Seven companies pass Richard’s minimum quality filter, but only two of them impress. He takes a closer look at RELX, a company that has earned an impeccable reputation selling information, data, and tools to insurers, scientists and lawyers.

5 Strikes

Since my last update, at least seven companies have published annual reports and passed my minimum quality filter, but only two survived further scrutiny and achieved less than three strikes.

| Name | TIDM | Prev AR | Strikes | # Strikes |

|---|---|---|---|---|

| Centrica | CNA | 19/2/26 | ? Acquisitions – Growth – ROCE | 3 |

| Mondi | MNDI | 19/2/26 | ? Holdings ? Acquisitions – CROCI – Debt – Growth ? ROCE – Shares | X |

| Rio Tinto | RIO | 19/2/26 | – Holdings ? Acquisitions – Growth | 3 |

| IDOX | IDOX | 17/2/26 | ? Holdings ? Acquisitions ? Growth ? ROCE – Shares | 3 |

| Motorpoint | MOTR | 16/2/26 | ? CROCI – Debt – Growth – ROCE | 3 |

| IntegraFin | IHP | 9/1/26 | – CROCI | 1 |

| Click here for our 5 Strikes explainer | 04/03/2026 | |||

IntegraFin, a platform for financial advisers, is a company I’ve admired before. I hope to pick up the trail soon.

RELX is not in the table. Although it has published its annual report for the year to December 2025 and I have put it through the 5 Strikes process, its annual report publication has not yet been updated in ShareScope.

REL [? Holdings – Debt ? Growth]

With really big companies some of my benchmarks break down. RELX directors own a tiny fraction of the company, for example, (just over a tenth of one per cent) but RELX is a big company. Its market capitalisation of £42 billion means that even a tiny fraction is a lot of money.

Chief Executive Erik Engstrom is the most invested of the directors, which is not surprising as has held the role since 2009. For five years before that he was chief executive of Elsevier, one half of Reed Elsevier – renamed RELX in 2015.

I like to think a significant shareholding means executives have skin in the game. At a share price of £24, Engstrom’s 0.0773% stake is worth about £32 million. Is that a lot, or a little, for a man who earned the best part of £11.5 million in 2025? I don’t know, hence the question mark against directors’ holdings.

Judging by a profile published by the FT in 2024, Engstrom might not be motivated by money, or fame. An “unflashy” Swede, he flies economy and has only been interviewed once in his fifteen years as ceo.

“One of the great incrementalists”, he surprised analysts when he took charge by declaring a strategic review was unnecessary. He continued with a strategy of converting paper publications about risk, science, and the law into data, insights and tools. He also continued with the company’s trade show businesses.

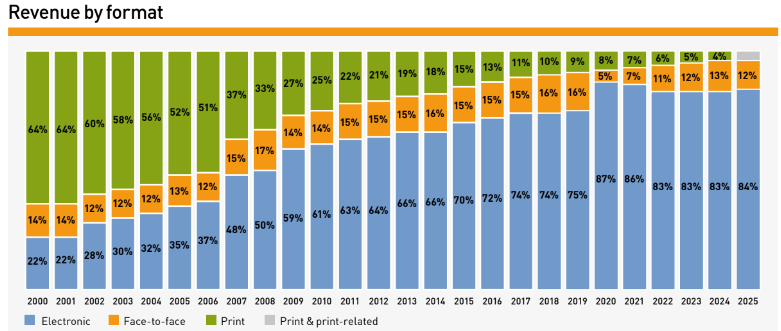

I imagine he likes this chart, from the annual report (year to December 2025):

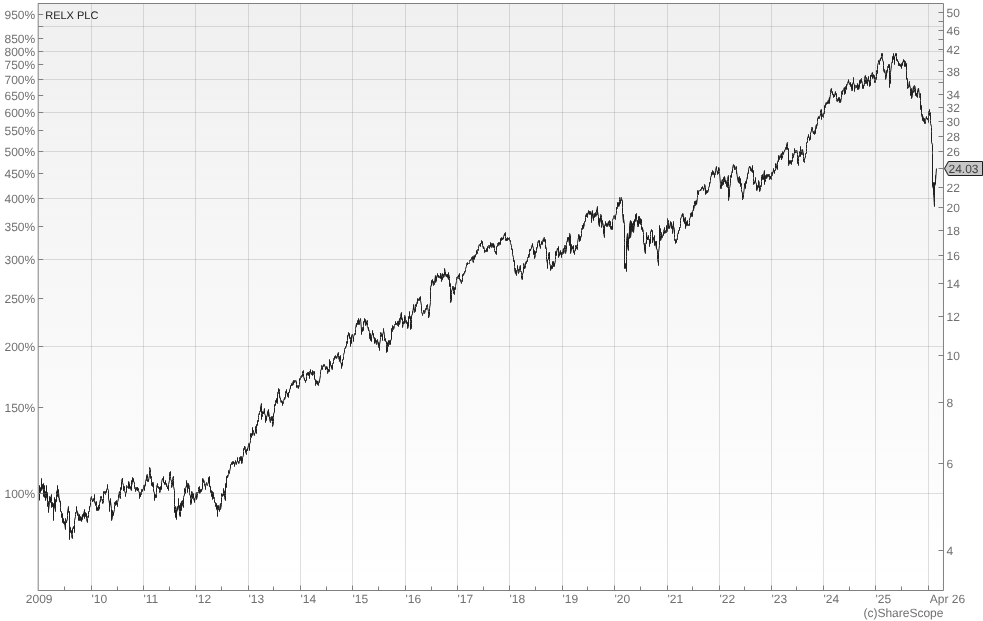

The result of incremental digitisation and incremental acquisitions was a behemoth that had made shareholders rich, although as so often happens when bosses and businesses receive plaudits, the nearly two years since have been more eventful for the share price.

The dramatic decline in the share price since early 2025 is not obviously related to the performance of the business.

RELX is heavily indebted in one sense. Debt, including operating leases, is 385% of capital, which earned the company a strike when I put it through 5 Strikes. The debt to capital ratio is also higher than it used to be but, in theory, RELX could pay the debt off in three years if 2025’s £2.5 billion free cash flow proves to be sustainable. Debt may not be dangerously high.

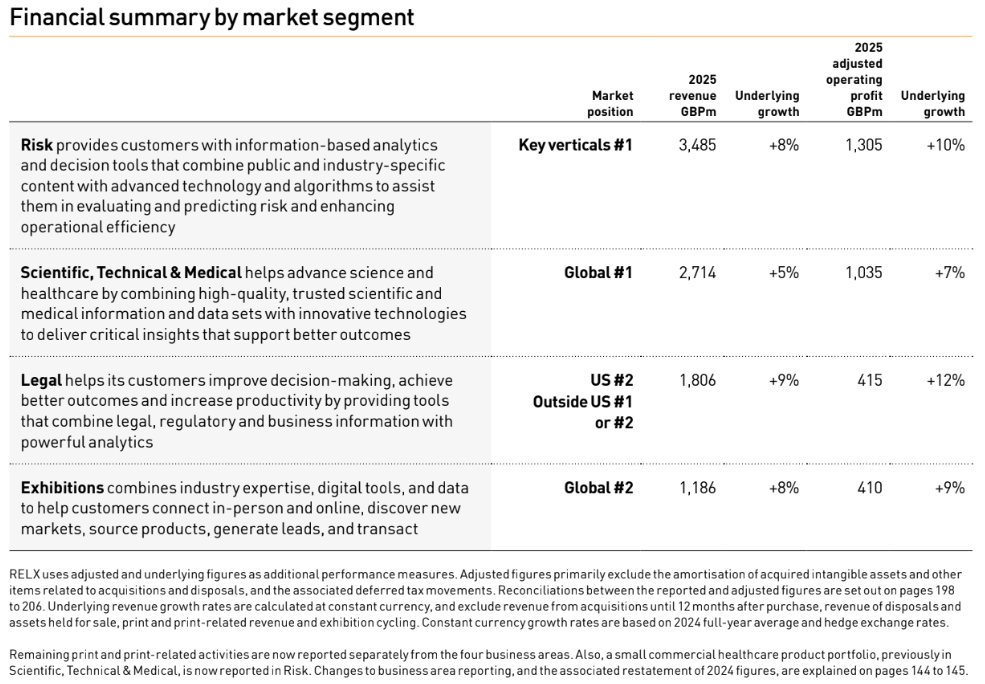

These assessments are, of course, judgments, based on the fact that RELX has been highly profitable and cash generative in the past and on the fact that I have heard of its famous brands (LexisNexis and Elsevier) even though I am not an insurer, lawyer or scientist. The company says it is number one or number two in its markets:

RELX has grown in seven of the last eight years and the one year it didn’t was the first year of the pandemic. We can see from the “revenue by format” chart above that the trade show business took a big hit that year and the year after, which was probably the main reason for the contraction and a bit of a one-off.

However, for such a profitable business RELX’s turnover growth is underwhelming. Although profit has grown more, Engstrom likes to keep “cost growth below revenue growth”, most years the growth in turnover has been less than 5% giving me the impression RELX is quite a mature business. The compound annual growth rate since 2018 is 3%.

Of course, it’s the future that matters. Some incremental improvements in recent years have involved generative AI. The FT profile from 2024 concluded by pitching RELX as an AI winner, having launched three generative AI products. In its annual report, the company anticipates growth, which we can see in the Sharescope forecasts. But traders are uncertain…

I must admit the idea of picking AI winners and losers makes my head go fuzzy. When I thought about spending some time getting to know RELX, I rebelled. The size and potential complexity of the business is overwhelming enough, let alone assessing the impact of a novel technology that I only have a layman’s knowledge of.

I am looking for companies with good track records, like RELX, that should be able to extend them with modest tweaks to their strategies. That is much easier to do with conviction, if the world around the company is not changing much. Stability, unfortunately, is a rare commodity these days.

The big lurch downwards you can see at the end of RELX’s share price chart was in early February this year, an event dubbed the Claude Crash. It coincided with the launch of a legal plug-in for Claude, an AI Large Language Model made by Anthropic. This is one of a number of catalysts that provoked traders last month to dump shares in a wide range of companies thought to be most at risk from AI. Investors sold shares in data and software businesses including RELX rival Thomson Reuters.

Whether companies like these benefit from AI, or fall victim to it depends on what makes them special.

As I understand it, two things make RELX’s businesses special. The first is the data, and the second is the technology layered on top that gathers insights and allows customers to use the data. The data and tools have been gathered and developed over decades, particularly in the Risk business.

In the scientific and legal domains, where the information is often in written form, modern generative AI is having a bigger impact. RELX’s standard products for legal research and insights is Lexis+ AI, which is “built and trained on one of the world’s largest repositories of accurate and exclusive legal content”. The AI component provides conversational search, summarises results and drafts legal documents.

The AI is “multi-model”, which means the company uses a range of suppliers – including the generative AI or Large Language Model (LLM) companies you have heard of like Open AI, Anthropic and Google Gemini.

In one sense this is encouraging. To make the next generation of information products, information gatherers and LLM developers need each other. In Lexis+ AI, RELX says it chooses the best model for each use case, layers it with other technologies (that I understand even less) to get the best results, relying on human evaluation to oversee the quality of the results.

In the data tools and AI implementation, RELX may have plenty of opportunities to continue to differentiate products and its vast experience and proprietary information should give it an advantage. The fact that it can choose between “multiple” LLM suppliers reduces the probability of it becoming dependent on one.

RELX’s likely modest equity stake in Legal AI startup Harvey, shows it is prepared to consider other futures. Harvey is, I believe, the biggest Legal AI Unicorn, with a reported valuation of $11 billion.

It too is multi-model, and its weakness was data until the two companies announced a strategic partnership to make LexisNexis data and tools available on Harvey. By embedding its legal library in Harvey, RELX says it is “meeting customers where they work”.

The tie-up also makes RELX a supplier and partner, perhaps a very important one. LexisNexis contains one of only two “must have” proprietary US legal libraries, the other being Thomson Reuters’ Westlaw. Thomson Reuters, has acquired a smaller AI startup.

I have focused on Legal information in my first look at RELX because I needed to focus on something to get a feel for the challenges and opportunities ahead. For now I am assuming the rest of the information part of the business faces similar challenges, and opportunities. Essentially AI startups are developing tools that may be able to rival RELX’s but they may also have to come to RELX for information and data.

That raises more questions. Over the long term, I wonder how effectively RELX can protect its data against LLMs that seem to hoover it up. If it increasingly becomes a supplier and partner to specialist legal AI companies, I wonder how much of the value it can keep for itself. If it is to compete, it must spend more on software tools, and that cost is rising.

Richard Beddard

Contact Richard Beddard by email: richard@beddard.net, web: beddard.net

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.