Bruce Packard highlights why, despite a darkening near-term outlook, investors may still have reasons to stay optimistic for the long term, as he examines developments across Burford (BUR), YouGov (YOU) and Treatt (TET).

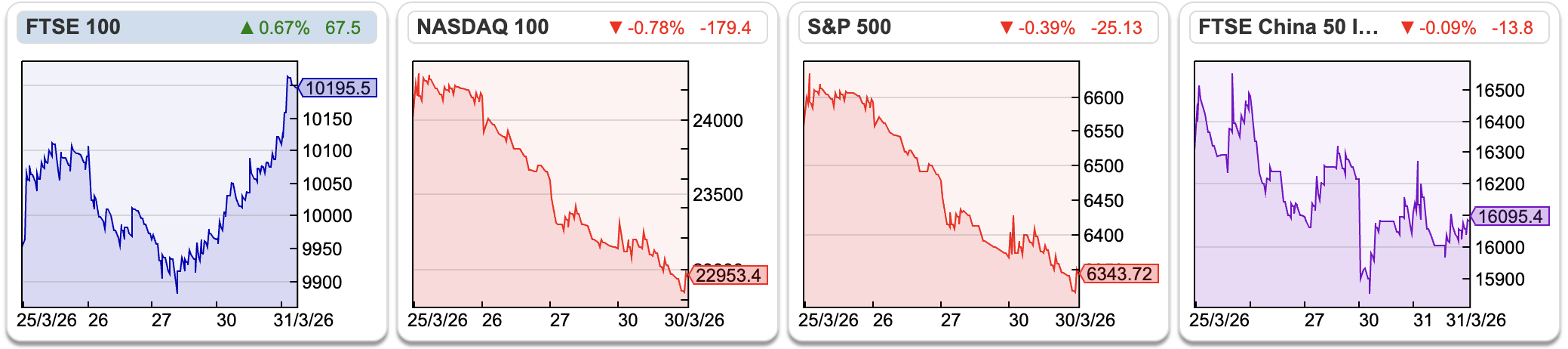

The FTSE 100 was up +2.3% in the last 5 days, and is now 10,195, helped by oil companies, miners and pharma sectors. The Nasdaq100 was down -5%, the worst performing major index. The US technology index is down -9% YTD, while the VIX is at 30.

The FTSE 100 was up +2.3% in the last 5 days, and is now 10,195, helped by oil companies, miners and pharma sectors. The Nasdaq100 was down -5%, the worst performing major index. The US technology index is down -9% YTD, while the VIX is at 30.

Brent Crude is currently $107 per barrel, up +76% YTD. People are beginning to worry about higher cost of fertiliser causing food price inflation. I found this 10 min YouTube interview by the former head of MI6, Sir Alex Younger insightful. He thinks Trump “underestimated the task” and has lost the initiative. Iran has “horizontally escalated”, attacking neighbours and undermined many countries energy security. The short term outlook is negative.

More optimistically Larry Fink, CEO of $14 trillion AuM Blackrock, has published his annual shareholders letter here. Although Blackrock has crushed UK fund managers like Aberdeen, Jupiter and Impax AM he is keen to attract more savings into the financial markets away from the banking system. He points out that even in the USA, which has the highest level of market participation, roughly 40% of the population has no exposure to the higher returns available from capital markets. This reminds me a little of Coca Cola saying that their biggest competitor was tap water. When your group becomes the most dominant player in the sector, people begin to ask questions about whether that’s healthy. Encouraging everyone to drink more fizzy, sugary coke rather than tap water, probably isn’t.

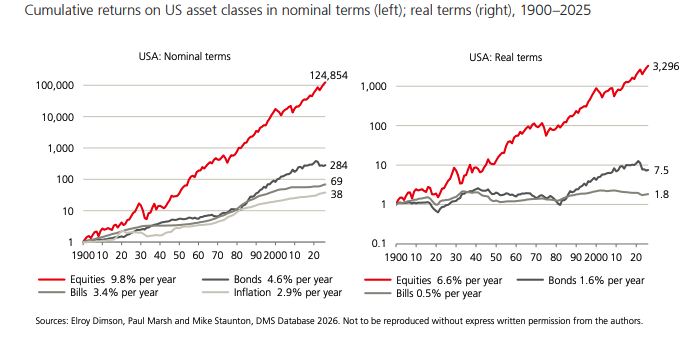

It’s worth reminding ourselves to remain long-term optimistic. The table shows the nominal (left) and real (right) returns in the stockmarket, according to the UBS Global Investment Returns Yearbook. I’ve used the US data, because UBS didn’t publish the UK market returns in the freely available summary version. According to the Barclays Equity Gilt study, UK real returns are +5% CAGR, and over a 2 year period equities beat cash 70% of the time (rising to 90% of the time over a decade). I’m cautious about the near-term outlook and have begun trimming positions, the idea is to make cash available to reinvest when valuations become compelling.

I now have my Mello ticket for 2nd and 3rd of June, at the Clayton Hotel in Chiswick. Looking forward to seeing many of you there.

This week I look at YouGov’s profit warning and dividend cut, and Treatt rising despite warning of an H2 weighting. But I start with Burford’s disappointment on losing their YPF expropriation case on Appeal.

Burford loses case against YPF case on Appeal

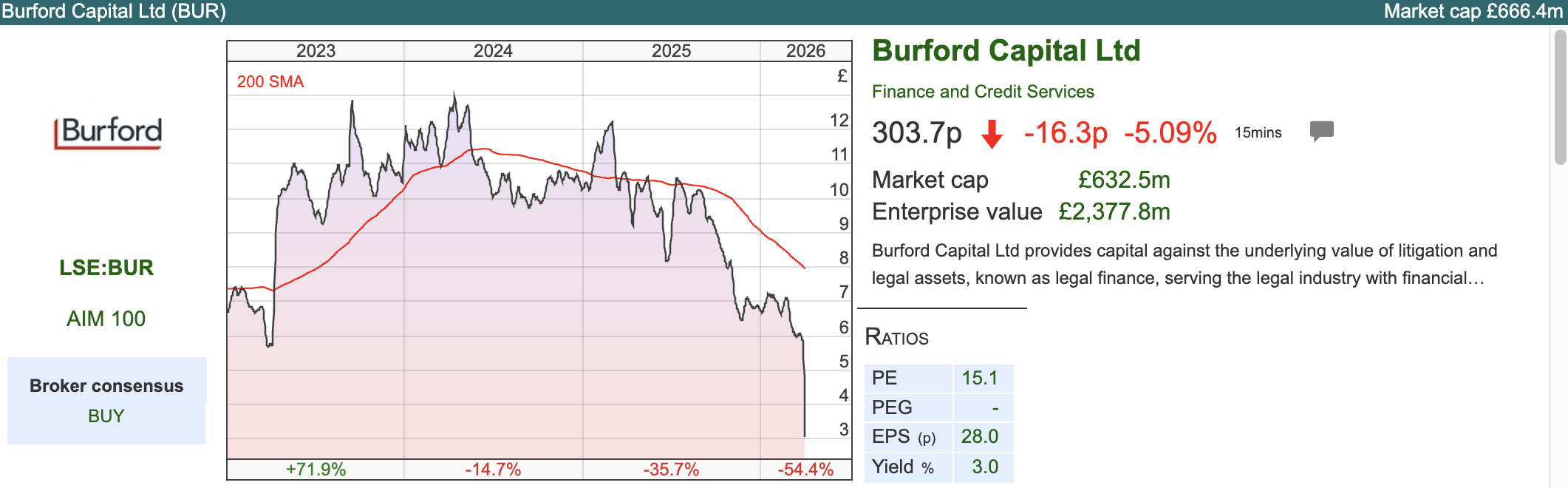

Disappointing news for Burford shareholders, including myself. As a reminder, this case has been running for a decade and a half, after Argentina nationalised oil company YPF, wiping out minority shareholders. Burford bought the claims and took them to court in New York, winning a $16bn judgement in Sept 2023, of which Burford would receive circa $6-7bn. This was on Burford’s book at a fair value of $1.7bn, as of Dec 2025, so there will be a significant write down of Burford’s equity value ($2.4bn shareholders equity, or 850p per share). The Appeals court in New York has decided that shareholders who suffered a loss should have attempted to take the Argentinian government to court in Argentina, rather than a private lawsuit in the USA.

Disappointing news for Burford shareholders, including myself. As a reminder, this case has been running for a decade and a half, after Argentina nationalised oil company YPF, wiping out minority shareholders. Burford bought the claims and took them to court in New York, winning a $16bn judgement in Sept 2023, of which Burford would receive circa $6-7bn. This was on Burford’s book at a fair value of $1.7bn, as of Dec 2025, so there will be a significant write down of Burford’s equity value ($2.4bn shareholders equity, or 850p per share). The Appeals court in New York has decided that shareholders who suffered a loss should have attempted to take the Argentinian government to court in Argentina, rather than a private lawsuit in the USA.

A non-cash write down wouldn’t be too serious if Burford was 100% financed by equity, however there’s also $2.2bn of debt financing on the balance sheet too. They have reduced refinancing risk but their covenants might prevent them from issuing more debt, effectively preventing them from issuing new bonds to fund cases until they can rebuild their equity through case wins from the investment portfolio. I have long pondered if litigation financing returns are so attractive, why then do groups like Burford or Manolete need to rely on debt to fund their opportunities? Are the returns only attractive when borrowing costs are low and what happens now that the “risk free” government bond yield has risen?

In response Burford say:

“We are sensitive that we now have more debt than the level we previously suggested was ideal. That said, we believe we are still not highly leveraged, we have carefully laddered our debt maturities to stretch out over the next eight years, and managing our debt load will be front of mind as we proceed. Given our strong cash position and our expected cash proceeds from our portfolio, we remain confident in our ability to achieve both continued growth and debt rationalization.”

Burford also say that their existing growth plans don’t rely on issuing more debt in the short and medium term and their debt covenants are not subject to debt equity ratio restrictions. The market reaction is not giving management the benefit of the doubt.

Valuation: Burford’s book value was 850p, or just over $11 per share. But that was before the writedown of the YPF case. Burford are still going to pursue the case through international arbitration, but I think investors might write off the whole $1.7bn in their minds, equating to 588p per share. Deducting that from the historic book value gives 259p versus a price off 303p today. In their most recent shareholder letter management suggests they aim to achieve 20% RoE over the long term – which would imply a multiple of 2-3x book value (depending on the assumed growth rate).

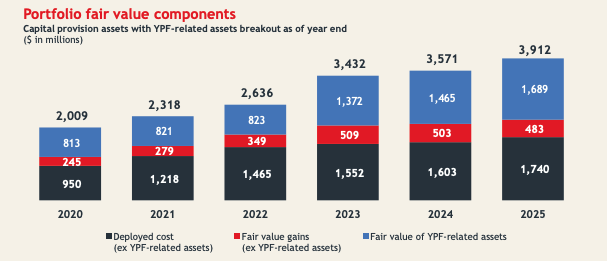

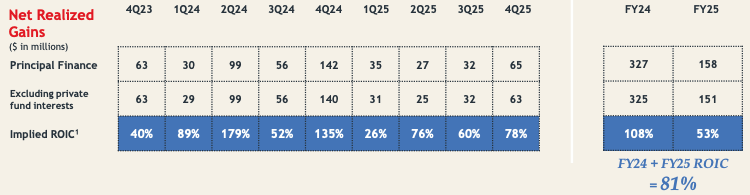

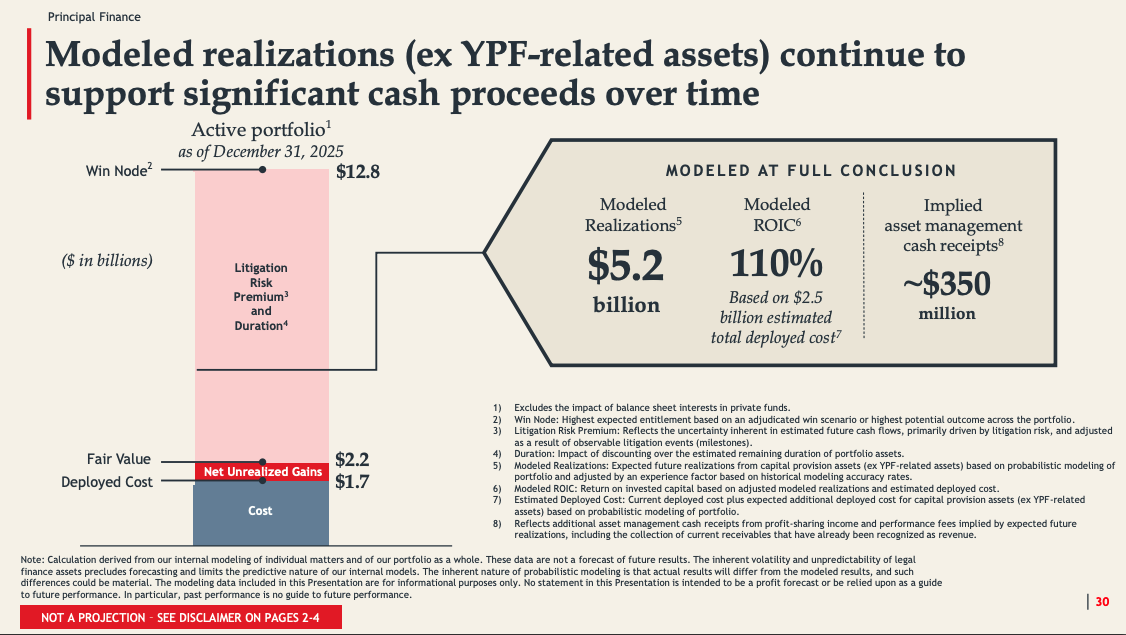

Interestingly, Burford’s share price had already more than halved in value since the Sept 2023 judgement, probably because investors were already anticipating an unfavourable decision from the Appeals court after the oral arguments were heard. The share price fell -41% last Friday, but Burford does still have $2.2bn of ex YPF litigation matters, of which more than ¾ is held at cost. They’ve modelled $5.2bn realisations from that portfolio – implying a 110% ROIC. That’s not a ballpark away from reality, though the historic cumulative ROIC achieved has been lower at 83%, and in 2025 this fell to 53% (down from 108% FY Dec 2024). Those $5.2bn realisations would be £18 per share, less debt of £7.60, would still leave a portfolio value just over £10 per share. Of course, you’d need to capitalise and deduct annual operating costs from that figure (£181m FY Dec 2025) and finance costs (£151m FY Dec 2025).

Opinion: Hard to believe but I bought early so I’ve still made a paper gain. Obviously, my paper gain would have been several times larger if I’d sold earlier! I tend to hold on to my winners, which can result in some painful paper losses. I won’t panic sell, but I’m not wedded to this position either. Litigation finance companies were supposed to provide uncorrelated returns to the rest of the index – unfortunately they’ve achieved that by going down when the market has risen over the last few years.

YouGov H1 Jan Results and Dividend Cut

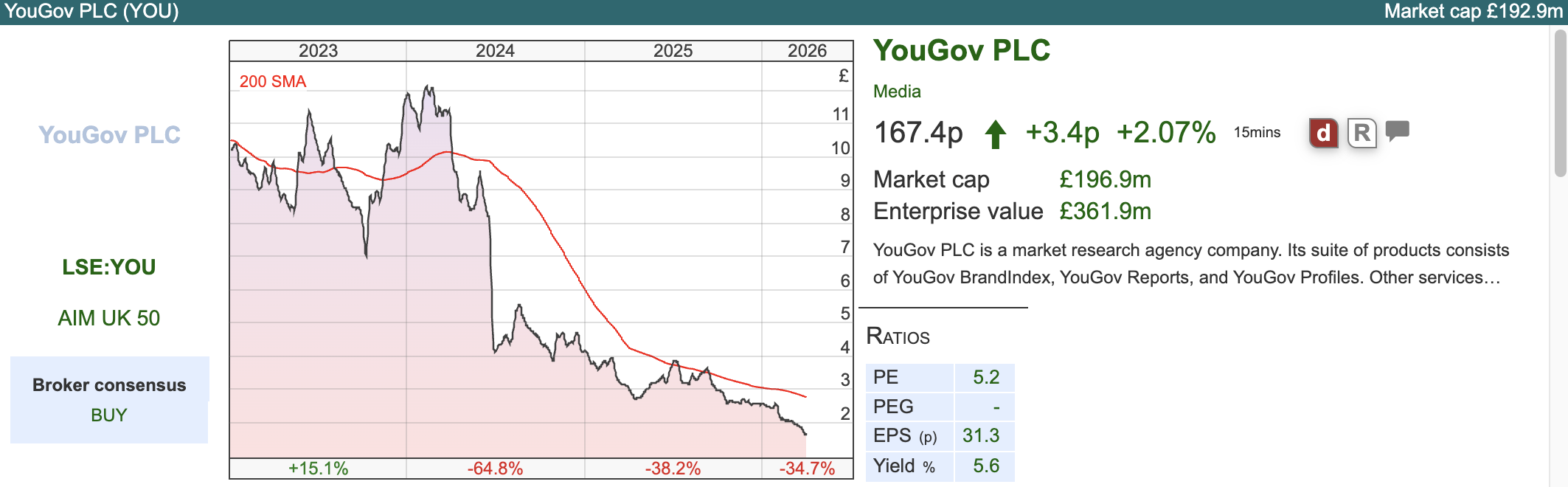

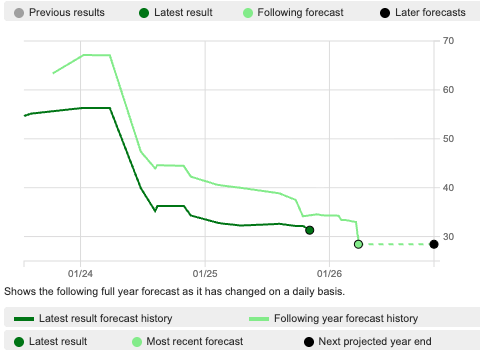

This marketing data and analytics reported revenue up +2% to £195m and statutory PBT +4% to £8.6m. However adj PBT was down -30% to £17m, and the Board has decided to scrap the dividend launching a buyback instead. That’s certainly a bold decision with net debt 2.1x EBITDA and EPS forecasts declining, as the Sharescope chart below shows.

This marketing data and analytics reported revenue up +2% to £195m and statutory PBT +4% to £8.6m. However adj PBT was down -30% to £17m, and the Board has decided to scrap the dividend launching a buyback instead. That’s certainly a bold decision with net debt 2.1x EBITDA and EPS forecasts declining, as the Sharescope chart below shows.

There was a nasty profit warning when the shares fell -40% in June 2024, which I wrote about here. The co-founder Stephan Shakespeare returned in early 2025 to turn things around. The share price has continued to decline and the Board has commenced a CEO search but with Shakespeare expected to remain in role until “the company is well positioned for its next stage of growth.” The CEO/co-founder currently owns less than 2% of the shares, according to Sharescope, so not exactly “skin in the game”. He owned 8% of the group in Nov 2020, so he most of the 6% he sold at between 900p and 1,150p—receiving over £50 million in value before the stock’s significant decline in 2024. More recently he’s been buying, in August and Oct 2025, but only 126K shares, worth significantly less than half a million pounds.

Adjustments: The reason that statutory PBT has improved versus the adjusted number, is that there’s a lower amortisation charge for acquired customer lists, and lower integration costs. Cash generated from operations was steady at £37m, but that falls to £14m after working capital and income tax paid (a -33% decline on the previous year). That’s almost 3x less than adj EBITDA of £38.5m.

There’s £418m of goodwill and intangible assets, after management bought GfK’s Consumer Panel Business for €315m in July 2023. YouGov’s traditional business focuses on survey’s asking what people think, the GfK Panel business (now called “Shopper”) focuses on what people actually buy. Their customers tend to be in the FMCG and retail sectors. However, this looks to have been a poor deal, they paid just under 10x EV/EBITDA (YOU currently EV/EBITDA 4x) £50m of the proceeds were funded with a placing at £9.20 per share (current YOU price £1.67). Net tangible assets are minus £231m, while net debt ex IFRS liabilities was £160m or 2.1x EBITDA.

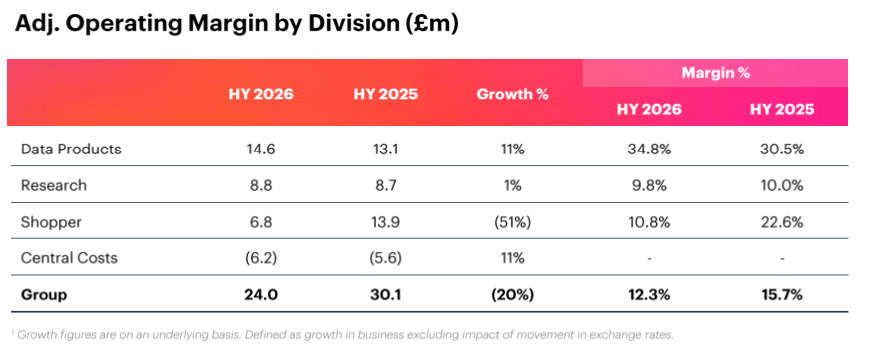

Divisional performance: They say the disappointing -2% revenue decline at the Shopper division reflects timing differences and expect the division to return to growth by the year end. They have responded by increasing investments in Shopper, hence the -51% decline in adj operating profits. They’ve launched a strategic review, presumably looking to sell the business.

On the bright side, the Data Products business (Brand Index and audience profiling). recorded a 35% adj operating margin, around 3x the group average.

Outlook: Management are investing an incremental £6m in their “Shopper” division so they now expect FY Jul group adjusted operating profit of £52-£56m. Effectively a -10% profit reduction.

Comparison with FUTR: We also saw Future warn on profits with the share price falling -23% yesterday morning. Both these groups look cheap on valuation basis, but the combination of debt on the balance sheet and declining revenue means that they could be “melting ice cubes”, disrupted by AI agents.

Valuation: YOU is trading on a PER of below 5x FY Jul 2027F and an EV/EBITDA of 3.5x the same year. For comparison, FUTR is on a PER of below 3x FY Sept 2027F and EV/EBITDA 2.4x the same year, though FUTR eps downward earnings revisions will take a couple of days to update.

Opinion: YouGov looks like a classic case of a successful business that makes a poor acquisition. The move to scrap the £10m dividend and replace it with a share buyback, is a bold move. If they can turn things around, they’ll look smart – but it is a risk if performance continues to struggle. The shares peaked at £16 at the end of 2021, while the share count has only increased +5% since then. If I had to choose between FUTR and YOU, I would chose YOU – but don’t own either.

Treatt AGM statement

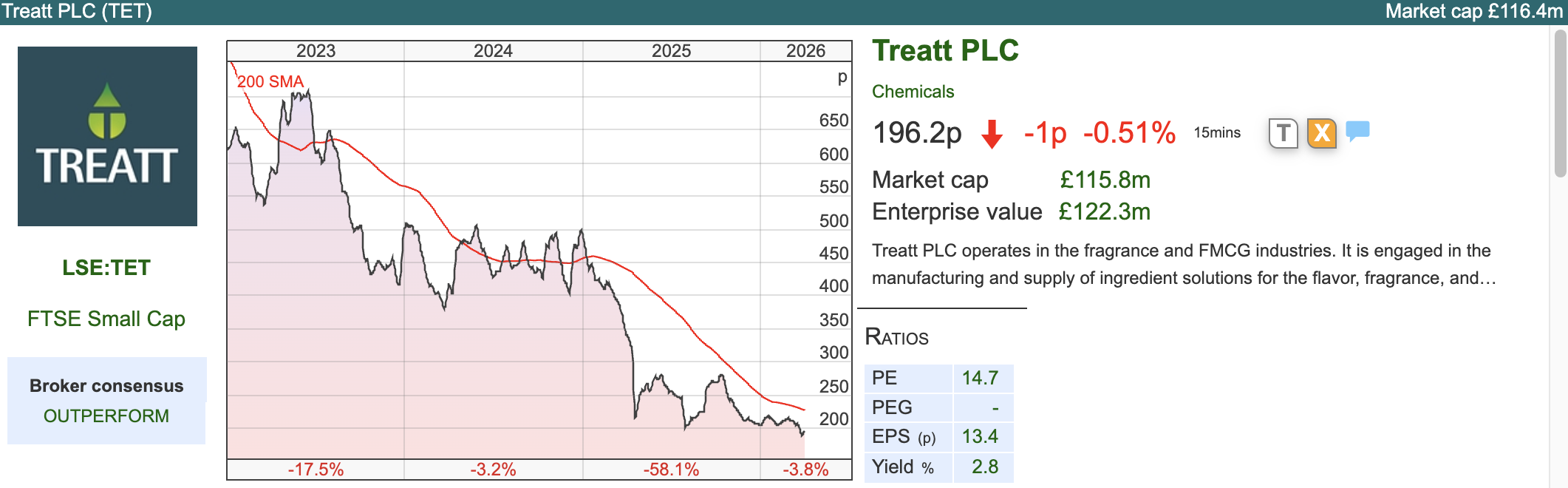

This group which makes natural additives for drinks, food flavour and fragrances released a H1 March trading update. Despite searching for a new CEO and warning of an H2 weighting the shares price rose +5% on the morning of the RNS, suggesting investor relief that performance hadn’t deteriorated. The next update will be on 12th May when H1 results will be announced. Hopefully management will have more visibility on H2 by then.

This group which makes natural additives for drinks, food flavour and fragrances released a H1 March trading update. Despite searching for a new CEO and warning of an H2 weighting the shares price rose +5% on the morning of the RNS, suggesting investor relief that performance hadn’t deteriorated. The next update will be on 12th May when H1 results will be announced. Hopefully management will have more visibility on H2 by then.

Recent history: As a reminder, the share price was strong over the pandemic, rising to over £13 per share. Investors were assuming, incorrectly as it turned out, that this was the type of business which could pass on higher costs of raw ingredients (citrus) to customers. An August 2022 profit warning meant we could reject that hypothesis. In late 2025 there was then an approach from Natara Global (backed by P.E. firm Exponent) at 260p per share, raised to 290p per share. Döhler, a German ingredients business, bought a blocking stake by buying up shares to take their holding to 28% – just below the 30% threshold where they would be required to make a bid for the entire company. Döhler now have representation on the board, though it’s not clear (to me at least) what their next move will be.

Valuation: The shares are trading on 13x Sept 2027F and EV/EBITDA of 6x.. Remember though that there’s an H2 weighting – so we should be less confident about those forecasts than other groups that have more visibility.

Opinion: I already opened a starter position. As Döhler continue their blocking stake, you could argue that they’ve made sure that a key supplier isn’t going to use inflation as an excuse to hike prices (as an aggressive P.E. backed management might try to do). It’s a fascinating situation, on a two year time horizon I think TET looks fundamentally undervalued, but we’re unlikely to see another bid emerge while Döhler has a blocking stake. Possibly Döhler themselves bid, which would mean acquiring their target without a bidding war against Private Equity.

Bruce Packard

@bruce_packard

Notes

Bruce own shares in TET and BUR

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Bi-Weekly Market Commentary | 01/04/2026 | BUR, YOU, TET | Long-term optimism

Bruce Packard highlights why, despite a darkening near-term outlook, investors may still have reasons to stay optimistic for the long term, as he examines developments across Burford (BUR), YouGov (YOU) and Treatt (TET).

Brent Crude is currently $107 per barrel, up +76% YTD. People are beginning to worry about higher cost of fertiliser causing food price inflation. I found this 10 min YouTube interview by the former head of MI6, Sir Alex Younger insightful. He thinks Trump “underestimated the task” and has lost the initiative. Iran has “horizontally escalated”, attacking neighbours and undermined many countries energy security. The short term outlook is negative.

More optimistically Larry Fink, CEO of $14 trillion AuM Blackrock, has published his annual shareholders letter here. Although Blackrock has crushed UK fund managers like Aberdeen, Jupiter and Impax AM he is keen to attract more savings into the financial markets away from the banking system. He points out that even in the USA, which has the highest level of market participation, roughly 40% of the population has no exposure to the higher returns available from capital markets. This reminds me a little of Coca Cola saying that their biggest competitor was tap water. When your group becomes the most dominant player in the sector, people begin to ask questions about whether that’s healthy. Encouraging everyone to drink more fizzy, sugary coke rather than tap water, probably isn’t.

It’s worth reminding ourselves to remain long-term optimistic. The table shows the nominal (left) and real (right) returns in the stockmarket, according to the UBS Global Investment Returns Yearbook. I’ve used the US data, because UBS didn’t publish the UK market returns in the freely available summary version. According to the Barclays Equity Gilt study, UK real returns are +5% CAGR, and over a 2 year period equities beat cash 70% of the time (rising to 90% of the time over a decade). I’m cautious about the near-term outlook and have begun trimming positions, the idea is to make cash available to reinvest when valuations become compelling.

I now have my Mello ticket for 2nd and 3rd of June, at the Clayton Hotel in Chiswick. Looking forward to seeing many of you there.

This week I look at YouGov’s profit warning and dividend cut, and Treatt rising despite warning of an H2 weighting. But I start with Burford’s disappointment on losing their YPF expropriation case on Appeal.

Burford loses case against YPF case on Appeal

A non-cash write down wouldn’t be too serious if Burford was 100% financed by equity, however there’s also $2.2bn of debt financing on the balance sheet too. They have reduced refinancing risk but their covenants might prevent them from issuing more debt, effectively preventing them from issuing new bonds to fund cases until they can rebuild their equity through case wins from the investment portfolio. I have long pondered if litigation financing returns are so attractive, why then do groups like Burford or Manolete need to rely on debt to fund their opportunities? Are the returns only attractive when borrowing costs are low and what happens now that the “risk free” government bond yield has risen?

In response Burford say:

“We are sensitive that we now have more debt than the level we previously suggested was ideal. That said, we believe we are still not highly leveraged, we have carefully laddered our debt maturities to stretch out over the next eight years, and managing our debt load will be front of mind as we proceed. Given our strong cash position and our expected cash proceeds from our portfolio, we remain confident in our ability to achieve both continued growth and debt rationalization.”

Burford also say that their existing growth plans don’t rely on issuing more debt in the short and medium term and their debt covenants are not subject to debt equity ratio restrictions. The market reaction is not giving management the benefit of the doubt.

Valuation: Burford’s book value was 850p, or just over $11 per share. But that was before the writedown of the YPF case. Burford are still going to pursue the case through international arbitration, but I think investors might write off the whole $1.7bn in their minds, equating to 588p per share. Deducting that from the historic book value gives 259p versus a price off 303p today. In their most recent shareholder letter management suggests they aim to achieve 20% RoE over the long term – which would imply a multiple of 2-3x book value (depending on the assumed growth rate).

Interestingly, Burford’s share price had already more than halved in value since the Sept 2023 judgement, probably because investors were already anticipating an unfavourable decision from the Appeals court after the oral arguments were heard. The share price fell -41% last Friday, but Burford does still have $2.2bn of ex YPF litigation matters, of which more than ¾ is held at cost. They’ve modelled $5.2bn realisations from that portfolio – implying a 110% ROIC. That’s not a ballpark away from reality, though the historic cumulative ROIC achieved has been lower at 83%, and in 2025 this fell to 53% (down from 108% FY Dec 2024). Those $5.2bn realisations would be £18 per share, less debt of £7.60, would still leave a portfolio value just over £10 per share. Of course, you’d need to capitalise and deduct annual operating costs from that figure (£181m FY Dec 2025) and finance costs (£151m FY Dec 2025).

Opinion: Hard to believe but I bought early so I’ve still made a paper gain. Obviously, my paper gain would have been several times larger if I’d sold earlier! I tend to hold on to my winners, which can result in some painful paper losses. I won’t panic sell, but I’m not wedded to this position either. Litigation finance companies were supposed to provide uncorrelated returns to the rest of the index – unfortunately they’ve achieved that by going down when the market has risen over the last few years.

YouGov H1 Jan Results and Dividend Cut

There was a nasty profit warning when the shares fell -40% in June 2024, which I wrote about here. The co-founder Stephan Shakespeare returned in early 2025 to turn things around. The share price has continued to decline and the Board has commenced a CEO search but with Shakespeare expected to remain in role until “the company is well positioned for its next stage of growth.” The CEO/co-founder currently owns less than 2% of the shares, according to Sharescope, so not exactly “skin in the game”. He owned 8% of the group in Nov 2020, so he most of the 6% he sold at between 900p and 1,150p—receiving over £50 million in value before the stock’s significant decline in 2024. More recently he’s been buying, in August and Oct 2025, but only 126K shares, worth significantly less than half a million pounds.

Adjustments: The reason that statutory PBT has improved versus the adjusted number, is that there’s a lower amortisation charge for acquired customer lists, and lower integration costs. Cash generated from operations was steady at £37m, but that falls to £14m after working capital and income tax paid (a -33% decline on the previous year). That’s almost 3x less than adj EBITDA of £38.5m.

There’s £418m of goodwill and intangible assets, after management bought GfK’s Consumer Panel Business for €315m in July 2023. YouGov’s traditional business focuses on survey’s asking what people think, the GfK Panel business (now called “Shopper”) focuses on what people actually buy. Their customers tend to be in the FMCG and retail sectors. However, this looks to have been a poor deal, they paid just under 10x EV/EBITDA (YOU currently EV/EBITDA 4x) £50m of the proceeds were funded with a placing at £9.20 per share (current YOU price £1.67). Net tangible assets are minus £231m, while net debt ex IFRS liabilities was £160m or 2.1x EBITDA.

Divisional performance: They say the disappointing -2% revenue decline at the Shopper division reflects timing differences and expect the division to return to growth by the year end. They have responded by increasing investments in Shopper, hence the -51% decline in adj operating profits. They’ve launched a strategic review, presumably looking to sell the business.

On the bright side, the Data Products business (Brand Index and audience profiling). recorded a 35% adj operating margin, around 3x the group average.

Outlook: Management are investing an incremental £6m in their “Shopper” division so they now expect FY Jul group adjusted operating profit of £52-£56m. Effectively a -10% profit reduction.

Comparison with FUTR: We also saw Future warn on profits with the share price falling -23% yesterday morning. Both these groups look cheap on valuation basis, but the combination of debt on the balance sheet and declining revenue means that they could be “melting ice cubes”, disrupted by AI agents.

Valuation: YOU is trading on a PER of below 5x FY Jul 2027F and an EV/EBITDA of 3.5x the same year. For comparison, FUTR is on a PER of below 3x FY Sept 2027F and EV/EBITDA 2.4x the same year, though FUTR eps downward earnings revisions will take a couple of days to update.

Opinion: YouGov looks like a classic case of a successful business that makes a poor acquisition. The move to scrap the £10m dividend and replace it with a share buyback, is a bold move. If they can turn things around, they’ll look smart – but it is a risk if performance continues to struggle. The shares peaked at £16 at the end of 2021, while the share count has only increased +5% since then. If I had to choose between FUTR and YOU, I would chose YOU – but don’t own either.

Treatt AGM statement

Recent history: As a reminder, the share price was strong over the pandemic, rising to over £13 per share. Investors were assuming, incorrectly as it turned out, that this was the type of business which could pass on higher costs of raw ingredients (citrus) to customers. An August 2022 profit warning meant we could reject that hypothesis. In late 2025 there was then an approach from Natara Global (backed by P.E. firm Exponent) at 260p per share, raised to 290p per share. Döhler, a German ingredients business, bought a blocking stake by buying up shares to take their holding to 28% – just below the 30% threshold where they would be required to make a bid for the entire company. Döhler now have representation on the board, though it’s not clear (to me at least) what their next move will be.

Valuation: The shares are trading on 13x Sept 2027F and EV/EBITDA of 6x.. Remember though that there’s an H2 weighting – so we should be less confident about those forecasts than other groups that have more visibility.

Opinion: I already opened a starter position. As Döhler continue their blocking stake, you could argue that they’ve made sure that a key supplier isn’t going to use inflation as an excuse to hike prices (as an aggressive P.E. backed management might try to do). It’s a fascinating situation, on a two year time horizon I think TET looks fundamentally undervalued, but we’re unlikely to see another bid emerge while Döhler has a blocking stake. Possibly Döhler themselves bid, which would mean acquiring their target without a bidding war against Private Equity.

Bruce Packard

@bruce_packard

Notes

Bruce own shares in TET and BUR

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.