Private equity fund in transition – new addition to Dynamic 35

Listed private equity funds have had a chequered record on the London Stock Exchange. On paper they are a great innovation, allowing private investors access to usually institutional grade alternative assets. Crucially they allow investors to put money to work in profitable, scaled up private businesses, many of which might find their way to an IPO in the next few years.

Back in the real world, listed private equity funds have faced a number of headwinds. First off, there is a general sense of unease about the high level of fees embedded within these structures, with the 2 and 20 model very much still alive.

The more substantive concern though has centred on transparency. The listed funds tend to invest in long term LLP structures and sometimes it has proved very difficult to work out what’s going on inside the portfolio businesses.

And if all this wasn’t bad enough, many of the listed private equity funds have made unforced errors, such as issuing shares when their shares trade at a big discount – a tactic almost perfectly designed to annoy investors. Which brings us to the last problem – discounts. All these concerns have snowballed into a general feeling that these funds can be, in effect, expensive black boxes. That has resulted in a raft of persistent discounts to stated net asset value.

Many of these headwinds have impacted our newest addition to the Dynamic 35, Oakley Capital Investments. The fund should be something of a stockmarket favourite given that one of its founder is the inestimable Peter Dubens who boasts a stellar track record as a technology investor.

It invests in sexy sectors – think tech and well-known brand names- and has a fairly unique deal origination process. Put very simply, rather than trade assets with other PE firms, Oakley has built up a network of experienced entrepreneurs who bring it almost constant deal flow. That combined with a focus on earlier stage mature businesses – profitable, but not necessarily valued in the billions – should make it an attractive fund for investors. Unfortunately, the fund has continued to trade at a substantial discount, which currently stands at around 25 to 30% compared to a sector average that is closer to 15%.

Then again Oakley’s misfortune could be your opportunity. The funds managers have radically improved transparency at the portfolio level. They have also started to shift away from an earlier emphasis on consumer brands such as Time Out towards a more tech and educational services heavy approach. That makes a great deal of sense to me and I think the opportunities in the educations sector are huge. So, in sum, you have a very activist PE manager, focused on the right sectors, slowly trying to narrow that discount. To me, that sounds like a classic, slightly boring, fund transformation.

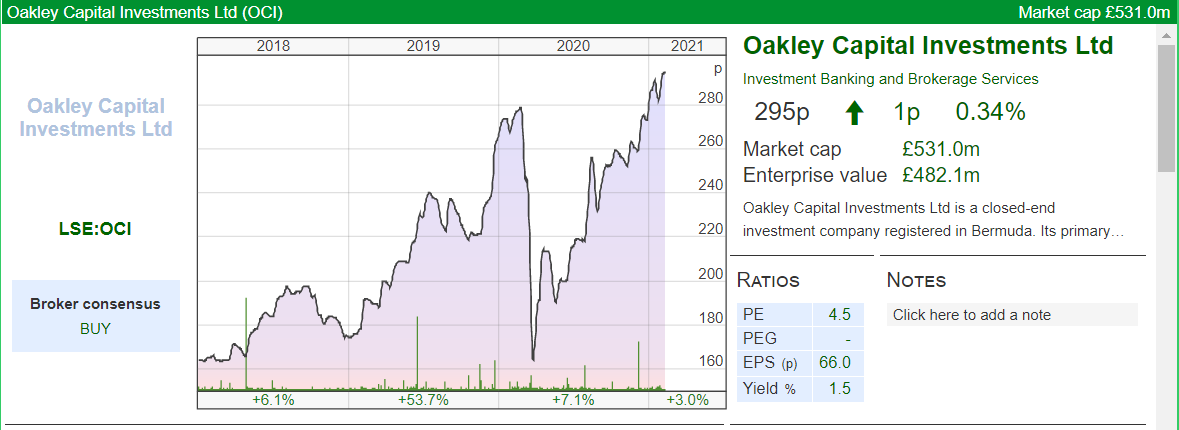

Fund Basics

- What is it? OCI is a listed fund investing in funds managed by Oakley Capital that concentrate on digitally focused businesses across Western Europe in the technology, education and consumer sectors.

- Share price – 293p

- Ticker OCI

- Market cap £529m

- Of note: Peter Dubens is Managing Partner of Oakley Capital

- Discount: 27%

Recent results

A good place to start an analysis of OCI is to look at its impressive recent full year results out a few weeks back. The top line is that at year end 2020, the fund’s Net asset value per share stood at 403p, which represented a total return of 14% since June.

Highlights for the year

| ● | Net Asset Value (“NAV”) per share of 403 pence |

| ● | Total NAV return per share of 18% since 31 December 2019 |

| ● | The Company invested £152 million and received proceeds of £341 million |

| ● | Year-end cash of £223 million |

| ● | Outstanding Oakley Fund commitments of £534 million, including the Origin Fund commitment |

| ● | Total Origin Fund commitment of £116 million |

| ● | Buy-back and cancellation of 18 million shares |

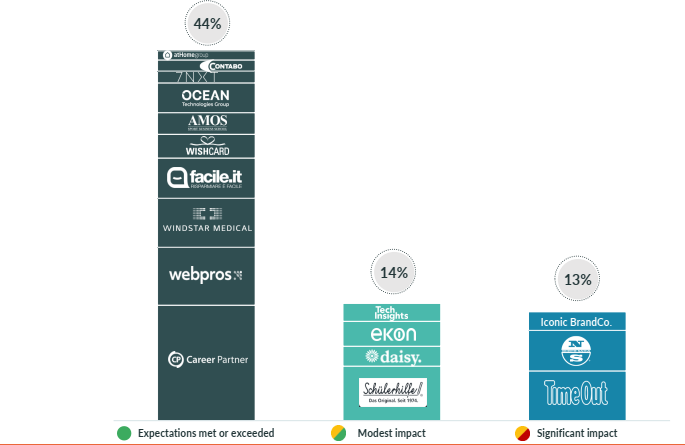

Helpfully given the impact of Covid, the manager has separated the portfolio of private businesses into three COVID-19 impact categories.

| 1. | Expectations met or exceeded – 10 companies – 44% of NAV*

Business Service Software, Web Hosting, Online Consumer platforms and Education Technology businesses, each grew EBITDA at or above pre-COVID expectations |

| 2. | Modest impact – 4 companies – 14% of NAV*

Telecoms and Education businesses that experienced some disruption to their expected financial performance, with new business wins or enrolments impeded due to social restrictions |

| 3. | Significant impact – 3 companies – 13% of NAV*

Physical footprint and direct-to-consumer businesses whose operations suffered material disruption as a result of repeated Europe-wide lockdowns. |

Covid impact in chart form

According to an analysis by fund researchers at Numis, three of the holdings in the portfolio moved from COVID category two – ‘modest impact‘, to category one – ‘expectations met or exceeded‘.

According to the Numis report, “based on the descriptions of the businesses now included within the categories it appears that the three holdings are Facile, Ekon and the residual position in Casa….category one holdings would have continued to drive the portfolio’s performance. We also note three investments continue to sit in COVID category three – ‘significant impact‘ – North Sails, Time Out and Iconic Brandco”.

It’s also very important to understand the balance sheet of all private equity funds. In very simplistic terms you need to keep on four moving parts – how much cash is available to invest, what are the future commitments to underlying funds, how much debt there is in the businesses (which includes a sense of business refinancings) and finally, perhaps most importantly, how successful the underlying funds have been in realisations i.e selling on businesses.

These annual results show good progress on that last front – Oakley Capital Investments received proceeds from exits and refinancings of £341m. By contrast the fund invested £152m in new businesses during the year.

Significant realisations included WebPros, Casa, Inspired and the partial realisation of atHome, generating an average gross money multiple of 3.3x. Since inception the average premium to carry value on exit is 37%.

As for the rest of the balance sheet, here’s the key facts:

| ● | Balance sheet – OCI has no leverage and had cash on the balance sheet of £223 million at 31 December 2020, comprising 31% of NAV. This cash level is significantly higher than the long-term average due to the quantum of realisations in the period |

| ● | Recent commitments – OCI’s total commitment to the Oakley Capital Origin Fund, which closed in January 2021, was €129 (£116) million. This latest Oakley Fund will apply Oakley’s proven investment strategy to companies in the lower mid-market segment |

| ● | Total outstanding commitments – outstanding Oakley Fund commitments are £534 million. These will be deployed into new investments over a five-year period |

Subsequent to the year-end OCI has received £22m (via OCF II) from a sale of Daisy’s Digital Wholesale Solutions division, and has agreed (via OCF IV) to make a £43m minority investment in idealista.

Overall, these are healthy numbers though I note that OCI still has commitments to invest £534m in future fund raisings, against cash on hand of around £220m. That equates to a funding ratio of roughly 0.40 which could be cause for concern. Then again, the fund could also receive extra cash from future realisations which could fill a large part of that gap and the commitments are very from being owed tomorrow i.e the fund could space out its payments over a period of time to manage cash flows.

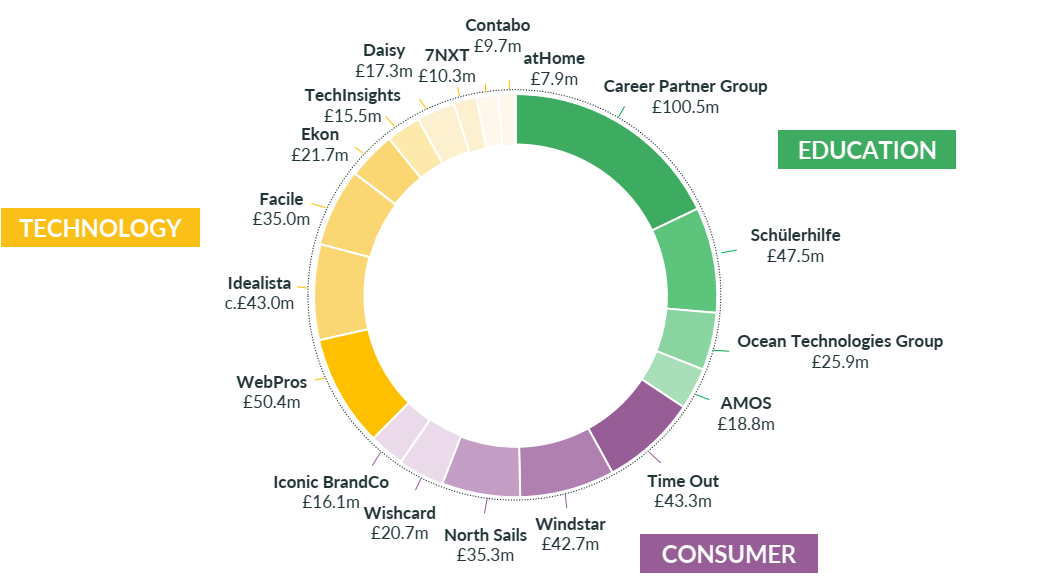

What’s in the portfolio?

There are some similarities with another listed private equity fund Hg Capital, in that many of Oakley’s portfolio companies have a strong technology bias – on my reckoning 12 of the 17 investee companies deliver their products or services digitally. Overall, the portfolio businesses sit in one of three buckets:

- Technology/ This in part built on heritage of backing Web hosting business Daisy. This sector has now expanded to include a range of Business services and solutions businesses such as WebPros and Idealista. Collectively these make up 37% of the value of the portfolio.

- Consumer (brands) which include the listed business Time Out and North Sails plus Windstar. 28% of the portfolio.

- Education. This fast growing segment of the portfolio includes the single biggest holding of the fund (by value) Career Partner Group as well as Schulerhilfe and Ocean Technologies. 34% of the portfolio.

The graphic below from Oakley maps out these portfolio businesses.

One key fact worth highlighting is that OCI has a very strong continental European flavour to it, with the majority of the businesses operating in Germany, Spain and Italy. One way of putting a number on this is to look at Foreign exchange exposure, where the fund is running 75% Euro exposure.

Another way of examining the fund is to look at its NEW investments, which should in turn give investors a sense of where the future focus of the portfolio might lie. In the 12 months to 31 December 2020, OCI invested c.£152 million, in the following:

| ● | Platform investments – £90 million – the acquisitions of WebPros (Fund IV), Globe-Trotter, 7NXT and WindStar Medical |

| ● | Follow on investments – £21 million – bolt-ons to Ocean Technologies Group and Ekon, and further indirect fund investments into North Sails and Time Out |

| ● | Direct investments – £41 million – including equity participation in Time Out’s refinancing and an increase in the debt investment provided to North Sails |

Post these end of year numbers OCI also announced a minority investment in idealista, which is, according to Oakley the leading online real estate classifieds platform in Southern Europe, present in Spain, Italy, and Portugal. One of the OCI sub funds, Fund IV, will invest €175 million alongside the management team of idealista and EQT, who will remain the majority shareholders in the Company.”

Its useful, I think, to dig a little deeper into this new investment as it clearly shows the focus on digital platforms, many of which have a slightly copycat feel to them i.e they copy the business model of market leading Anglo American firms and then export them to a new geography. Idealista is described in the following terms:

“Founded in 2000 and headquartered in Madrid, Spain, idealista supports approximately 40,000 real estate agents and 38 million unique monthly visitors across Southern Europe by providing an online real estate classifieds marketplace for home buyers and sellers. The Company’s online platform and diversified portfolio of digital services, such as CRM tools, data analytics, and online mortgage brokerage, help facilitate efficient real estate transactions, making it a key destination for prospective homeowners and sellers in Spain, Italy, and Portugal. idealista is a clear leader in Spain and Portugal and has a growing presence in Italy, a market where the Company will benefit from Oakley’s previous experience with Casa. idealista’s underlying market is supported by favourable secular megatrends, such as the increasing penetration of the online classifieds market in Italy, Spain and Portugal as they mature in line with more developed global classifieds markets; the shift from offline to online marketing spend by real estate agents; and the significant network effects driven by the platform’s strong brand recognition.”

Bottom Line

Oakley is, I would contend, a fund in transition. It is trying its damndest to become more private investor friendly. As I said at the beginning, it has become much more transparent about how it manages its portfolio and balance sheet. And the board have also become much more proactive in explaining the story and deploying the right tools to narrow down its discount.

That hasn’t necessarily had much impact on the share price though. The last time I looked, the discount was at 26% which compares to an average for the sector of around 10%. Crucially the average discount for Oakley/OCI shares has been closer to 18% over the near term. That implies that if those efforts by the manager and the board pays off, we could see a meaningful reduction in the discount from 26 to 18%. Buy backs will help on this score – during the last financial year OCI completed the buy-back and cancellation of 18 million shares at an average price of 230 pence per share, resulting in a NAV uplift of 12.6 pence.

But the real driver of a narrowing discount will be a run of positive NAV numbers and realisations. And on that score OCI is making real progress. These last full year results were impressive, especially considering the Covid background, and they might get even better if the vaccine allows some businesses to return to normal. Sure, there are some businesses such as Time Out and Northsails which are clearly in a difficult market but that could change if the wider macro-economic environment regains positive momentum. More importantly I think the renewed focus on digital products especially in education makes a great amount of sense.

Jefferies view

“Having taken a number of steps to improve governance, we feel OCI is on an upward trajectory as an investment proposition. While there is still some limited work to do, current governance and disclosure arrangements should now allow most investors to get comfortable with the fund. Moreover, we see near-term upside to the portfolio valuation when incorporating H2 marks, as well as the potential for a medium-term increase in valuation multiples. OCI also benefits from a 22.5% headline discount that should continue to narrow to reflect the fund’s progress, and so we initiate coverage with a Buy recommendation.”

Numis comments after full year numbers

Commenting on the recent full year results : “This is a strong NAV for Oakley. We had been expecting tailwinds to valuations given the significant valuation lag, with the previous NAV being at June, a focus on technology enabled businesses and a number of positive realisations. We estimate a NAV of 397.9p allowing for movements in quoted holding, Time Out (-0.6%) and currency (-0.7%), which based on last night’s price of 281p represents a 29% discount to the estimated NAV. We believe the discount offers significant value, given a large portion of the portfolio in technology-orientated businesses. We expect that the discount partly reflects historic corporate governance transgressions, which the company has committed not to repeat, and a focus on Time Out, which has becoming a smaller portion of the portfolio than it once was.”

David Stevenson

Contact on Twitter: @advinvestor

Check out my blog at www.adventurousinvestor.com

Executive editor at www.altfi.com and www.etfstream.com

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.