Alpesh Patel applies his quality and momentum filters to 54 stocks recently upgraded by major investment banks. He highlights the themes driving analyst conviction and identifies where opportunities and risks may be emerging across global markets.

Full stock-by-stock analysis available exclusively to Alpesh Patel Special Edition subscribers.

THE METHOD — WHY THIS LIST EXISTS

Every month I aggregate stocks that have received recent buy upgrades from the major investment banks — UBS, Barclays, Citi, Goldman Sachs, JP Morgan, Morgan Stanley, Bank of America — and run them through my own screen. The result is a curated list of names where institutional analyst conviction and my own quality and momentum filters overlap.

Bank upgrades are a useful starting point, not a finishing line. Buy ratings outnumber sells at every major institution by roughly four to one. Conflicts of interest exist. Banks frequently upgrade stocks after they have already moved 50–80%. My job is to separate the names where the bank conviction is real and the chart confirms it from the ones where analysts are arriving late to a party that is nearly over.

This month’s list covers 54 stocks across ten sectors. The macro backdrop is the second leg of the AI infrastructure build-out, a healthcare insurer partial recovery, energy services and offshore revival, and a consumer market that is splitting sharply between premium and mid-market. Several of the names in the screen are genuinely compelling. Several others carry flags that the fair value discount alone does not capture. Knowing which is which is what the full analysis provides.

| Bank upgrades narrow the universe. The MACD tells you whether momentum is behind the thesis right now. Use both — neither alone is sufficient. |

June 2026 — WHAT IS DRIVING THE UPGRADE LIST

Five macro forces are cutting across virtually every name on this list. Understanding them first prevents you from reading individual stock situations in isolation.

- AI infrastructure — second leg: The first wave was hyperscalers buying GPUs. The second is everything that makes those GPUs work — power, cooling, storage, networking, testing, grid infrastructure. Semiconductor, test equipment, storage, and energy-services names on this list are all catching this tailwind. Several have already moved 50–90% on it.

- Healthcare insurer reset: Managed care stocks collapsed in 2025 on Medicaid and Medicare Advantage policy fears. They have partially recovered. Banks are leaning back in on valuation. The open question is whether the policy environment has actually stabilised or whether this is a relief rally that still has policy risk ahead of it.

- Energy services and offshore revival: Offshore dayrates remain structurally elevated. Permian frac activity is recovering. Banks are buying the services and drilling names broadly. These are high-cycle, high-beta stocks — the kind that fall 60% when the cycle turns. Sizing discipline is the only risk management that works in this group.

- Rate normalisation and financial services: Banks are appearing on bank-analyst buy lists as the rate curve steepens and deal and IPO volumes recover from 2024-25 lows. The commercial real estate overhang and the next consumer credit cycle are the risks that have not yet been tested.

- Consumer bifurcation: Premium brands are performing. Mid-market names are under pressure. The retail and consumer picks on this list reflect specific brand-momentum and turnaround stories, not a broad consumer recovery bet.

WHAT IS ON THE LIST — SECTOR BY SECTOR

Below I give you the flavour of what each sector contains. The full stock-by-stock analysis — with exact MACD readings, bank coverage detail, bull and bear case, and my verdict — is available to Special Edition subscribers.

Healthcare, Insurers & Biotech — 6 Names

| Managed care has partially recovered from its 2025 collapse. Banks are buying the bounce. Three biotech names are genuine opportunities — but binary, news-driven, and not suitable as core holdings. |

|

The two managed care names on the list have experienced very different recoveries. One is the highest-concentration Medicaid managed care operator in the US — it trades roughly 70% below estimated fair value with the MACD turning from deeply oversold territory. The other is a Blue Cross Blue Shield licensee across 14 states: higher quality, lower beta, and a cleaner balance sheet. Banks are backing both with multiple buy ratings.

The biotech names range from a genuine clinical breakout story with a broad analyst buy consensus — the kind of setup where the chart and the fundamental story are aligned — to a value trap risk where a structural business decline is being obscured by a misleading discount to fair value.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Healthcare — Full Analysis — Which managed care name has the cleaner fundamental setup — The biotech with the broadest bank buy consensus and why the chart confirms it — The one biotech that looks cheap but isn’t — and why the bears are right — Exact MACD readings, bank coverage, bull/bear cases, and 12-month verdicts Upgrade at sharescope.co.uk/alpeshpatel |

Semiconductors & Test Equipment — 9 Names

| The AI capex cycle is inflating expectations and multiples across the whole sector. Banks are net-positive. Several names have made 50–90% moves. The single most important rule: add on pullbacks, never chase a vertical chart. |

|

Nine semiconductor and test equipment names appear this month. They span the full risk spectrum: from a near-unanimously covered AI infrastructure play with a genuine structural demand tailwind, to a speculative foundry turnaround where the bank coverage is dominated by holds rather than buys, to analogue names whose Apple concentration means the investment thesis is effectively a single customer relationship.

The test equipment name in particular stands out — every AI chip designed anywhere in the world has to be tested before it ships, and this company is the dominant provider of that testing infrastructure. The bank consensus is six buys and no dissent. The chart has moved 94%. The question, as with everything that has already moved this far, is whether you add on the current chart or wait for the next pullback.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Semiconductors — Full Analysis — The pick-and-shovel AI play with 6 buy ratings and no dissent — The near-unanimous AMD thesis — and the one specific risk that could derail it — Which analogue names are mean-reversion trades vs structural plays — The Intel turnaround — what the holds-dominated bank coverage is telling you — Exact MACD, analyst targets, and position-size guidance for each name Upgrade at sharescope.co.uk/alpeshpatel |

Oil, Gas & Pipelines — 7 Names

| Banks are warm on energy majors and integrateds. A natural gas midstream operator has reached all-time highs on the AI data centre electricity narrative. Several E&P names offer WTI beta at steep discounts to fair value. |

|

The natural gas infrastructure name has become a consensus trade — banks are unanimously positive, the chart is at all-time highs, and the AI data centre electricity story is now widely understood. That consensus cuts both ways. When a thesis becomes universally accepted, the chart is usually already pricing it. The discipline here is to buy pullbacks, not to chase the current level.

Further down the risk spectrum, two E&P names offer materially different risk profiles. One has an excellent balance sheet and genuine earnings growth at 60% below estimated fair value — a clean oil-bull thesis. The other is a smaller refiner with a 64% chart breakout, strong bank backing, and earnings that are forecast to decline for three consecutive years from here.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Oil, Gas & Pipelines — Full Analysis — The midstream name at all-time highs — why ‘buy pullbacks’ matters now more than ever — The cleanest E&P setup on the list and what could derail it — The refiner whose three-year earnings decline forecast contradicts the upgrade thesis — BP and Petrobras: where each sits on the value/risk spectrum for UK investors — Full MACD, analyst coverage, and 12-month scenarios Upgrade at sharescope.co.uk/alpeshpatel |

Energy Services & Offshore Drilling — 8 Names

| The highest-beta way to play sustained energy capex. Banks are broadly buying. Drawdowns of 40–60% from peak to trough are normal in this group. Position sizing is the entire discipline. |

|

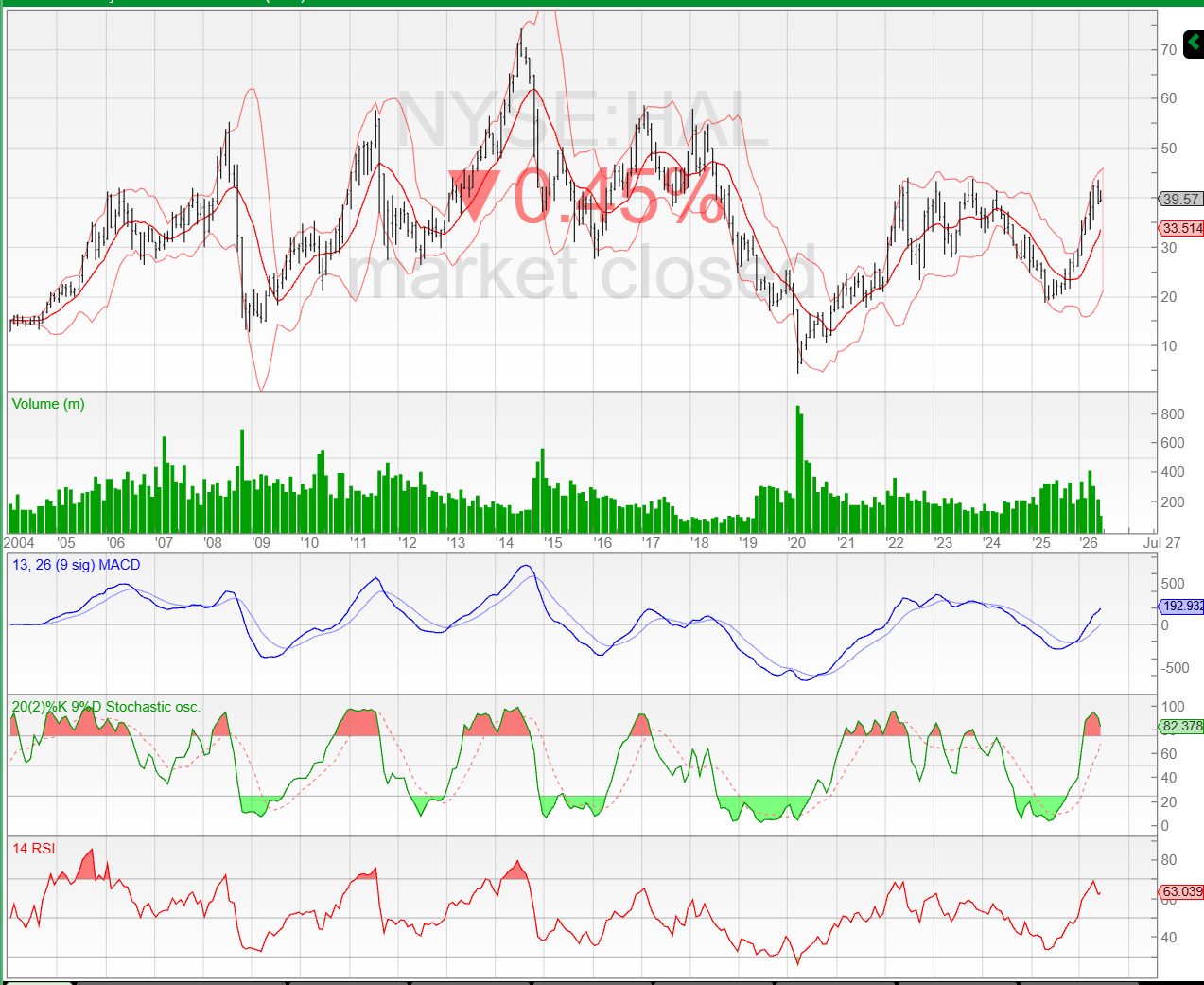

Eight energy services and offshore drilling names appear this month — ranging from the quality oilfield services business with broad bank consensus and a clean balance sheet, to the highest-beta deepwater driller with a history of bankruptcy restructuring and boom-bust cycles of 70%+ in both directions. Banks are buying the whole group. The underlying logic is sound: if oil prices stay elevated, services companies generate exceptional returns. The risk is always the same: cycle turns are sudden and severe.

One name in particular carries a warning that does not appear in the bank upgrade notes. Two major investment banks — both with strong resources sector research teams — carry sell ratings on it simultaneously. When that happens, a 43% chart breakout and a 93% discount to fair value are not enough to override the signal.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Energy Services & Offshore — Full Analysis — The quality services name with broad bank consensus — and the right way to build a position — Offshore drilling: which names have the most defensible balance sheets — The name with two simultaneous sell ratings from major banks — what they know — Position sizing framework for high-cycle energy services exposure — Full MACD, bank coverage, and cycle risk assessment for all 8 names Upgrade at sharescope.co.uk/alpeshpatel |

Banks & Financial Services — 2 Names

| Rate-curve normalisation plus IB recovery plus benign credit is the thesis. The unknown is commercial real estate exposure and the next consumer credit cycle. |

Two financial services names on this month’s list. One is a wealth management and investment banking franchise at all-time highs with a P/E below the broad US market — an unusual combination. The other is executing one of the most strategically significant acquisitions in financial services in years, creating a vertically integrated payments business that eliminates its dependency on the major card networks. Eight analyst buy ratings and no dissents from major institutions. The execution risk and the credit cycle are the variables that matter.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Banks & Financial Services — Full Analysis — Which name to buy on a pullback and which to add to now — The Discover acquisition logic — why the strategic case is compelling — The consumer credit cycle risk that the fair value models are not capturing — Full MACD, analyst targets, and 12-month verdict Upgrade at sharescope.co.uk/alpeshpatel |

Industrials, Aerospace & Specialty — 4 Names

| Idiosyncratic stories with generally defensive cash flows. Quality varies significantly across the four names. |

The standout in this group is an aerospace engine aftermarket services business — a recent addition to the public markets with strong structural characteristics: once an airline certifies a maintenance provider for a specific engine type, switching is expensive and time-consuming. 316% earnings growth last year, 17.77% forecast growth, and five buy ratings from banks covering it. At 28.8% below estimated fair value, the numbers are attractive.

A second name is one of the most consistent compounders in the environmental services sector — 13 years of compound growth with genuine barriers to entry in hazardous waste disposal. The hold ratings from several major banks likely reflect limited near-term catalyst rather than fundamental concern.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Industrials & Aerospace — Full Analysis — The aerospace aftermarket business — why switching costs make this structurally defensible — The environmental compounder with 13 years of track record — Which industrial names have quality-of-earnings questions that need addressing — Full MACD, bank coverage, and 12-month verdicts for all four names Upgrade at sharescope.co.uk/alpeshpatel |

Software & Communications Platforms — 2 Names

Two software names this month — one that turned profitable in 2025 after years of burning cash on growth, and one recovering from a significant security breach that damaged customer trust. The profitable one has seven buy ratings and a 55% chart breakout. The recovery story requires more conviction in the competitive position before treating it as more than a tactical position.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Software — Full Analysis — The CPaaS platform that became profitable — full thesis and risks — The identity management recovery — what the breach history means for competitive position — Exact MACD readings and what to watch for confirmation Upgrade at sharescope.co.uk/alpeshpatel |

Retail & Consumer Brands — 5 Names

| Consumer is bifurcated. Banks are picking specific brand-momentum and quality stories. The mid-market names face real structural pressure. |

|

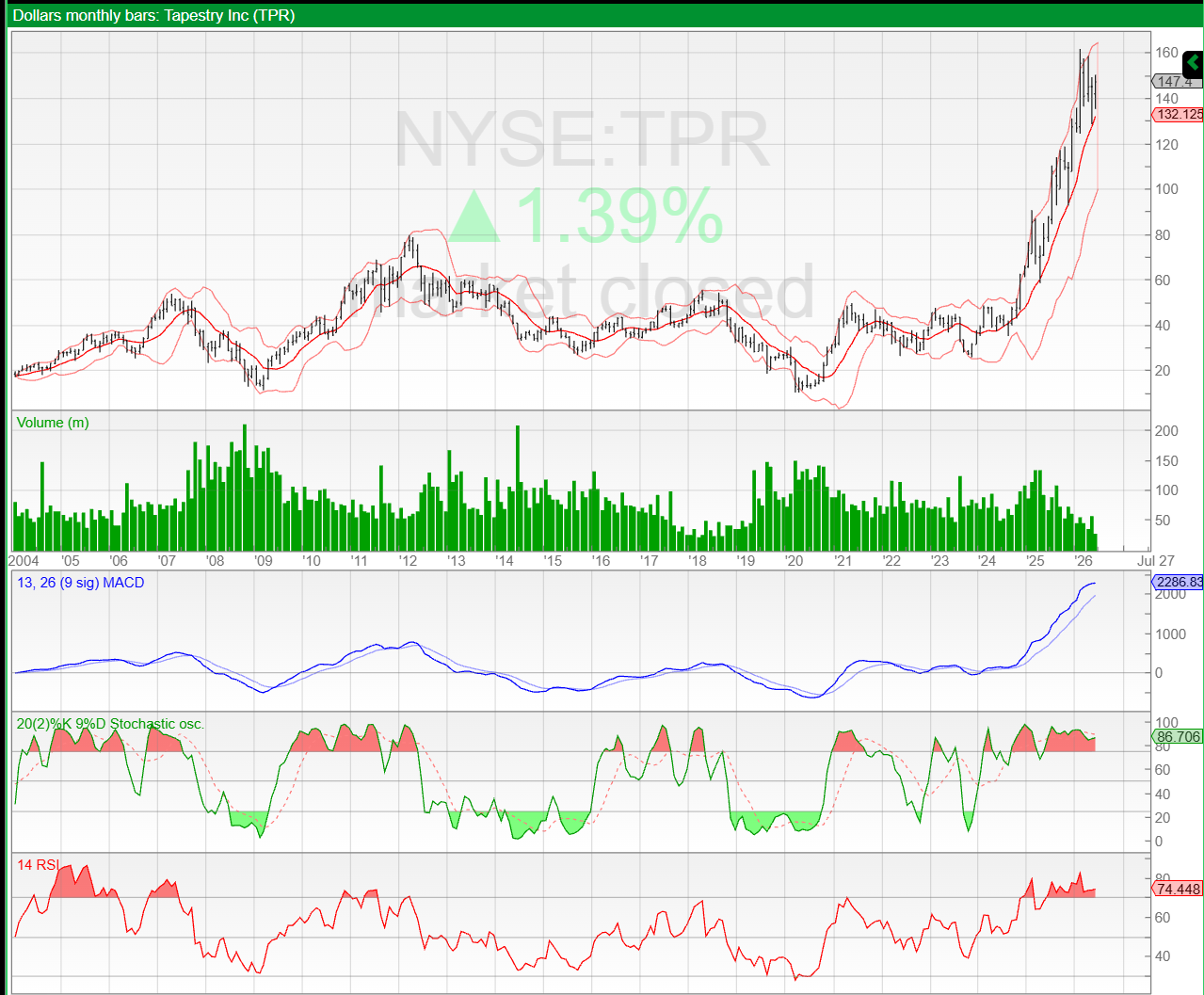

Five consumer names span from an accessible-luxury brand with genuine momentum and six analyst buys to a home improvement retailer with a reliable dividend and quality balance sheet. The luxury brand’s profit margin compression from 12.5% to 8.4% is the number to watch most closely — the full thesis requires that to reverse. The home goods omni-channel retailer is the lowest-risk consumer pick on the list: modest growth, flawless balance sheet, established dividend.

One automotive name appears on the list with a buy from one bank and a sell from another. That kind of split conviction, combined with the specific risk profile of this business in the current environment, makes it one of the names I address explicitly in the full analysis.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Retail & Consumer — Full Analysis — The accessible-luxury brand — why the margin trend is the key metric to watch — Which consumer names are quality compounders vs turnaround plays — The automotive name with a Sell rating from Wells Fargo — what that reflects — Full MACD, analyst coverage, and 12-month verdicts for all five names Upgrade at sharescope.co.uk/alpeshpatel |

Media & Entertainment — 5 Names

Five media names. Two that are straightforward quality holds. One that appears cheap but has two sell ratings from major banks that the fair value model is not capturing. One live sports franchise with genuine platform characteristics. One Chinese streaming platform with a flawless balance sheet but an ADR overhang that creates specific risks for non-US investors.

The standout avoid on this list received two sell ratings from Wells Fargo and Bank of America. A 70% discount to estimated fair value does not override sell ratings from two major institutions when the business is a newly merged entity with integration risk and debt not covered by operating cash flow. Full details in the subscriber analysis.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Media & Entertainment — Full Analysis — Netflix — why it is a core hold not a momentum trade — The live sports franchise and why live content is structurally different to streaming — The post-merger media name with two sell ratings — full red flag analysis — Bilibili: the China ADR risk profile for UK-based investors — Full MACD and 12-month verdicts for all five names Upgrade at sharescope.co.uk/alpeshpatel |

Latin American Opportunities — 3 Names

Three names with Latin American exposure. One is a genuinely unusual airline business — the Panama hub operator that connects intra-Latin American routes with near-monopoly characteristics, clean balance sheet, and seven unanimous analyst buy ratings. The second is a Mexican airport concessionaire with quality infrastructure economics and US-Mexico political risk that requires a view on the bilateral relationship. The third is a declining-earnings telecom with a sell rating — not recommended without a specific conviction in the macro thesis.

| 🔒 ALPESH PATEL SPECIAL EDITION SUBSCRIBERS ONLY

Latin America — Full Analysis — The Latin American airline with 7 unanimous buy ratings — and why the hub model is defensible — Mexican airports: quality infrastructure business vs political risk — Why the telecom name should be avoided at current positioning — Full MACD, analyst targets, and currency risk assessment for UK investors Upgrade at sharescope.co.uk/alpeshpatel |

ALL 54 NAMES — DIRECTION AT A GLANCE

Below is the complete list with directional signals. Ticker, sector, and momentum direction are shown. The full write-up on every name — bull case, bear case, exact MACD readings, analyst coverage, and 12-month verdict — is available to Special Edition subscribers.

| # | Company | Sector | Direction | Detail |

| CNC | Centene | Healthcare | Recovering ↗ | Full analysis: APSE only 🔒 |

| ELV | Elevance Health | Healthcare | Bullish ✓ | Full analysis: APSE only 🔒 |

| INSM | Insmed | Biotech | Breakout ▲ | Full analysis: APSE only 🔒 |

| BIIB | Biogen | Biotech | Turning → | Full analysis: APSE only 🔒 |

| ARWR | Arrowhead Pharma | Biotech | Breakout ▲ | Full analysis: APSE only 🔒 |

| CLDX | Celldex Therapeutics | Biotech | Watch only | Full analysis: APSE only 🔒 |

| AMD | Adv. Micro Devices | Semiconductors | Breakout ▲ | Full analysis: APSE only 🔒 |

| MRVL | Marvell Technology | Semiconductors | Breakout ▲ | Full analysis: APSE only 🔒 |

| TXN | Texas Instruments | Semiconductors | Breaking out → | Full analysis: APSE only 🔒 |

| ON | ON Semiconductor | Semiconductors | Recovering ↗ | Full analysis: APSE only 🔒 |

| SITM | SiTime Corp | Semiconductors | Strong ▲ | Full analysis: APSE only 🔒 |

| TER | Teradyne | Test Equipment | Strong ▲ | Full analysis: APSE only 🔒 |

| SWKS | Skyworks | Semiconductors | Bouncing → | Full analysis: APSE only 🔒 |

| QRVO | Qorvo | Semiconductors | Bounce only | Full analysis: APSE only 🔒 |

| INTC | Intel | Semiconductors | Breakout ▲ | Full analysis: APSE only 🔒 |

| STNG | Scorpio Tankers | Energy / Tankers | Breakout ▲ | Full analysis: APSE only 🔒 |

| PBR | Petrobras | Energy / EM | Watch → | Full analysis: APSE only 🔒 |

| BP | BP plc | Energy / Integrated | Recovering ↗ | Full analysis: APSE only 🔒 |

| PSX | Phillips 66 | Energy / Refining | Strong ▲ | Full analysis: APSE only 🔒 |

| PARR | Par Pacific | Energy / Refining | Breakout ▲ | Full analysis: APSE only 🔒 |

| CHRD | Chord Energy | Energy / E&P | Bullish ✓ | Full analysis: APSE only 🔒 |

| WMB | Williams Companies | Energy / Midstream | All-time high ▲ | Full analysis: APSE only 🔒 |

| HAL | Halliburton | Energy Services | Bullish ✓ | Full analysis: APSE only 🔒 |

| PTEN | Patterson-UTI | Energy Services | Breakout ▲ | Full analysis: APSE only 🔒 |

| PUMP | ProPetro | Energy Services | Breakout ▲ | Full analysis: APSE only 🔒 |

| SDRL | Seadrill | Offshore Drilling | Recovering ↗ | Full analysis: APSE only 🔒 |

| NE | Noble Corp | Offshore Drilling | Breakout ▲ | Full analysis: APSE only 🔒 |

| RIG | Transocean | Offshore Drilling | Breakout ▲ | Full analysis: APSE only 🔒 |

| AESI | Atlas Energy | Energy / Proppants | Mixed ⚠ | Full analysis: APSE only 🔒 |

| WBI | WaterBridge Infra | Energy / Midstream | New story → | Full analysis: APSE only 🔒 |

| MS | Morgan Stanley | Banks / Finance | All-time high ▲ | Full analysis: APSE only 🔒 |

| COF | Capital One | Banks / Finance | Recovering ↗ | Full analysis: APSE only 🔒 |

| SARO | StandardAero | Aerospace / Indus. | Bullish ✓ | Full analysis: APSE only 🔒 |

| CLH | Clean Harbors | Industrials | Bullish ✓ | Full analysis: APSE only 🔒 |

| CWST | Casella Waste | Industrials | Rolling over ▼ | Full analysis: APSE only 🔒 |

| ADNT | Adient plc | Auto / Industrials | Recovering ↗ | Full analysis: APSE only 🔒 |

| TWLO | Twilio | Software | Breakout ▲ | Full analysis: APSE only 🔒 |

| OKTA | Okta | Software | Recovering → | Full analysis: APSE only 🔒 |

| VSCO | Victoria’s Secret | Retail / Consumer | Watch → | Full analysis: APSE only 🔒 |

| LOW | Lowe’s Companies | Retail / Consumer | Bullish ✓ | Full analysis: APSE only 🔒 |

| WSM | Williams-Sonoma | Retail / Consumer | Bullish ✓ | Full analysis: APSE only 🔒 |

| TPR | Tapestry / Coach | Retail / Consumer | Bullish ✓ | Full analysis: APSE only 🔒 |

| F | Ford Motor | Automotive | Mixed ⚠ | Full analysis: APSE only 🔒 |

| NFLX | Netflix | Media / Streaming | Near fair value → | Full analysis: APSE only 🔒 |

| NXST | Nexstar Media | Media / TV | Caution ▼ | Full analysis: APSE only 🔒 |

| PSKY | Paramount Skydance | Media / Entmt | Avoid ⚠ | Full analysis: APSE only 🔒 |

| TKO | TKO Group | Media / Sports | Bullish ✓ | Full analysis: APSE only 🔒 |

| BILI | Bilibili | Media / China | Recovering ↗ | Full analysis: APSE only 🔒 |

| CPA | Copa Holdings | Airlines / LatAm | Bullish ✓ | Full analysis: APSE only 🔒 |

| OMAB | Grupo OMAB | Airports / Mexico | Bullish → | Full analysis: APSE only 🔒 |

| TEO | Telecom Argentina | Telecom / LatAm | Declining ▼ | Full analysis: APSE only 🔒 |

| RHP | Ryman Hospitality | REIT / Hospitality | Bullish ✓ | Full analysis: APSE only 🔒 |

| SWX | Southwest Gas | Utilities | Steady → | Full analysis: APSE only 🔒 |

| STX | Seagate Technology | Storage / AI | Parabolic ▲ | Full analysis: APSE only 🔒 |

| RELX | RELX plc | Info Analytics | Bullish ✓ | Full analysis: APSE only 🔒 |

HOW TO USE SHARESCOPE ON THIS LIST

You do not need the full analysis to start working with this universe in ShareScope. Here is a simple starting workflow:

- Search each ticker and pull up the weekly chart before reading anything else about the stock — let the chart tell you the first story

- Add MACD (12,26,9): MACD above signal and rising from below zero is the confirmation signal. MACD below signal with both lines negative means wait, regardless of how cheap the stock looks

- Check the direction column in the table above — names marked Avoid ⚠ or Declining ▼ have explicit warnings in the full analysis that go beyond the chart. Double check and analyse for yourself always. Markets move fast and things can have moved significantly even by the time I finish writing this sentence.

- For any stock showing a 70–90% chart move, ask yourself: am I buying the business or buying the momentum? The answer changes what MACD level and position size are appropriate

- Use the APSE Value/Growth filter for the quality check — ROCE, earnings growth, and cash conversion are your anchors. If a stock passes the chart test but fails the quality filter, treat it as a trade not an investment

| The names on this list range from quality compounders at genuine discounts to speculative cycle plays that will fall 60% when conditions change. The full analysis tells you which is which. The MACD and quality filter in ShareScope are your tools for staying on the right side of that distinction. |

| Want the Full Analysis on All 54 Stocks?

Alpesh Patel Special Edition subscribers get the complete write-up on every name — exact MACD readings, bank coverage detail, bull and bear case, risk flags, and a 12-month verdict. Plus APSE filter layouts pre-loaded in ShareScope so you can run the screen yourself. sharescope.co.uk/alpeshpatel |

Alpesh Patel OBE | @alpeshbp | www.alpeshpatel.com/sharescope

www.campaignforamillion.com | www.alpeshpatel.com/shares

This article is for informational and educational purposes only. It does not constitute personalised investment guidance, a financial promotion, or a recommendation to buy or sell any security. Bank analyst ratings reflect views at the time of publication and are subject to change. The value of investments can fall as well as rise and you may receive back less than you invest. Always conduct your own due diligence. Alpesh Patel OBE provides mentoring and education, not regulated financial advice.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

And of course feel free to email me any questions you have at all in case I miss any comments.