Bruce returns with a looks at some of AIM’s top performers (EEE, MTL, YU.) since the market peaked in Sept 2021. Plus results from SRT and CRW.

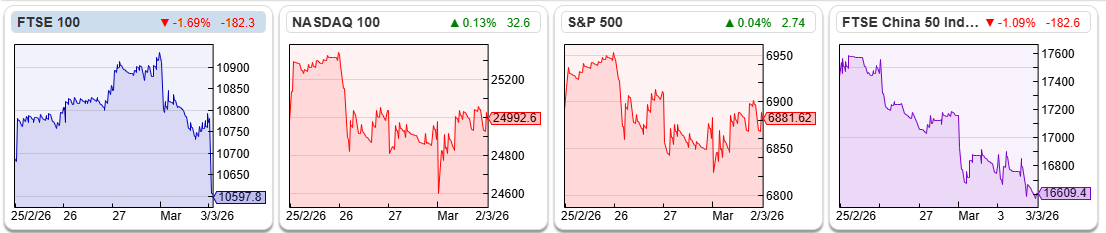

The FTSE 100 fell -1% but remained above 10,000 over the last 5 trading days. The Nasdaq100 was up +1%, while the FTSE China 50 fell -4.6%. Brent Crude was up +14% as conflict between US, Israel and Iran closed the Straits of Hormuz. Qatar shutdown LNG at world’s largest export facility after it was targeted in an Iranian drone attack.

The FTSE 100 fell -1% but remained above 10,000 over the last 5 trading days. The Nasdaq100 was up +1%, while the FTSE China 50 fell -4.6%. Brent Crude was up +14% as conflict between US, Israel and Iran closed the Straits of Hormuz. Qatar shutdown LNG at world’s largest export facility after it was targeted in an Iranian drone attack.

Aside from violence and instability in the Gulf region, there’s still much talk of the tech/AI bubble bursting in the US markets, and a reckoning is coming. Palantir ($340bn market cap) is trading on 80x revenue according to ShareScope and some people think SpaceX ($15bn revenue 2025) is worth $1.5trillion. The Nasdaq 100 looks like it could be forming a top after 3 strong years.

Something that I’ve been pondering: even if an investor can correctly identify a market top, what then?

One answer is to sell everything and go into cash, sail away on a yacht with no internet, then wait 3-4 years. Presumably at least two people have had the self-discipline to do that, because their picture was on the ShareScope website a couple of years ago!

Gold is attractive as a “safe haven asset” but the price of the yellow metal at $5,300 is already up +80% since the start of last year and up 4.5x since before the pandemic.

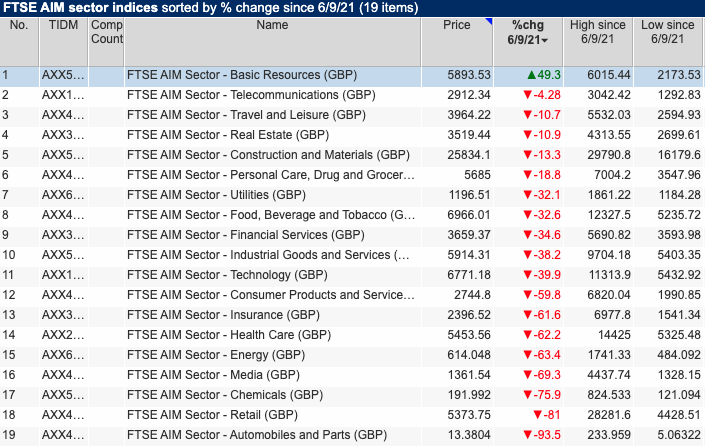

Another approach is to look at themes for companies that have done well when the market as a whole does badly. While US markets could be approaching a top, London’s AIM peaked in Sept 2021 at 1,310, versus 815 currently. Below I’ve used ShareScope to show the top performers even as the index itself has disappointed (finally troughing at 620 in April 2025).

Since Sept 2021 the only Industry in positive territory is Basic Materials (ie mining and oil, and within that Precious Metals and Mining sector) up +49%. Individual names such as Empire Metals, Metals Exploration, Borders & Southern Petroleum, Rockhopper and Strategic Minerals are all resource extraction. The only stock I own in that list above is MS International, the defence group, which I bought well before the pandemic. Below we can see that 7 AIM sectors, including Retail and Media have had a terrible time, down -60% or more. Even though the Nasdaq 100 is up +60% since Sept 2021, the AIM listed Technology sectors has struggled, down -40%.

The fact that EEE and MTL followed very different paths to multi-bagger glory suggests that success was idiosyncratic. Metals Exploration was heavily indebted with $111m of net debt in 2021 (only just below the previous FY revenue of $122m) and management had struggled with high fixed costs to generate profits from their Philippines based Runruno gold project. So, on top of financial leverage the gold mine was also operationally geared. MTL was operating a marginal business model when the gold price was below $2,000 an ounce. However, that high fixed cost base and paying down debt delivered impressive increases in profit as the gold price rose.

Empire Metals was even more fortunate. The original investment case was based on finding copper in Western Australia. By accident, they discovered the Pitfield Titanium Project in Western Australia which drilling revealed to be a giant titanium mineral system.

Empire Metals was even more fortunate. The original investment case was based on finding copper in Western Australia. By accident, they discovered the Pitfield Titanium Project in Western Australia which drilling revealed to be a giant titanium mineral system.

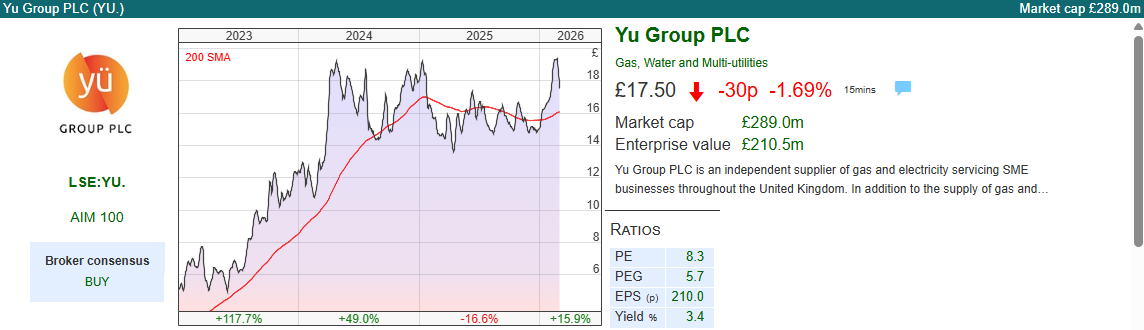

Other stocks on the top performers list are Filtronic, up +1510%, the second best performer here, which I wrote about here. Yü Group up +613% below.

Yü Group helps businesses “shop around” and manage their energy contracts. There were some similarities with the business model of Utilitywise, which failed after some investors questioned the accounting policies (recognising revenue upfront for multi-year contracts). Both groups were trying to disrupt the B2B energy buying process. Understandably, investors had beaten down the valuation of Yü Group.

Credit to Bobby Kalar, founder and majority shareholder of the business. He stayed on as Chief Exec, realigned incentives, fixed the controls, took some tough decisions and the company survived. Not only survived it became multi-bagger success story, rising over 30x from its pandemic low in April 2020! At the start of 2021 Yü was reporting ahead of consensus revenue, cash and profit. So, when you see a market top, try to keep an eye out for turnarounds that are just starting to deliver and there’s a great deal of (perhaps deserved!) investor scepticism. I’ve already missed most of the upside on Yü Group, indeed Paul Hill and Paul Scott point out on their YouTube show that Yü may be a victim of AI agent disruption.

Credit to Bobby Kalar, founder and majority shareholder of the business. He stayed on as Chief Exec, realigned incentives, fixed the controls, took some tough decisions and the company survived. Not only survived it became multi-bagger success story, rising over 30x from its pandemic low in April 2020! At the start of 2021 Yü was reporting ahead of consensus revenue, cash and profit. So, when you see a market top, try to keep an eye out for turnarounds that are just starting to deliver and there’s a great deal of (perhaps deserved!) investor scepticism. I’ve already missed most of the upside on Yü Group, indeed Paul Hill and Paul Scott point out on their YouTube show that Yü may be a victim of AI agent disruption.

Thus, I take two general lessons from the analysis above: 1) Be open minded about sectors, if everyone else is avoiding speculative miners, it doesn’t take much to keep up a passing interest. 2) Pay attention when beaten down sectors start announcing positive news and ahead of expectations RNS’s.

The two most hated sectors I can think of at the moment are marketing (SFOR, SAA, NFG) and litigation finance (BUR, MANO). If we start to see companies in these sectors beating consensus, then being open minded could turn out to be highly rewarding.

This week I look at SRT Marine’s latest maritime surveillance contract win and Craneware’s (SaaS US hospital billing) H1 Dec results. Although both are in the information and data business, I think they both have genuine “moats” and make an interesting case study in what might be difficult for AI Agents to disrupt.

SRT Marine $20.5m Contract Win

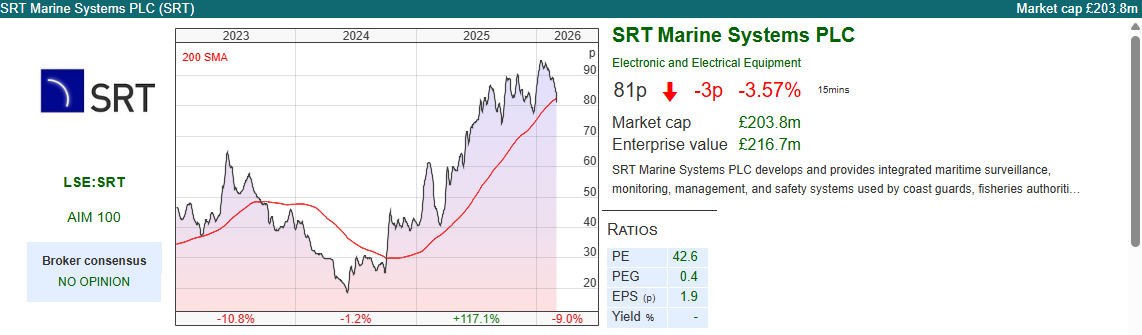

This Midsomer Norton (Somerset, UK) based provider of maritime surveillance systems (for governments) and maritime navigation safety systems (for boats and infrastructures) put out a $20.5m contract win announcement last week. That follows a January trading update, which saw H1 Dec group revenue up +96% to £51m and PBT +47% to £3.1m.

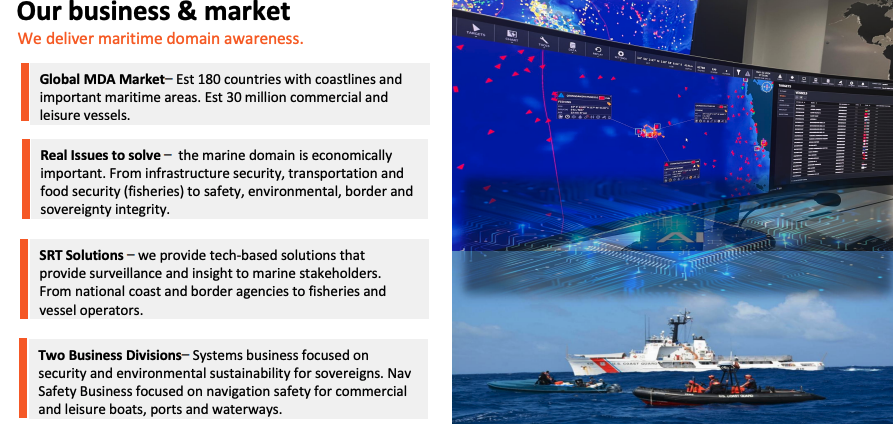

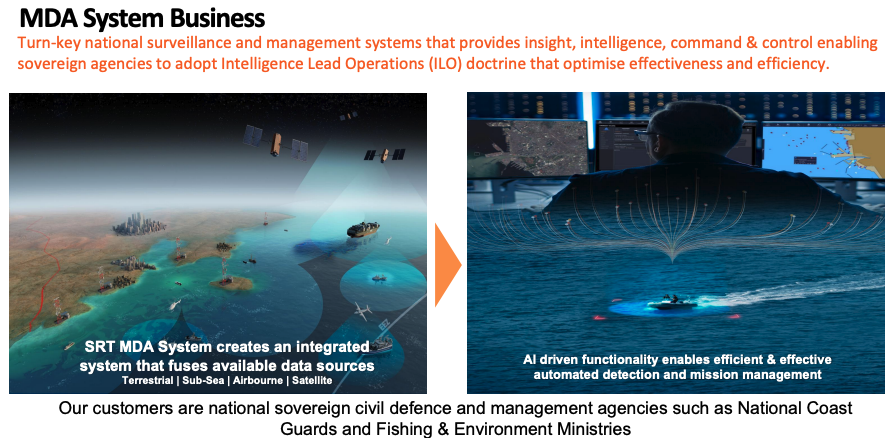

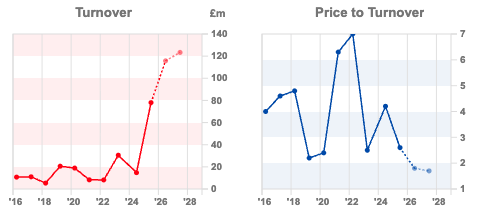

Their Maritime Domain Awareness (MDA) technology helps sovereign agencies such as Coast Guards and Fishery Authorities to track activity for maritime safety and security. Their navigation safety systems enable vessel operators to navigate more safely and efficiently. I don’t think they’ve said anything publicly, but I would imagine the rise of Russia’s shadow uninsured tanker fleet has been a commercial tailwind. So, you won’t find a button on their website saying “press here to track Russian tankers”, but SRT’s core business is selling the “eyes and ears” that governments use for that purpose. As the shadow fleet becomes more sophisticated at hiding, the demand for SRT’s high-end surveillance systems help “unmask” the dark fleet. Revenue is forecast to grow to £116m FY Jun 2026F, compared to £8.2m FY Mar 2022 – that’s an increase of 14x in 4 years.

The latest contract $20.5m win is with an existing sovereign customer, so a follow-on contract to expand the scope of existing work. Cavendish, their broker, say that timing remains unclear but says that there’s “good visibility” on £500m worth of contracts, within an impressive £1.8bn validated sales pipeline. There are no changes to forecasts following last week’s RNS, but presumably we can be more confident that FY Jun 2026F £116m revenue and adj PBT of £10.2m and FY Jun 2027F £123m revenue and adj PBT of £11m will be achieved. Worth noting that even with rapid revenue growth the margin is still less than 10%, so although the tech is impressive, this doesn’t seem to have operational gearing in the same way that a software platform does.

Valuation: Using Cavendish’s forecasts suggests EV/EVITDA of 18x both Jun 2026F and 2027F, with an price/sales of just below 2x. The PER ratio is 20x Jun 2026F, dropping to 19x the following year.

Opinion: Frustrated that I missed this. The shares fell below 20p in Jun 2024, down by -75% versus Jun the previous year. That does highlight the risk of lumpy contracts, SRT went on a hiring spree and invested in equipment, and the revenue didn’t come through until the following financial year. The group now seems to be on an “even keel”, and the technology looks both useful and hard to disrupt. However looking at the chart the shares are testing the 200 moving average, so might be worth waiting to see if the price fall through that support level?

Craneware H1 Dec results

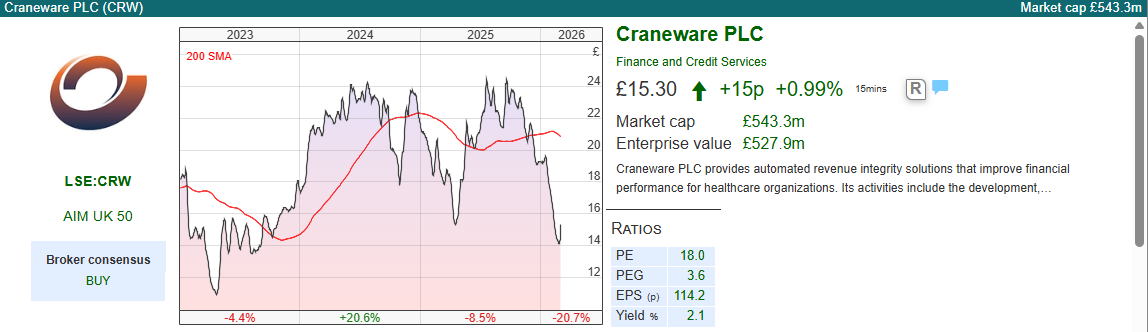

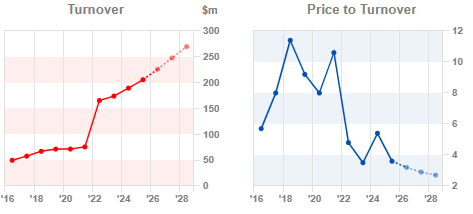

This Edinburgh based Software as a Service (Saas) group which provides billing services to US hospitals announced group revenue + 6% to $106m and statutory PBT up +29% to $13m. Annual Recurring Revenue (ARR) also continues to grow +4% while the customer retention rate is above 90%. The gross margin is 85%. The shares 20 bagged from 2007-2018, but since then share price performance has been dull. Last year there was an opportunistic approach from Private Equity that was rebuffed and CRW management have announced a buyback with $25m to be returned to shareholders.

This Edinburgh based Software as a Service (Saas) group which provides billing services to US hospitals announced group revenue + 6% to $106m and statutory PBT up +29% to $13m. Annual Recurring Revenue (ARR) also continues to grow +4% while the customer retention rate is above 90%. The gross margin is 85%. The shares 20 bagged from 2007-2018, but since then share price performance has been dull. Last year there was an opportunistic approach from Private Equity that was rebuffed and CRW management have announced a buyback with $25m to be returned to shareholders.

There’s little sign of fear from disruption by AI Agents in the management commentary, with CEO Keith Neilson saying: “The US healthcare market continues to evolve at pace, and with each new piece of legislation or change, the need for data led insights and a secure and scalable technology partner grows. We have never been more confident in the vital role we play…“

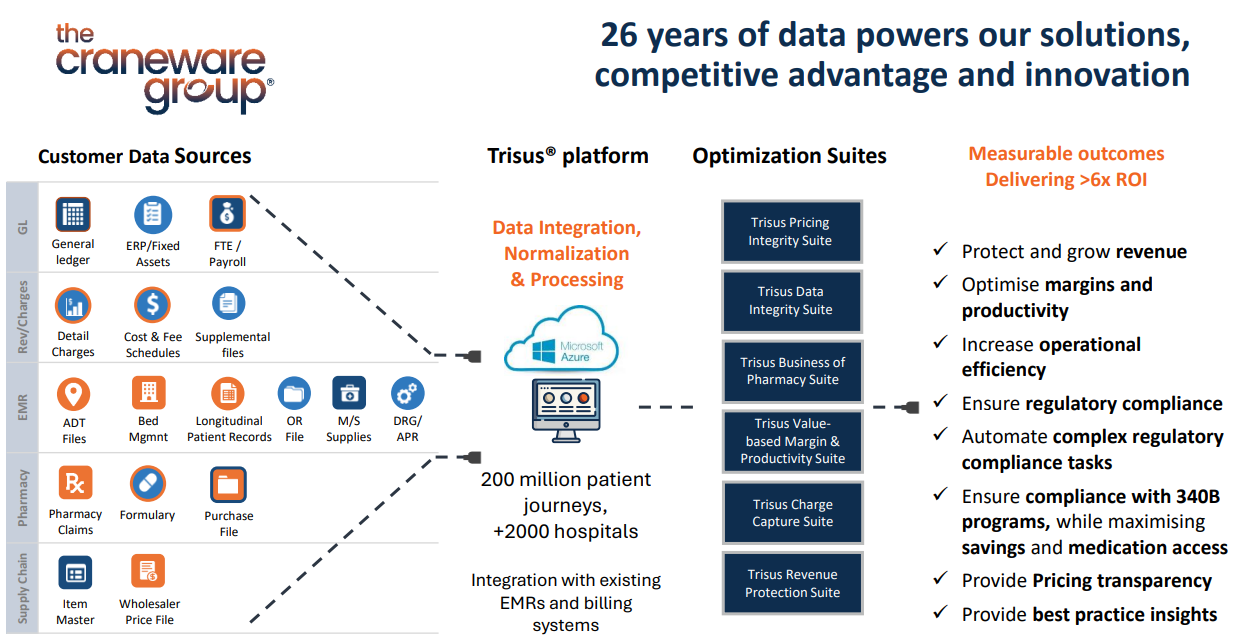

Management have already announced a partnership with Microsoft, to implement AI through the group’s Trisus platform. Around 40% of US hospitals are customers, which spend almost a trillion dollars, so CRW costs are a tiny share of overall hospital operating expenses, the risk from switching to a more disruptive platform seem to greatly outweigh any cost saving benefits. In addition CRW software is hard-coded into the hospital’s financial ledger, so unlike a company like LSEG where company data is publicly available, Tirsus operates behind hospital firewalls. No LLM can “scrape” a hospital’s internal pharmacy spend and an agent can’t interface with a hospital’s billing system without the underlying protocols Craneware provides.

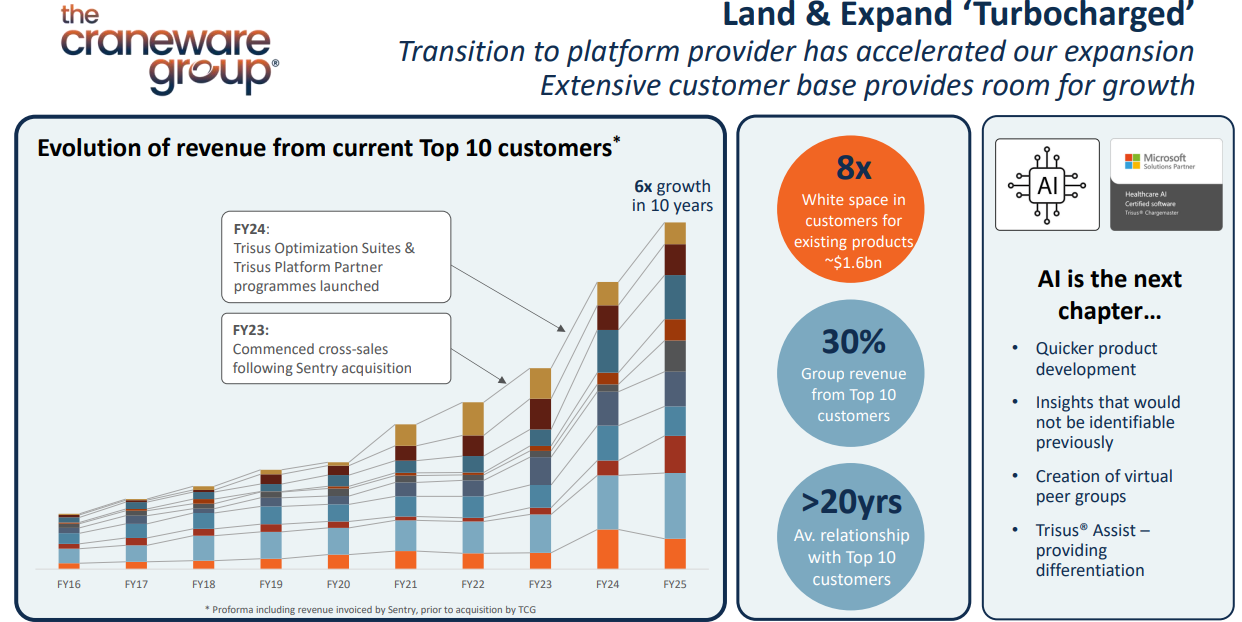

Acquisition: In June 2021, management announced the acquisition of Sentry Data Systems, which had a customer base of 10,000 hospitals, pharmacies and clinics, including over 600 US hospitals (of which only approximately 35% overlapped with existing Craneware customers). The $400m price represented 4.3x historic sales, and 17x EBITDA.

Valuation: Craneware shares are trading on 15x 2027F PER and 8.5x EV/EBITDA or 2.9x price/sales the same year. So the group’s current valuation ratios represents around half of the multiples they paid for Sentry 5 years ago. To be fair, Sentry does seem to helped them generate organic growth since 2022.

When Maynard looked at CRW in 2019, the PER had been as high as 60x and price/sales > 10x, so he worried (rightly as it turned out) about profits growing, but the multiples were too high and the shares being at beginning of a long term de-rating.

Given the mid 80’s gross margin, I was surprised to see 3 year average RoCE was just 4.5%. The cause seems to be the $400m acquisition Sentry Data Systems in 2021 and capitalised R&D spend being added to the balance sheet, which increases the “Capital Employed” denominator.

For comparison, Tristel the chorine dioxide medical device disinfectant group which also reported on Monday, has a gross margin above 80%, but reports ROCE above 20%, with an EBIT margin of 22%.

Opinion: There was an approach for Craneware from Bain Capital in May last year, at a price of £26.50 per share or a c. 30% premium to the undisturbed price. Although the current share price of 1530p is well below the Bain offer, my view is that management were right to reject the approach. It looks to me like CRW is in an “investment phase” at the moment, and we could see the benefits of that come through in 2-5 years time. Private Equity tend to buy companies when profits are suppressed by investment, then wait a few years and float companies back to public markets having starved those companies of investment and flattered profits. I’ve never understood why professional fund managers let P.E. firms do this.

I think Craneware (and SRT Marine for that matter) make an interesting case study on what AI Agents might not be able to disrupt. Clearly investors are sceptical at the moment of groups like LSEG, RELX and even RMV, but Craneware does seem to have a genuine “moat”. I don’t own any, but think the investment case looks reasonable.

Bruce Packard

@bruce_packard

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Bi-Weekly Market Commentary | 04/03/2026 | EEE, MTL, YU., SRT, CRW | What to buy at the top

Bruce returns with a looks at some of AIM’s top performers (EEE, MTL, YU.) since the market peaked in Sept 2021. Plus results from SRT and CRW.

Aside from violence and instability in the Gulf region, there’s still much talk of the tech/AI bubble bursting in the US markets, and a reckoning is coming. Palantir ($340bn market cap) is trading on 80x revenue according to ShareScope and some people think SpaceX ($15bn revenue 2025) is worth $1.5trillion. The Nasdaq 100 looks like it could be forming a top after 3 strong years.

Something that I’ve been pondering: even if an investor can correctly identify a market top, what then?

One answer is to sell everything and go into cash, sail away on a yacht with no internet, then wait 3-4 years. Presumably at least two people have had the self-discipline to do that, because their picture was on the ShareScope website a couple of years ago!

Gold is attractive as a “safe haven asset” but the price of the yellow metal at $5,300 is already up +80% since the start of last year and up 4.5x since before the pandemic.

Another approach is to look at themes for companies that have done well when the market as a whole does badly. While US markets could be approaching a top, London’s AIM peaked in Sept 2021 at 1,310, versus 815 currently. Below I’ve used ShareScope to show the top performers even as the index itself has disappointed (finally troughing at 620 in April 2025).

Since Sept 2021 the only Industry in positive territory is Basic Materials (ie mining and oil, and within that Precious Metals and Mining sector) up +49%. Individual names such as Empire Metals, Metals Exploration, Borders & Southern Petroleum, Rockhopper and Strategic Minerals are all resource extraction. The only stock I own in that list above is MS International, the defence group, which I bought well before the pandemic. Below we can see that 7 AIM sectors, including Retail and Media have had a terrible time, down -60% or more. Even though the Nasdaq 100 is up +60% since Sept 2021, the AIM listed Technology sectors has struggled, down -40%.

The fact that EEE and MTL followed very different paths to multi-bagger glory suggests that success was idiosyncratic. Metals Exploration was heavily indebted with $111m of net debt in 2021 (only just below the previous FY revenue of $122m) and management had struggled with high fixed costs to generate profits from their Philippines based Runruno gold project. So, on top of financial leverage the gold mine was also operationally geared. MTL was operating a marginal business model when the gold price was below $2,000 an ounce. However, that high fixed cost base and paying down debt delivered impressive increases in profit as the gold price rose.

Other stocks on the top performers list are Filtronic, up +1510%, the second best performer here, which I wrote about here. Yü Group up +613% below.

Yü Group helps businesses “shop around” and manage their energy contracts. There were some similarities with the business model of Utilitywise, which failed after some investors questioned the accounting policies (recognising revenue upfront for multi-year contracts). Both groups were trying to disrupt the B2B energy buying process. Understandably, investors had beaten down the valuation of Yü Group.

Thus, I take two general lessons from the analysis above: 1) Be open minded about sectors, if everyone else is avoiding speculative miners, it doesn’t take much to keep up a passing interest. 2) Pay attention when beaten down sectors start announcing positive news and ahead of expectations RNS’s.

The two most hated sectors I can think of at the moment are marketing (SFOR, SAA, NFG) and litigation finance (BUR, MANO). If we start to see companies in these sectors beating consensus, then being open minded could turn out to be highly rewarding.

This week I look at SRT Marine’s latest maritime surveillance contract win and Craneware’s (SaaS US hospital billing) H1 Dec results. Although both are in the information and data business, I think they both have genuine “moats” and make an interesting case study in what might be difficult for AI Agents to disrupt.

SRT Marine $20.5m Contract Win

This Midsomer Norton (Somerset, UK) based provider of maritime surveillance systems (for governments) and maritime navigation safety systems (for boats and infrastructures) put out a $20.5m contract win announcement last week. That follows a January trading update, which saw H1 Dec group revenue up +96% to £51m and PBT +47% to £3.1m.

Their Maritime Domain Awareness (MDA) technology helps sovereign agencies such as Coast Guards and Fishery Authorities to track activity for maritime safety and security. Their navigation safety systems enable vessel operators to navigate more safely and efficiently. I don’t think they’ve said anything publicly, but I would imagine the rise of Russia’s shadow uninsured tanker fleet has been a commercial tailwind. So, you won’t find a button on their website saying “press here to track Russian tankers”, but SRT’s core business is selling the “eyes and ears” that governments use for that purpose. As the shadow fleet becomes more sophisticated at hiding, the demand for SRT’s high-end surveillance systems help “unmask” the dark fleet. Revenue is forecast to grow to £116m FY Jun 2026F, compared to £8.2m FY Mar 2022 – that’s an increase of 14x in 4 years.

The latest contract $20.5m win is with an existing sovereign customer, so a follow-on contract to expand the scope of existing work. Cavendish, their broker, say that timing remains unclear but says that there’s “good visibility” on £500m worth of contracts, within an impressive £1.8bn validated sales pipeline. There are no changes to forecasts following last week’s RNS, but presumably we can be more confident that FY Jun 2026F £116m revenue and adj PBT of £10.2m and FY Jun 2027F £123m revenue and adj PBT of £11m will be achieved. Worth noting that even with rapid revenue growth the margin is still less than 10%, so although the tech is impressive, this doesn’t seem to have operational gearing in the same way that a software platform does.

Valuation: Using Cavendish’s forecasts suggests EV/EVITDA of 18x both Jun 2026F and 2027F, with an price/sales of just below 2x. The PER ratio is 20x Jun 2026F, dropping to 19x the following year.

Opinion: Frustrated that I missed this. The shares fell below 20p in Jun 2024, down by -75% versus Jun the previous year. That does highlight the risk of lumpy contracts, SRT went on a hiring spree and invested in equipment, and the revenue didn’t come through until the following financial year. The group now seems to be on an “even keel”, and the technology looks both useful and hard to disrupt. However looking at the chart the shares are testing the 200 moving average, so might be worth waiting to see if the price fall through that support level?

Craneware H1 Dec results

There’s little sign of fear from disruption by AI Agents in the management commentary, with CEO Keith Neilson saying: “The US healthcare market continues to evolve at pace, and with each new piece of legislation or change, the need for data led insights and a secure and scalable technology partner grows. We have never been more confident in the vital role we play…“

Management have already announced a partnership with Microsoft, to implement AI through the group’s Trisus platform. Around 40% of US hospitals are customers, which spend almost a trillion dollars, so CRW costs are a tiny share of overall hospital operating expenses, the risk from switching to a more disruptive platform seem to greatly outweigh any cost saving benefits. In addition CRW software is hard-coded into the hospital’s financial ledger, so unlike a company like LSEG where company data is publicly available, Tirsus operates behind hospital firewalls. No LLM can “scrape” a hospital’s internal pharmacy spend and an agent can’t interface with a hospital’s billing system without the underlying protocols Craneware provides.

Acquisition: In June 2021, management announced the acquisition of Sentry Data Systems, which had a customer base of 10,000 hospitals, pharmacies and clinics, including over 600 US hospitals (of which only approximately 35% overlapped with existing Craneware customers). The $400m price represented 4.3x historic sales, and 17x EBITDA.

Valuation: Craneware shares are trading on 15x 2027F PER and 8.5x EV/EBITDA or 2.9x price/sales the same year. So the group’s current valuation ratios represents around half of the multiples they paid for Sentry 5 years ago. To be fair, Sentry does seem to helped them generate organic growth since 2022.

When Maynard looked at CRW in 2019, the PER had been as high as 60x and price/sales > 10x, so he worried (rightly as it turned out) about profits growing, but the multiples were too high and the shares being at beginning of a long term de-rating.

Given the mid 80’s gross margin, I was surprised to see 3 year average RoCE was just 4.5%. The cause seems to be the $400m acquisition Sentry Data Systems in 2021 and capitalised R&D spend being added to the balance sheet, which increases the “Capital Employed” denominator.

For comparison, Tristel the chorine dioxide medical device disinfectant group which also reported on Monday, has a gross margin above 80%, but reports ROCE above 20%, with an EBIT margin of 22%.

Opinion: There was an approach for Craneware from Bain Capital in May last year, at a price of £26.50 per share or a c. 30% premium to the undisturbed price. Although the current share price of 1530p is well below the Bain offer, my view is that management were right to reject the approach. It looks to me like CRW is in an “investment phase” at the moment, and we could see the benefits of that come through in 2-5 years time. Private Equity tend to buy companies when profits are suppressed by investment, then wait a few years and float companies back to public markets having starved those companies of investment and flattered profits. I’ve never understood why professional fund managers let P.E. firms do this.

I think Craneware (and SRT Marine for that matter) make an interesting case study on what AI Agents might not be able to disrupt. Clearly investors are sceptical at the moment of groups like LSEG, RELX and even RMV, but Craneware does seem to have a genuine “moat”. I don’t own any, but think the investment case looks reasonable.

Bruce Packard

@bruce_packard

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.