David Stevenson explores why UK equities continue to look undervalued, examines an AI-focused investment trust and assesses a new ETF targeting the infrastructure powering the AI revolution.

This month, we investigate why Fidelity thinks UK equities are cheap, an investment trust that is all in on the AI boom, and a new ETF that is laser-like focused on AI hardware rollout.

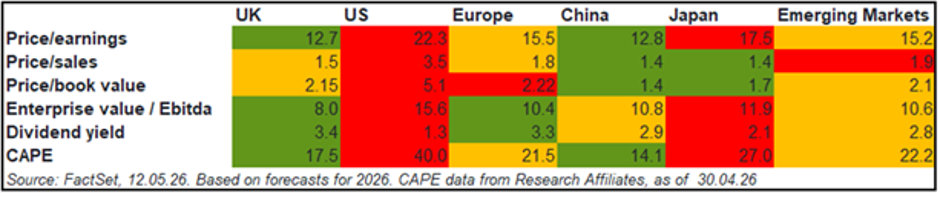

UK shares are cheap

I’ve long maintained that many UK equities, especially amongst internationally minded FTSE 250s and FTSE Small Cap stocks, are cheap – and ripe for PE deals. Easyjet, for instance, is just the latest in a long line of businesses that could be snapped up at what amounts to a bargain-basement price. And some investors think what’s true for Easyjet is more generally true for much of UK PLC.

Take Fidelity, which manages a very successful UK equities investment trust called Fidelity UK Special Values PLC, managed by Alex Wright. Fidelity has looked at a range of metrics that suggest UK stocks are really cheap – and US stocks much more expensive.

The table below provides a snapshot of how stock markets are valued worldwide. It brings together six commonly used measures that compare share prices with fundamentals such as company earnings and dividends. A lower number generally indicates a cheaper investment, except for dividend yield, while higher numbers suggest a more expensive one.

According to Fidelity, the picture is clear: the UK stands out as one of the cheapest markets across most measures. By contrast, the US is the most expensive by a wide margin. Crucially, using one of the most closely watched indicators, the cyclically adjusted price-to-earnings (CAPE) ratio, highlights this gap. The CAPE ratio is a more sophisticated version of the price/earnings ratio. It looks at a stock market’s profits from the past 10 years, takes an average, and adjusts it for inflation. A decade ago, UK and US markets were valued at similar levels. Since then, the gap has widened significantly, as US stocks – particularly in technology – have surged ahead.

According to Fidelity, although the FTSE 100 has shown signs of catching up, supported by sectors such as energy, mining and defence, “US valuations are climbing again following a bumper earnings season. While cheaper markets may offer opportunities, higher valuations often reflect stronger expectations for future growth. Markets such as the US and, more recently, Japan have attracted strong investor demand, pushing valuations higher. This leaves investors balancing two key questions: where markets look cheapest today, and where future growth is likely to come from.”

Forward price/earnings ratio

I rate highly Fidelity’s Special Values UK investment trust as well as Gary Channon of Phoenix, who manages the Aurora Investment Trust, which is a more disciplined, focused value-style investment trust with a very concentrated portfolio. That said, my own hunch is that the Small Cap market is especially strong, helping to boost returns for active fund managers of investment trusts such as Odyssean, Rockwood, and Onward Opportunities.

Gold’s wobbling

Gold is looking really very weak on technical measures. Last week, gold briefly broke below 4,000 dollars for the first time since November, then steadied near 4,050, marking its fourth straight weekly fall. The technical picture has now turned outright bearish: price sits below the 20, 50, 100, and 200-day moving averages, and, crucially, the 50-day average has slipped just beneath the 200-day, completing a death cross that reverses the golden cross that had defined the bull market. The 14-day RSI near 31 is close to oversold, which can precede short-term bounces, but momentum, the MACD and the moving-average stack all point lower.

The drivers are macro rather than physical: a firm dollar and a hawkish Federal Reserve, which markets now expect to raise rates as many as three times this year, have lifted real yields and the opportunity cost of holding a non-yielding asset, while the fading Middle East war premium has removed a safe-haven bid. In technical terms, support sits at the 4,000 psychological level and then toward 3,800. My own key target is that $3800 level – if that’s breached, I’d expect the next stop to be as low as $3000. But I’d also be a buyer on the way down. I would wager that this time next year, all the concerns about fiscal debasement will come racing back, with US interest rates heading down (not up) and geopolitical fears building, especially around China.

All in on the AI revolution: Manchester and London Investment Trust

Something extraordinary happened recently – Alphabet raised $80 billion in extra capital – presumably to finance its AI ambitions – and barely any of us noticed. The full $80 billion is less than 2% of Alphabet’s mammoth $4.6 trillion market cap, and around half of the total is an initial raise, with a $30 billion offering alongside the $10 billion from Berkshire Hathaway. The other $40 billion is a flexible drip-feed mechanism that can be used gradually over time.

I actually believe this to be a smart move by Alphabet, eschewing debt in favour of long-term capital and underscores why I think it’s the best play on the AI revolution currently sweeping markets. I’d be an enthusiastic buyer of the stock if not for its slightly elevated price at the moment – it’s trading at 28 times earnings.

My own view, for what it’s worth, is that the AI melt-up will last for longer than we all expect, but then, like Icarus, its hubris will catch up with it, and we’ll see the mother of all crashes. But I’m also happy to be proved wrong and accept that we may all be collectively underestimating the huge market opportunity in AI. In particular, I am quietly impressed with Anthropic and Claude, which I rate highly. I just struggle to see how it can make enough money to justify its possible valuation.

One person who categorically disagrees with me on this score is Mark Sheppard, who manages the Manchester and London investment trust. On paper, this is a global equities fund that also serves as a family vehicle. In reality, it’s aggressively bullish on the technology sector broadly and on AI specifically. Until recently, it was effectively a pure-play AI fund, investing the majority of its capital in just two stocks: Microsoft and Nvidia. The cynics might suggest avoiding paying the manager’s fee and buying these two stocks directly, but that argument no longer holds. In recent months, Mark has made some very big changes, cutting down those two holdings and significantly diversifying his tech stock portfolio, with a particular focus on the picks-and-shovels businesses behind the AI revolution, notably photonics businesses. He’s also said he’s very interested in buying Anthropic stock during its IPO.

Details: Manchester and London Investment Trust

· Fund Manager: Mark Sheppard

· Key facts: Ticker MNL

· Key shareholder: Manchester & Metropolitan Investment Ltd (manager’s family) 62.8%

· Discount 22.3% (above 52-week average)

· Market Cap £417m

· YTD Share price return 40.8%, Nav return YTD 32.4%, 5 year NAV returns 214%

· OCF: 0.91%

In the two graphics below, you can see the new look of Manchester and London fund holdings. NVIDIA is still in the top three with a 10% exposure, but Broadcom is in the number one slot, TSMC is at four, Photonics play Lumentum is at number 5, then AMD, SK Hynix, and Micron Technology.

The next graphic shows the portfolio’s active bets versus a benchmark, in this case QQQ, Invesco’s NASDAQ 100 tracker.

The big standout stock is Bloom Energy Corporation, a stock I know nothing about. According to online sources, Bloom Energy was incorporated in 2001 and designs, manufactures, and installs solid-oxide fuel cell (SOFC) systems that convert natural gas, biogas, or hydrogen into electricity via electrochemical reactions without combustion. This distinguishes Bloom from both traditional generators and from PEM (proton exchange membrane) hydrogen fuel cells used by competitors such as Plug Power (PLUG) and Ballard Power (BLDP). The Bloom Energy Server is the core product: a modular, scalable power generation platform deployable from 20 MW to 500 MW+ per site, with availability up to 99.999% (five nines). Historically, the company served hospitals, retail, telecom, and manufacturing. Since 2024-2025, the company has pivoted decisively towards hyperscale AI data centres.

Bloom’s stock has undergone one of the most dramatic re-ratings in US equity markets over the past 12 months, transforming from a perennially loss-making fuel cell manufacturer into the primary beneficiary of the AI data centre buildout in power infrastructure. The stock traded at $18.39 at its 52-week low and reached $322.83 at its 52-week high (a near 17× swing) before settling at $273.51 as of 2 June 2026, implying a market capitalisation of approximately $77.8B. To be fair, the revenue line does look impressive. Revenue grew 37.3% year-on-year to $2.02B in FY2025, gross margin expanded to 29% from 12% at the 2022 trough, and the company turned operationally cash-flow positive. Maybe one to look at in future letters!

My bottom line? Sheppard’s restructuring of his portfolio means he’s embracing a much more diversified basket of AI-related stocks. And be under no illusions, this is an aggressively AI-related portfolio. Polar Capital Technology Trust, for instance, looks much less benchmark agnostic, with the top five holdings consisting of Nvidia (8.9%), Alphabet (8.5%), TSMC (5.1%), Broadcom (4.9%) and Apple (4.5%). The true test for Manchester and London will now be whether this diversified portfolio can produce the results against, say, Polar Capital Technology.

New AI infrastructure ETF

Sticking with the tech bulls’ story, despite my worries about tech valuations, I think we are firmly in an AI-infused bull market that is now broadening to include many more sectors and geographies. As I’ve already said, I think it’s possible we might even see another year of positive momentum as the rollout proceeds. Personally, given my own risk appetite – I’m no spring chicken – I’m very cautious of having too much exposure to this clearly exciting space. But I also think that ignoring the AI infrastructure rollout, especially if you are a younger investor than me, might possibly be a disaster.

If you are willing to take on the bubble risk – I’m increasingly reluctant to do so – then the key task is to ensure you have exposure to the businesses that are making most of the money in this scramble. It’s obvious that this means the semiconductor companies, which are at the heart of the AI rollout. The Manchester and London investment trust does invest in some of these businesses, but it has a broader, AI-informed portfolio.

There is, however, an interesting, even more laser-focused alternative in the exchange-traded fund space. It’s an ETF recently launched by WisdomTree, with a strategy designed to provide investors with targeted exposure to companies enabling the development and scaling of the AI economy, including key companies beyond NVIDIA, such as SK Hynix, Lam Research, Lumentum and Vertiv. The ETF is called the AI Infrastructure UCITS ETF (WAGI). While it offers diversified exposure to companies enabling AI development, investors should consider risks such as sector concentration, valuation levels, and potential market volatility, especially given the current high PE ratios and rapid growth expectations.

AI infrastructure categories

As it’s an exchange-traded fund, it tracks an index, in this case the WisdomTree SemiAnalysis Artificial General Intelligence Infrastructure UCITS Index. The Index is designed to track the performance of global companies that enable, support, and power the artificial intelligence (AI) computing ecosystem and could serve as the foundation for developing artificial general intelligence. In this case, WisdomTree has partnered with SemiAnalysis, a leading independent research firm specialising in semiconductors and AI infrastructure, to design and develop the index. SemiAnalysis leverages its research insights to identify the companies best positioned to benefit from the scaling of AI infrastructure.

Fund details: the Wisdom Tree AI Infrastructure UCITS ETF

· The fund: Total Expense Ratio (TER) of 0.50%.

· Ticker is WAGI and WAGB (£), IE000XHZP7D3

· The ETF does not pay a dividend: its an accumulating fund

· Current AuM $16.6m

· Estimated forecast PE ratio 25.04

· Country exposure: US exposure 59.50%, Taiwan 19.16%, and South Korea 8%

WisdomTree AI Infrastructure UCITS ETF: Top ten holdings

· SK Hynix Inc – 4.72%

· Micron Technology Inc – 4.50%

· Advanced Micro Devices – 4.27%

· Samsung Electronics Co Ltd – 3.28%

· LAM RESEARCH CORP – 3.21%

· KLA Corp – 3.19%

· Nvidia Corp – 3.17%

· ASML Holding NV – 3.15%

· Intel Corp – 3.12%

· Applied Materials Inc – 3.08%

My bottom line? I can see this as a very useful way to build low-cost, diversified but focused exposure to the picks-and-shovels businesses currently making a fortune from the AI capex boom. Personally, I think it’s far too risky because I have serious concerns that we are in the midst of a historic asset price bubble.

That said, it’s very possible I am way too cautious, and if the capex boom continues to power ahead this year and next – a distinct possibility – then this very concentrated portfolio could be a real winner. These companies are not fly-by-night operators – many are highly profitable and poised to make even more profits over the next two years. Note the forecast PE ratio for the businesses in this portfolio: “just” 25 times earnings. We are far from the dot.com world of ludicrously overvalued businesses.

There are some other risks, not least it’s a concentrated portfolio heavily exposed to a cyclical sector. But for the right investor, it’s a clean, low-cost tracking way to buy into the AI boom without buying the LLM companies themselves.

David Stevenson

Twitter: @advinvestor

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.