Bruce Packard explores the debate between holding cash and inflation-protected bonds, alongside three contrasting investment cases. Companies covered include Accesso (ACSO), Gateley (GTLY) and ME Group (MEGP).

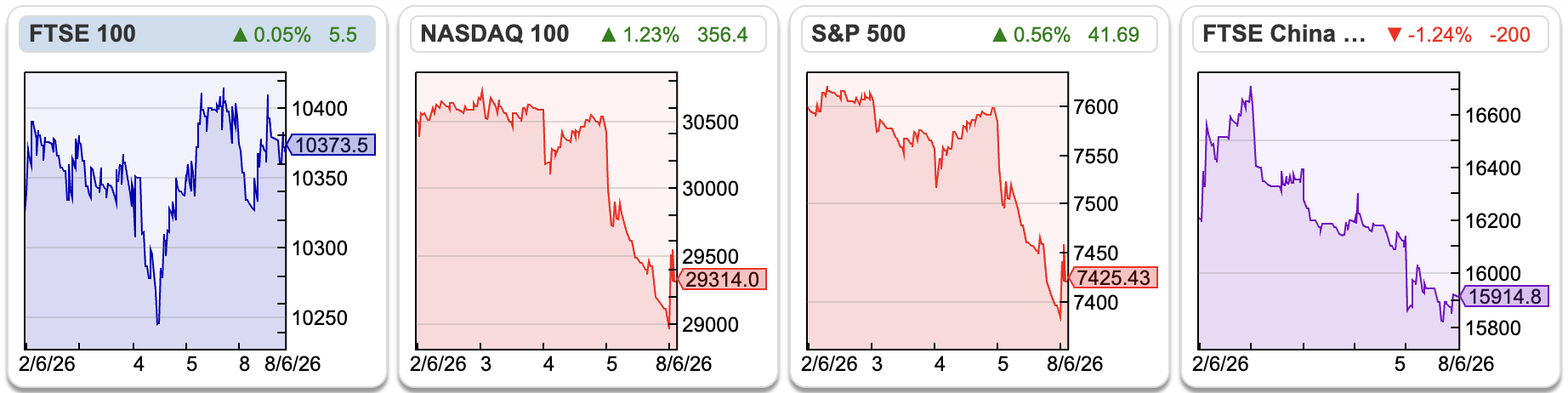

The FTSE 100 was up by +0.3% to 10,373 over the last 5 days. Both the Nasdaq100 and S&P500 sold off heavily last Friday, and were down -4% and -2% over the last 5 trading days. Bitcoin continues to fall, and is now down -27% YTD, while gold is flat YTD at $4,320, though also down -20% from its peak earlier in the year. Copper, on the other hand, is up +12% YTD. That implies the strength of US equity markets is based on fundamental economic activity, rather than liquidity driven price appreciation. Strong non farm payrolls numbers for May suggested that the Fed may even start raising interest rates at some point.

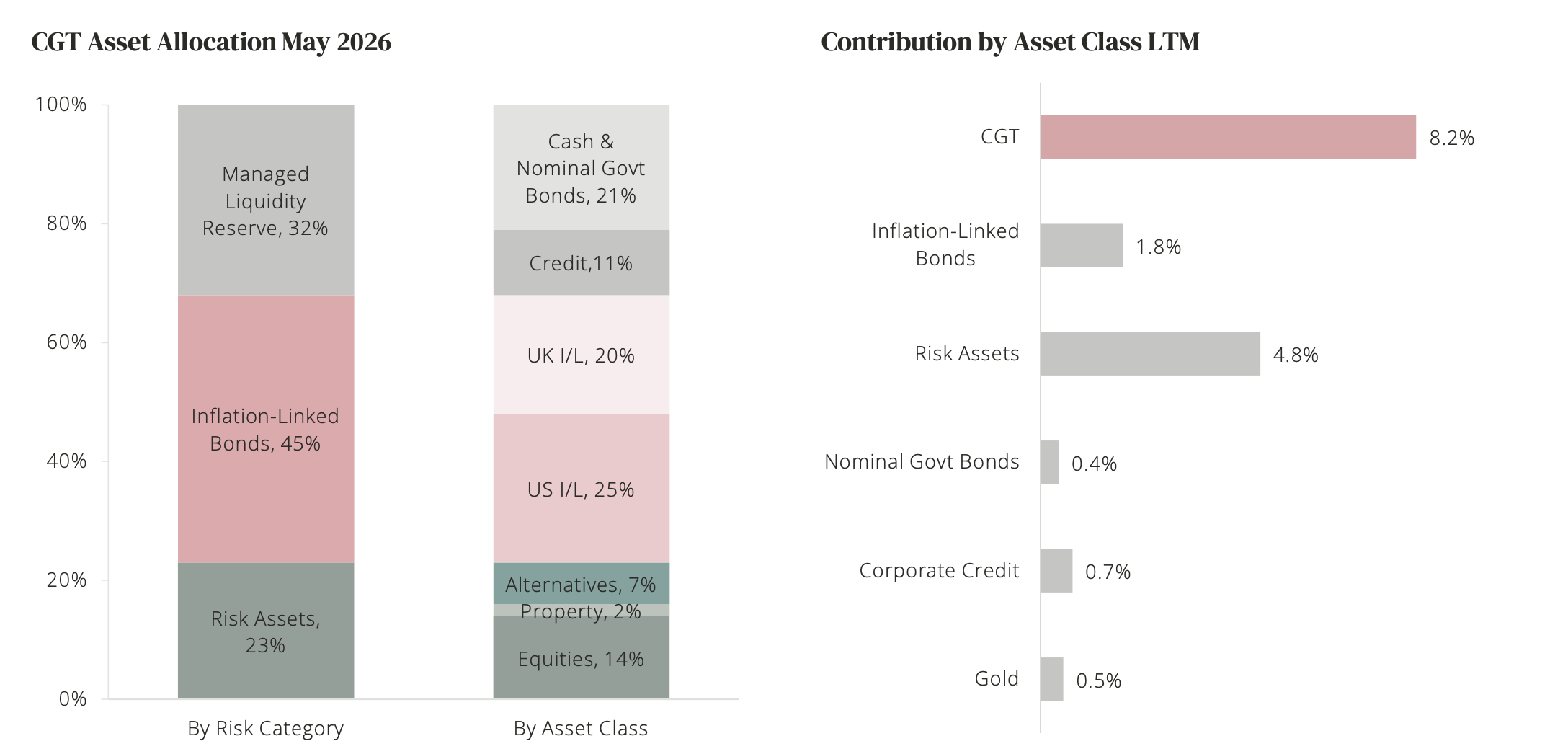

Hopefully everyone had a great time at Mello. My personal highlight was Paul Hill’s talk on takeover candidates that started 8.30AM in the morning, and a poorly attended presentation by Capital Gearing Trust. They were competing against Christopher Mills, who filled the big room, but I was curious about a trust that had around half of its assets in medium duration inflation protected government bonds. This sparked a lively conversation in the bar afterwards, about which “financial regime” it is better to own inflation linked bonds versus a cash ETF, and why long duration inflation linked bonds had performed so badly in 2022, when Putin’s invasion of Ukraine caused unexpected inflation and interest rate rises.

This week I look at legal firm Gateley, which is profitable and growing, but struggling to generate cashflow, plus Constellation Software’s disclosable stake in queuing software group Accesso. I start with ME Group, which had a nasty profit warning last week.

ME Group H1 April Profit Warning

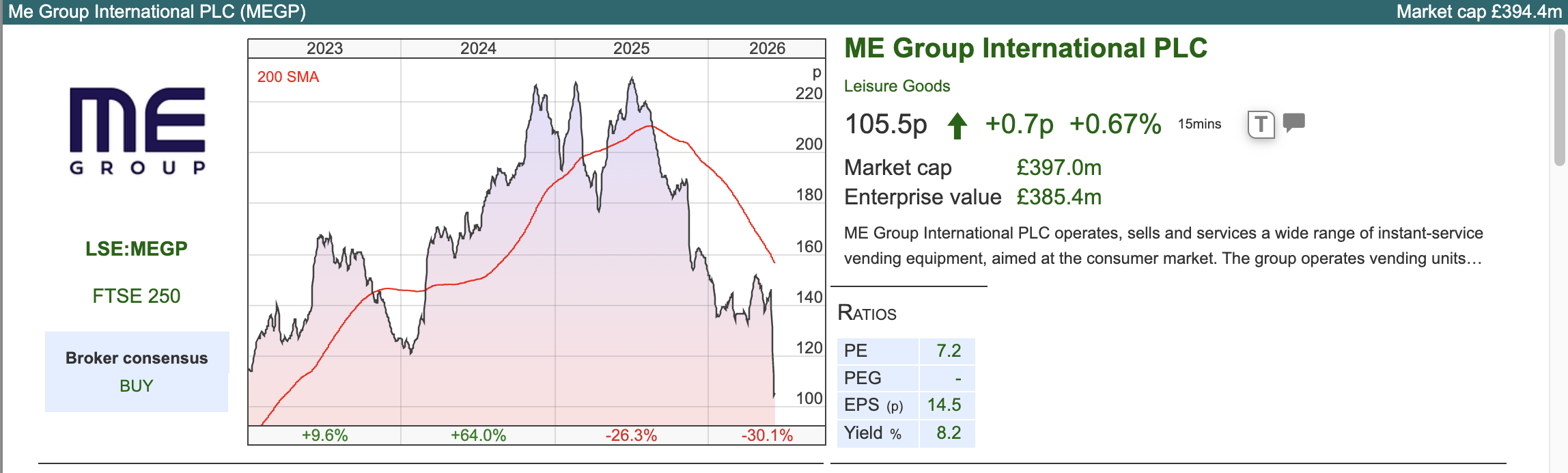

This photo booth to laundry and other vending machines Group put out a nasty profit warning, with the shares down -26% on the morning of the results. Their FY Oct 2025 results were announced at the end of March, when they said performance was in line with expectations for FY Oc 2026F: ShareScope shows +3% revenue growth and +8% EPS growth. So April, the final month in their H1, has been very disappointing with Photo.ME revenue down -17%. Wash.ME revenue up only +3%.

They blame the disappointment on lower consumer confidence due to ongoing conflict in the Middle East, particularly in France.

The other services are Print.ME (digital printing kiosks), Feed.ME (food vending machines), Amuse.ME (Children’s Rides) and Copy.ME (photo copying).

Balance sheet: There’s no mention of cash in the RNS, but net cash was £26.5m 31 Oct 2025, but since then they launched a buyback of £18m. Intangibles are £27m, as they bought a competitor (APS) which had 116 photobooths. Intangibles are still only 13% of shareholders equity, so the balance sheet shouldn’t be a concern. However, ShareScope shows poor FCF conversion and FCFf has been on a declining trend as the group has invested in capex to expand overseas and roll-out its laundry business in Continental Europe.

Serge Crasnianski, who is in his 80’s, the CEO and Deputy Chair still owns 36% of the shares. He originally founded KIS in 1963 (which was acquired by Photo-Me in 1994). Both Vlad Crasneanscki, the Deputy CEO plus Head of IR and Tania Crasnianski, another family member are also on the Board. The slightly different spelling is down to transliteration of the family’s original Slavic name into French and English documents, according to the LLM that I asked. Schroders own more than 10%, while Fidelity and abrdn both hold more than 5%, so the family influence hasn’t put off institutional shareholders.

Valuation: The shares are trading on a PER of 8x Oct 2026F, dropping to 7x the following year. On an EV/EBITDA they are below 3.5x.

Opinion: Using ShareScope to look at the chart history back to 1994, does show steep share price declines when consumer confidence comes under pressure. The share price collapsed -95% after the internet bubble burst, -90% during the financial crisis then fell by 2/3 at the start of the pandemic. So this is more sensitive to consumer spending than I would have first thought. WH Smith also made cautious outlook comments reflecting the impact on passenger numbers and weaker consumer confidence at the end of April.

I’m not going to catch a falling knife at this stage, but I wonder if other groups selling to UK and European consumers have also experienced a very difficult April, but have yet to update the market as they are hoping performance improves over May and June.

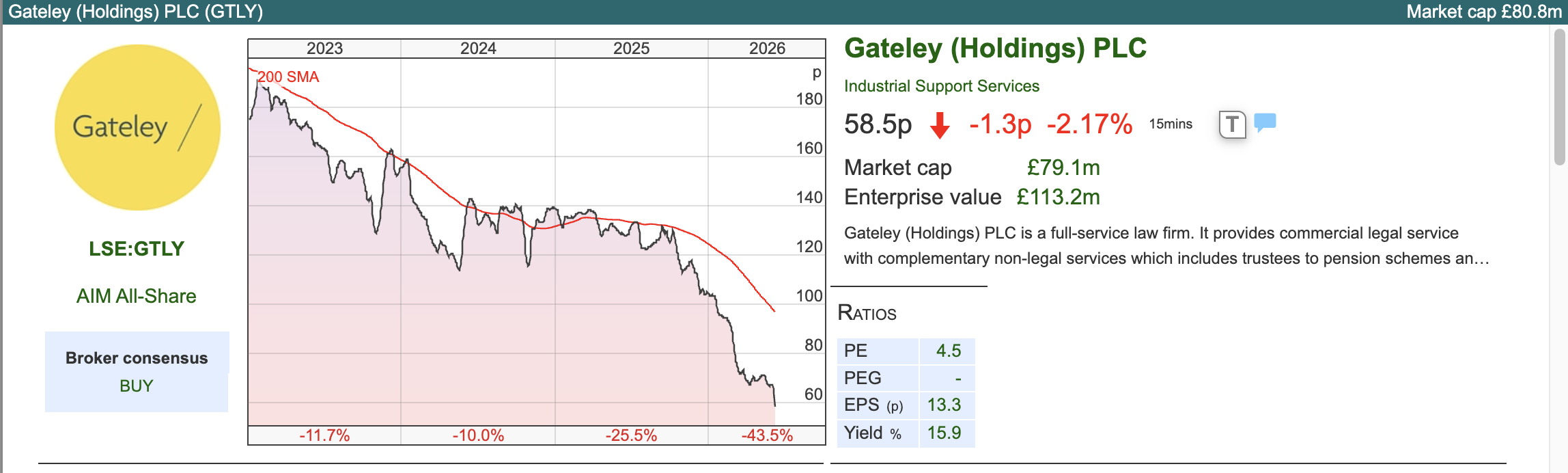

Gateley FY April Trading Update

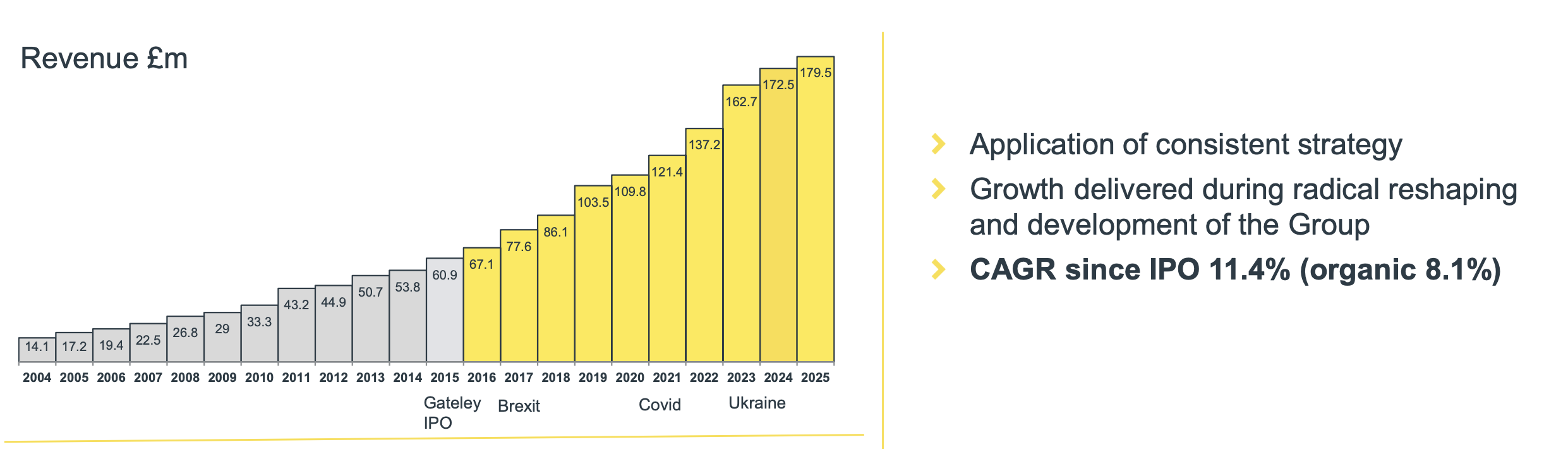

This law and professional services firm put out a trading update say FY April 2026 revenue should be up +7% to £193m, with underlying operating PBT of between £21-£22m. They say revenue is ahead of expectations and the profit figure is inline – at the H1 stage they gave consensus as £189m and £24m, so on their own measure of PBT that could be a c. 10% disappointment. Net debt ex leases was £25m (versus £7m Apr 2025). An inline update for a company trading on less than 5x PER can often be taken as a positive; however in GTLY’s case the shares were down -12%.

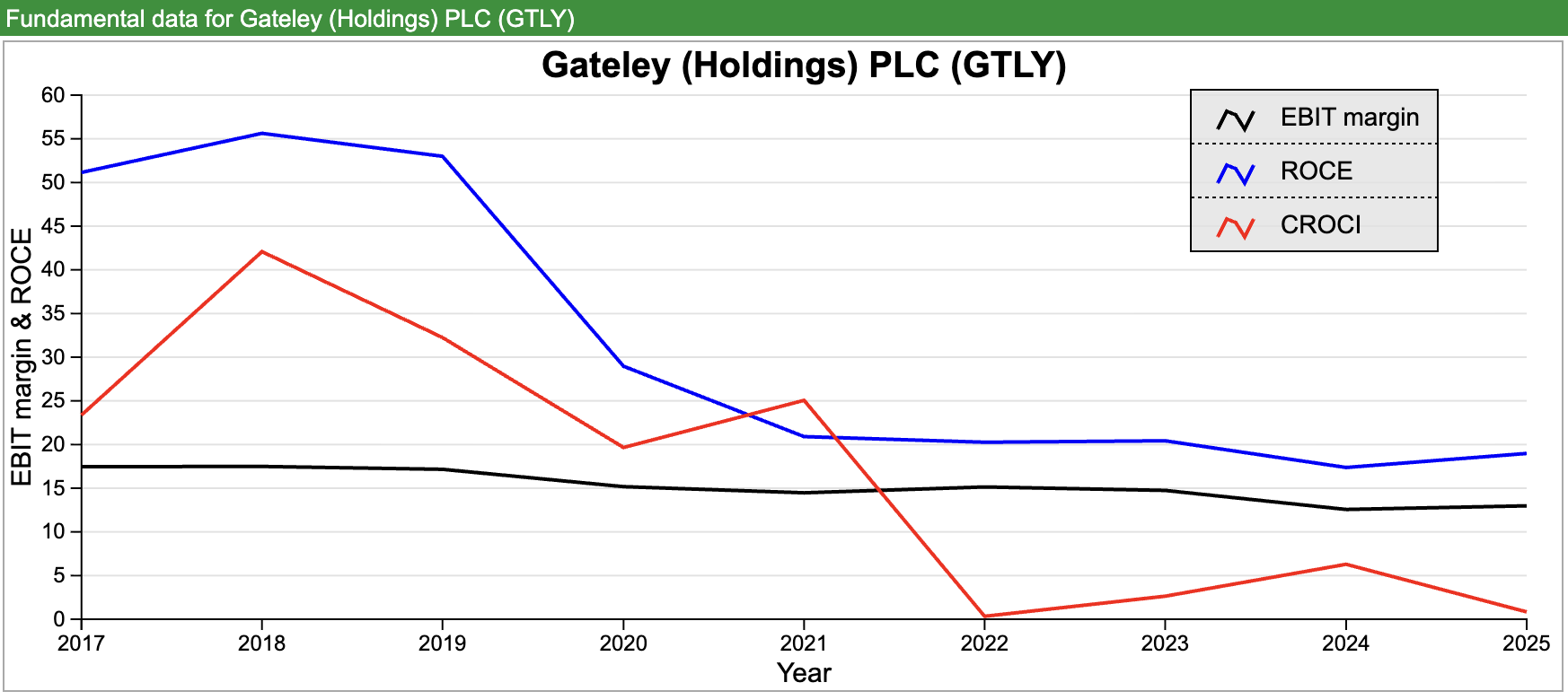

Events in the Middle East and the change in medium term interest rate expectations have meant transaction volumes have slowed in property and corporate sectors. They’ve also targeted work in “contentious” matters, perhaps seeking to take advantage of RBGP’s problems, but this has resulted in significant contingent unbilled time. They say that this is an attractive area from a margin perspective, but that does of course rely on successful outcomes. The commentary says management are focused on margin improvement from 11.1% FY April, yet fail to re-iterate that they are on track to achieve 13.5% near term margin target, which was a bullet point in their H1 results, which came out in December. The ShareScope chart below shows that EBIT margin has declined from high teens a decade ago to low teens. Profitablity measures like RoCE and particularly CashRoCI have deteriorated badly.

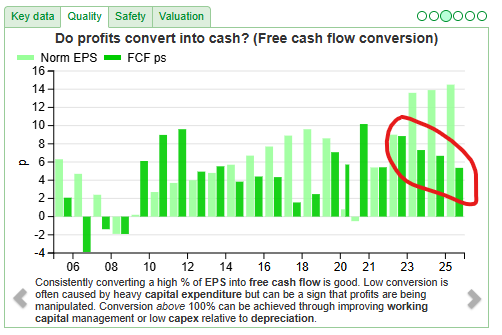

Balance sheet: Originally I thought that the acquisitions had led to a large increase in goodwill in the capital base but only £14m (20%) of shareholders’ equity (£71m) is goodwill. I was also surprised to see total assets at H1 were £159m, given that a law firm has very little Plant, Property and Equipment. Over half of the balance sheet consists of Contract assets £32m and £71m of Trade and other receivables. The former is time that fee-earners have already spent on a case, which has been recognised as revenue in the P&L, but not yet be invoiced. Add to that, receivables are high because people are slow to pay their lawyers after they’ve been invoiced, so the margins might be attractive, but the cashflow poor.

So Gateley’s capital employed expanding not because of goodwill from acquisitions, but due to unbilled time and unpaid invoices becoming an increasingly large component of capital. Indeed, ShareScope’s quality tab shows a 19% RoCE but FCF conversion at just 25%.

Valuation: At the half year the Board approved a 3.3p H1 dividend, paid in March. The total dividend is 9.5p, so with a yield above 16% the market is signalling scepticism. The PER is below 5x for Apr 2027F, and EV/EBITDA below 3.5x.

That looks optically cheap, but having got Manolete wrong last summer, I’m reluctant to flag this is “good value” with a high conviction. In this sector “cheap” can be “cheap for a reason”.

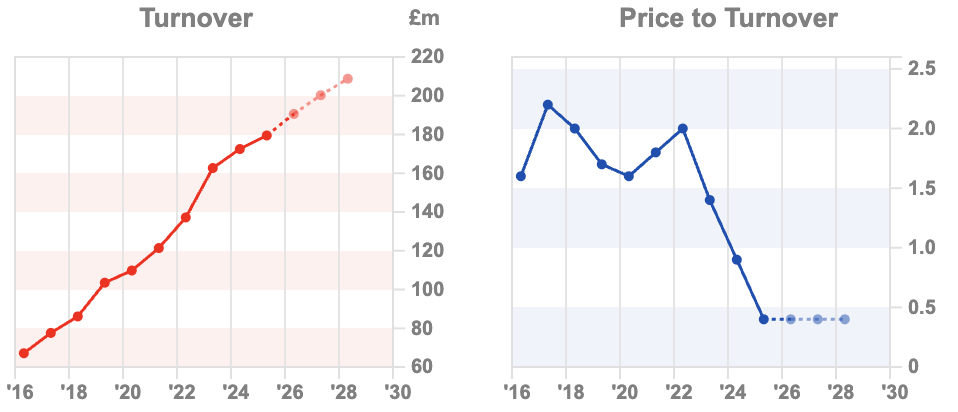

The chart above shows that this is yet another AIM listed group with a growing revenue line but a de-rating from over 1.5x sales to 0.5x.

Opinion: There’s little value for shareholders if management are growing revenue, but that isn’t converting to cash, which is what the charts above are signalling. The most recent TR-1 announcement shows Octopus have been selling.

This looks to have decent margins and growth, so I would imagine if management can fix the cash conversion, we would see a very strong re-rating – it’s hard to think of many 19% RoCE businesses growing turnover, but trading on a PER of 5x.

Accesso Constellation Software TR-1

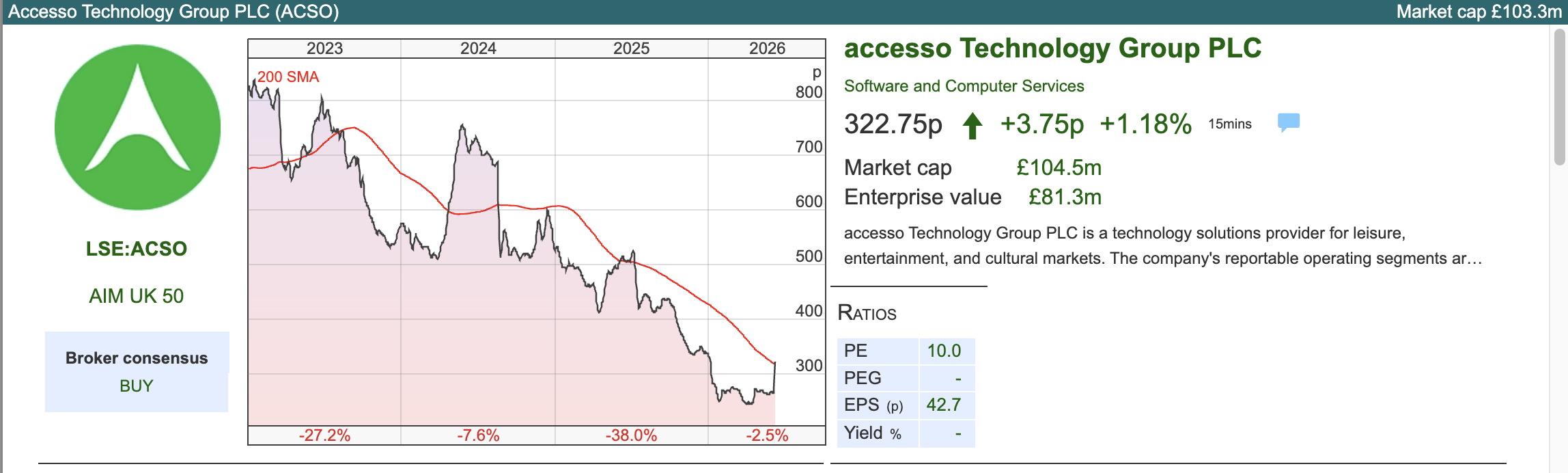

Some sharp-eyed investors spotted that Accesso, the ticketing and queue management technology group, released an RNS showing that Constellation Software, C$62bn market cap Canadian software company had bought a 3.2% stake in them. That triggered a +22% rise in the ACSO share price last Friday.

ACSO was one of the best performing shares on AIM for the decade following the financial crisis, rising over 100x between 2008 and 2018. The shares then sold off heavily just before the pandemic, before bouncing hard when the previous Chief Exec returned and investors realised that the group would benefit from customers implementing contactless solutions and capacity-management tools. Then pressure on disposable incomes led to another plunge: Accesso relies on transaction volumes so less money in consumers’ wallets directly impacts the group’s revenue. The long term share price chart looks like a wild roller coaster ride.

The most recent set of ACSO results were FY Dec 2025, released at the end of March, showing revenue growth +2% to $155m, and statutory PBT +38% to $14m. They had $30m of net cash. Steve Brown, the returning Chief Exec, who had left in 2018 and rejoined in 2020 to stabilise the business, confirmed this March that he would step down, to be replaced by Lee Cowie, in an orderly transition.

Outlook: Management said in March that the group was trading in line with expectations (approximately $146m of revenue and $20m cash EBITDA) which would imply -6% fall in revenue and -13% fall in cash EBITDA. They did flag that problems in the Middle East might put around $5m of revenue at risk, though of course, we also saw that ME Group suggesting French people visiting their laundry sites less often because of the knock-on effects of the conflict.

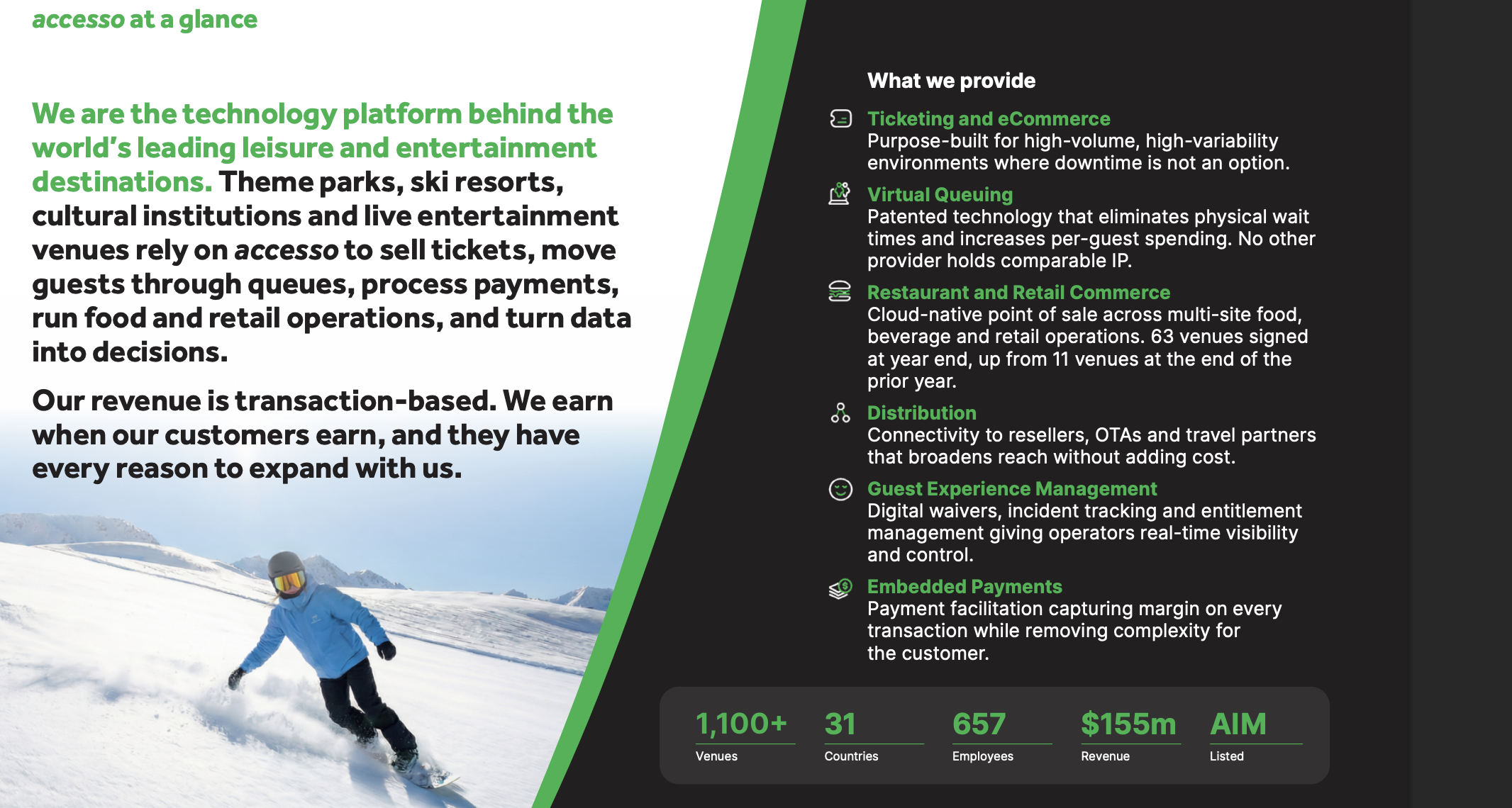

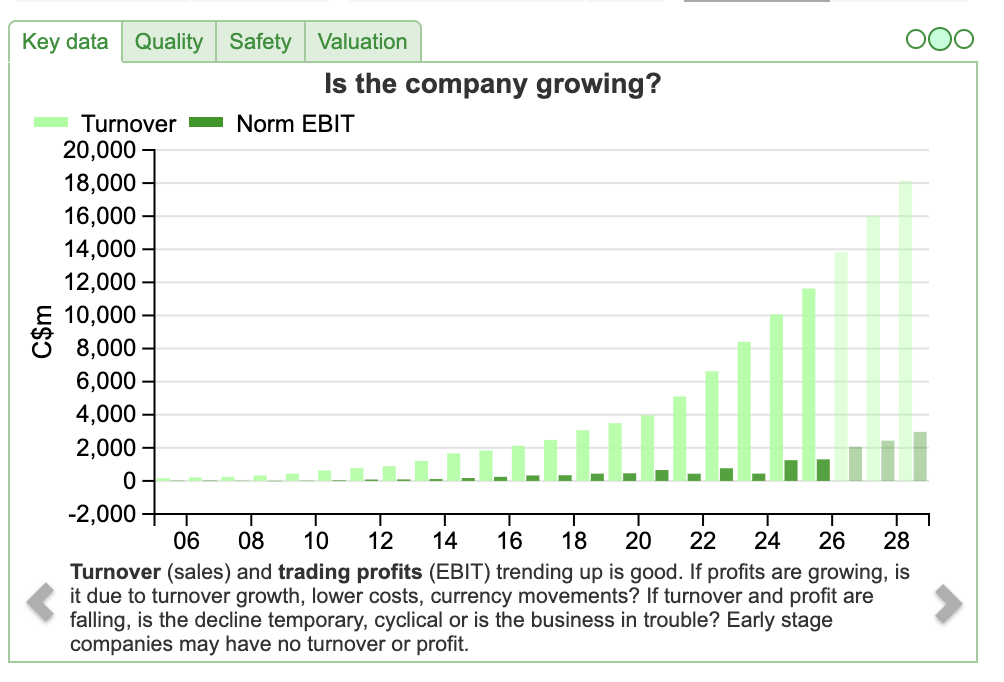

Constellation Software: Constellation (TSX.CSU) strategy involves acquiring “mission critical” software in niche area’s with customer. Accesso’s ticketing, virtual queuing platforms are embedded into the infrastructure of over 1,000 theme parks, ski resorts, and other venues, so the switching costs would be high, which would make them an attractive target for the Canadian group. It seems unlikely that Constellation would take a 3% stake in Accesso without eventually making a bid for the shares or creating value in some other way. I had a look on their website for an investor presentation, but Mark Leonard, Constellation’s founder and president, doesn’t like powerpoint presentations – instead preferring investors to read his letters. I rather like this “voluntary disclosure” approach, as thoughtful essays on corporate finance, capital allocation and organisational bloat can give a much better understanding of the investment case than graphics and diagrams. The chart below shows Constellation’s long term track record.

Valuation: Following the +20% share price jump, Accesso is now trading on a PER of 11x Dec 2026F, dropping to 10x the following year. That translates to an EV/EBITDA of just 5x and a price to sales of 1.2x. That looks cheap for a software group, though of course revenue is declining year on year.

Opinion: Looks like an interesting situation. I’m rather surprised that Constellation didn’t just make an approach and offer a 30-40% premium, instead acquiring a stake just above the disclosable threshold. One aspect to note is that ShareScope’s quality indicators show management have struggled to generate double digit RoCE and CashRoCI – and an EBIT margin of below 10% is disappointing for a software platform. So Constellation might be able to buy this and reduce central costs to improve returns and margins.

Bruce Packard

@bruce_packard

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Inflation protection: The most cautious seems to be TI5G – short duration 0-5y US TIPS hedged from $ to £. ShareScope says Yield is 5.9%. Longer duration has high risk of falls on rising interest rates. The only risk from TI5G seems to be if US inflation is below UK inflation.

The ultimate caution?

Thanks Lawman. Yes, short duration inflation protected bonds are less sensitive to interest rate rises than longer dated ones. These short duration assets will behave in a similar way to cash in most scenarios, but will likely outperform when the Fed let’s the economy “run hot”, that is inflation above target, but doesn’t raise interest rates to slow activity.

Bruce