Ramin Nakisa of PensionCraft explains how he uses ShareScope to screen for ETFs and funds, focusing on cost, global exposure and practical usability. He walks through three screening setups that help users research and compare funds using criteria such as cost, exposure and fund size for both long-term portfolios and tactical ideas.

I’ve been using ShareScope, on and off, since the days of dial-up-modems. Since I started PensionCraft in 2017 I’ve been using it almost daily. Now my business is very much focussed on low-cost index investing. That means that I have to find index funds that give exposure to all the major asset classes, countries, styles and sectors. I simply couldn’t have done that job without ShareScope. So in this article, I’ll go through how I use ShareScope to help me find what I need and what my community needs.

I separate my “core” portfolio, which makes up 90% of my investments, from my “fun” portfolio which makes up the remaining 10%. My core is simple, has just two funds in it and is hardly ever changed. The fun portfolio is, as its name suggests, where I behave badly and where, despite all evidence to the contrary, I try to beat the market. I’ll share some screens that I use for both of those portfolios.

The main equity component of my core portfolio is global equity exposure. That in turn means that finding a suitable global equity fund is extremely important. What seems simple on the surface is actually surprisingly difficult for a UK retail investor. That’s because you have so many choices! Personally my criteria are (a) cost, (b) truly global exposure (not just developed markets which exclude EM), (c) funds that trade in sterling and (d) accumulation funds to reduce maintenance time.

Another consideration is whether to look for Exchange Traded Funds or Open Ended Investment Companies. I’m fairly ambivalent about the legal fund wrapper as I’m not too bothered about intra-day pricing. That’s because I usually buy and hold for years at a time. However, on some investment platforms I use they are ETF only so that’s all I can use. For some UK investment platforms the fee to simply hold an OEIC can be a percentage of the amount you hold which can become very expensive indeed. I tend to stay away from those platforms, but that’s worth knowing.

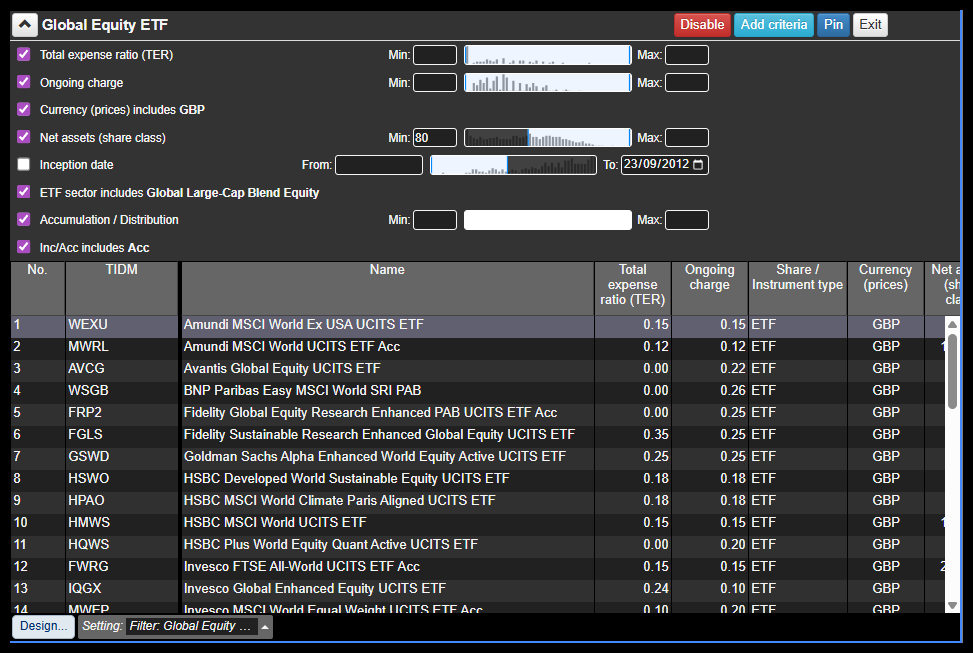

Finding Global Equity ETFs

Starting with global equity ETFs the criteria I’d typically choose would start with the right ETF sector. This would include “Global Large-Cap Blend Equity”. I’d also include “Ongoing charge” and the results would be sorted by this measure. It’s worth including Total Expense Ratio too as sometimes ongoing charge is zero whereas TER isn’t. Many platforms charge for FX conversions so I limit ETFs to be traded in GBP (Currency (prices) includes “GBP”). I try to avoid tiny funds which haven’t got much in terms of assets as these may be more likely to shut, so I apply a minimum “Net assets (share class)”. If you trade frequently, filtering for ETFs with larger net assets usually also means smaller bid-offer spreads. A reasonable minimum might be £80 million but this is easy to adjust and the histogram for each row is very useful indeed because you can instantly see how many of the funds you’re including or excluding with a particular range of that variable. Finally I’d include a filter for “Inc/Acc” to match just “Acc” so that any income is reinvested and doesn’t require any work on my part.

(You can run this screen for yourself by selecting the “PensionCraft – Global Equity ETF” filter within ShareScope’s Filter Library.)

Working with OEICs

If you’re filtering fund types (OEICs) then you can use the Investment Association’s categories. In the case of global equity OEICs for example you’d use IA sector “Global”. If it was, say, money market funds then you could choose IA Sector “Money Market” or “Short Term Money Market”

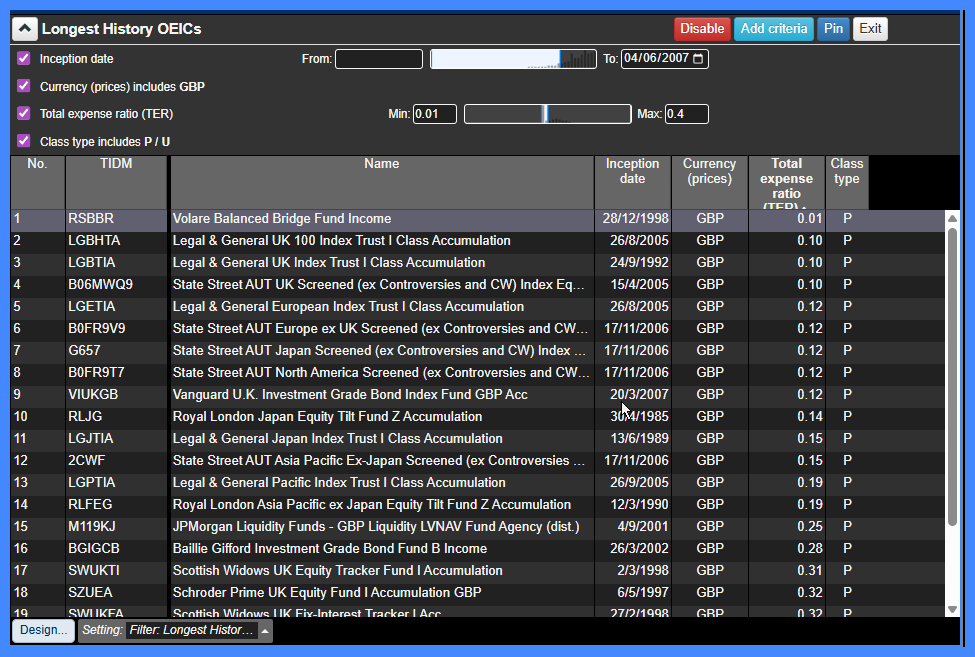

What about OEICs? Now I’d love to take credit for something that was added to ShareScope which is the ability to filter on whether an OEIC is the “primary” share class. That sounds trivial but it’s immensely valuable. Unlike most ETFs which come in a single form on all platforms OEICs come with multiple share classes that have a letter. This allows fund managers to take the same underlying portfolio and wrap it differently to service different clients. The same fund will have different fee levels, distribution types, target investors (retail vs institutional), platform rebates, or currencies based on this share class. If you filter OEICs, however, what this means in practice is that you’ll end up with multiple copies of the same fund. I only want one, ideally the one my platform is most likely to offer! And so ShareScope’s “Class Type” filter, which can have values “Primary”, “Alternative” or “Undefined” allows me to choose just the primary share class.

(You can run this screen for yourself by selecting the “PensionCraft – Longest History OEICs” filter within ShareScope’s Filter Library.)

Let’s say I want to find the OEICs with the longest histories for back-testing. That now becomes trivial. I set up a filter that includes “Inception date”, “Currency (prices)” which I choose to include GBP, Total Expense Ratio (TER) and Class type where I choose to include “P”. I can then sort the results by inception date to get the oldest retail funds available to UK investors. I’d usually also set a maximum expense ratio of 0.4% as I would only pay more than this for very special funds that offer something unusual.

The breadth and quality of the data available in ShareScope can substantially reduce the time required to check individual fund information, although important information should still be verified against current fund documentation.

Filtering for High Income

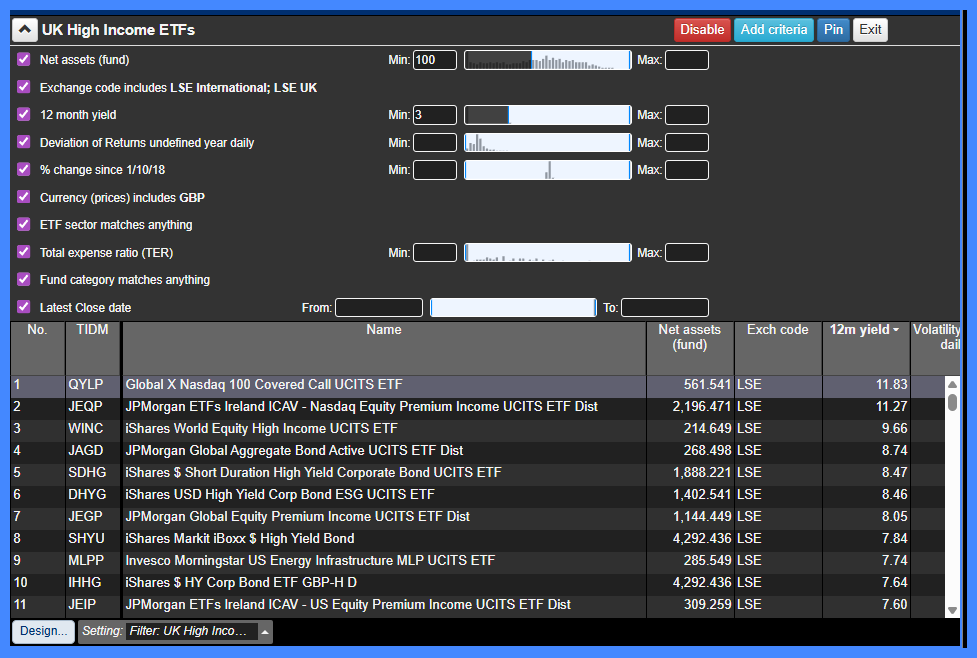

Finally another popular question is selecting high income funds and we can use ETFs as an example. I would typically apply my other usual criteria on cost, currency and size but there are some other things to think about in this case. If we filter based on minimum 12 month yield the problem is this selects funds where the price has crashed recently. Dividend yield is income divided by price so a suddenly much smaller price can result in huge yields. This means looking at recent return for the fund over the last 3 months, say, can be helpful. By choosing funds where the 3 month return is above a threshold you can omit these funds. I find volatility helpful here too because a fund that generates more yield (income) for the same amount of risk (volatility) is preferable. In ShareScope this is “Deviation of Returns” and I usually choose a period covering the last year measured with a daily sample frequency. If you filter by latest Close date being recent (last week or so) you can also ensure that this is not a fund that is not priced regularly and that the fund hasn’t been closed down.

(You can run this screen for yourself by selecting the “PensionCraft – UK High Income ETFs” filter within ShareScope’s Filter Library.)

Exporting Data for Analysis

This isn’t usually where my analysis ends. The result of filters is a table that displays the filtering columns but also any other columns you want. This means I can export the table (“Sharing”, then “Export table…”). The output is a CSV file that you can import to your favourite analysis package. For me that’s the statistical language R, but increasingly I suspect it would be your favourite AI model. You can then plot any relationship or build statistical models that describe the relationship between variables in the data.

When I first used ShareScope you’d wait minutes for data to load over a phone line. Now I’m piping its CSV exports into AI models for analysis. The platform has kept pace with every change in how I invest without sacrificing data quality. And that, more than anything, is why I keep coming back.

Ramin Nakisa

You can follow Ramin on the YouTube PensionCraft channel where he publishes a new video every Saturday and hosts a live Q&A on the first Thursday of each month at 7pm (UK time).

If you want to learn more about investing, explore the PensionCraft membership for in-depth tools, insights, and a supportive community: https://pensioncraft.com/membership.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Great walkthrough, Ramin. The ‘fun portfolio’ vs ‘core portfolio’ approach is a classic for a reason. Regarding those high-income filters, have you found that the volatility/yield ratio remains consistent across different market cycles, or do you find yourself having to adjust those thresholds more frequently lately?

Hi I tend to use the filters intermittently and I usually export as CSV files to do the analysis in R. For filters like volatility and yield I usually do it via ranking which is more stable than absolute numbers. But you’re right the absolute numbers aren’t stable