Alpesh Patel examines the latest holdings of some of the world’s top-performing hedge fund managers, combining elite fund disclosures with his own technical and quality framework to identify the most compelling opportunities. He also highlights the key macro themes shaping markets.

Before We Begin – What Caught My Eye this month

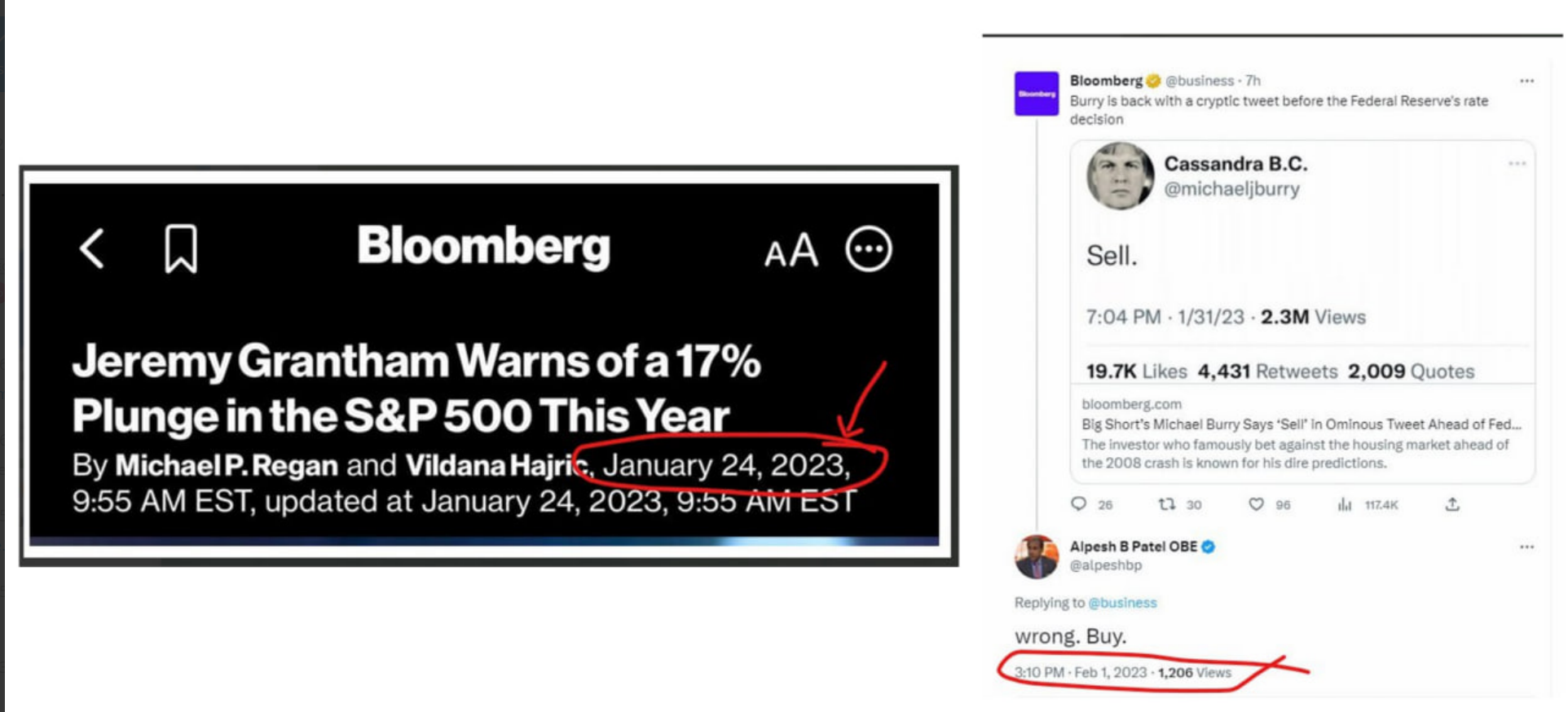

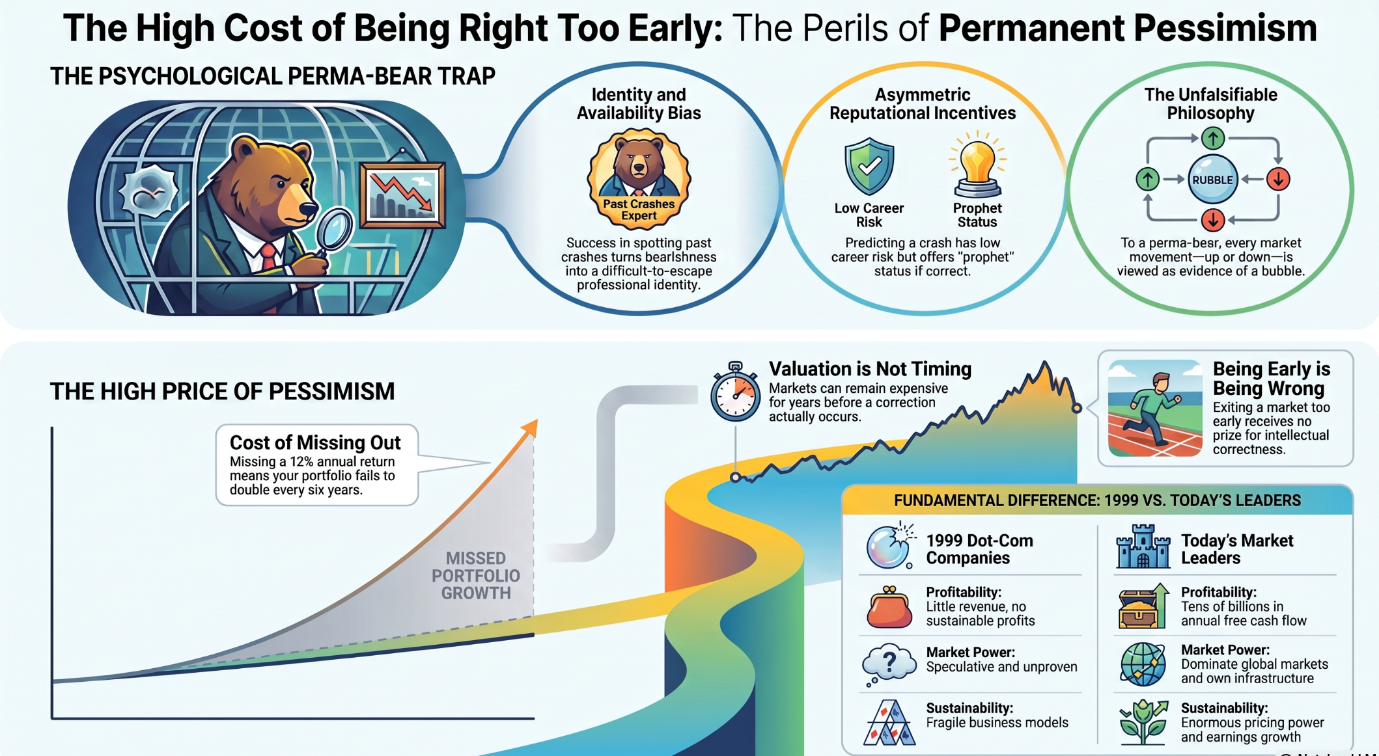

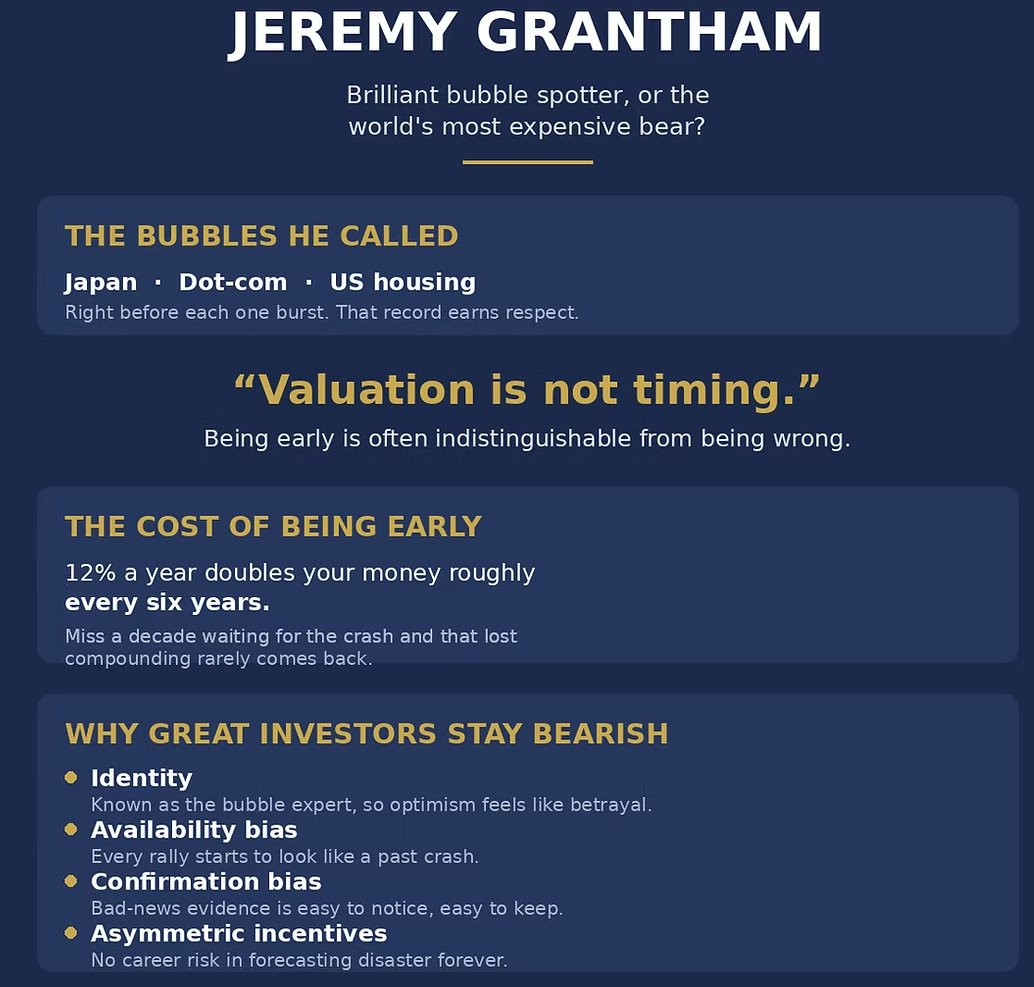

Perma-bears

Busy Month

Firstly birthday on the anniversary of the first atomic explosion and the first manned mission to the moon. Something about a big explosion and rockets in my life.

Above is my dashboard. Enjoy. And below – congrats to a customer

Not sure if any space is left but if you’d like to meet me in Parliament, my event below.

What the World’s Best Hedge Fund Managers Are Holding Right Now

A 39-position screen across six elite hedge fund filings — July 2026

Full stock-by-stock analysis available exclusively to Alpesh Patel Special Edition subscribers.

THE METHOD — WHY THIS LIST EXISTS

Every quarter, the world’s most successful hedge fund managers are forced to show their hand through US regulatory filings. Each month I take a small group of elite managers — every one with returns of 40% per annum sustained over at least three years, more than $1 billion under management, and the stock representing at least 5% of the fund — and run each disclosed position through my own screen: the chart, the MACD, the quality metrics, and live analyst sentiment. The managers do the discovery. We do the discipline.

Filings are a useful starting point, not a finishing line. They are published with a delay, so a manager may have trimmed or exited before you see the position. And a great manager owning a stock tells you nothing about whether now is the right time on the chart. My job is to separate the positions where elite conviction and the technical picture agree from the ones where you would be buying someone else’s exit.

This month’s list covers 39 positions across six managers: Elliott, Kopernik, Marshfield, Abrams Bison, H&H International and Altarock. The backdrop is a defensive rotation into healthcare, an early-July semiconductor selloff after a Q2 doubling, oil round-tripping to $68, and a US labour market that just printed 57,000 jobs. Several of the names are genuinely compelling setups. Several others are quality businesses in exactly the wrong part of the momentum cycle. Knowing which is which is what the full analysis provides.

| The managers narrow the universe. The MACD tells you whether momentum is behind the thesis right now. Use both — neither alone is sufficient. |

JULY 2026 — WHAT IS DRIVING THE LIST

Five macro facts are cutting across virtually every position this month. Understanding them first prevents you from reading individual situations in isolation.

- Middle East and the growth downgrade: the conflict that began in late February remains, in the OECD’s words in its 3 June 2026 Economic Outlook, the dominant force shaping the global economy. The OECD projects global growth slowing from 3.4% in 2025 to 2.8% in 2026, with the US at 2.0%, the UK at 0.9% and China at 4.5%.

- Inflation and the Fed: US inflation reached 4.2% in May 2026, its highest in three years. G20 inflation is projected at 4.0% for 2026, and the Federal Reserve debate has shifted from when to cut towards whether to hike.

- Oil has round-tripped: WTI crude fell to around $68 in the first days of July, down nearly 20% in two weeks and back near its early-March levels, as a fragile ceasefire holds despite the 26 June Strait of Hormuz drone incident, per Schwab and CNBC reporting.

- The tape changed at the end of June: the S&P 500 sits near 7,350, up ~7.7% year to date on an AI capex boom (~$725bn of combined 2026 hyperscaler spending), but semiconductors, which roughly doubled in Q2, fell hard in early July on profit-taking while healthcare became the best-performing sector.

- The labour market is softening: the June US jobs report, released 2 July, showed just 57,000 new jobs, roughly half expectations, with unemployment at 4.2%. That rotation into defensives matters directly to this list.

WHAT THE FRAMEWORK FOUND

Each position receives one of four statuses under my framework: CONFIRMED where momentum and fundamentals support each other, MIXED where the timeframes conflict or material flags exist, COMPROMISED where the monthly MACD regime is bearish and capital preservation takes priority regardless of valuation, and SPECULATIVE where the business is pre-profit or the listing history is too short to classify. This month: 16 CONFIRMED, 18 MIXED, 3 COMPROMISED and 2 SPECULATIVE. Two of the COMPROMISED names are household-name businesses with near-unanimous analyst buy ratings — which is precisely why the framework exists.

ELLIOTT INVESTMENT MANAGEMENT — 3 POSITIONS

| Ranked 11 of 488 hedge fund managers tracked. Portfolio gain of +339% since March 2020. Sharpe ratio 5.94 against a tracked hedge fund average of 1.49. Assets under management $20.1 billion. Three-year annualised return +54.5%. |

Three positions, and a distinctly old-economy tilt at a time when the market’s attention sits almost entirely on AI. One is a refining and midstream giant Elliott has been pressing for over two years, trading at a steep discount with an activist catalyst attached. One is a Canadian integrated oil producer that broke out of a three-year base and is now digesting the oil pullback. The third is an airline where the campaign has already forced board change — and where falling oil is a direct tailwind, meaning Elliott is effectively hedged across the oil price inside its own top positions.

|

| MORE AVAILABLE IN THE ALPESH PATEL SPECIAL EDITION NEWSLETTER – SUBSCRIBERS ONLY. EXISTING APSE SUBSCRIBERS PLEASE REFER TO LATEST NEWSLETTER.

Elliott — Full Analysis — Which of the two energy names has the cleaner technical setup right now — The airline that passes my VGI quality threshold — and the one flagged risk — Exact MACD reads, statuses, 12-month chart projections and analyst coverage for all three Upgrade at sharescope.co.uk/alpeshpatel |

KOPERNIK GLOBAL INVESTORS — 7 POSITIONS

| Ranked 8 of 488 hedge fund managers tracked. Portfolio gain of +555% since January 2016. Sharpe ratio 6.62. Assets under management $1.43 billion. Three-year annualised return +53.0%. |

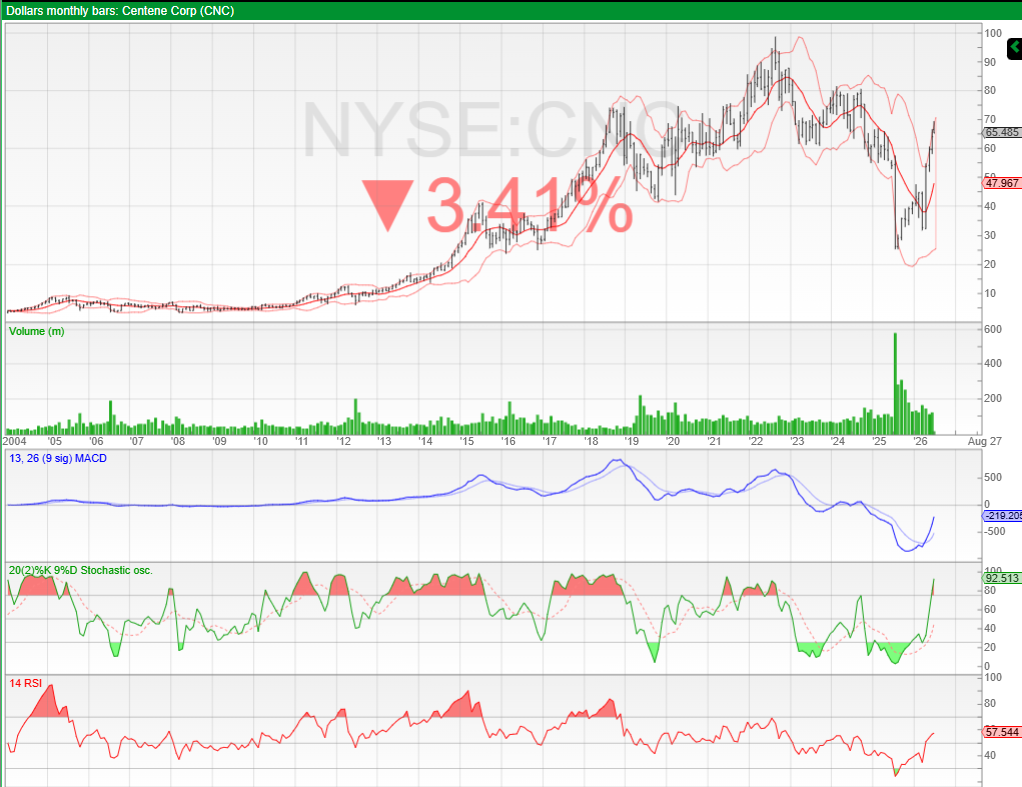

Seven positions and the most uncomfortable book in the report — which is the point. They range from a pre-revenue gold developer with less than a year of cash runway, to Korea’s incumbent telecom on 8 times earnings with completely clean risk checks, to the world’s largest fertiliser producer, to an asset-management turnaround carrying the joint-highest quality score of the month. The standout is a managed care insurer that collapsed through 2025 and now matches my special situation template exactly: monthly MACD rising from deep oversold with the weekly confirming.

One position in this book screens cheap on every fundamental metric and carries a wall of analyst buys — and still received my most cautious classification, because both MACD timeframes are falling together and price has broken its 2025 range floor. The fundamental case may win eventually. The technical case says there is no need to be early.

|

| MORE AVAILABLE IN THE ALPESH PATEL SPECIAL EDITION NEWSLETTER – SUBSCRIBERS ONLY. EXISTING APSE SUBSCRIBERS PLEASE REFER TO LATEST NEWSLETTER.

Kopernik — Full Analysis — The special-situation recovery with a 68% per year earnings growth forecast — The VGI 8 turnaround that just broke a four-year downtrend — and the sell ratings worth respecting — The stock I classify COMPROMISED despite buy ratings from two major banks — Exact MACD reads, statuses and 12-month chart projections for all seven names Upgrade at sharescope.co.uk/alpeshpatel |

MARSHFIELD ASSOCIATES — 10 POSITIONS

| Ranked 2 of 488 hedge fund managers tracked. Portfolio gain of +542% since January 2016. Sharpe ratio 9.05. Assets under management $4.99 billion. Three-year annualised return +51.7%. |

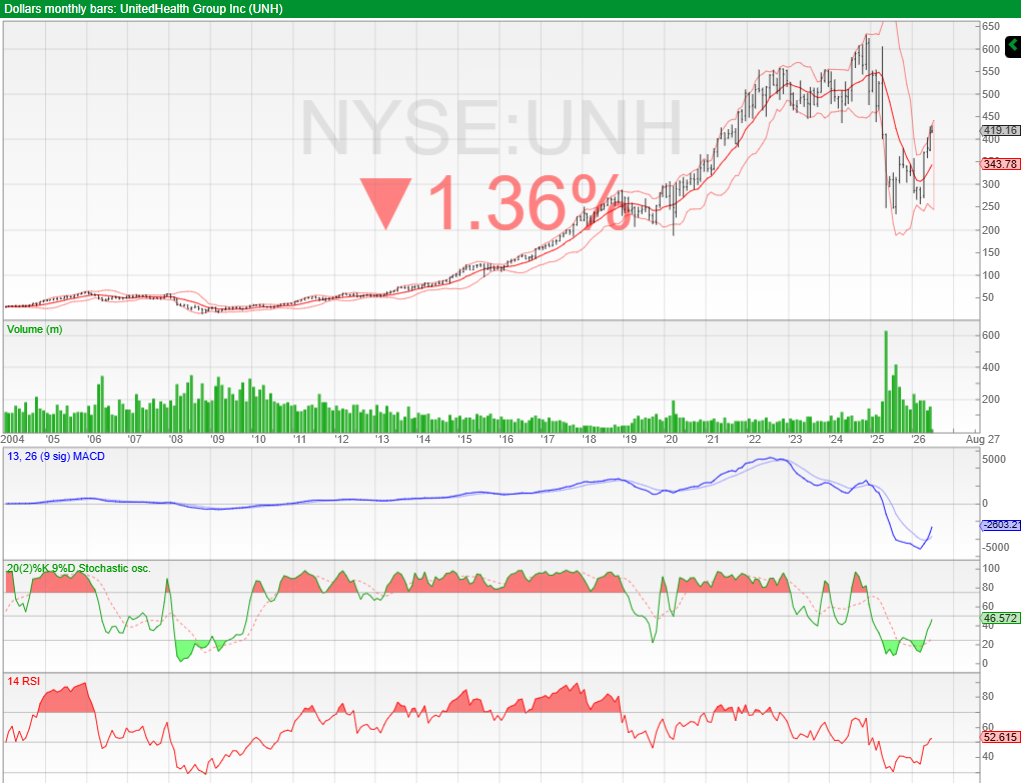

The number two ranked manager in the database, with a Sharpe ratio of 9.05 that is frankly extraordinary: six times the tracked hedge fund average. Ten positions above 5%, the broadest list in the report, all quality: moats, pricing power, duopolies. Two great compounders in the same retail niche sit side by side — and one of them has just triggered the single most cautionary monthly MACD event in my framework after an advance from under $700 to above $4,000. The book also holds the most convincing recovery in the S&P 500, both global payment duopolists through their correction, an off-price retailer at all-time highs riding the trade-down consumer, and the weakest chart in the entire report.

|

| MORE AVAILABLE IN THE ALPESH PATEL SPECIAL EDITION NEWSLETTER – SUBSCRIBERS ONLY. EXISTING APSE SUBSCRIBERS PLEASE REFER TO LATEST NEWSLETTER.

Marshfield — Full Analysis — The compounder that just triggered the Daddy Bear signal — and its healthier twin — The recovery with the highest-asymmetry setup in my playbook, backed by five June buy ratings — Which payments duopolist carries the larger discount — and why two elite managers hold it — The franchise name I say to avoid until the weekly stabilises, whatever the 37% upside consensus says — Exact MACD reads, statuses and 12-month projections for all ten names Upgrade at sharescope.co.uk/alpeshpatel |

ABRAMS BISON INVESTMENTS — 8 POSITIONS

| Ranked 7 of 488 hedge fund managers tracked. Portfolio gain of +535% since January 2016. Sharpe ratio 6.72. Assets under management $2.31 billion. Three-year annualised return +51.1%. |

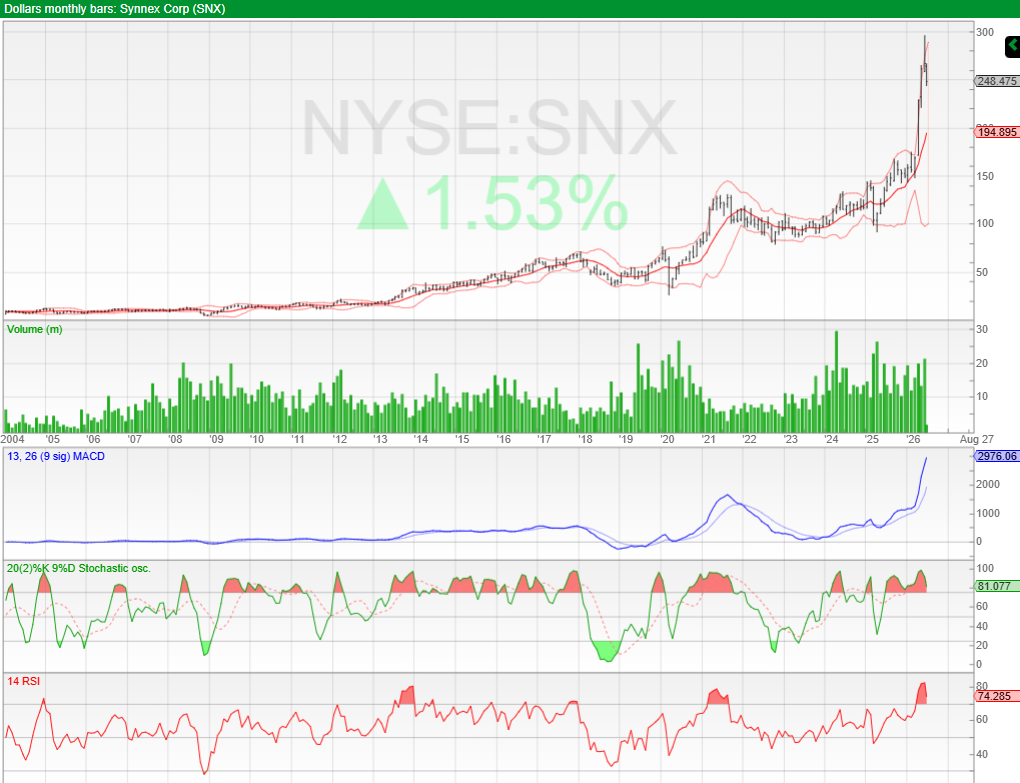

The most eclectic list in the report, from equipment rental to vacuum cleaners to the New York Times. It includes the former FTSE 100 stalwart every UK investor knows, three months into its NYSE relisting; an IT distributor that has gone vertical out of a four-year base and carries the strongest combined fundamental and technical setup of the month; a semiconductor equipment giant that fell 10% in a single session in the July chip selloff; a consumer products compounder with the most eye-catching chart projection in the entire report; and a collapsed medtech attempting the same early-recovery MACD shape as the healthcare names.

|

| MORE AVAILABLE IN THE ALPESH PATEL SPECIAL EDITION NEWSLETTER – SUBSCRIBERS ONLY. EXISTING APSE SUBSCRIBERS PLEASE REFER TO LATEST NEWSLETTER.

Abrams Bison — Full Analysis — The VGI 8 name with a unanimous June buy wall — and the two risks that come with a vertical chart — What the ex-Ashtead relisting means for UK holders, and why my framework cannot classify it yet — The 148% chart projection — what it is, and what it is not — The recovery speculation with real fundamental hair on it, and how I would size it — Exact MACD reads, statuses and 12-month projections for all eight names Upgrade at sharescope.co.uk/alpeshpatel |

H&H INTERNATIONAL INVESTMENT — 6 POSITIONS

| Ranked 10 of 488 hedge fund managers tracked. Portfolio gain of +368% since December 2018. Sharpe ratio 6.00. Assets under management $20.0 billion. Three-year annualised return +49.2%. |

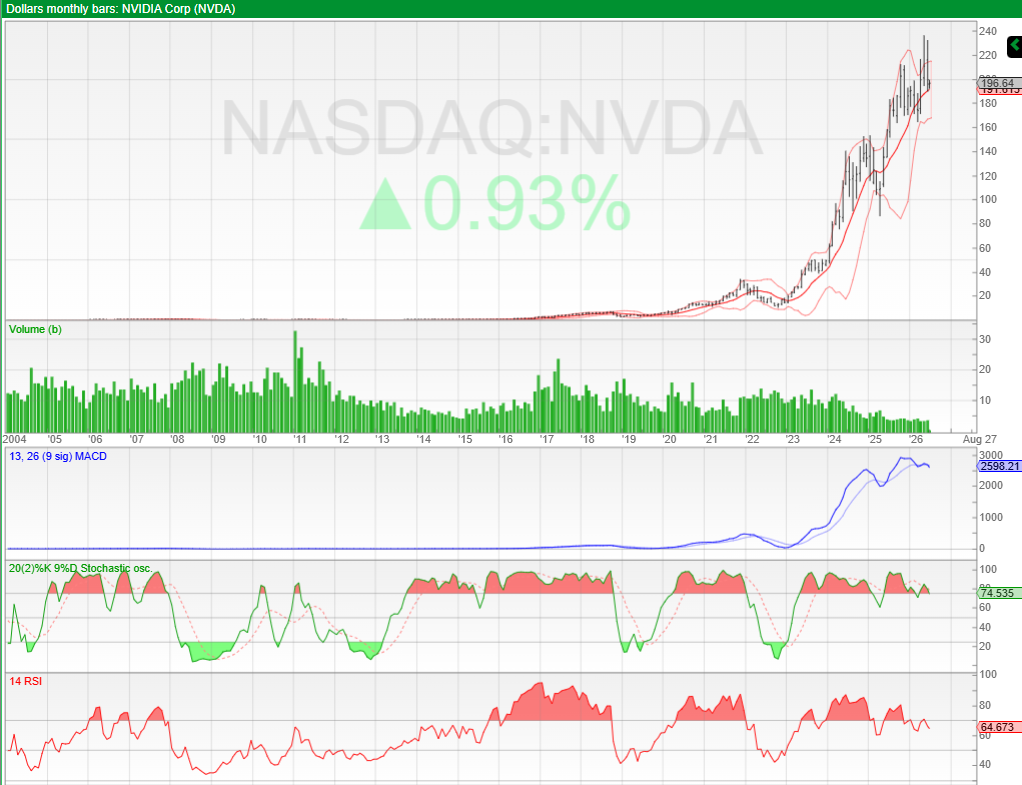

A $20 billion book concentrated in the mega-cap franchises everyone recognises. The value this manager adds is not stock discovery but position sizing and staying power: nearly 50% annualised over three years by holding the obvious in size through every drawdown. This month that means one mega cap at all-time highs, one consolidating sideways on a record cash pile, the axis of the AI trade with its monthly momentum flattening at record extremes, a deep-value China e-commerce name on 7.6 times earnings, a two-year coil awaiting resolution, and the standout mega-cap performer of the past year.

|

| MORE AVAILABLE IN THE ALPESH PATEL SPECIAL EDITION NEWSLETTER – SUBSCRIBERS ONLY. EXISTING APSE SUBSCRIBERS PLEASE REFER TO LATEST NEWSLETTER.

H&H International — Full Analysis — The mega cap whose forward P/E now sits below its own sector average — and what that tells you — The China name where cheapness is real but the catalyst is political, with a defined November deadline — Which of the six charts is confirmed, which is coiling, and which asks only for patience — Exact MACD reads, statuses and 12-month projections for all six names Upgrade at sharescope.co.uk/alpeshpatel |

ALTAROCK PARTNERS — 5 POSITIONS

| Ranked 6 of 488 hedge fund managers tracked. Portfolio gain of +484% since January 2016. Sharpe ratio 6.82. Assets under management $4.13 billion. Three-year annualised return +46.2%. |

Perhaps the purest quality-compounder book in the database: a handful of wide-moat franchises, almost no turnover, and a refusal to own anything without pricing power. Five names, every one a toll road on the modern economy — including the most surprising chart in the report: a mega-cap platform down roughly a third from its 2025 highs, now on its cheapest multiple in years, with the largest analyst consensus upside of the month and 107 buy ratings against zero sells. The tension between that fundamental profile and a falling monthly MACD is exactly the kind of conflict my framework exists to arbitrate.

|

| MORE AVAILABLE IN THE ALPESH PATEL SPECIAL EDITION NEWSLETTER – SUBSCRIBERS ONLY. EXISTING APSE SUBSCRIBERS PLEASE REFER TO LATEST NEWSLETTER.

Altarock — Full Analysis — The fallen mega cap: why the monthly says wait and the weekly says the turn may have begun — The aerospace consolidator at a rare discount — and why its scariest flags are features, not accidents — The dual-conviction payments holding and how I would time the add — Exact MACD reads, statuses and 12-month projections for all five names Upgrade at sharescope.co.uk/alpeshpatel |

ALL 39 POSITIONS — STATUS AT A GLANCE

Below is the complete list with ticker, manager and my framework status. The full write-up on every name — bull case, bear case, exact MACD readings, analyst coverage and 12-month chart projection — is available to Special Edition subscribers.

| Ticker | Company | Manager | Status | Detail |

| PSX | Phillips 66 | Elliott | Confirmed ✓ | Full analysis: APSE only |

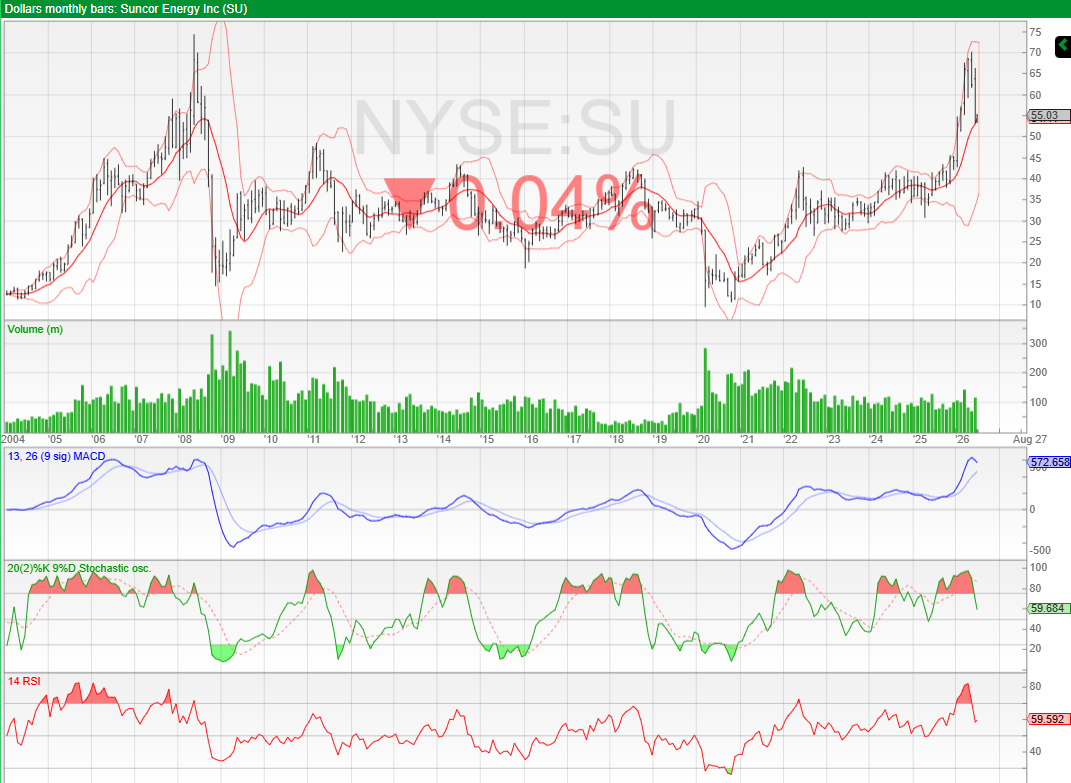

| SU | Suncor Energy | Elliott | Confirmed ✓ | Full analysis: APSE only |

| LUV | Southwest Airlines | Elliott | Confirmed ✓ | Full analysis: APSE only |

| SA | Seabridge Gold | Kopernik | Speculative ⚠ | Full analysis: APSE only |

| RRC | Range Resources | Kopernik | Mixed → | Full analysis: APSE only |

| KT | KT Corporation | Kopernik | Mixed → | Full analysis: APSE only |

| NTR | Nutrien | Kopernik | Mixed → | Full analysis: APSE only |

| CNC | Centene | Kopernik | Confirmed ✓ | Full analysis: APSE only |

| BEN | Franklin Resources | Kopernik | Confirmed ✓ | Full analysis: APSE only |

| EXE | Expand Energy | Kopernik | Compromised ▼ | Full analysis: APSE only |

| AZO | AutoZone | Marshfield | Compromised ▼ | Full analysis: APSE only |

| UNH | UnitedHealth Group | Marshfield | Confirmed ✓ | Full analysis: APSE only |

| PGR | Progressive | Marshfield | Mixed → | Full analysis: APSE only |

| ROST | Ross Stores | Marshfield | Confirmed ✓ | Full analysis: APSE only |

| V | Visa | Marshfield | Mixed → | Full analysis: APSE only |

| MA | Mastercard | Marshfield | Mixed → | Full analysis: APSE only |

| ORLY | O’Reilly Automotive | Marshfield | Mixed → | Full analysis: APSE only |

| ACGL | Arch Capital Group | Marshfield | Mixed → | Full analysis: APSE only |

| DPZ | Domino’s Pizza | Marshfield | Compromised ▼ | Full analysis: APSE only |

| EXPD | Expeditors International | Marshfield | Confirmed ✓ | Full analysis: APSE only |

| SUNB | Sunbelt Rentals Holdings | Abrams Bison | Speculative ⚠ | Full analysis: APSE only |

| SNX | TD SYNNEX | Abrams Bison | Confirmed ✓ | Full analysis: APSE only |

| AMAT | Applied Materials | Abrams Bison | Confirmed ✓ | Full analysis: APSE only |

| SN | SharkNinja | Abrams Bison | Confirmed ✓ | Full analysis: APSE only |

| URBN | Urban Outfitters | Abrams Bison | Mixed → | Full analysis: APSE only |

| TFX | Teleflex | Abrams Bison | Mixed → | Full analysis: APSE only |

| NYT | New York Times | Abrams Bison | Confirmed ✓ | Full analysis: APSE only |

| BFAM | Bright Horizons Family Solutions | Abrams Bison | Mixed → | Full analysis: APSE only |

| AAPL | Apple | H&H International | Confirmed ✓ | Full analysis: APSE only |

| BRK.B | Berkshire Hathaway (B) | H&H International | Mixed → | Full analysis: APSE only |

| NVDA | Nvidia | H&H International | Confirmed ✓ | Full analysis: APSE only |

| PDD | PDD Holdings | H&H International | Mixed → | Full analysis: APSE only |

| TSLA | Tesla | H&H International | Mixed → | Full analysis: APSE only |

| GOOG | Alphabet (Class C) | H&H International | Confirmed ✓ | Full analysis: APSE only |

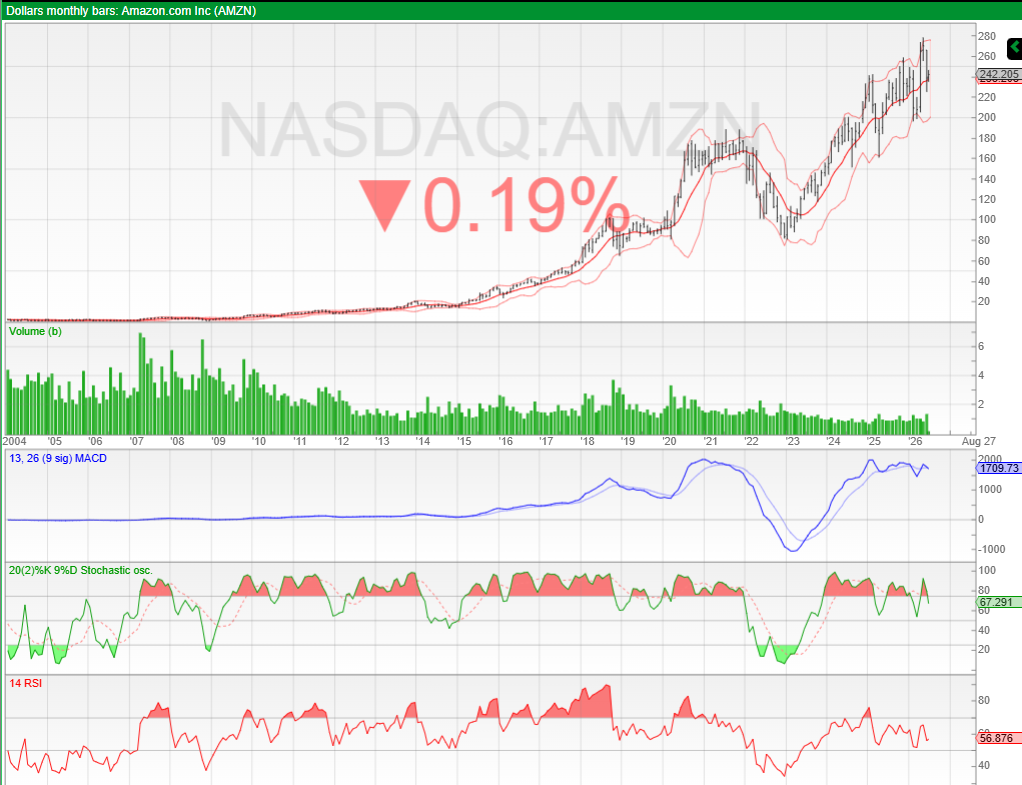

| AMZN | Amazon.com | Altarock | Confirmed ✓ | Full analysis: APSE only |

| TDG | TransDigm Group | Altarock | Mixed → | Full analysis: APSE only |

| MSFT | Microsoft | Altarock | Mixed → | Full analysis: APSE only |

| MCO | Moody’s | Altarock | Mixed → | Full analysis: APSE only |

| MA | Mastercard | Altarock | Mixed → | Full analysis: APSE only |

HOW TO USE SHARESCOPE ON THIS LIST

You do not need the full analysis to start working with this universe in ShareScope. Here is a simple starting workflow:

- Pull up the monthly chart first — before reading any filing, fair value estimate or analyst note. In my framework the monthly is the climate and the weekly is the weather. When they conflict, the monthly wins.

- Add MACD (12,26,9) on both timeframes: monthly above signal and rising means the climate supports the position. Monthly below signal and falling means capital preservation comes first, whatever the valuation says.

- Run the quality check with the APSE Value/Growth filter — ROCE, earnings growth and cash conversion are your anchors. A stock that passes the chart test but fails the quality filter is a trade, not an investment.

- Respect the filing lag: these positions come from regulatory filings published with a delay. Any manager may have added, trimmed or exited since. Verify the current chart before acting on anything here.

- Size to the status: CONFIRMED names can carry full position sizes. MIXED names deserve half-size or a staged entry. COMPROMISED and SPECULATIVE names belong on the watchlist or at 1–2% of portfolio maximum.

- Double check and analyse for yourself always. Markets move fast and things can have moved significantly even by the time I finish writing this sentence.

| The names on this list range from quality compounders backed by the highest-Sharpe managers in the world to businesses in exactly the wrong part of the momentum cycle. The full analysis tells you which is which. The MACD and quality filter in ShareScope are your tools for staying on the right side of that distinction. |

| MORE AVAILABLE IN THE ALPESH PATEL SPECIAL EDITION NEWSLETTER – SUBSCRIBERS ONLY. EXISTING APSE SUBSCRIBERS PLEASE REFER TO LATEST NEWSLETTER.

Want the Full Analysis on All 39 Positions? — The complete write-up on every name: exact MACD readings, analyst coverage, bull and bear case, risk flags, and a 12-month chart projection — The statuses explained per stock, including the two household names classified COMPROMISED — Plus APSE filter layouts pre-loaded in ShareScope so you can run the quality screen yourself Upgrade at sharescope.co.uk/alpeshpatel |

Alpesh Patel OBE | @alpeshbp | www.alpeshpatel.com/sharescope

www.campaignforamillion.com | www.alpeshpatel.com/shares

This article is for informational and educational purposes only. It does not constitute personalised investment guidance, a financial promotion, or a recommendation to buy or sell any security. Hedge fund positions are drawn from public regulatory filings which are published with a delay and may no longer reflect current holdings. Price projections shown are chart-derived trend illustrations, not forecasts or price targets. The value of investments can fall as well as rise and you may receive back less than you invest. All data as of July 2026. Always conduct your own due diligence. Alpesh Patel OBE provides mentoring and education, not regulated financial advice.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.