Screening For My Next Quality Winner: Foresight Group (LSE: FSG)

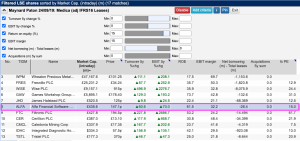

High margins, rising profits, significant director ownership and a modest valuation are among the attractive credentials of Foresight Group. Maynard Paton studies the fund manager’s positive progress based on investing in a ‘decarbonised future’. I am not a great fan of the fund-management industry. I cannot think of another sector where the employees typically collect