Recruitment agency SThree surprises Maynard Paton by appearing in a screen that hunts for asset-backed bargains. A notable cash position and a huge debtor book are the key deep-value attractions.

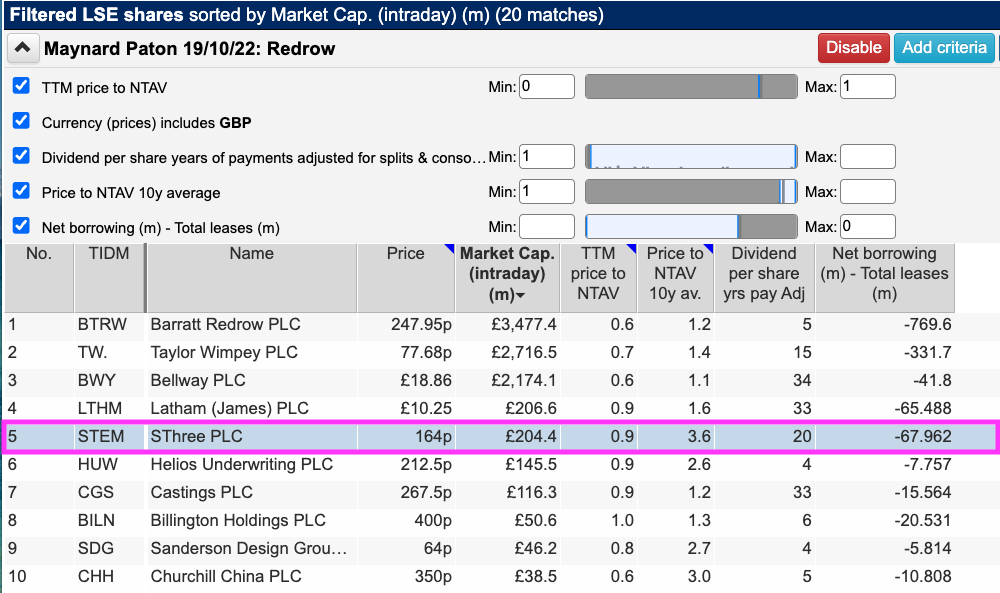

I am once again looking for ‘value bargains’ and revisiting a screen that identifies companies trading at less than book value.

Importantly, this screen attempts to avoid ‘value traps’ by demanding the shares offer net cash, dividend payments and a history of trading above book value.

The exact filter criteria I redeployed were:

- A price to net tangible assets of no more than 1;

- A dividend being paid during the most recent year;

- A 10-year average price to net tangible assets of at least 1;

- Net borrowings less total leases of no more than 0 (i.e. a net cash position excluding IFRS 16 lease obligations), and;

- A share price denominated in pounds sterling.

This time ShareScope returned 20 companies, including Castings, Churchill China and James Latham:

(You can run this screen for yourself by selecting the “Maynard Paton 19/10/22: Redrow” filter within ShareScope’s superb Filter Library. My instructions show you how.)

I selected SThree because I was very surprised to discover this recruitment agency was trading below book value alongside asset-heavy shares such as house builders.

But sure enough, SThree’s 164p shares were priced a fraction less than the group’s 172p per share net tangible asset value:

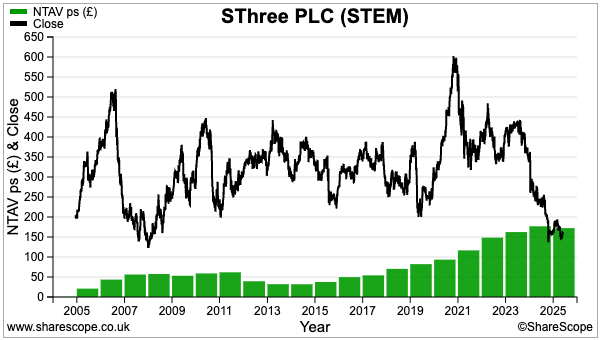

I see the shares have in the past traded at beyond 5x net tangible value.

Let’s take a closer look.

Introducing SThree

“I worked for a number of other companies and I saw more of what I didn’t like than of what I did. We thought generally we could do it better.”

So recounted Bill Bottriell during this Independent interview about why he and Simon Arber left their jobs in IT and recruitment to start their own business.

The pair invested £3,000 each during 1986 to establish staffing agency Computer Futures and set about trying to place IT workers into new jobs.

Companies House reveals early success, with the 1987 accounts showing revenue of £320k and a £91k profit. A tricky few years during the early 1990s recession were then followed by a sector boom as employers desperately sought IT contractors to handle the Year 2000 problem and the introduction of the Euro.

By 2000, revenue had soared to £302 million while profit had surged to £29 million. By that point Computer Futures was associated with other IT recruitment agencies backed by Messrs Bottriell and Arber, including Progressive, Real IT Resourcing, Huxley Associates and Mercer Gray.

All the agencies were reorganised under the SThree parent company during 1999 and today the group claims to be the “global STEM workforce consultancy” (STEM standing for Science, Technology. Engineering and Mathematics).

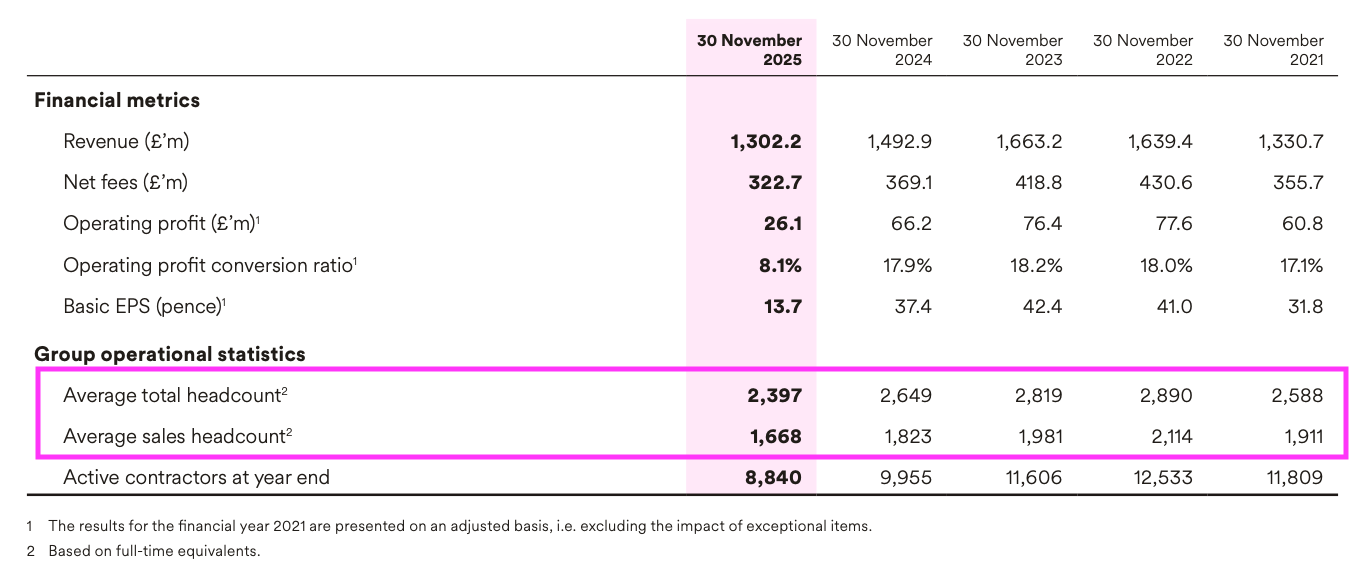

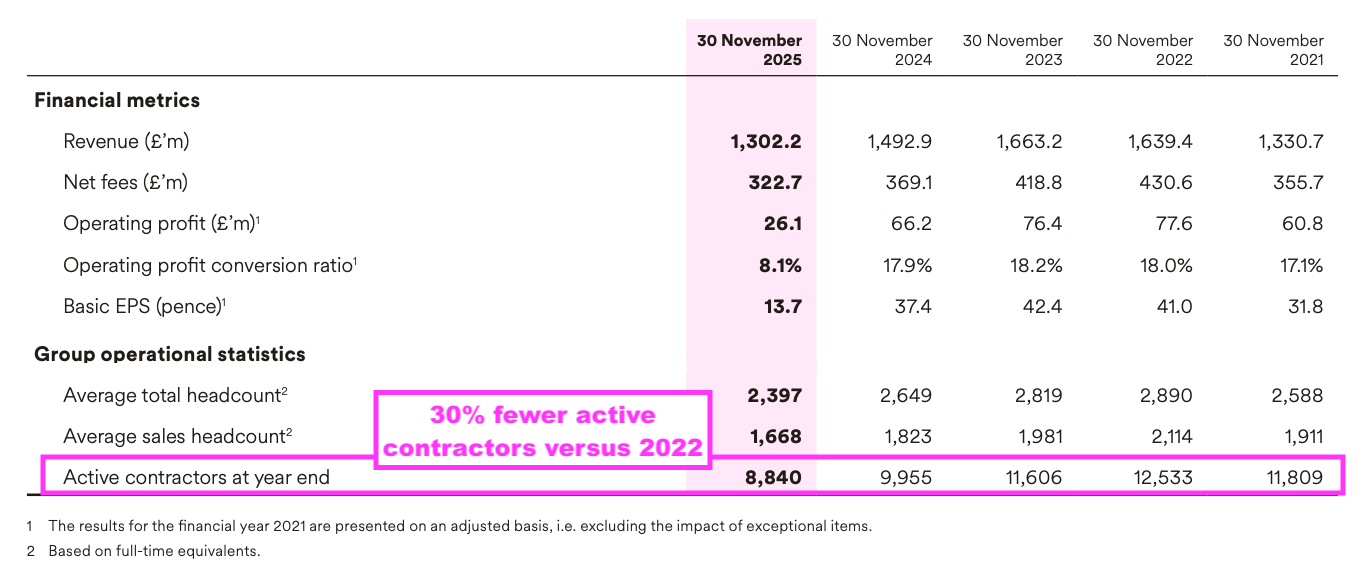

Last year SThree operated from 33 offices within 11 countries and placed 12,042 candidates with c6,000 clients within the IT, engineering, life sciences and financial sectors. The 8,840 contractors working through SThree last year enjoyed an average contract length of 60 weeks and an average contract salary of £107k.

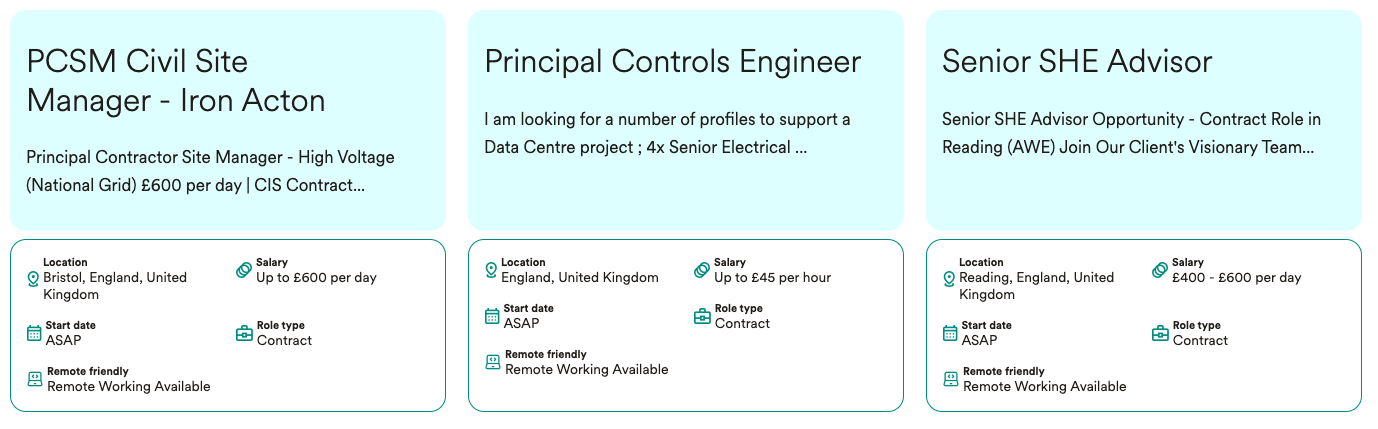

Roles currently available through SThree include a rail programme manager with pay up to £550 per day…

…a junior software engineer with pay between $80k and $140k a year…

…and a controls engineer with pay up to £45 an hour:

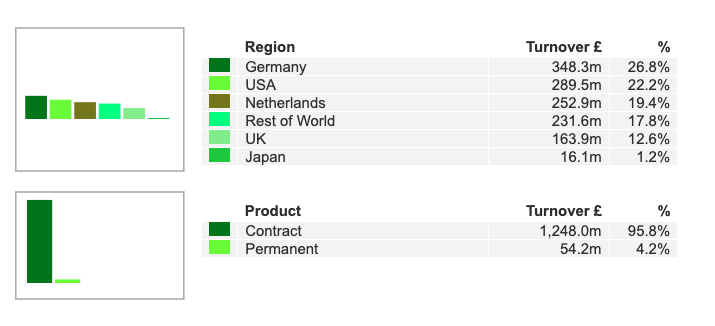

SThree’s largest markets are Germany, the United States and the Netherlands, and the group’s income is dominated by supplying contractors rather than permanent staff:

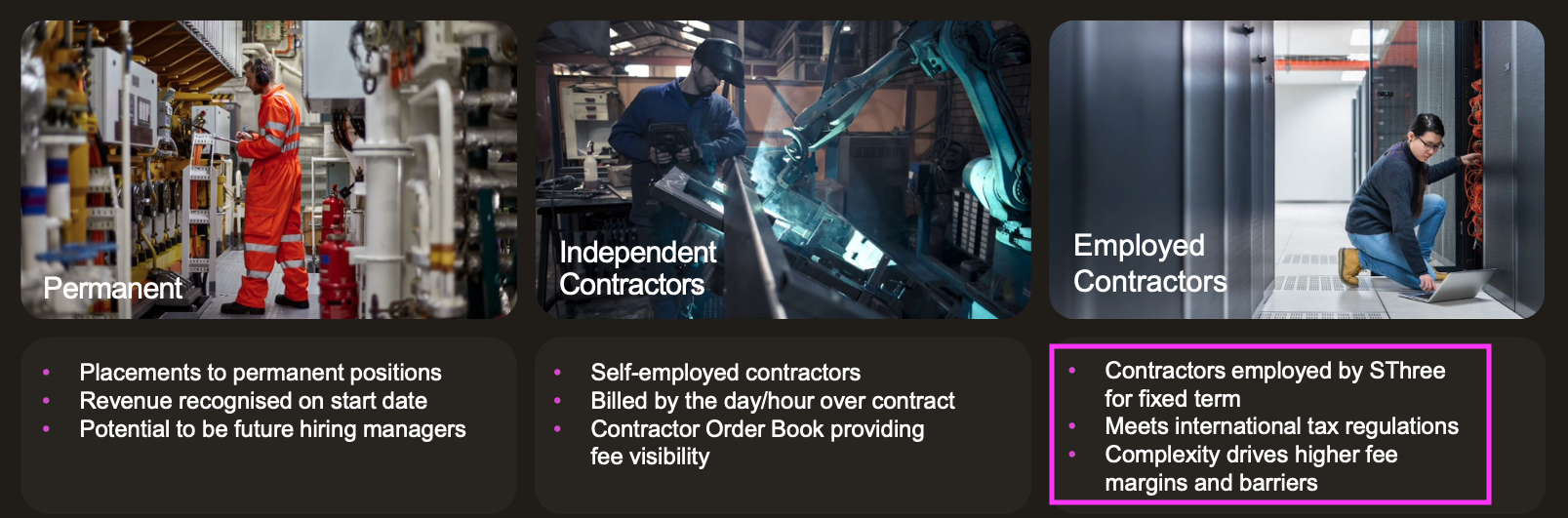

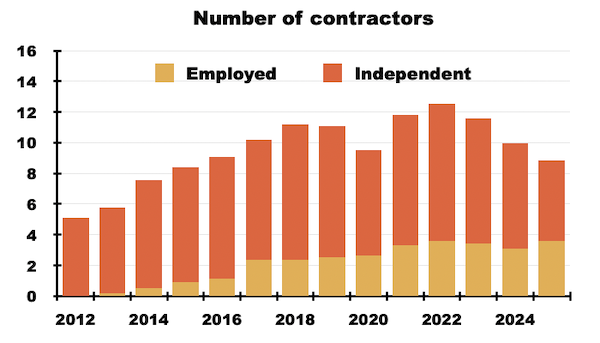

Note that SThree supplies contractors both through conventional ‘independent’ agreements, whereby the individuals placed are self employed, and through an ’employed contractor model’, whereby the individuals placed are legal employees of SThree:

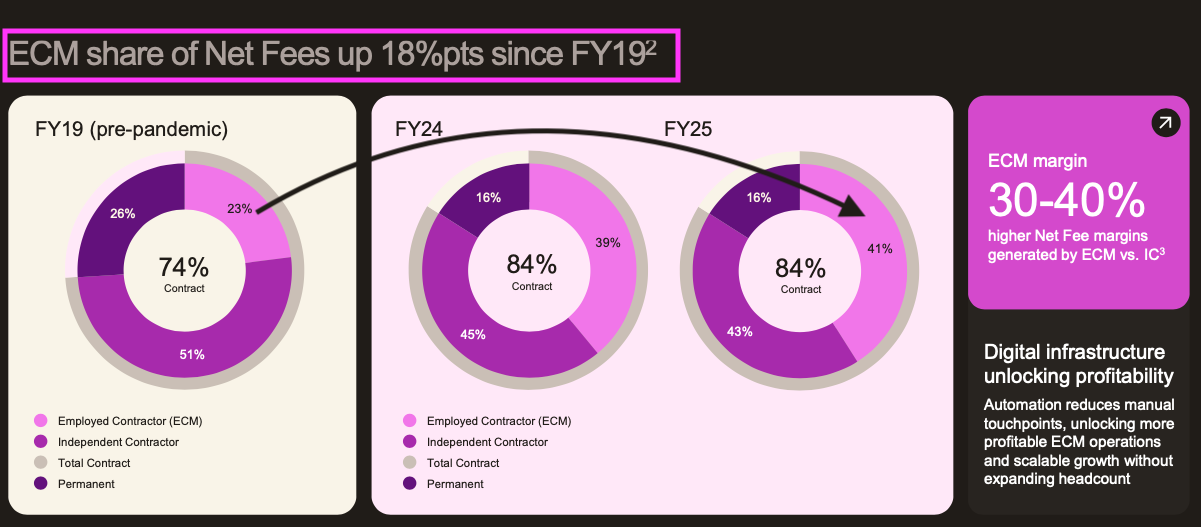

The proportion of fees from ’employed contractors’ has advanced over time:

SThree states ’employed contractors’ lead to higher margins and importantly, are employed on fixed terms that presumably match the lengths of their associated contracts.

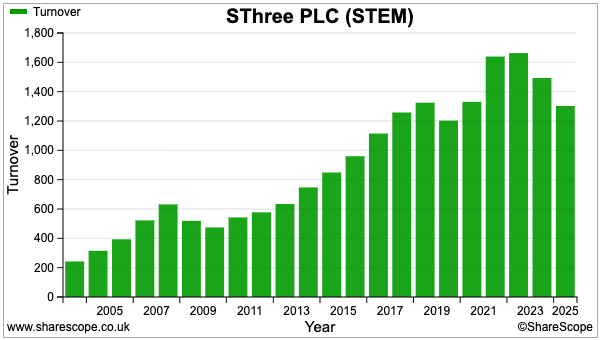

SThree’s revenue generally reflects the ‘gross fees’ billed to clients for the work undertaken by the contractors, and last year declined 13% to £1.3 billion:

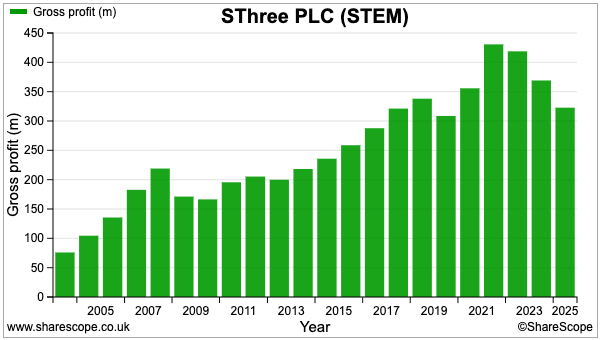

Gross profit meanwhile represents ‘net fees’ — or SThree’s share of the billings generated by the contractors — which last year declined 13% to £323 million:

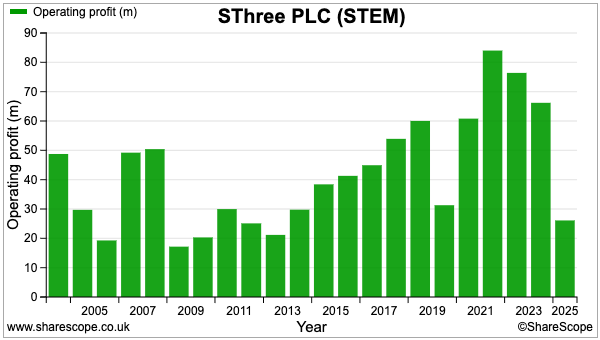

Last year’s lower revenue and lower gross profit in turn left operating profit down a thumping 61% at £26 million:

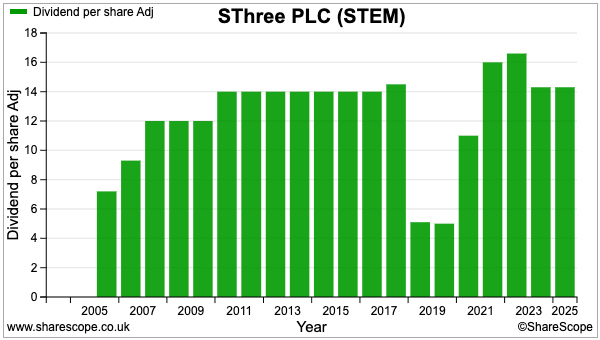

But at least the dividend was maintained:

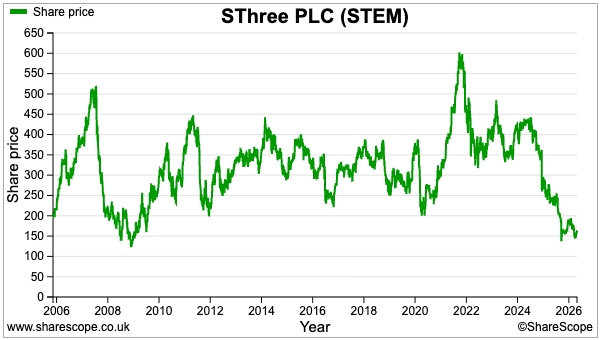

The profit collapse has sent SThree’s share price tumbling to levels last seen during the 2008 banking crash:

SThree joined the main market at 200p during 2005 and the recent 164p share price supports a £204 million market cap.

Balance sheet

Any potential book-value investment must start with the balance sheet. And SThree does not score too badly with its assets.

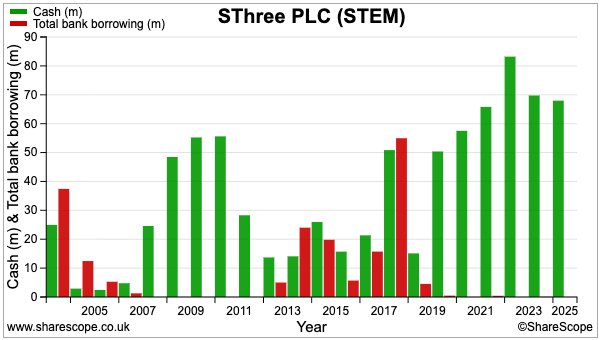

First and foremost, the group has operated with significant cash and minimal bank debt since 2019:

The £68 million net cash position declared for 2025 equates to approximately 33% of the recent market cap.

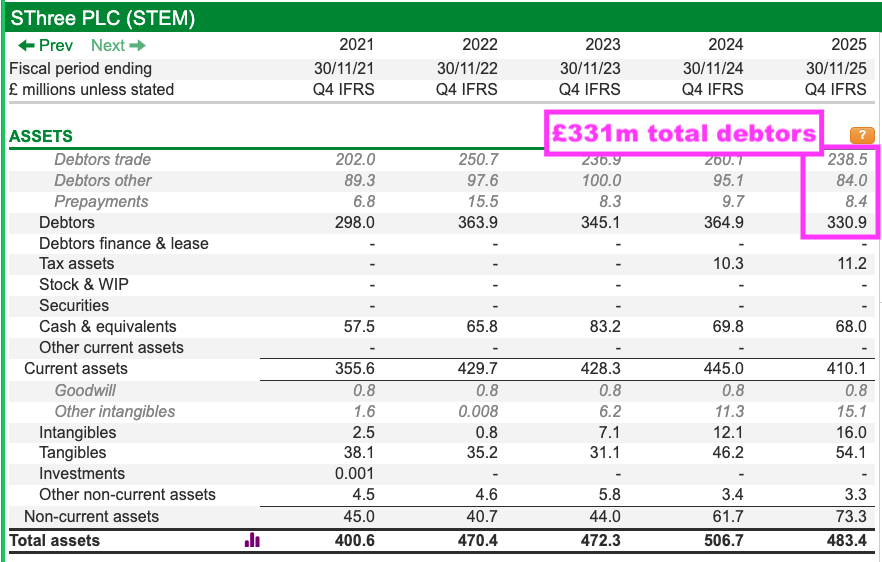

However, SThree’s largest asset is its £331 million debtor entry:

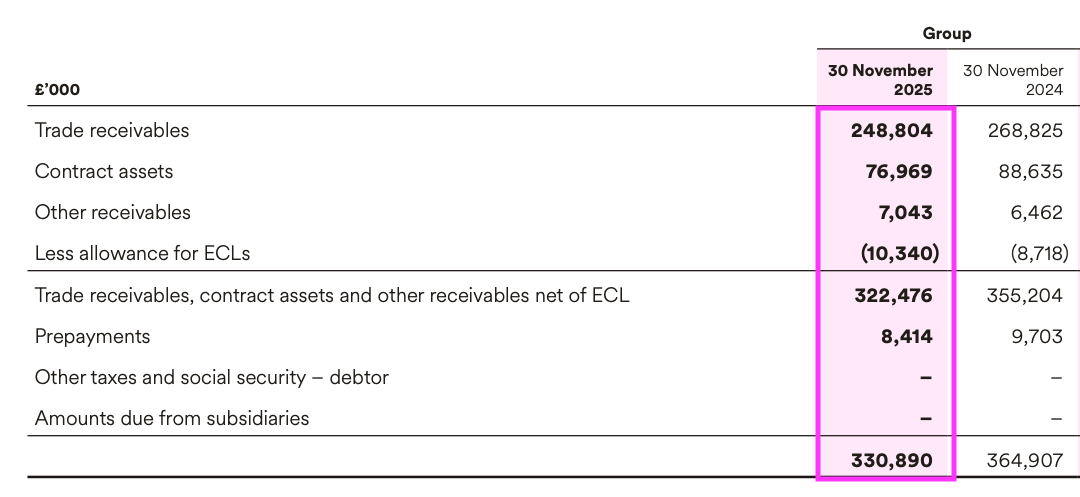

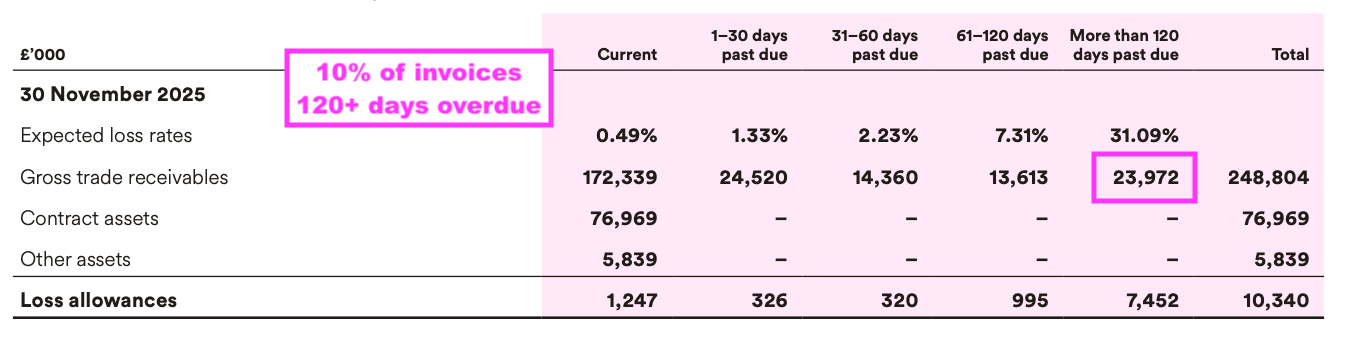

The group’s 2025 annual report reveals exactly what that £331 million entry consists of:

Trade receivables of £249 million reflect invoices yet to be paid by clients, while contract assets of £77 million reflect amounts owed by clients that SThree has yet to invoice.

The “allowance for ECLs” represents SThree’s best guess as to how much of the £249 million and £77 million will not be collected.

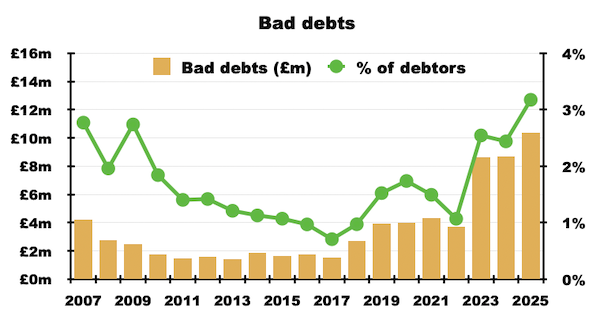

The £10 million expected bad debt is equivalent to just 3.2% of what clients owe, which does not seem enormous…

…but the proportion was 2.4% for 2024 and was less than 2% between 2010 and 2022. For extra perspective, the proportion for 2009 following the banking crash was 2.7%.

Bad debts therefore appear to be at record levels and the footnote below is perhaps further evidence of clients taking greater time to pay their bills:

Invoices overdue by more than 120 days represented 10% of all year-end invoices versus between 3% and 4% for 2020, 2021, 2022 and 2023. I should add SThree claims clients take 53 days on average to pay their bills.

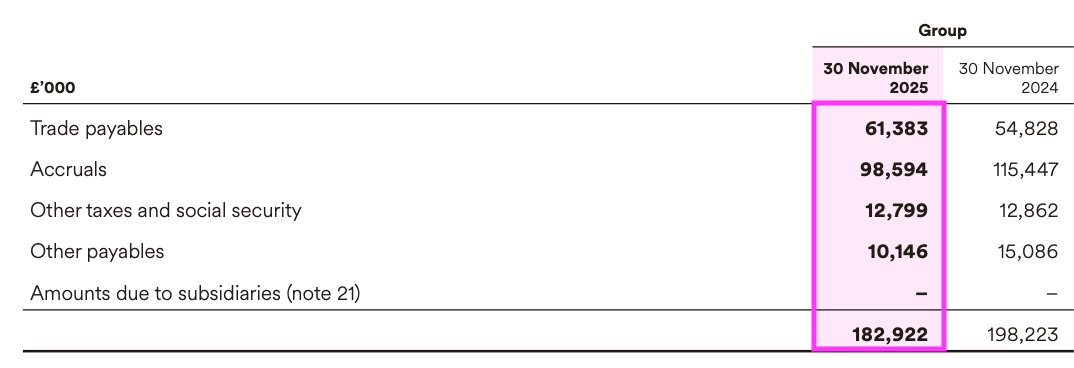

Counterbalancing SThree’s debtors are the group’s creditors:

Trade payables of £61 million reflect contractor invoices yet to be settled by SThree, while accruals of £99 million reflect all the other expenses the group has incurred but has yet to pay.

The group’s trade debtors and contract assets less trade creditors and accruals amount to £155 million or approximately 75% of the recent market cap.

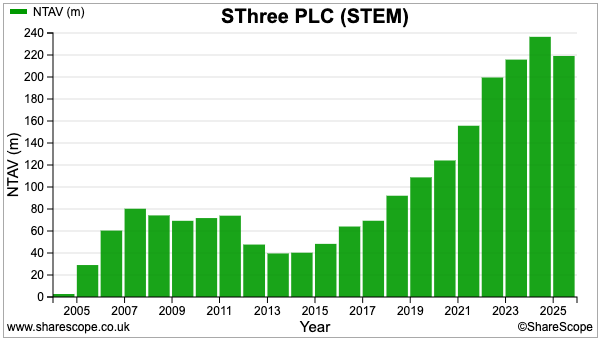

Adding the £68 million cash and £155 million working-capital together gives £223 million, with other balance sheet entries (mostly IFRS 16 office-lease assets and liabilities) trimming the overall tangible book value to £219 million or 172p per share.

SThree’s balance sheet has suffered only one notable contraction: net tangible assets declined by £34 million to £40 million between 2011 and 2013:

That reversal was due primarily to paying a £13 million special dividend plus conducting a £7 million buyback during 2012, and then maintaining the annual dividend at £17 million after incurring exceptional costs of £11 million during 2013.

Employee productivity and other financials

Recruitment is very much a ‘people business’, and staff-productivity ratios should help outside shareholders assess SThree’s progress.

Although ‘productivity’ is mentioned 24 times within SThree’s 2025 annual report, the group sadly does not publish any formal productivity measures for investors to monitor.

But SThree does invite shareholders to make their own calculations by presenting average full-time equivalent headcount figures:

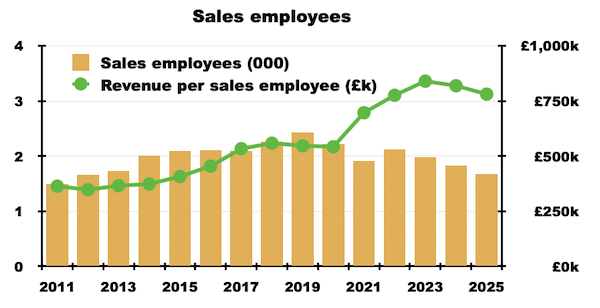

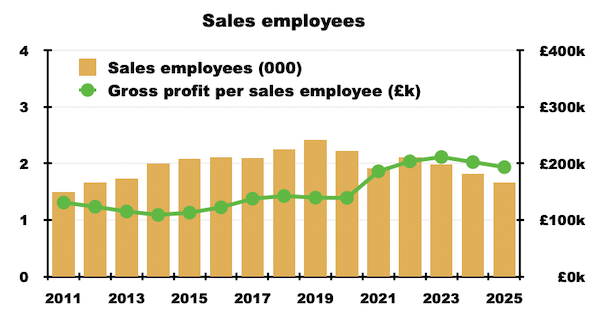

My charts below divide revenue and gross profit by the salesperson headcount:

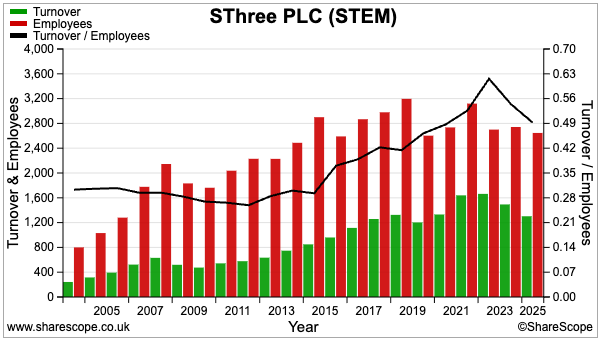

While both measures have performed positively since 2014, the last few years have witnessed progress cooling. ShareScope’s own revenue per employee data confirms a similar trend:

The reduced productivity coincides with SThree reporting fewer active contractors:

Indeed, the aforementioned 12,042 candidates placed last year compares to 22,074 placed during 2022:

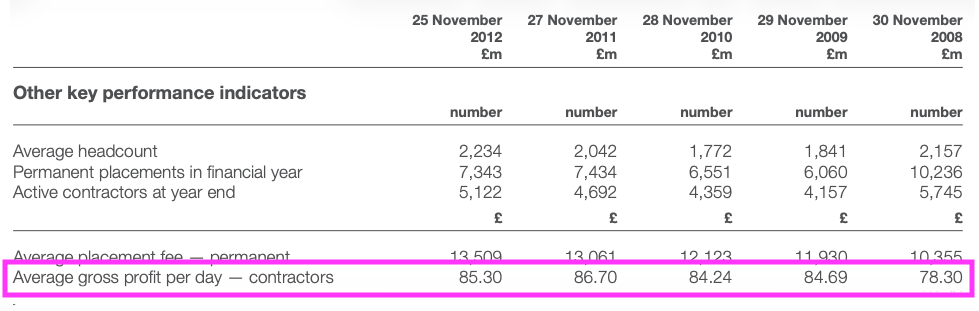

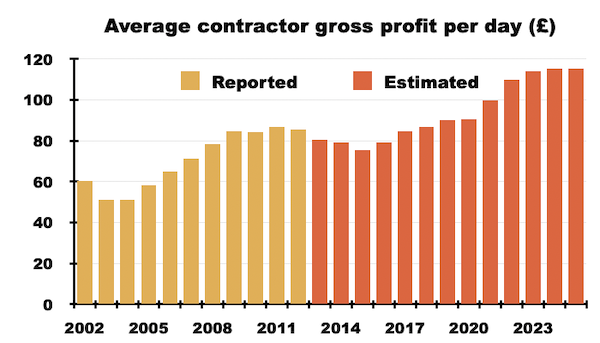

SThree used to disclose the average gross profit per day from its contractors:

My own calculations are reasonably close to those SThree produced up to 2012, and I believe gross profit per contractor per day has now reached £115:

To summarise all of these statistics, I get the impression SThree has become more dependent on fewer contractors who earn greater salaries. And I do wonder if SThree’s headcount needs to reduce further given the lower level of placements.

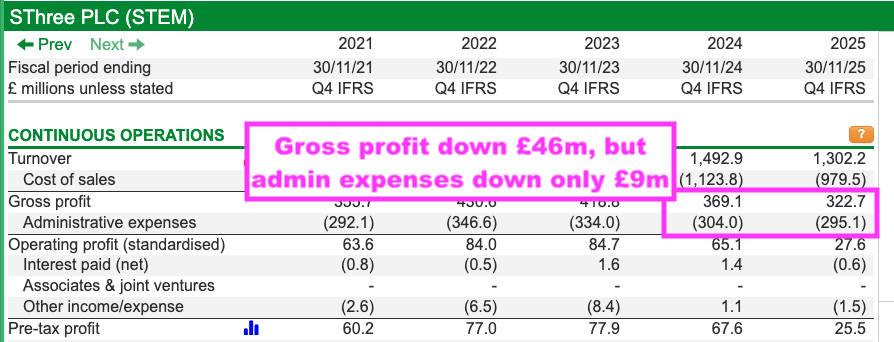

After all, the aforementioned 61% profit collapse during 2025 was due primarily to gross profit reducing by £46 million…

…but administrative expenses reducing by only £9 million.

Assuming revenue and gross profit remain unchanged, to recover profit back to £60-plus million requires admin expenses to be cut by £35 million…

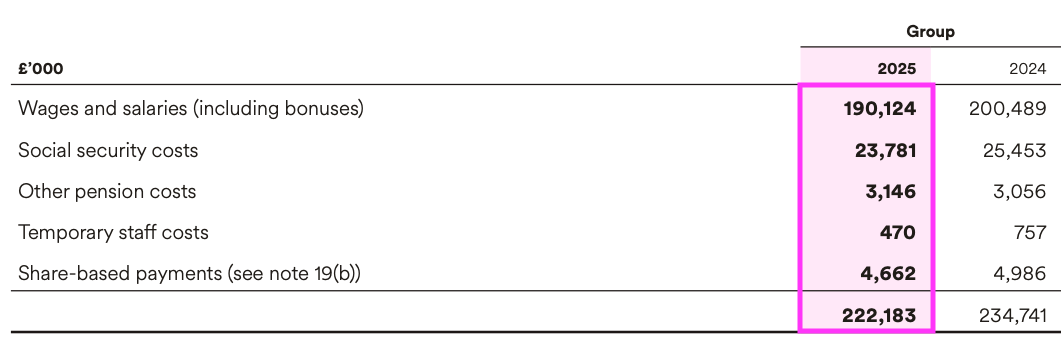

…and by far SThree’s largest expense is employee remuneration:

The average cost per employee last year was approximately £93k, meaning SThree may have to let go more than 350 employees — equivalent to 15% of the workforce — to achieve that £35 million saving.

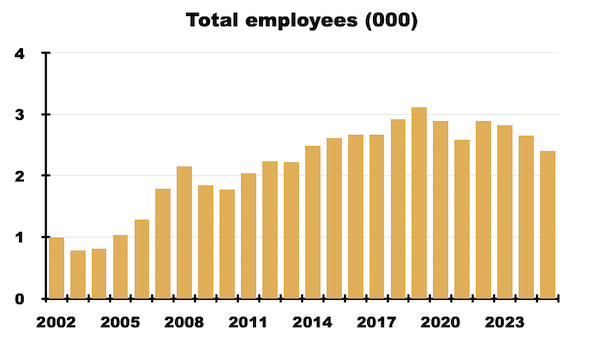

I note the headcount has already reduced by 23% since 2019:

Maybe the board could start making savings by reassessing executive bonuses.

The chief exec collected a useful £254k bonus last year despite presiding over that 61% profit collapse:

In fact, the chief exec has pocketed an aggregate £1.1 million bonus since taking the top job at the start of 2022. In the meantime, shareholders have seen both reported earnings and the share price slide by almost 70%.

Just so you know, the aforementioned co-founders Bill Bottriell and Simon Arber stepped down from the board before the flotation and disappeared from the notifiable shareholder register during 2020 and 2011 respectively.

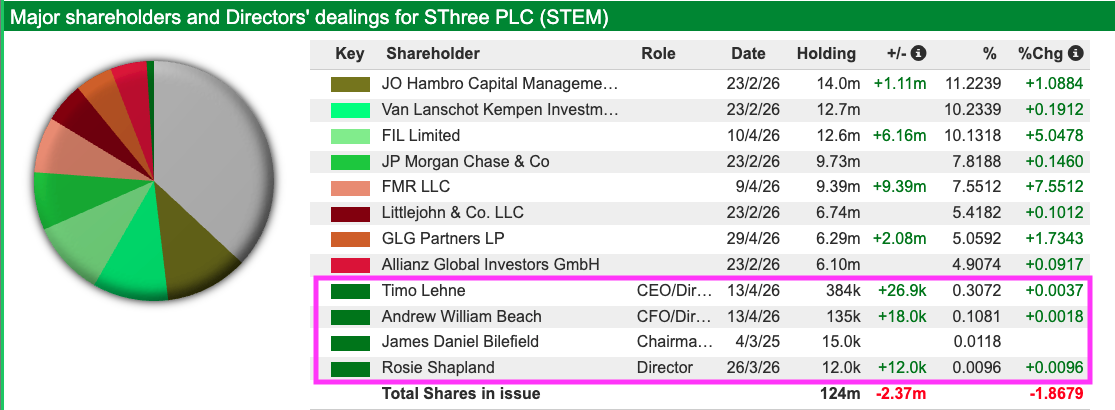

The present board has therefore become a typical ‘professional’ set-up, with the directors last year collecting total pay of £1.8 million versus their combined shareholding currently worth approximately £900k:

My reading of other parts of the accounts has not unearthed anything obviously alarming. I particularly welcome SThree’s lack of acquisitions and I am pleased profit adjustments have been minimal since 2019.

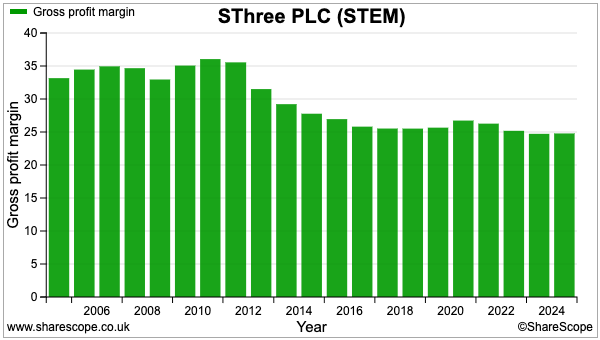

SThree’s gross margin has settled at approximately 25% for the last decade…

…which implies a client pays, say, £100k a year for a contractor through SThree, whereby the contractor receives £75k and SThree keeps £25k.

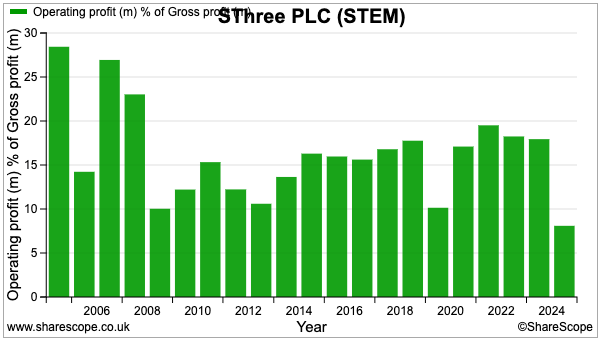

SThree has often then converted 15% of that £25k into an operating profit:

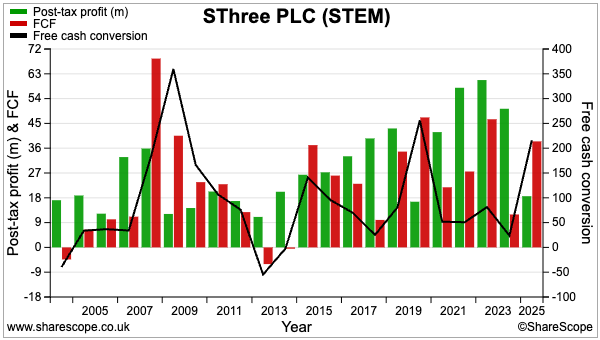

Possibly the greatest accounting drawback is the very haphazard cash conversion:

During periods of growth, significant chunks of SThree’s accounting profit are held within the large debtor book rather than converted into free cash. But the trading ups and downs tend to even things out, and during the last ten years cash conversion has averaged a respectable 95%.

Valuation and verdict

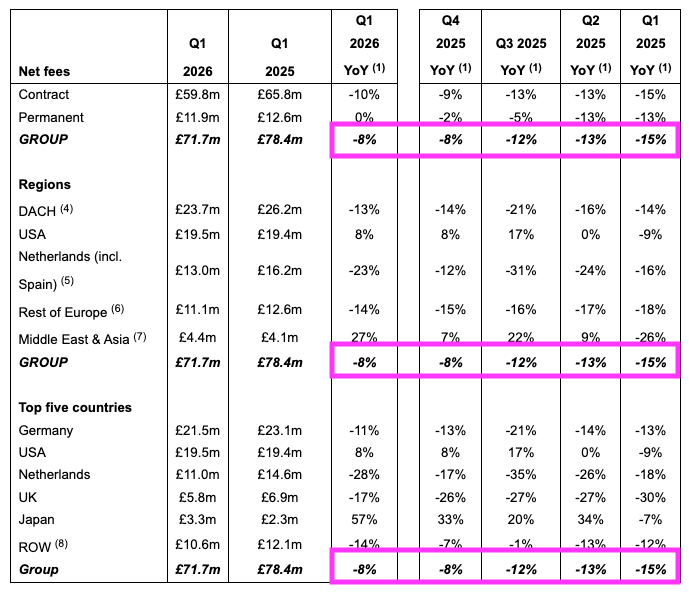

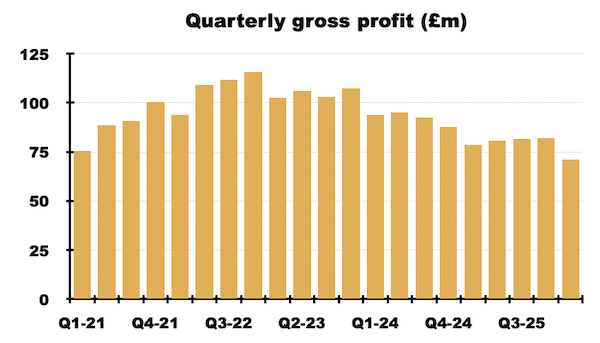

SThree’s latest trading update extended a long run of negative percentages:

Q1 2026 gross profit fell 8% to £72 million — a level 30% below the £103 million recorded for Q1 2023:

In fact, gross profit within all of SThree’s major territories and STEM segments are now lower than they were three years ago.

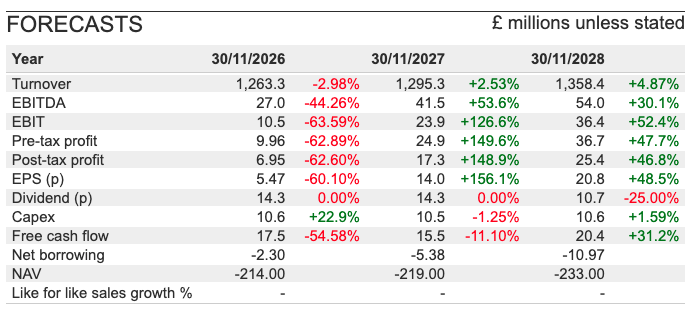

The latest update reiterated earlier 2026 profit guidance of £10 million, and ShareScope confirms shareholders should be braced for another profit slump:

Possible 2026 earnings are predicted to be 5.5p per share that leaves the 14.3p per share dividend very uncovered.

Assuming the 2026 projections are accurate and the aforementioned £68 million cash position sustains the payout, then SThree’s net assets may reduce by almost 9p per share (i.e. 5.5p less 14.3p).

SThree blamed the Q1 shortfall on the “ongoing macroeconomic volatility, including geopolitical uncertainty and rapid technological change, which continues to influence business priorities and investment decisions.”

“Rapid technological change” presumably refers to AI, and numerous investors now worry lots of lucrative white-collar jobs will be lost to the likes of Claude, Gemini and Perplexity…

…which could be very bad news for recruitment agencies.

Determining whether SThree will eventually be sunk by AI — or whether the group is simply enduring yet another cyclical downturn — is unfortunately not straightforward and something potential shareholders can only undertake for themselves.

SThree did say its Q1 headcount had reduced by 4%, and I would maintain the workforce should be cut much further to match the lower volume of placements. Those deciding to leave the group include the finance director, which sadly implies those negative Q1 numbers will not turn positive anytime soon.

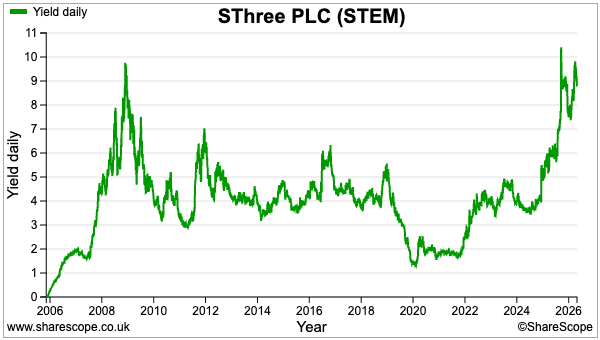

Despite the weak trading, high headcount, board bonuses and AI threat, SThree’s shares do appear exceptionally depressed and I would venture the cash position and the debtor book — the latter supported by clients who generally pay their bills in full — ought to provide a firm foundation for the market cap from here.

Indeed, I would say SThree should be able to convert its debtor book into cash faster than other ‘deep value’ shares trying to do likewise with surplus property, old machinery or slow-moving stock. I would therefore not argue against SThree becoming part of a diversified, deep-value/contrarian/turnaround portfolio at 164p.

A near-9% yield also awaits for anyone who reckons the dividend will be maintained by the cash pile and an earnings recovery will one day emerge:

Until next time, I wish you safe and healthy investing with ShareScope.

Maynard Paton

Disclosure: Maynard does not own shares in SThree.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Hi Maynard,

I’ve had SThree in my portfolio a couple of times since 2020 and for me it’s essentially a high-quality but cyclical business operating in a recruitment environment that could safely be described as a blood bath.

I think all of the big UK-listed recruitment firms are having an absolute nightmare of a time, largely because clients and candidates are reluctant to hire or switch job because of all the unending economic uncertainty and, of course, whether or not companies will need to hire anybody in an AI-first world.

My SThree position is currently underwater by quite a long way, but I won’t sell unless I see some hard evidence that this is anything more than a very prolonged post-pandemic/Trump/Tech-disruption downturn.

Hi John

Thanks for the comment. Yes, I agree with your sentiments and surely a lot of future bad news is already priced in. Will be fascinating to see how the ‘AI-first world’ plays out and how many STEM jobs will survive. History suggests societies do adapt to new ways of working and new occupations do emerge over time.