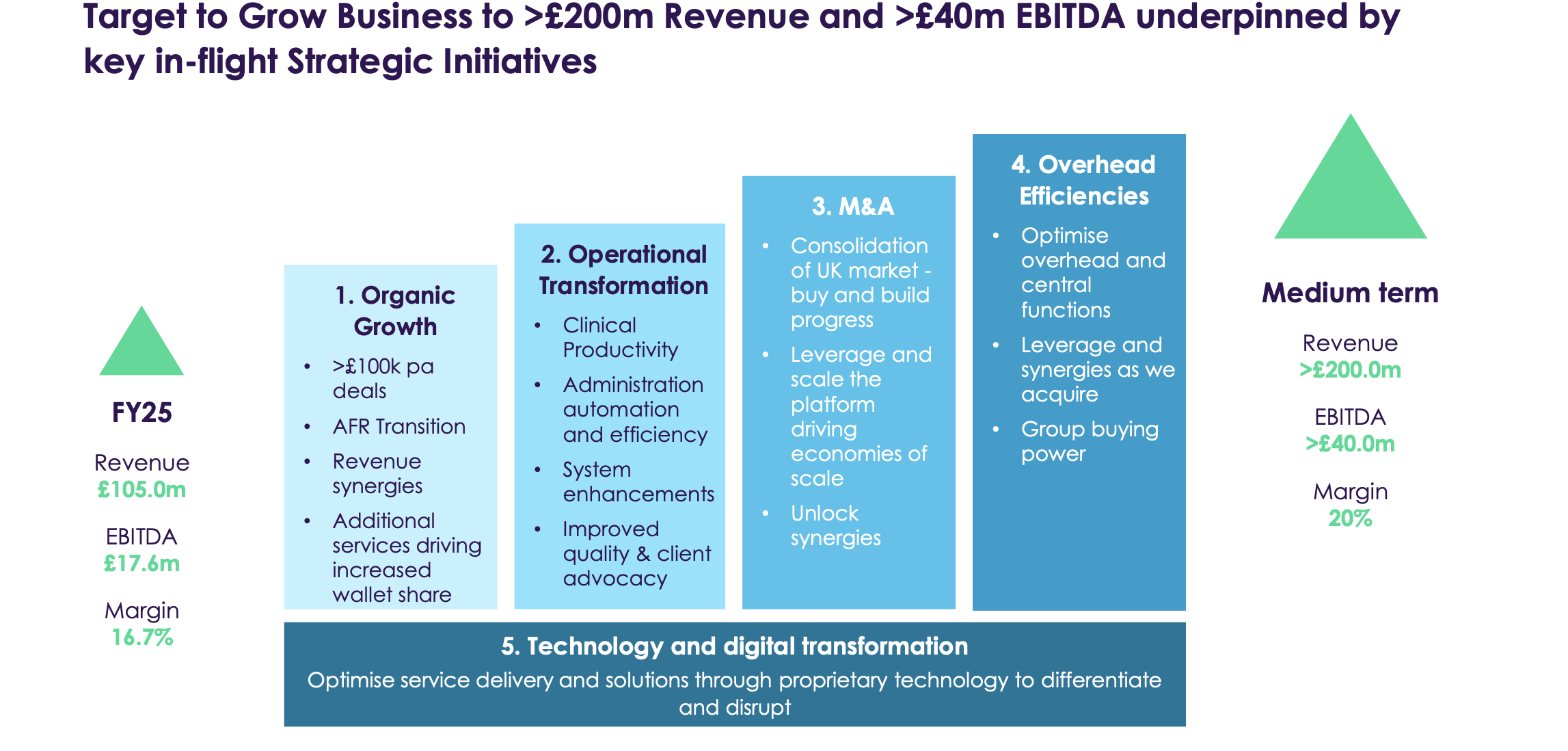

History: This came to market in Sept 2024, and the Admission Document suggests the Total Addressable Market in the UK should be around £1.4bn in 2028, underpinned by statutory demands placed on employers by the Health and Safety at Work Act. Optima has around 10% market share, but is the largest provider approximately 1.8x bigger than the second largest provider by revenue. According to Cavendish, there’s a long term ambition to achieve 25% market share (ie over £350m of revenue). The group has medium term targets of: greater than £200m revenue, greater than £40m EBITDA and 20% EBITDA margin.

Valuation: Cavendish, their broker, are expecting revenue to jump +72% FY Mar 2027F to £208m (that is, achieving the revenue target, but not the EBITDA or margin target). Most of that growth comes from the PAM deal. FY Mar 2028F revenue grow drops to a still healthy +11%. Adjusted EPS of 17.5p the same year implies a PER of 11x FY Mar 2028F.

Valuation: Cavendish, their broker, are expecting revenue to jump +72% FY Mar 2027F to £208m (that is, achieving the revenue target, but not the EBITDA or margin target). Most of that growth comes from the PAM deal. FY Mar 2028F revenue grow drops to a still healthy +11%. Adjusted EPS of 17.5p the same year implies a PER of 11x FY Mar 2028F.

Opinion: Debt funded, acquisition led growth does tend to be treated with scepticism by investors, but I think given Lord Ashcroft’s involvement we should give this the benefit of the doubt. Valuation looks attractive, so gets the thumbs up from me, though I don’t own any myself.

Opinion: Debt funded, acquisition led growth does tend to be treated with scepticism by investors, but I think given Lord Ashcroft’s involvement we should give this the benefit of the doubt. Valuation looks attractive, so gets the thumbs up from me, though I don’t own any myself.

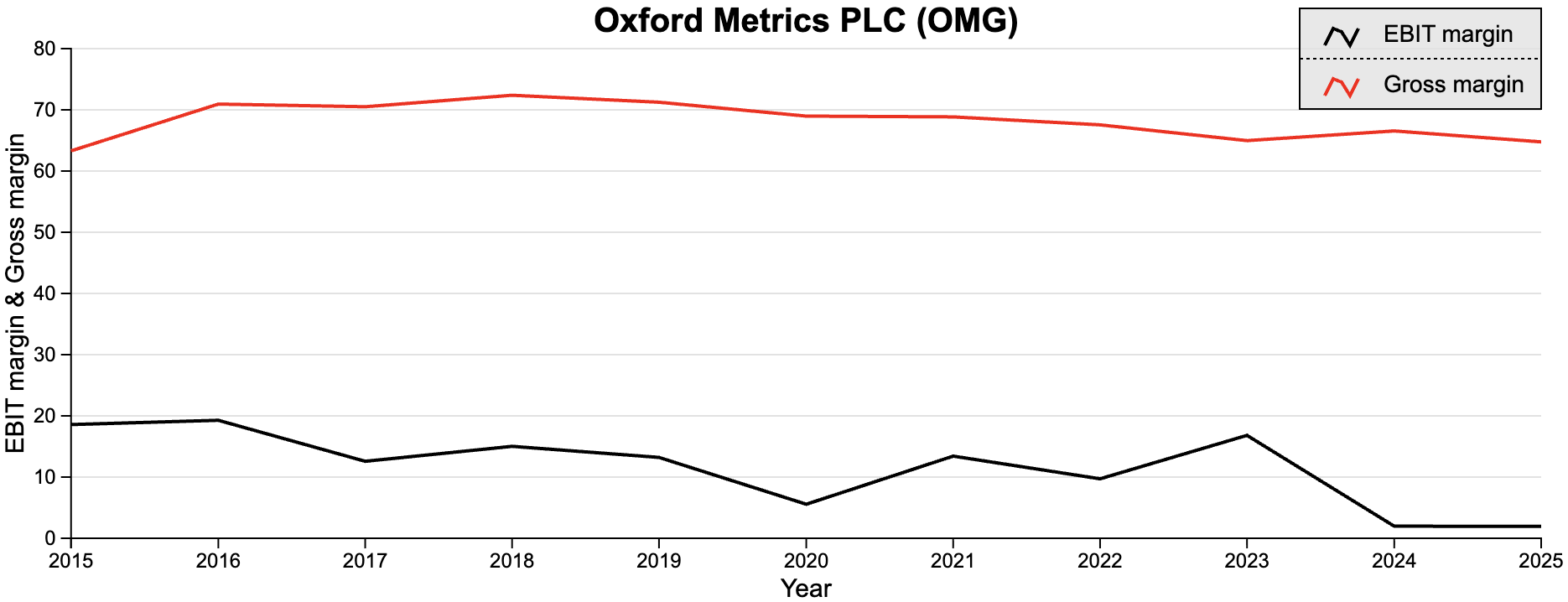

Oxford Metrics H1 Mar 2026 and Investor Update

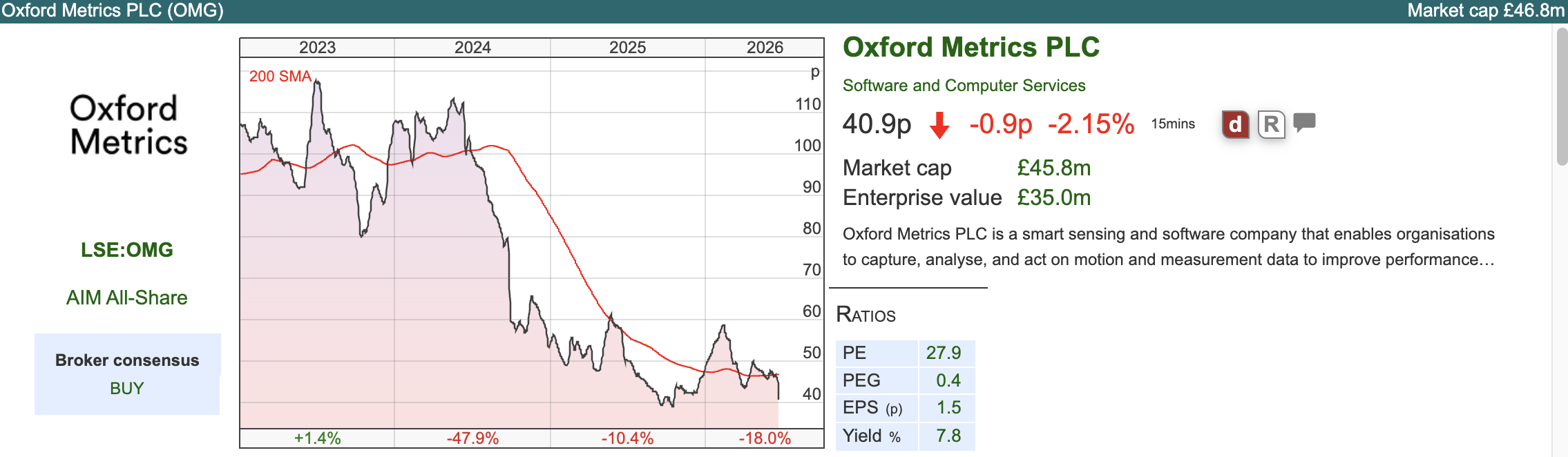

This loss making movement sensor and motion capture group was perceived to be at risk of disruption by AI technology. They sold a business (Yotta, for £52m) in 2022, and are still sitting on £32m of cash. Attractively priced opportunities were hard to find 4 years ago, but software groups have seen a significant de-rating, so they either need to spend the money to grow the business or return it to shareholders.

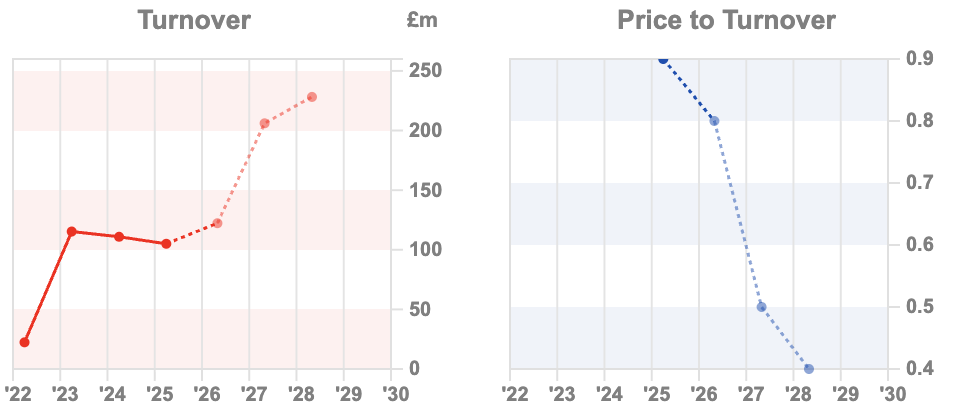

Unhelpfully management have decided to change their year end, from September to December. These results are H1 to March, showing revenue +3% to £21m and LBT reducing by -10% to £1m. One explanation for the change in year in could be that management are a country mile away from ambitious targets set out in their April 2024 Capital Markets Day. Management had a plan to increase FY Sept 2021 revenues by 2.5x to at a pre-tax margin of 15%, implying increasing from £27.5m to £70m revenues by the end of FY Sept 2026F. Annualising H1 revenue would imply £42m and Progressive, the research house, are forecasting £51m FY Dec 2027F.

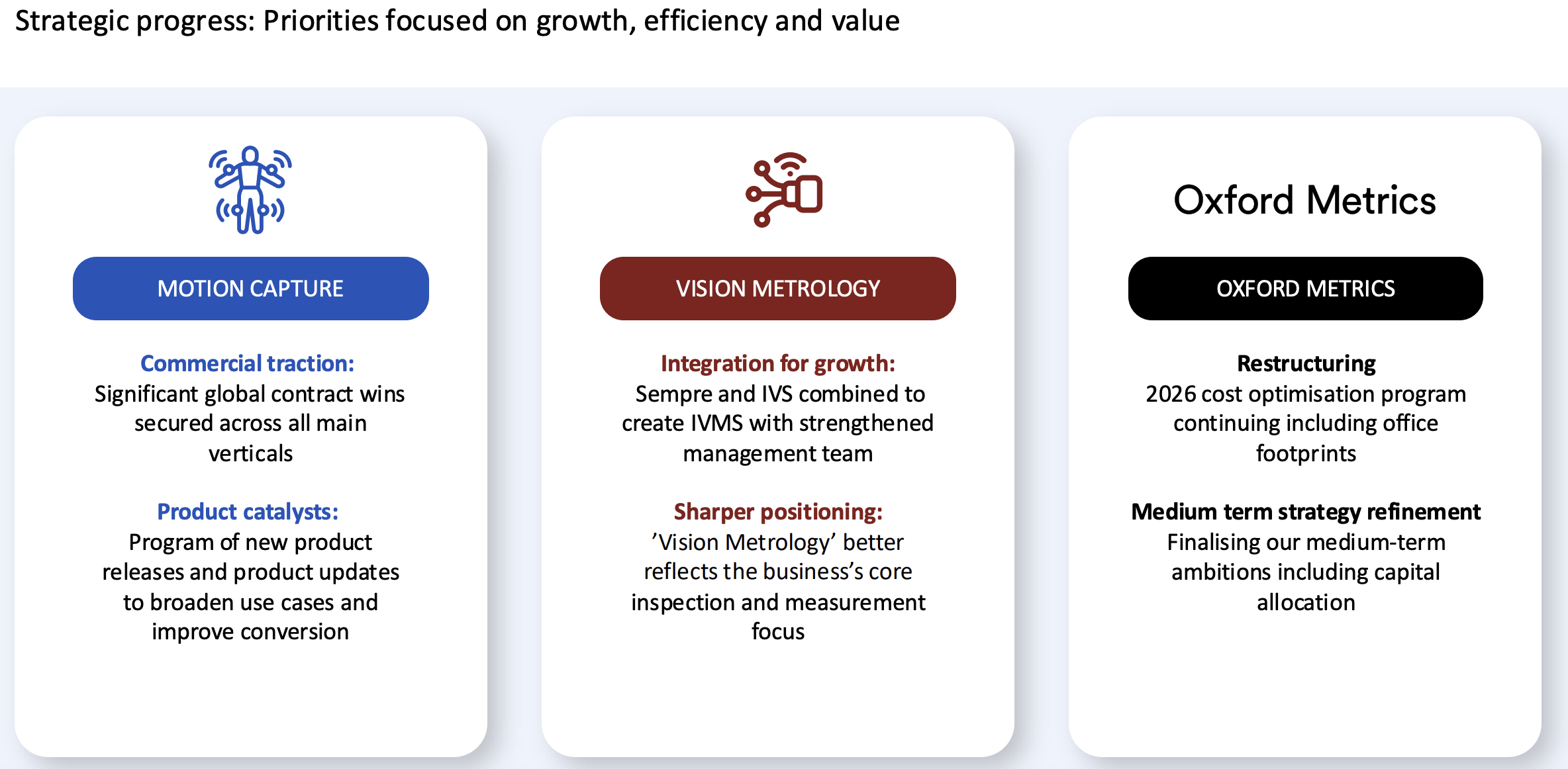

Last week they held another Capital Markets Day, this time the plan is to double revenue “in the medium term”, increase recurring revenue to 25% of group (currently 5%), increase the adj EBIT margin to mid teens (currently £0.2K loss). In the outlook statement management say they’re inline with FY expectations but flag an H2 weighting.

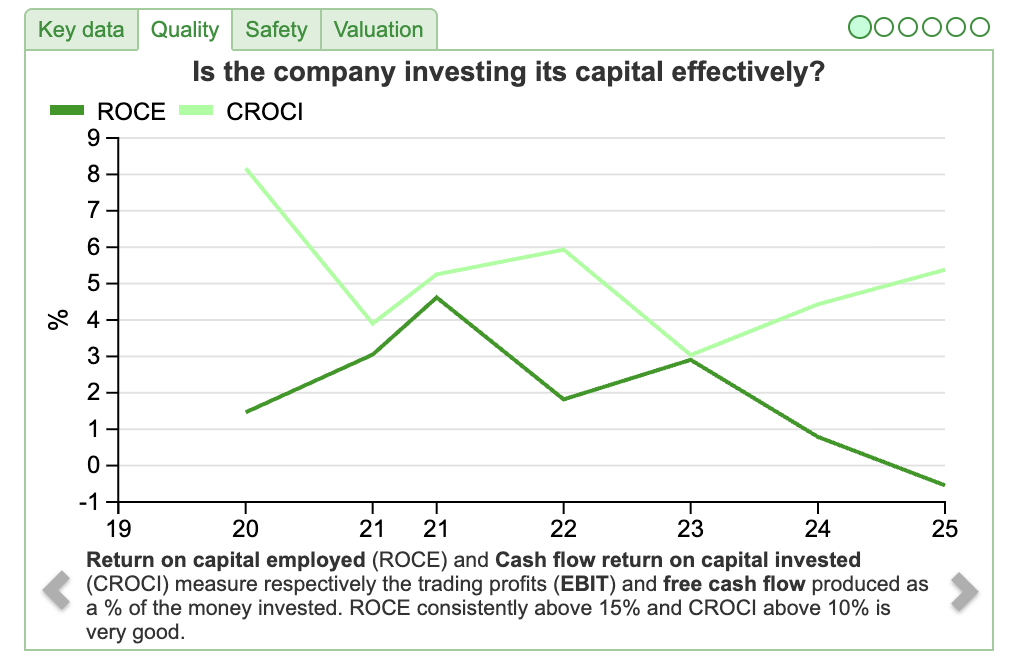

Valuation: The shares are trading on a PER of 14x Dec 2027F which doesn’t seem particularly attractive. On an EV/EBITDA basis they’re on below 3x, with the discrepancy explained by the fact that 70% of the market cap is cash. EV/Sales is 0.4x. Worth noting that ShareScope’s quality indicators suggest that this is a business which struggles to earn a decent return, which is surprising given that the gross margin is mid 60’s.

Opinion: I’ve held this for a few years, as there’s plenty of cash and expectations are low. I haven’t listened into the investor presentation yet, so I don’t know if they cover why they have disappointed and why we should give them the benefit of the doubt for their medium term targets now. I think I’ll wait to see if there are any signs of revenue growth, but if they disappoint again in H2 then I’ll cut my losses.

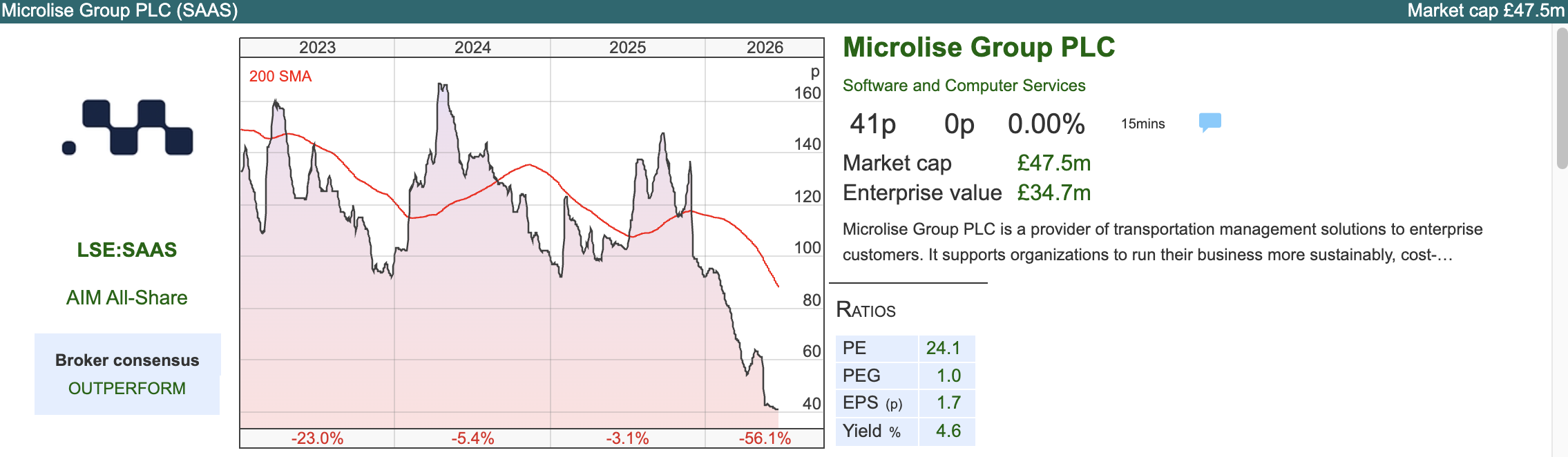

Microlise FY Dec Results

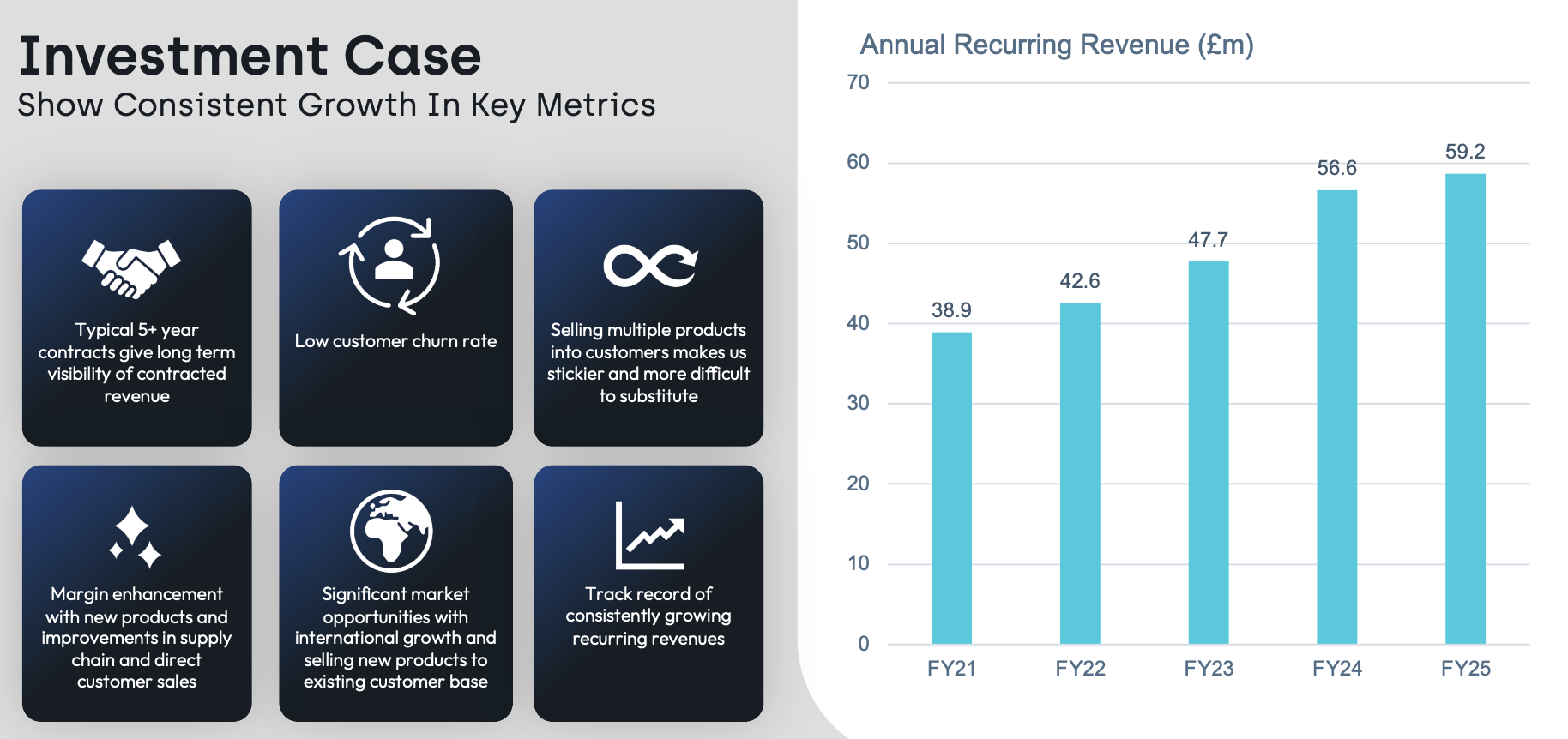

A contact at Mello suggested this 2021 IPO vintage, loss making logistics software group might be worth a second look. After several disappointments, including a cyber attack in 2024 and a profit warning in H2 last year it appears the “dumb money” institutional fund managers who backed the IPO are now exiting – perhaps presenting an opportunity for us “less dumb” amateur investors? The FY Dec results came out in May, just before Mello, but I’m looking at it now. The ticker is SAAS, and with the share price down -56% YTD, this has suffered its very own SaaS Apocalypse.

FY Dec results showed revenue +6% to £84m and LBT of £2.5m (versus £2.3m LBT 2024). There’s concentration risk, because one customer represents a quarter of revenue. The group has cash of £17m and an undrawn £10m revolving credit facility from HSBC. What has spooked investors (I think) is the consistent lack of profitability and that trade and other payables are £52m, of which £17m fall due in the next 12 months. Receivables, on the asset side of the balance sheet are £17m, so rather than bank borrowing, the working capital position looks challenging. There’s also £82m of intangible assets on the balance sheet, presumably at some risk of being written down, and net tangible equity is negative £14m.

It seems odd that a SaaS group would owe so much money to suppliers – in fact trade payables are just £3.5m. The bulk of payables is not trade suppliers, instead there are 2 other buckets that explain the £52m of trade and other payables : 1) Deferred revenue: Microlise has received cash upfront, but can’t recognise this as revenue until the service (software) has been delivered. Instead that payment sits as contract liabilities, which are 74% (£39m) of trade and other payables 2) There’s £8m of “other payables” in note 20 of the RNS. That’s not very helpful. I think that could be deferred consideration from previous acquisitions. In my view, companies ought to make the disclosure around this as helpful as possible, as these liabilities can cause serious problems (M&C Saatchi and SFOR Capital spring to mind).

The “going concern” statement says: “The Directors are satisfied that the Group has sufficient resources to respond to reasonably foreseeable scenarios and conclude that a scenario that would result in the need for the Group to require additional funding to be remote.”

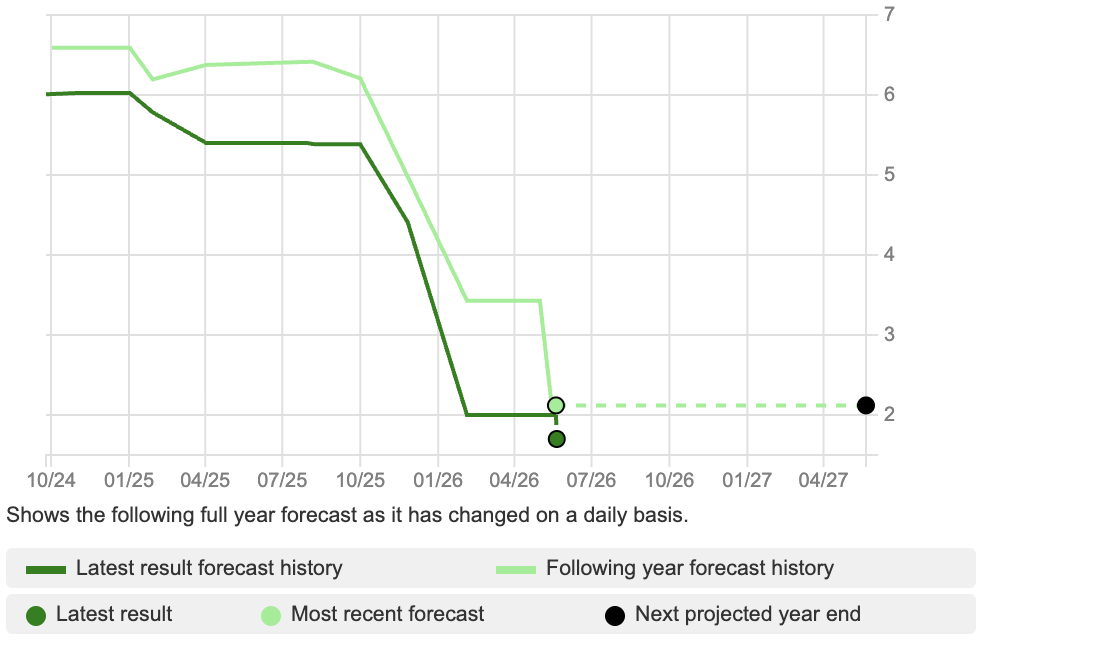

Outlook: The outlook statement says Q1 2026 was in line, but flag investment in the business, both cloud platform and sales headcount. For FY Dec 2026, management gave consensus revenue as £87m and adjusted EBITDA £11.2 million to £12.0 million, as at 13 May 2026 but suggested they would be bottom of the range. ShareScope shows analysts have responded by slashing EPS forecasts -61% reminding us that adj EBITDA guidance can be a nonsense.

Perhaps their financial PR should have a quiet word with management suggesting that now their market cap is now below £50m, SAAS are below the radar for many institutions. Instead they need to get retail investors onside; this “bottom of the range” adj EBITDA guidance but EPS forecasts down -61% is unlikely to do that.

Valuation: On a PER basis the shares look expensive on 19x Dec 2026F, dropping to 15x 2027F. However, like OMG covered above, they trade on an EV/Sales ratio of 0.4x, which is remarkably cheap for a software group with 64% gross margin, 70% recurring revenues. ShareScope shows strong FCF cash conversion of 270%, but the 3 year average ROCE below 2% is the problem. Revenue has grown by a third since FY Dec 2022, but that growth isn’t creating any value so management haven’t been able to demonstrate operational gearing.

Opinion: Nadeem Raza the Chief Exec owns just over 50% of the shares, so this would have been seen as a possible target for a take private bid a couple of years ago. That looks less likely following the SaaS Apocalypse, as Private Equity is becoming more cautious of cashflows from the enterprise software sector given the threat of disruption from AI Agents.

The SAAS investment case now looks to be the mirror opposite of legal services group Gateley (19% ROCE, but 25% FCF conv) which I wrote up a couple of weeks ago, SAAS has low profitability but excellent cash conversion. Both charts look like “falling knives”, but for completely different reasons. If management can turn this around, it could do very well, but we need to see evidence that the turnaround is starting to work. I can understand the institutional investors who have lost patience and decided to cut their losses.

Bruce Packard

Notes

Bruce owns shares in OMG

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Bi-Weekly Market Commentary | 24/06/2026 | OPT, OMG, SAAS | Surely we can fix this…

Bruce looks at OPT, the occupational health group, OMG the cash rich motion sensor company and logistics software group SAAS, which has suffered its own SaaS Apocalypse.

In the UK, Sir Keir Starmer started the week by resigning as Prime Minister. This was widely expected and had limited effects on financial markets. For instance, ShareScope shows UKTSY10 has fallen below 4.8% versus a peak of 5.15% in mid May.

Lynch thought that financial analysts who questioned Autonomy’s accounting were “corrupt”. Walking down Piccadilly he suggested one bear could be persuaded to change his “sell” recommendation, blurting out “I’ve got £100m in the bank. Surely we can fix this with a big bag of drugs and a bag of money and a prostitute?” His outburst reveals he never understood the motivation of analysts who questioned the story.

Speaking of boats, in an attempt to recreate the ShareScoping marketing, I have been writing this from my laptop on a boat. Readers will be pleased that I have not included any photos looking into the sunset with my shirt off though.

Optima Health FY Mar Trading Update

History: This came to market in Sept 2024, and the Admission Document suggests the Total Addressable Market in the UK should be around £1.4bn in 2028, underpinned by statutory demands placed on employers by the Health and Safety at Work Act. Optima has around 10% market share, but is the largest provider approximately 1.8x bigger than the second largest provider by revenue. According to Cavendish, there’s a long term ambition to achieve 25% market share (ie over £350m of revenue). The group has medium term targets of: greater than £200m revenue, greater than £40m EBITDA and 20% EBITDA margin.

Oxford Metrics H1 Mar 2026 and Investor Update

This loss making movement sensor and motion capture group was perceived to be at risk of disruption by AI technology. They sold a business (Yotta, for £52m) in 2022, and are still sitting on £32m of cash. Attractively priced opportunities were hard to find 4 years ago, but software groups have seen a significant de-rating, so they either need to spend the money to grow the business or return it to shareholders.

Unhelpfully management have decided to change their year end, from September to December. These results are H1 to March, showing revenue +3% to £21m and LBT reducing by -10% to £1m. One explanation for the change in year in could be that management are a country mile away from ambitious targets set out in their April 2024 Capital Markets Day. Management had a plan to increase FY Sept 2021 revenues by 2.5x to at a pre-tax margin of 15%, implying increasing from £27.5m to £70m revenues by the end of FY Sept 2026F. Annualising H1 revenue would imply £42m and Progressive, the research house, are forecasting £51m FY Dec 2027F.

Last week they held another Capital Markets Day, this time the plan is to double revenue “in the medium term”, increase recurring revenue to 25% of group (currently 5%), increase the adj EBIT margin to mid teens (currently £0.2K loss). In the outlook statement management say they’re inline with FY expectations but flag an H2 weighting.

Valuation: The shares are trading on a PER of 14x Dec 2027F which doesn’t seem particularly attractive. On an EV/EBITDA basis they’re on below 3x, with the discrepancy explained by the fact that 70% of the market cap is cash. EV/Sales is 0.4x. Worth noting that ShareScope’s quality indicators suggest that this is a business which struggles to earn a decent return, which is surprising given that the gross margin is mid 60’s.

Opinion: I’ve held this for a few years, as there’s plenty of cash and expectations are low. I haven’t listened into the investor presentation yet, so I don’t know if they cover why they have disappointed and why we should give them the benefit of the doubt for their medium term targets now. I think I’ll wait to see if there are any signs of revenue growth, but if they disappoint again in H2 then I’ll cut my losses.

Microlise FY Dec Results

A contact at Mello suggested this 2021 IPO vintage, loss making logistics software group might be worth a second look. After several disappointments, including a cyber attack in 2024 and a profit warning in H2 last year it appears the “dumb money” institutional fund managers who backed the IPO are now exiting – perhaps presenting an opportunity for us “less dumb” amateur investors? The FY Dec results came out in May, just before Mello, but I’m looking at it now. The ticker is SAAS, and with the share price down -56% YTD, this has suffered its very own SaaS Apocalypse.

FY Dec results showed revenue +6% to £84m and LBT of £2.5m (versus £2.3m LBT 2024). There’s concentration risk, because one customer represents a quarter of revenue. The group has cash of £17m and an undrawn £10m revolving credit facility from HSBC. What has spooked investors (I think) is the consistent lack of profitability and that trade and other payables are £52m, of which £17m fall due in the next 12 months. Receivables, on the asset side of the balance sheet are £17m, so rather than bank borrowing, the working capital position looks challenging. There’s also £82m of intangible assets on the balance sheet, presumably at some risk of being written down, and net tangible equity is negative £14m.

It seems odd that a SaaS group would owe so much money to suppliers – in fact trade payables are just £3.5m. The bulk of payables is not trade suppliers, instead there are 2 other buckets that explain the £52m of trade and other payables : 1) Deferred revenue: Microlise has received cash upfront, but can’t recognise this as revenue until the service (software) has been delivered. Instead that payment sits as contract liabilities, which are 74% (£39m) of trade and other payables 2) There’s £8m of “other payables” in note 20 of the RNS. That’s not very helpful. I think that could be deferred consideration from previous acquisitions. In my view, companies ought to make the disclosure around this as helpful as possible, as these liabilities can cause serious problems (M&C Saatchi and SFOR Capital spring to mind).

The “going concern” statement says: “The Directors are satisfied that the Group has sufficient resources to respond to reasonably foreseeable scenarios and conclude that a scenario that would result in the need for the Group to require additional funding to be remote.”

Outlook: The outlook statement says Q1 2026 was in line, but flag investment in the business, both cloud platform and sales headcount. For FY Dec 2026, management gave consensus revenue as £87m and adjusted EBITDA £11.2 million to £12.0 million, as at 13 May 2026 but suggested they would be bottom of the range. ShareScope shows analysts have responded by slashing EPS forecasts -61% reminding us that adj EBITDA guidance can be a nonsense.

Perhaps their financial PR should have a quiet word with management suggesting that now their market cap is now below £50m, SAAS are below the radar for many institutions. Instead they need to get retail investors onside; this “bottom of the range” adj EBITDA guidance but EPS forecasts down -61% is unlikely to do that.

Valuation: On a PER basis the shares look expensive on 19x Dec 2026F, dropping to 15x 2027F. However, like OMG covered above, they trade on an EV/Sales ratio of 0.4x, which is remarkably cheap for a software group with 64% gross margin, 70% recurring revenues. ShareScope shows strong FCF cash conversion of 270%, but the 3 year average ROCE below 2% is the problem. Revenue has grown by a third since FY Dec 2022, but that growth isn’t creating any value so management haven’t been able to demonstrate operational gearing.

Opinion: Nadeem Raza the Chief Exec owns just over 50% of the shares, so this would have been seen as a possible target for a take private bid a couple of years ago. That looks less likely following the SaaS Apocalypse, as Private Equity is becoming more cautious of cashflows from the enterprise software sector given the threat of disruption from AI Agents.

The SAAS investment case now looks to be the mirror opposite of legal services group Gateley (19% ROCE, but 25% FCF conv) which I wrote up a couple of weeks ago, SAAS has low profitability but excellent cash conversion. Both charts look like “falling knives”, but for completely different reasons. If management can turn this around, it could do very well, but we need to see evidence that the turnaround is starting to work. I can understand the institutional investors who have lost patience and decided to cut their losses.

Bruce Packard

Notes

Bruce owns shares in OMG

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.