Top of the shops this year is Shoe Zone with a 46% share-price gain. Maynard Paton explores the discount retailer’s post-Covid progress and wonders whether the 10x P/E offers re-rating potential.

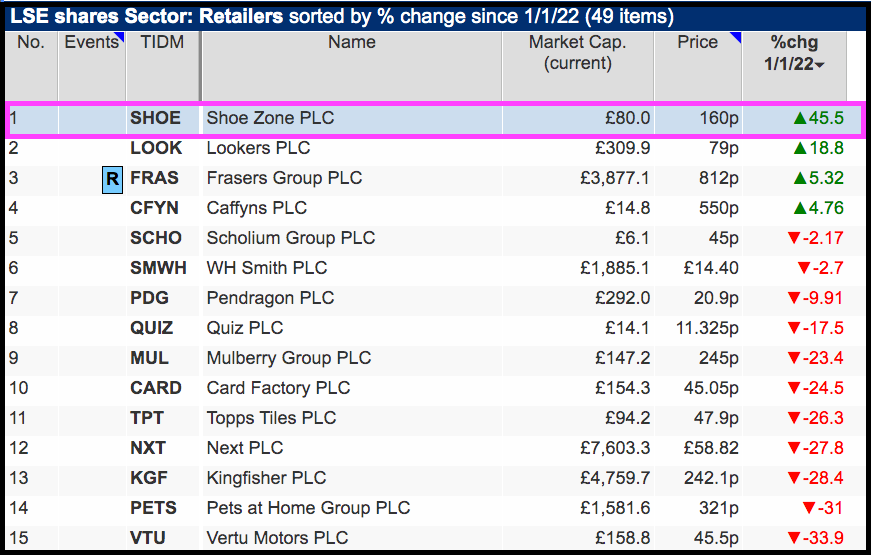

Top of the shops among this year’s market carnage has been Shoe Zone.

The discount shoe retailer has enjoyed an amazing 46% share-price gain so far this year in a sector blighted by rising costs and recessionary fears:

A trio of upbeat trading statements caught the market’s attention this summer.

The first occurred during June and referred to “strong margin improvements“:

“29 June: Shoe Zone is pleased to announce that since the publication of its interim results in May, the business has been trading well and has also seen strong margin improvements and cost savings, in particular as a result of rent reductions and good supply chain management, which are expected to continue into Q4 of the Company’s financial year for the 52 weeks to 2 October 2022″.

The second update followed in July, and revealed “stronger than expected” trading:

“26 July: Shoe Zone is pleased to announce that since the publication of its trading update on 29 June 2022, trading has been stronger than expected due to higher than expected demand for summer products, particularly in the last two weeks. The Company has also continued to experience margin improvements as a result of good supply chain and cost management.”

And the third update occurred last month, and confirmed trading had “continued to exceed expectations“:

“31 August: Shoe Zone is pleased to announce that since the publication of its trading update on 26 July 2022, trading has continued to exceed expectations due to continued strong demand for summer and back-to-school products throughout August. The Company also continues to benefit from the margin improvements as outlined in recent trading updates.”

The remarkable run of RNSs also revealed the group lifting its current-year profit expectations from “not less than £8.5 million” to “not less than £10.5 million“.

The profit upgrades and share-price surge will of course be welcomed by shareholders, although the company’s longer-term performance could mean the positive summer may not be a persistent phenomenon.

The shares joined AIM at 160p during 2014 and, eight years later, the price stands at… 160p:

Let’s take a closer look.

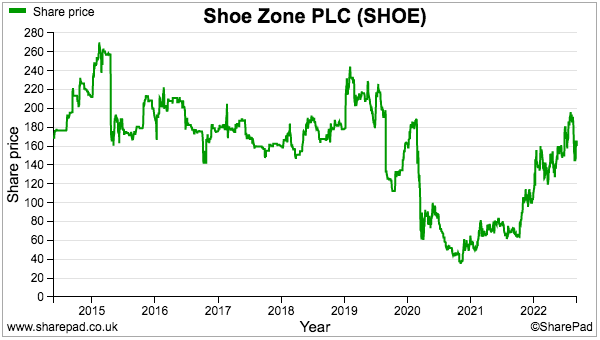

Falling sales, profit warnings and special dividends

The underwhelming share price since the flotation reflects a rather unconvincing financial history:

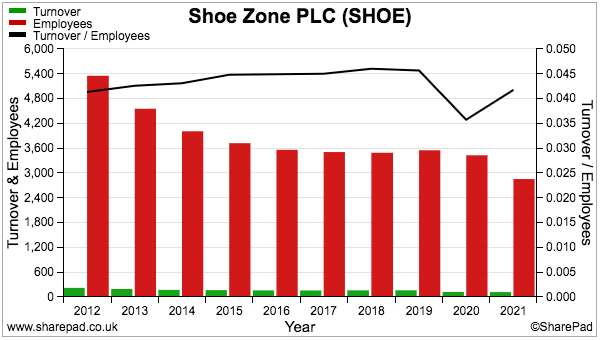

Prior to the pandemic, revenue had at best stagnated as the chain closed shops and re-jigged others to combat greater competition and higher expenses.

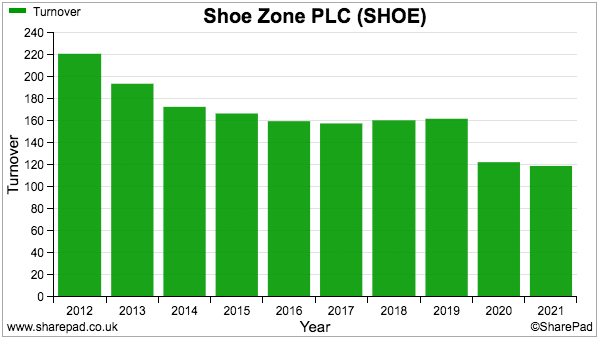

Profit meanwhile fluctuated as the group suffered at least two setbacks.

Shoe Zone blamed the weather for selling fewer higher-priced ladies boots during 2015:

“The warm weather conditions had a material impact on autumn/winter trading which slowed revenues in the first half. While footwear sales volumes increased, the average price was down due to the different product mix sold, e.g. lower priced ladies ankle boots were favoured over long leg boots.”

Then an update during 2019 simply cited “challenging” high street conditions:

“Trading conditions since the Group’s Interim Results on 21 May 2019 have been challenging and as a result, the Board now expects to deliver a full year performance below its expectations.”

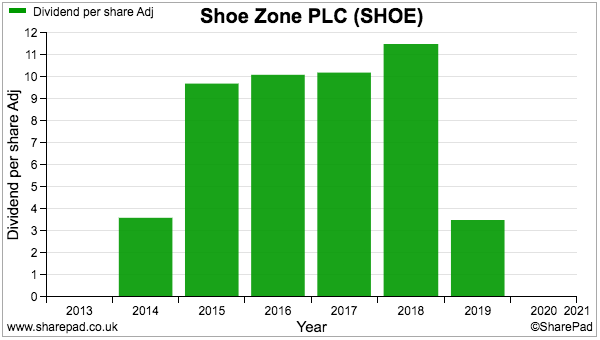

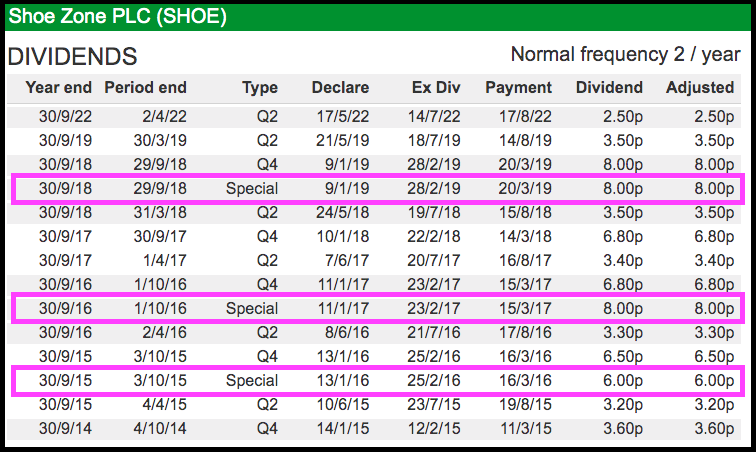

But dividends have been paid:

And significantly, special payouts were declared during 2016 (6p per share), 2017 (8p) and 2019 (8p):

The pandemic of course halted dividends, and the 2021 results warned payouts would disappear until 2025:

“Until the business is debt free, has tackled the pension deficit, repaired the balance sheet and restored capital expenditure, the business will not be in a position to make dividend payments. We anticipate this will not be before 2025.”

But first-half results issued during May this year disclosed dividends recommencing, which signalled growing management confidence and perhaps (with hindsight) that trio of summer profit upgrades.

From high streets to ‘Big Boxes’

Shoe Zone’s unsteady track record reflects the group’s attempts to extricate itself from an underperforming high street estate.

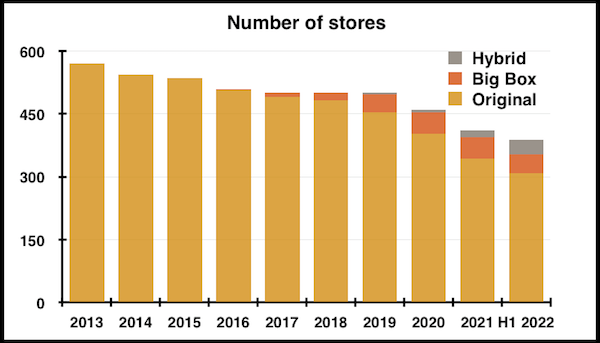

The number of shops have shrunk from more than 800 back in 2009 to less than 400 today:

The last few years have seen Shoe Zone close many ‘Original’ town-centre locations and open new ‘Big Box’ outlets, which are larger premises on retail estates that offer a much wider selection of shoes.

Other high street stores have been converted into ‘Hybrid’ shops, which are effectively mini ‘Big Box’ outlets. The new sites try to attract more affluent purchasers by stocking brands such as Crocs, Kickers and Skechers alongside Shoe Zone’s own ranges.

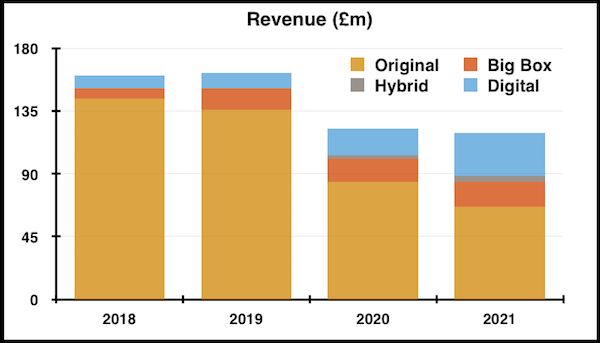

Revenue from the Big Box locations has improved from £7 million to £18 million since 2018, with Hybrid outlets last year producing £4 million:

But the Original high street locations continue to support the bulk of the group’s income.

In fact, ‘Digital’ revenue through website orders have exhibited at least as much promise as the new larger shops. Such sales have tripled to £30 million since 2018 as customers became more accustomed to buying online during the pandemic.

Financial improvements post-pandemic

Whether the shift to larger shops and greater online activity are enhancing Shoe Zone’s economics is hard to judge.

The group has certainly made headway with rents. During each of the last five years, Shoe Zone has achieved rent reductions on renewals of at least 20%, with a stunning 53% reduction reported for 2021 that will save almost £2 million a year.

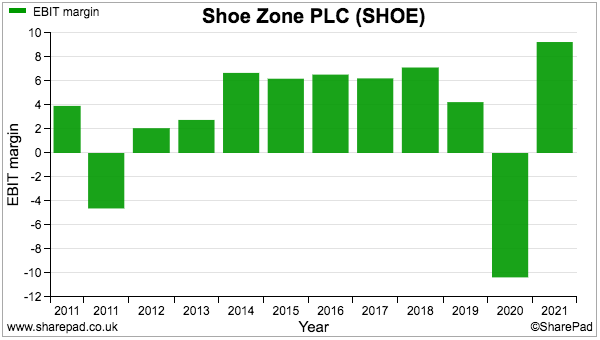

Lower rents helped the group’s margin reach a record 8% for 2021…

…with 8% seeming very creditable given the shoes command a typical selling price of just £12 a pair.

May’s interim figures meanwhile disclosed the group’s best-ever first-half profit of £4 million, which was notably assisted by energy contracts being fixed until September 2023.

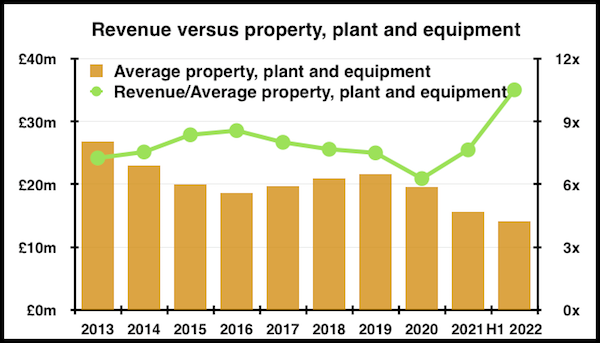

Another measure heading firmly in the right direction has been revenue versus the carrying value of property, plant and equipment:

This improvement may suggest the cost of fitting-out new shops and maintaining old ones is — just like the rents — becoming a lot cheaper.

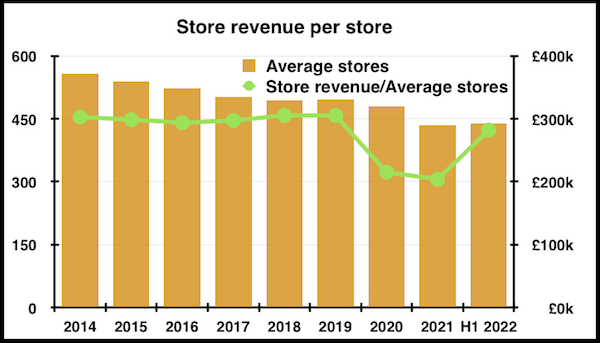

But other measures of Shoe Zone’s post-Covid progress do not yet show clear improvements. Excluding online sales, revenue per store remains slightly below the £300k witnessed prior to the pandemic:

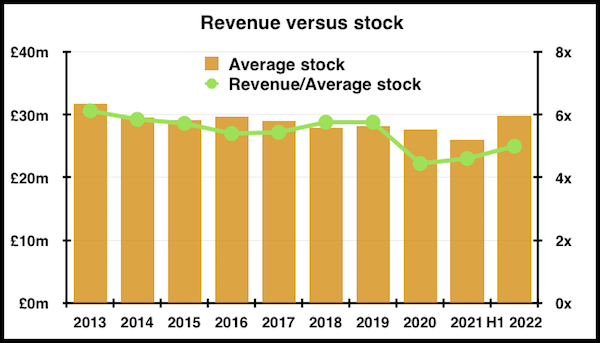

Furthermore, total revenue versus stock — Shoe Zone’s largest expense and asset — has not yet reached pre-pandemic levels:

And revenue per employee is still to return to pre-pandemic levels, let alone show any benefits from the larger shops and greater online sales:

Balance sheet liabilities

Shoe Zone’s balance-sheet liabilities are worth highlighting.

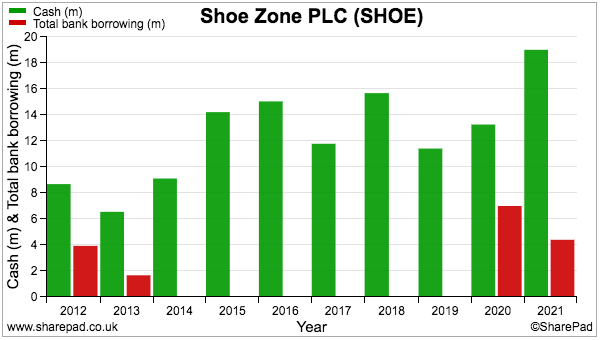

Although the accounts have regularly enjoyed a cash-positive balance sheet…

…the group’s cash is not truly ‘surplus to requirements’ because the bank balance is mostly a function of owing significant sums to suppliers:

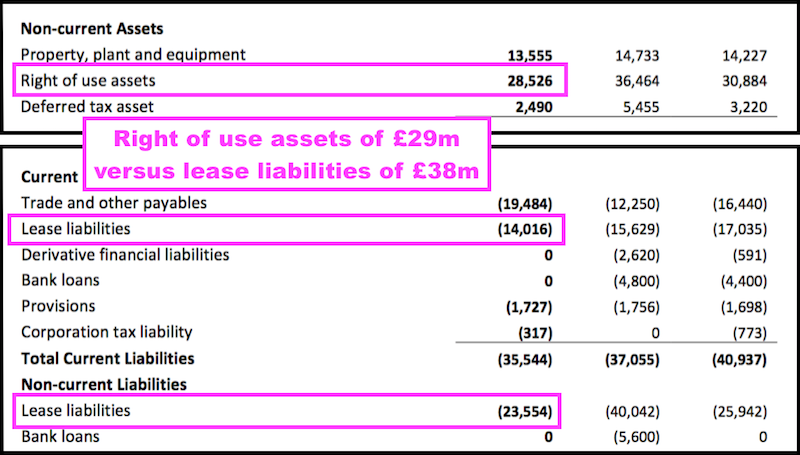

Future lease payments (almost entirely future property rents) total £38 million, but compare to right-of-use assets of £29 million:

The implication here with the IFRS 16 accounting is that Shoe Zone is on the hook to pay £9 million (£38 million less £29 million) extra through future rents than it would have to pay if the group were to agree to the same leases today.

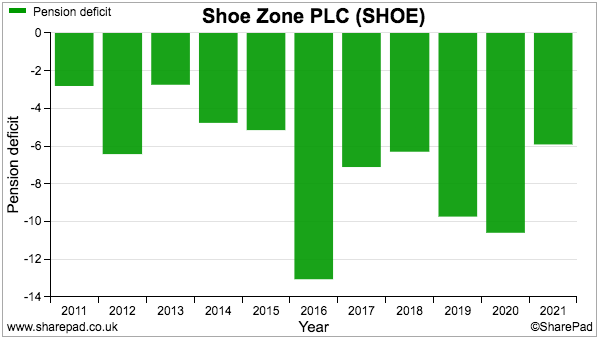

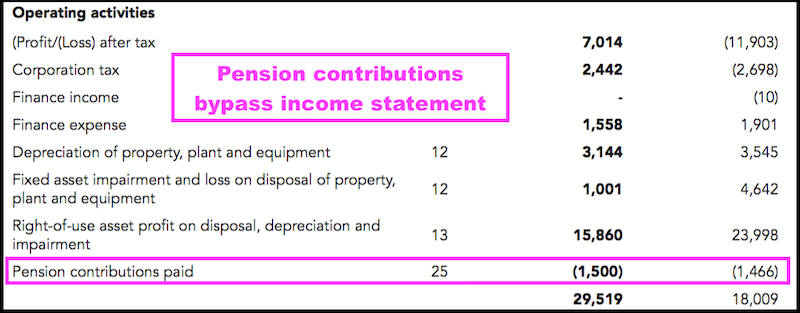

And a pension liability has been a niggling bookkeeping feature for a decade:

Some £5 million has been injected into the pension scheme between 2017 and 2021 — all of which has not been charged to reported earnings:

At the last count, Shoe Zone’s two defined-benefit schemes owned assets of £90 million and were paying annual benefits of £3 million. Recent contributions of £1.5 million a year look sufficient to ensure the benefits can be maintained without the scheme assets suffering too much risk of erosion.

Family management owns 54%

Shoe Zone’s veteran management is the by far the group’s most compelling feature:

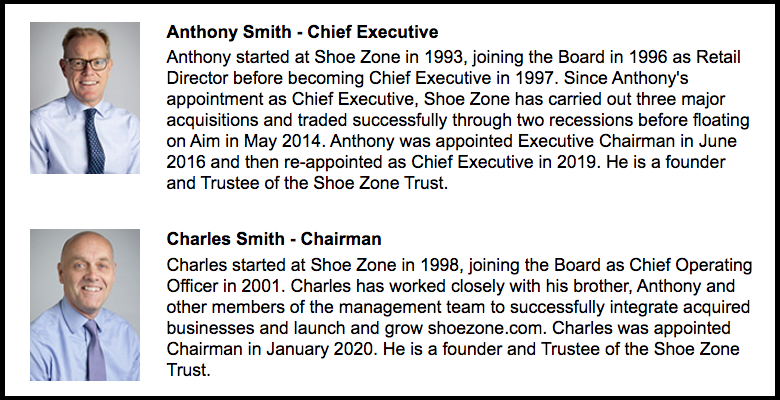

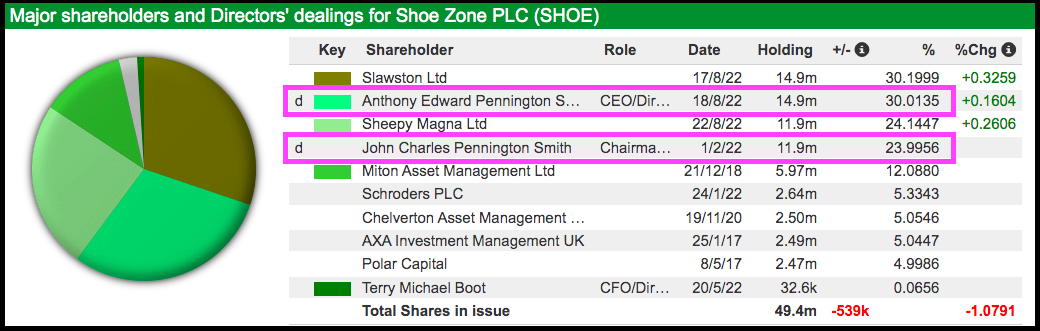

Brothers Charles and Anthony Smith have led Shoe Zone for more than 20 years and presently act as executive chairman and chief executive respectively.

The pair control 54% of the share count, a shareholding derived through their father and uncle who acquired what became Shoe Zone during the early 1980s:

The Smith brothers sold a collective 45% of their shareholdings at the flotation, and sold a few more at 190p during 2015 but then bought a few more at 80p last year.

Management’s significant shareholding no doubt explains the aforementioned special dividends, and most likely explains why the board operates without an option scheme.

Shoe Zone is not adverse to ‘outsiders’ holding non-exec positions, which is a very refreshing attitude compared to many family-controlled boardrooms that effectively operate as ‘closed shops’.

Current non-execs providing insight for the executives are the former footwear director of New Look and the supply chain director at The Works.

The Smith brothers are in their fifties and succession planning should therefore not be an immediate concern, although Charles does now work a four-day week.

Valuation and summary

SharePad carries the following forecasts:

The pre-tax profit forecast for 2022 reflects the £10.5 million figure cited within the last of those summer updates.

But the projections for 2023 look very alarming, and clearly show a small deduction to revenue converting into a significant profit shortfall.

Although the summer updates indicated better-than-expected margins, May’s half-year statement did admit capital expenditure for new shops, refits, IT systems and warehouse enhancements would “accelerate” during the second half and into next year.

Note, too, that the current second half is set to show a pre-tax profit of approximately £7.4 million — which is much lower than the £12 million profit struck within the second half of the prior year.

Predicted earnings of almost 17p per share place the 160p shares on a multiple of less than 10x.

Although the rating is modest, the market has never really applied a generous multiple to the group’s progress.

When the shares peaked at 270p during 2015 the trailing multiple was 15x, and when the shares climbed to 240p during 2019 the trailing multiple was 13x.

Whether Shoe Zone can ever attract a premium valuation is difficult to say. The jury remains out as to whether the group’s efficiency — as measured by revenue per shop and per employee — will eventually improve after Covid.

May’s results outlined the following growth plans:

“Our ultimate goal is a doubling of Big Box locations to approximately 100 and an increase in Hybrid stores to 200 in the medium term. We anticipate trading from a similar sales square footage, albeit from a reduced number of locations.”

Doubling Big Box locations could add another £20 million to sales and possibly the same could be said for taking Hybrid stores to 200. All the new larger stores might then push revenue from approximately £150 million to something close to £200 million.

Adjust for lost income from closed high street outlets, and maybe Shoe Zone’s top line could grow at 5% per annum or so for the next few years. Will that growth rate be enough to extend the P/E multiple back to, say, 13x?

Perhaps the best hope for shareholders is extra income. The Smith brothers did like their special dividends before the pandemic, and further such payouts would be the definitive way to underline Shoe Zone’s post-Covid progress and value-share credentials.

Until next time, I wish you safe and healthy investing with SharePad.

Maynard Paton

Maynard writes about his portfolio at maynardpaton.com. He does not own shares in Shoe Zone.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.