Stepping in for Bruce this week, Jamie Ward looks at the ever-shrinking London Stock Exchange as well as a couple of sources of possible further shrinkage; namely the BREE/MSLH rejected merger and the DCC takeover. He then rounds it off with a discussion on whether TUNE is finally emerging from its post-COVID slump.

Living through the final few months of 2008 as an equity analyst was unlike anything I’d experienced before. During October and November, the global banking system appeared to be unravelling. The mood was one of outright panic with slightly macabre jokes in the office about whether we will still have jobs tomorrow. For those of us managing money through it, it genuinely felt as though investing itself might not survive – a sort of capital markets extinction event. Markets looked broken and, for a while, even capitalism seemed to be in question.

The roots of that crisis stretched back many years. Banks had become dangerously leveraged, encouraged by an era of exceptionally loose monetary policy. Much of the responsibility for that sits with the US Federal Reserve under Alan Greenspan, whose death in June, aged 100, has prompted renewed debate about his legacy. The opinions seem to vary from his tenure wasn’t so bad really to yes it really was that bad.

Greenspan began his intellectual life as a disciple of Ayn Rand and a champion of free markets. Yet during his tenure as Federal Reserve chairman, from 1987 onwards, he repeatedly cut interest rates whenever markets ran into trouble. This approach stood at complete odds with Rand’s philosophy of objectivism. Investors quickly assumed the Federal Reserve would always step in to cushion losses, establishing the market dynamic known as the Greenspan Put.

Combined with the wave of banking deregulation during the Clinton years, such as the replacement of the 1933 Glass-Steagall Act, this encouraged an enormous build-up of debt and risk-taking. By the time Ben Bernanke succeeded Greenspan in 2006, the foundations of the crisis had already been laid.

When the bubble finally burst in 2008, the consequences were severe. With the benefit of hindsight, the event resembled the beginning of an ice age rather than a sudden meteor strike. The crisis itself did not inflict the lasting damage on the London Stock Exchange; that came via the regulatory reaction afterwards.

In the years that followed, regulators understandably focused on making the financial system safer. The result was a much heavier compliance burden. Reforms such as MiFIDII also fragmented trading across multiple venues, weakening the central order books that had traditionally supported liquidity and price discovery. These changes undoubtedly reduced the chances of another banking crisis, but they also made UK public markets less attractive and less efficient.

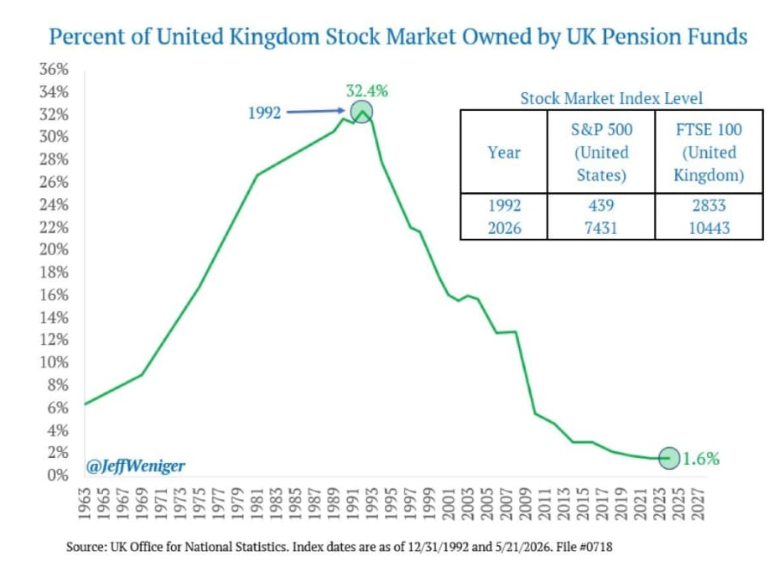

At the same time, domestic institutional investors steadily retreated from UK equities. In 1992, pension and insurance funds owned 32% of the UK stock market. Today, it is a fraction of that at around 1.2%. Accounting changes such as FRS 17 (which changed the accounting for pension funds) and the rise of liability-driven investment encouraged pension funds to favour bonds over equities, removing one of the market’s most important sources of long-term capital.

The knock-on effects have been nasty. Money has increasingly flowed into passive funds, private equity and venture capital instead. Meanwhile, many smaller quoted companies have been left trading on very low valuations, not because their businesses are poor, but because there are too few institutions willing or able to own them. Faced with high listing costs, greater scrutiny and a lack of investor support, many businesses now conclude they’re better off staying private.

The post-crisis freeze shows up clearly in the listings data. London listings peaked immediately prior to the financial crisis at over 3,200 businesses, but the ensuing ice age has effectively halved the size of the domestic market, dragging the corporate sector down to fewer than 1,800 listed issuers today.

|

Year

|

LSE Main Market Issuers

|

AIM Listed Companies

|

Combined Listed Corporate Sector

|

|

1995

|

2,050

|

121

|

2,171

|

|

2005

|

1,623

|

1,399

|

3,022

|

|

2007 (Peak)

|

1,515

|

1,694

|

3,209

|

|

2015

|

1,196

|

1,044

|

2,240

|

|

2025

|

1,065

|

704

|

1,769

|

With fewer listed companies and depressed valuations, London has increasingly become a hunting ground for overseas buyers and private equity firms. In recent years we have seen businesses including Schroders and Darktrace disappear from the market, while Segro and DCC have both rejected takeover approaches.

By the middle of 2026, announced foreign takeovers of UK companies had reached record levels, with deals worth around $231 billion. Many were profitable, well-managed companies that simply found greater value outside the UK public market than within it.

The financial crisis of 2008 felt like the end of the world at the time. In reality, the bigger threat to the UK stock market has proved to be the slow erosion that followed. Rather than one dramatic collapse, it’s been a gradual decline, driven by regulation and the steady withdrawal of domestic capital.

The ongoing wave of corporate departures underlines the problem. Marshalls and DCC both show how public market undervaluation invites corporate suitors, while Focusrite offers a glimpse of a business attempting to navigate its way out of a cyclical trough

Marshalls/Breedon Proposed Merger

Sky News reported this week that Breedon approached Marshalls earlier this year about a possible all-share merger. Marshalls rejected the proposal and there are no active discussions, but the thinking behind the approach is easy enough to understand. Both companies are well managed and both are having to contend with one of the weakest UK construction markets in years. If you’re Breedon, trying to buy a quality business in an adjacent business area while the sector is out of favour is a perfectly sensible idea.

The proposed structure is perhaps more debatable. An all-share deal at this point in the cycle amounts to using one set of undervalued shares to buy another, so that much of the valuation benefit is diminished – albeit arguably Marshalls is more undervalued than Breedon.

A cash offer would have been more attractive if Breedon wanted to take full advantage of depressed prices. The problem is that Breedon already carries a fair amount of debt (net debt stands at roughly double forecast EBITDA), leaving little room to finance an acquisition of this size without stretching the balance sheet.

There would undoubtedly be operational benefits from combining the two businesses, although the overlap between them isn’t especially large. This feels less like a classic cost-cutting merger and more like an opportunity to build greater scale while adding another high-quality set of assets.

Valuation

Before the pandemic, Marshalls was one of the market’s favourite building materials companies. Investors were willing to pay a substantial premium for its consistent returns and strong market position. The slowdown in construction has changed that picture completely.

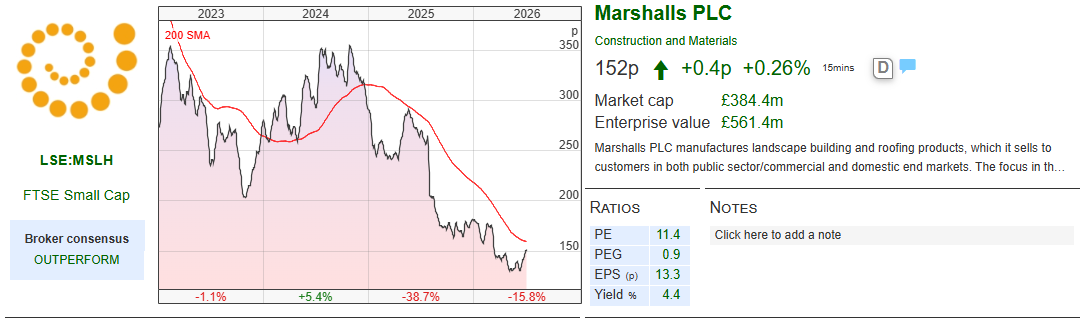

Today, Marshalls trades at around 150p, giving it a market value of roughly £384 million having traded higher than 800p a few years ago. Breedon, by comparison, trades at around 312p with a market value of just over £1 billion. A merger of the two companies would create a construction materials group with a combined market capitalisation of around £1.5 billion. While Breedon remains a decent compounder, today’s depressed valuations mean Marshalls arguably offers greater recovery potential if UK construction activity turns.

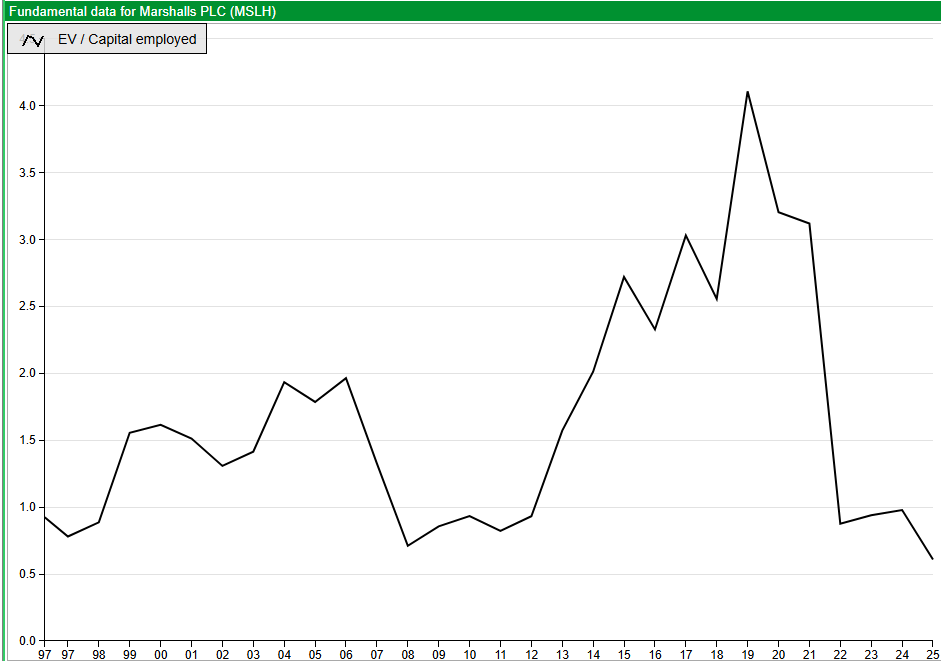

On some measures Marshalls (above) is cheaper than the depths of the GFC, but this is also true of Breedon (below).

My View

Breedon’s interest makes strategic sense. Acquiring a good business when sentiment is weak is often how the best deals are made, and had the merger gone ahead it could have proved rewarding over the long term for Breedon shareholders.

That said, if I were looking for exposure to a recovery in UK construction as a private investor, I’d be more inclined to look at Marshalls. Its earnings have been hit hard by the downturn, which also means they should recover strongly if activity picks up.

Investors willing to take on more risk could look even further down the quality spectrum. Companies such as SIG, Lords Trading and Speedy Hire are exposed to many of the same end markets and have seen their share prices fall even further. If the construction cycle turns, they could deliver larger percentage gains, but the risks are also higher.

Breedon remains a decent business with a management team that has earned a strong reputation over many years, while Marshalls is still a high-quality company despite its recent struggles. I’ve owned both in the past. For now, though, I’d be happy to wait until there’s clearer evidence that UK construction is turning before committing fresh capital to either.

Marshalls is clearly cheap. A cash acquirer could do well here and one wonders whether any private equity firms are looking at Marshalls.

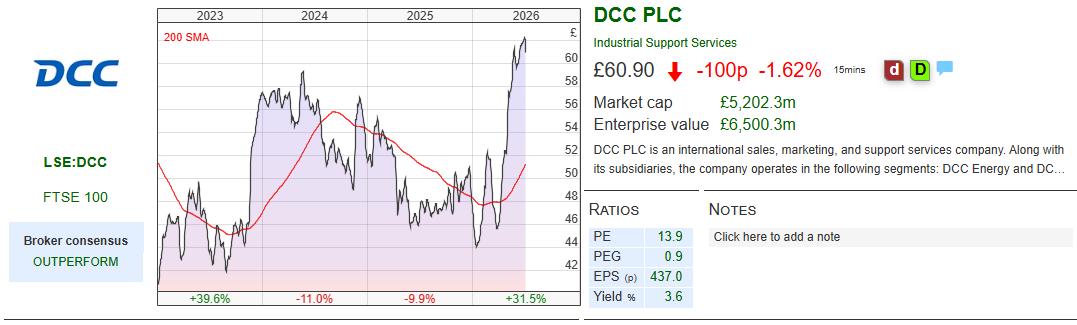

DCC Shareholders Rejecting Bid

Several of DCC’s largest shareholders have publicly opposed the revised takeover proposal from private equity firms KKR and Energy Capital Partners. This week Aviva Investors joined Ninety One and Fidelity in arguing that the offer undervalues the business, making it increasingly difficult for the bidders to secure shareholder support.

Their position isn’t difficult to understand. DCC has gone through a period where investors have questioned its long-term growth prospects, particularly given concerns about the future of fossil fuel distribution. Operationally however, the business has continued to perform well. In 2022, management set a target of delivering £830 million of operating profit by 2030, and with one notable exception the company has consistently remained on track, or ahead of plan.

That exception came during the energy crisis, when surging oil prices reduced fuel demand and temporarily weighed on distribution volumes. Even then, the underlying business remained resilient. Management has used the period to reshape the portfolio, selling the healthcare division and parts of the technology business while returning surplus cash to shareholders through share buybacks. The remainder of the technology business is slated to be sold later this year. It’s difficult to know how much DCC will receive for it but using Midwich (which is similar to DCC’s remaining technology business) as a guide, a value of £300m to £500m seems reasonable.

Valuation

The first approach from KKR and Energy Capital Partners, made in April, valued DCC at £58 per share in cash – a paltry premium to the pre-bid share price of c. £50. A revised proposal increased this to £65.25 per share, plus £1.47 in dividends, taking the total value to around £66.72.

Although the DCC board indicated it would be prepared to recommend the improved offer, several major shareholders clearly disagree. They believe the bid still fails to reflect the company’s long-term earnings potential, cash generation and portfolio of high-quality assets.

Valuation is subjective, but there is a reasonable argument that DCC is worth substantially more than the current offer if management continues to execute successfully over the next few years. Simplistically, the company should be generating £830m+ in EBIT in 2030 with as much as £500m to come back from the technology biz sale. That would leave a clean enterprise value of around £6b. This implies 7.5x EV/EBIT. That seems pretty low for a company that is still growing reasonably well.

My View

This is a familiar pattern in markets. When sentiment towards a good business deteriorates, private equity often steps in before public investors regain confidence. That appears to be what’s happening here.

The bidders are trying to acquire a high-quality company at a point when its valuation is still being held back by concerns over the energy transition. Whether those concerns prove justified remains to be seen, but DCC has demonstrated an ability to adapt its portfolio and allocate capital sensibly over many years.

What’s interesting is the view of several large institutional shareholders. Fund managers at Ninety One, Fidelity and Aviva Investors have all publicly argued that the current proposal is too low, increasing the likelihood that the bidders will either have to improve their offer or walk away.

I’ve followed DCC for several years and continue to think it’s one of the more underappreciated businesses in the FTSE 100. Given that DCC management built the modern group by executing over 300 disciplined, low-price acquisitions over the last three decades, it would be sadly ironic if the parent company itself was taken out so cheaply.

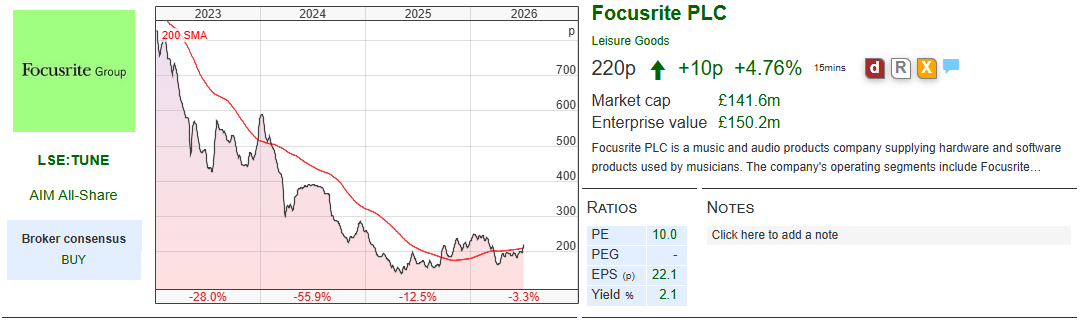

Focusrite Full-Year Results

Focusrite’s latest results suggest the business is finally getting back onto a more even footing after the post-pandemic slowdown. The stock has had a difficult few years as retailers worked through excess inventory, but that process now appears to be largely over. Trading is improving and the company delivered pro-forma adjusted EBITDA of £24.7 million despite a fairly tough backdrop.

One of the more interesting announcements was the development of a new hardware platform using Focusrite’s own chips. It’s still early days, but designing more of its own technology should give the company greater control over its products, reduce its reliance on outside suppliers and, hopefully, improve margins over time.

Not everything went to plan. Focusrite took a £9.8 million write-down on its Sequential synthesiser business after weaker demand and the closure of one of its US manufacturing partners. Production is already being moved elsewhere, so management appears to have dealt with the issue quickly.

The balance sheet also looks much healthier than it did a year ago. Net debt has fallen from £17.9 million to £8.6 million, helped by strong cash generation and lower working capital.

Valuation

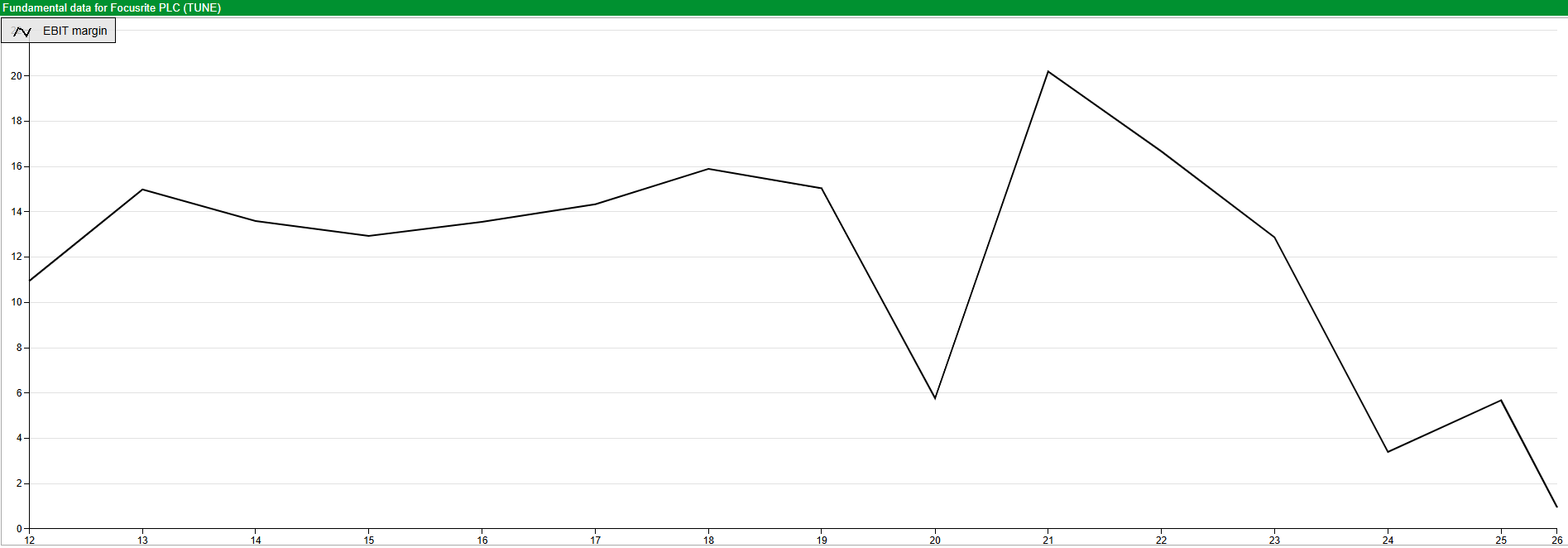

The shares currently trade just over 220p. Based on pro-forma earnings of 15.6p per share, that’s roughly 14 times earnings. But that 15.6p is still quite a way below where it was pre-COVID when the business was quite a bit smaller. Margins remain low and the opportunity is if they ever recover to levels seen in c. 2018/19 then EPS would be a lot higher than 15.6p.

Even if a margin rebound isn’t on the cards, 14 times hardly seems demanding.

My View

Focusrite was one of the big winners during lockdown as people bought equipment to record music and podcasts from home. It was always likely that demand would cool once life returned to normal, but I think the market has overreacted. The good times were extrapolated to fanciful levels so that the share price got above 1800p, now it seems that the bad times are being over extrapolated.

The latest results suggest the business has come through the worst of it. Inventory problems are fading, debt is falling and trading has started to improve again. The move towards using its own chips is another positive, although the benefits will take time to come through.

The write-down at Sequential is disappointing, but it doesn’t change my view of the wider business.

Focusrite feels like one of those businesses that is underearning and is trading on a low valuation to depressed earnings. If that’s true then eventually the shares have to reflect that it is a better business than the share price suggests. I bought shares in Focusrite about 18 months ago and whilst I have done reasonably well already, I’m not minded to sell out at anything like current levels.

Jamie Ward

@JamieCDubya

https://wonderstcks.substack.com/

Notes: Jamie owns shares in DCC and Focusrite

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Bi-Weekly Market Commentary | 08/07/2026 | BREE, MSLH, DCC, TUNE | The shrinking UK stock market

Stepping in for Bruce this week, Jamie Ward looks at the ever-shrinking London Stock Exchange as well as a couple of sources of possible further shrinkage; namely the BREE/MSLH rejected merger and the DCC takeover. He then rounds it off with a discussion on whether TUNE is finally emerging from its post-COVID slump.

Living through the final few months of 2008 as an equity analyst was unlike anything I’d experienced before. During October and November, the global banking system appeared to be unravelling. The mood was one of outright panic with slightly macabre jokes in the office about whether we will still have jobs tomorrow. For those of us managing money through it, it genuinely felt as though investing itself might not survive – a sort of capital markets extinction event. Markets looked broken and, for a while, even capitalism seemed to be in question.

The roots of that crisis stretched back many years. Banks had become dangerously leveraged, encouraged by an era of exceptionally loose monetary policy. Much of the responsibility for that sits with the US Federal Reserve under Alan Greenspan, whose death in June, aged 100, has prompted renewed debate about his legacy. The opinions seem to vary from his tenure wasn’t so bad really to yes it really was that bad.

Greenspan began his intellectual life as a disciple of Ayn Rand and a champion of free markets. Yet during his tenure as Federal Reserve chairman, from 1987 onwards, he repeatedly cut interest rates whenever markets ran into trouble. This approach stood at complete odds with Rand’s philosophy of objectivism. Investors quickly assumed the Federal Reserve would always step in to cushion losses, establishing the market dynamic known as the Greenspan Put.

Combined with the wave of banking deregulation during the Clinton years, such as the replacement of the 1933 Glass-Steagall Act, this encouraged an enormous build-up of debt and risk-taking. By the time Ben Bernanke succeeded Greenspan in 2006, the foundations of the crisis had already been laid.

When the bubble finally burst in 2008, the consequences were severe. With the benefit of hindsight, the event resembled the beginning of an ice age rather than a sudden meteor strike. The crisis itself did not inflict the lasting damage on the London Stock Exchange; that came via the regulatory reaction afterwards.

In the years that followed, regulators understandably focused on making the financial system safer. The result was a much heavier compliance burden. Reforms such as MiFIDII also fragmented trading across multiple venues, weakening the central order books that had traditionally supported liquidity and price discovery. These changes undoubtedly reduced the chances of another banking crisis, but they also made UK public markets less attractive and less efficient.

At the same time, domestic institutional investors steadily retreated from UK equities. In 1992, pension and insurance funds owned 32% of the UK stock market. Today, it is a fraction of that at around 1.2%. Accounting changes such as FRS 17 (which changed the accounting for pension funds) and the rise of liability-driven investment encouraged pension funds to favour bonds over equities, removing one of the market’s most important sources of long-term capital.

The knock-on effects have been nasty. Money has increasingly flowed into passive funds, private equity and venture capital instead. Meanwhile, many smaller quoted companies have been left trading on very low valuations, not because their businesses are poor, but because there are too few institutions willing or able to own them. Faced with high listing costs, greater scrutiny and a lack of investor support, many businesses now conclude they’re better off staying private.

The post-crisis freeze shows up clearly in the listings data. London listings peaked immediately prior to the financial crisis at over 3,200 businesses, but the ensuing ice age has effectively halved the size of the domestic market, dragging the corporate sector down to fewer than 1,800 listed issuers today.

Year

LSE Main Market Issuers

AIM Listed Companies

Combined Listed Corporate Sector

1995

2,050

121

2,171

2005

1,623

1,399

3,022

2007 (Peak)

1,515

1,694

3,209

2015

1,196

1,044

2,240

2025

1,065

704

1,769

With fewer listed companies and depressed valuations, London has increasingly become a hunting ground for overseas buyers and private equity firms. In recent years we have seen businesses including Schroders and Darktrace disappear from the market, while Segro and DCC have both rejected takeover approaches.

By the middle of 2026, announced foreign takeovers of UK companies had reached record levels, with deals worth around $231 billion. Many were profitable, well-managed companies that simply found greater value outside the UK public market than within it.

The financial crisis of 2008 felt like the end of the world at the time. In reality, the bigger threat to the UK stock market has proved to be the slow erosion that followed. Rather than one dramatic collapse, it’s been a gradual decline, driven by regulation and the steady withdrawal of domestic capital.

The ongoing wave of corporate departures underlines the problem. Marshalls and DCC both show how public market undervaluation invites corporate suitors, while Focusrite offers a glimpse of a business attempting to navigate its way out of a cyclical trough

Marshalls/Breedon Proposed Merger

Sky News reported this week that Breedon approached Marshalls earlier this year about a possible all-share merger. Marshalls rejected the proposal and there are no active discussions, but the thinking behind the approach is easy enough to understand. Both companies are well managed and both are having to contend with one of the weakest UK construction markets in years. If you’re Breedon, trying to buy a quality business in an adjacent business area while the sector is out of favour is a perfectly sensible idea.

The proposed structure is perhaps more debatable. An all-share deal at this point in the cycle amounts to using one set of undervalued shares to buy another, so that much of the valuation benefit is diminished – albeit arguably Marshalls is more undervalued than Breedon.

A cash offer would have been more attractive if Breedon wanted to take full advantage of depressed prices. The problem is that Breedon already carries a fair amount of debt (net debt stands at roughly double forecast EBITDA), leaving little room to finance an acquisition of this size without stretching the balance sheet.

There would undoubtedly be operational benefits from combining the two businesses, although the overlap between them isn’t especially large. This feels less like a classic cost-cutting merger and more like an opportunity to build greater scale while adding another high-quality set of assets.

Valuation

Before the pandemic, Marshalls was one of the market’s favourite building materials companies. Investors were willing to pay a substantial premium for its consistent returns and strong market position. The slowdown in construction has changed that picture completely.

Today, Marshalls trades at around 150p, giving it a market value of roughly £384 million having traded higher than 800p a few years ago. Breedon, by comparison, trades at around 312p with a market value of just over £1 billion. A merger of the two companies would create a construction materials group with a combined market capitalisation of around £1.5 billion. While Breedon remains a decent compounder, today’s depressed valuations mean Marshalls arguably offers greater recovery potential if UK construction activity turns.

On some measures Marshalls (above) is cheaper than the depths of the GFC, but this is also true of Breedon (below).

My View

Breedon’s interest makes strategic sense. Acquiring a good business when sentiment is weak is often how the best deals are made, and had the merger gone ahead it could have proved rewarding over the long term for Breedon shareholders.

That said, if I were looking for exposure to a recovery in UK construction as a private investor, I’d be more inclined to look at Marshalls. Its earnings have been hit hard by the downturn, which also means they should recover strongly if activity picks up.

Investors willing to take on more risk could look even further down the quality spectrum. Companies such as SIG, Lords Trading and Speedy Hire are exposed to many of the same end markets and have seen their share prices fall even further. If the construction cycle turns, they could deliver larger percentage gains, but the risks are also higher.

Breedon remains a decent business with a management team that has earned a strong reputation over many years, while Marshalls is still a high-quality company despite its recent struggles. I’ve owned both in the past. For now, though, I’d be happy to wait until there’s clearer evidence that UK construction is turning before committing fresh capital to either.

Marshalls is clearly cheap. A cash acquirer could do well here and one wonders whether any private equity firms are looking at Marshalls.

DCC Shareholders Rejecting Bid

Several of DCC’s largest shareholders have publicly opposed the revised takeover proposal from private equity firms KKR and Energy Capital Partners. This week Aviva Investors joined Ninety One and Fidelity in arguing that the offer undervalues the business, making it increasingly difficult for the bidders to secure shareholder support.

Their position isn’t difficult to understand. DCC has gone through a period where investors have questioned its long-term growth prospects, particularly given concerns about the future of fossil fuel distribution. Operationally however, the business has continued to perform well. In 2022, management set a target of delivering £830 million of operating profit by 2030, and with one notable exception the company has consistently remained on track, or ahead of plan.

That exception came during the energy crisis, when surging oil prices reduced fuel demand and temporarily weighed on distribution volumes. Even then, the underlying business remained resilient. Management has used the period to reshape the portfolio, selling the healthcare division and parts of the technology business while returning surplus cash to shareholders through share buybacks. The remainder of the technology business is slated to be sold later this year. It’s difficult to know how much DCC will receive for it but using Midwich (which is similar to DCC’s remaining technology business) as a guide, a value of £300m to £500m seems reasonable.

Valuation

The first approach from KKR and Energy Capital Partners, made in April, valued DCC at £58 per share in cash – a paltry premium to the pre-bid share price of c. £50. A revised proposal increased this to £65.25 per share, plus £1.47 in dividends, taking the total value to around £66.72.

Although the DCC board indicated it would be prepared to recommend the improved offer, several major shareholders clearly disagree. They believe the bid still fails to reflect the company’s long-term earnings potential, cash generation and portfolio of high-quality assets.

Valuation is subjective, but there is a reasonable argument that DCC is worth substantially more than the current offer if management continues to execute successfully over the next few years. Simplistically, the company should be generating £830m+ in EBIT in 2030 with as much as £500m to come back from the technology biz sale. That would leave a clean enterprise value of around £6b. This implies 7.5x EV/EBIT. That seems pretty low for a company that is still growing reasonably well.

My View

This is a familiar pattern in markets. When sentiment towards a good business deteriorates, private equity often steps in before public investors regain confidence. That appears to be what’s happening here.

The bidders are trying to acquire a high-quality company at a point when its valuation is still being held back by concerns over the energy transition. Whether those concerns prove justified remains to be seen, but DCC has demonstrated an ability to adapt its portfolio and allocate capital sensibly over many years.

What’s interesting is the view of several large institutional shareholders. Fund managers at Ninety One, Fidelity and Aviva Investors have all publicly argued that the current proposal is too low, increasing the likelihood that the bidders will either have to improve their offer or walk away.

I’ve followed DCC for several years and continue to think it’s one of the more underappreciated businesses in the FTSE 100. Given that DCC management built the modern group by executing over 300 disciplined, low-price acquisitions over the last three decades, it would be sadly ironic if the parent company itself was taken out so cheaply.

Focusrite Full-Year Results

Focusrite’s latest results suggest the business is finally getting back onto a more even footing after the post-pandemic slowdown. The stock has had a difficult few years as retailers worked through excess inventory, but that process now appears to be largely over. Trading is improving and the company delivered pro-forma adjusted EBITDA of £24.7 million despite a fairly tough backdrop.

One of the more interesting announcements was the development of a new hardware platform using Focusrite’s own chips. It’s still early days, but designing more of its own technology should give the company greater control over its products, reduce its reliance on outside suppliers and, hopefully, improve margins over time.

Not everything went to plan. Focusrite took a £9.8 million write-down on its Sequential synthesiser business after weaker demand and the closure of one of its US manufacturing partners. Production is already being moved elsewhere, so management appears to have dealt with the issue quickly.

The balance sheet also looks much healthier than it did a year ago. Net debt has fallen from £17.9 million to £8.6 million, helped by strong cash generation and lower working capital.

Valuation

The shares currently trade just over 220p. Based on pro-forma earnings of 15.6p per share, that’s roughly 14 times earnings. But that 15.6p is still quite a way below where it was pre-COVID when the business was quite a bit smaller. Margins remain low and the opportunity is if they ever recover to levels seen in c. 2018/19 then EPS would be a lot higher than 15.6p.

Even if a margin rebound isn’t on the cards, 14 times hardly seems demanding.

My View

Focusrite was one of the big winners during lockdown as people bought equipment to record music and podcasts from home. It was always likely that demand would cool once life returned to normal, but I think the market has overreacted. The good times were extrapolated to fanciful levels so that the share price got above 1800p, now it seems that the bad times are being over extrapolated.

The latest results suggest the business has come through the worst of it. Inventory problems are fading, debt is falling and trading has started to improve again. The move towards using its own chips is another positive, although the benefits will take time to come through.

The write-down at Sequential is disappointing, but it doesn’t change my view of the wider business.

Focusrite feels like one of those businesses that is underearning and is trading on a low valuation to depressed earnings. If that’s true then eventually the shares have to reflect that it is a better business than the share price suggests. I bought shares in Focusrite about 18 months ago and whilst I have done reasonably well already, I’m not minded to sell out at anything like current levels.

Jamie Ward

@JamieCDubya

https://wonderstcks.substack.com/

Notes: Jamie owns shares in DCC and Focusrite

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.