David Stevenson explores how shifting geopolitics may shape long-term markets, from gold and inflation fears to rising defence spending in Asia. He also highlights a resilient compounding investment trust and why income strategies could regain their appeal in volatile markets.

In this month’s funds article, we hazard a few guesses about the long-term impact of wars, focus on a steady compounding investment trust and suggest a closer look at the Asian defence spending surge – and an accompanying ETF. We also tentatively suggest that now might be a good time to revisit gold and silver.

Writing a monthly article about markets and funds is quite challenging at the moment, with nearly daily shifts in rhetoric around the Iran crisis/war/exercise/non-war. Markets might plummet the next day or surge the day after. One week, US equities outperform the rest of the world; the next week, the pattern reverses.

Later, I discuss lessons from history regarding geopolitics, but the message is clear: overall, most geopolitical events do not cause long-term changes. Even UK equities finished WW2 higher than they started, despite a global war!

However, there’s a caveat: sometimes wars lead to profound structural shifts. For example, the Yom Kippur war in the early 1970s triggered a significant inflationary surge. War was a catalyst but also sped up existing trends. My main belief is that whatever unfolds with the Iran crisis will accelerate an existing structural change, heightening fears that government debt will overwhelm debt markets and fuel inflation. This brings me to my first topic: gold and silver.

It’s now obvious to all except cave dwellers that investors got too excited and too narrative-driven about gold and especially silver. That bubble was always going to burst, and ironically, the price of gold is likely to fall further until the war ends.

But I stick with the long-term view that as the consequences of the war on government spending become ever more obvious, the worries about the lack of fiscal rectitude, i.e., fiscal debasement, will rekindle the gold narrative. I stick with a medium-term target of $ 6,000 per ounce by the end of the year.

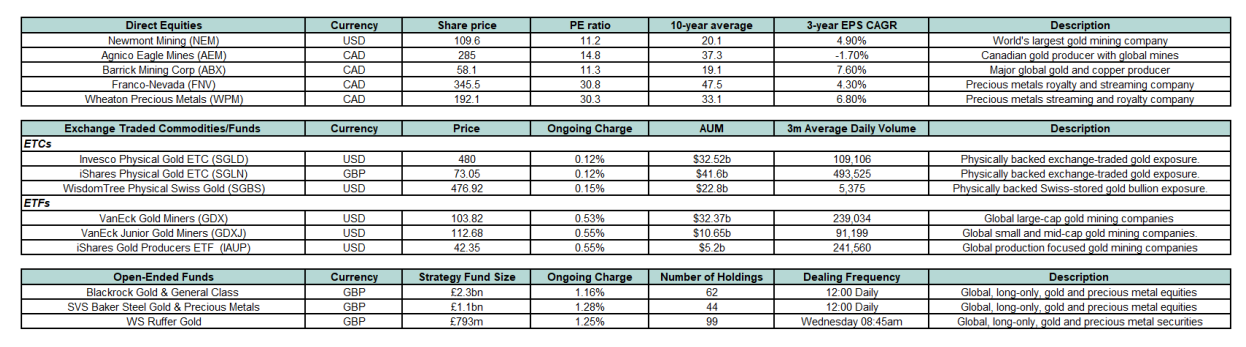

In particular, I would note that the odds of Trump and the Republicans losing both the House and the Senate are growing, prompting a government logjam and a massive showdown between the left and the right in the US. That will benefit gold prices. The table below from broker Killik and Co usefully spins through the various main market ways of building exposure to gold.

The damage so far in the world of investment trusts

Sticking with the theme of volatile markets and how to navigate them, I thought I might share the following table from Sharescope with readers. It looks at returns for the one month following the Iran escapade for a range of investment trusts, both successful ones and utter dogs.

I’ve colour-coded returns from March 2nd through March 30th, price returns only. I have also excluded some slightly smaller, slightly exceptional funds where the driver of returns has been somewhat eccentric or where liquidity is next to non-existent.

In the champs corner (in blue), I have highlighted a few funds in bold that I think are worth commenting on. There are funds like BioPharma Credit that have an exclusive focus on income. There’s also a handful of renewable funds, such as Greencoat UK Wind and Bluefield Solar, that have risen in value, though only after a torrid few months. I rate Greencoat UK Wind and BioPharma highly. And last but not least, there’s Majedie Investments, an interesting multi-asset fund that I think warrants further investigation for defensive investors seeking a commitment to absolute returns. It’s doing very well compared to its peers such as Ruffer Investment Company and BH Macro.

The Importance of income and dividends

My next suggestion is that in an increasingly volatile world, with inflation above the near-term trend and stock markets wobbling, dividends, their growth over time, and your subsequent reinvestment of those dividend cheques might make a huge difference. I think there is a sporting chance – just a chance, not a certainty – that equity income strategies will do well over the next decade. They won’t keep up with the next wave of AI and automation enthusiasm, but they’ll provide solid returns.

In this scenario, I’d expect dividend-oriented investment trusts to perform fairly well and offer some solace to anxious investors. Right on cue, the Association of Investment Companies (AIC) has just published its updated list of 20 dividend heroes. These investment trusts have consistently increased their annual dividends for at least 20 consecutive years. Half of the 20 dividend heroes have increased their dividends for 50 or more consecutive years. Topping the list with 59 years of dividend rises are City of London Investment Trust, Bankers Investment Trust and Alliance Witan, closely followed by Caledonia Investments with 58 years.

Source: theaic.co.uk / Morningstar. Data at 12/03/26. * Dividend rise announced on 16/3/2026

The next generation of dividend heroes

The next generation of dividend heroes are investment trusts that have increased their dividends for at least ten years, but less than 20.

Source: theaic.co.uk / Morningstar. Companies with the same number of years of consecutive dividend increases are ordered by the date the final dividend was declared. Data as at 18th March 2026

Asian Defence ETF

“The most compelling APAC investment cases aren’t driven by budget headlines; they’re driven by companies quietly building the industrial capacity to supply both their own region and Europe. The common thread is a deliberate move away from dependency on a single ally. When you look at APAC, you’re not reading a defence story. You’re reading a geopolitical realignment playing out in order books.”

Fredrik Ljungdahl, Analyst at Finserve

The quote above from an analyst at Europe’s biggest actively managed defence fund, Finserve, is, I think, very insightful. European investors have already worked out that European defence spending is set to increase radically, but they’ve yet to wake up to another story: the military boost in APAC/East Asia. The drivers are obvious: the rise of China and, to a lesser degree, India; geopolitical competition; and the huge increase in defence exports from South Korea and Japan (imminently). To address this theme, UK ETF issuer HANetf last year launched an ETF that specifically targets this space: the Future of Defence Indo-Pac ex-China UCITS ETF, which provides targeted exposure to Indo-Pacific defence companies ex-China.

My own view is that Asia will likely be the primary military arena over the next few decades, a possibly unsavoury prospect. Russia, though a real and deadly threat, is still a second-rate nuisance and agitator with a fundamentally weak military that should, over time, find itself outclassed by a resurgent Europe – assuming we spend the right of money on equipment and equally importantly, people.

China, by contrast, is a whole different beast, determined to reassert its traditional continental hegemony and, frankly, to push around other states in its region. Japan, by contrast, is a sleeping (military) giant whose interests rarely align with China. And we haven’t even started to think about how the India/China dynamic plays out. All the major states in APAC are spending substantially more money on defence, and I see no sign of that changing any time soon, not least while President Xi is still in power.

One other core dynamic: many Asian countries, like South Korea, are also building up formidable defence export bases, built on their pre-existing industrial strength. In this regard, it’s not impossible to view South Korea and Japan as the shipbuilding outposts of the USA (and Europe). The challenge, though, is investing in this broad spectrum of businesses: the key players are largely inaccessible to UK investors, which is where HANetf’s new ETF comes in.

Key features:

· USD

· AuM $20m

· TER 59 Bps

· Ticker QUAD

· Performance YTD to end Jan + 24%

Country weightings : South Korea 43.30%, India 28.49%, Japan 11.58%

Top Five holdings in APAC ETF

Cordiant Keeps Delivering — and a Big Move Is Coming

Digital infrastructure investment company CORD has posted a solid quarterly trading update, with portfolio revenue climbing 8.9% year-on-year on a like-for-like, constant-currency basis to £263m for the nine months to 31 December 2025. EBITDA rose 7.1% over the same period to £125m – it’s the kind of steady, unglamorous progress long-term infrastructure investors tend to love.

The more exciting near-term catalyst is the Prague Gateway data centre development. Growth capex hit £39m in the last twelve months, up from £29m in FY2025, with a chunk of that going into Prague Gateway groundworks and expanded data centre capacity. The development is currently carried at nil in the NAV, which implies shareholders are getting it for free, at least for now. Management has commissioned an independent valuation for inclusion in the March 2026 NAV, which analysts reckon could add a few pence per share. Whether that uplift is at the higher or lower end depends on factors such as whether an anchor tenant signs up before the valuation date and how far along contractor commitments are. The fact that management felt confident enough to commission the valuation at all is itself something of a signal. Meanwhile, the Czech Republic’s asset disposal programme is expected to generate at least CZK 340m (around £12.3m) this financial year, with more to follow in FY2027, providing a useful source of internal funding for reinvestment without tapping the market.

Perhaps the biggest headline, though, is CORD’s intention to migrate its ordinary shares from the London Stock Exchange’s Specialist Fund Segment to the Main Market. The company believes this will raise its profile, improve liquidity, and open the door to retail investors and, potentially, FTSE 250 inclusion, which becomes realistic around an £800m market cap. Analysts at Panmure Liberum have welcomed the move, noting that it should help narrow the discount at which the shares trade relative to peers such as 3IN and PINT.

On valuation, CORD still looks undemanding, trading at under 11x EV/EBITDA on a fair value basis. Its tower portfolio alone, typically valued at 15–20x in M&A transactions, represents meaningful embedded which the current share price simply doesn’t reflect. With a buy rating and a 120p target price from Panmure Liberum, and an illustrative net IRR of around 14%, the bull case here is fairly straightforward. I regard this fund as a core holding of mine.

A reminder from history

Every year, three academics – Elroy Dimson, Paul Marsh, and Mike Staunton – publish what has become the definitive long-run study of global financial markets. The 2026 edition of the UBS Global Investment Returns Yearbook draws on data stretching back to 1900, covering 35 countries and virtually every major asset class, and distils ten of the most important lessons from that 126-year history, from AI mania to gold surging to geopolitical tensions running hot.

The US vs the Rest of the World

From a relatively evenly distributed global equity market in 1900, the US now dominates, accounting for around 62% of total world equity market value – even though its relative GDP share has actually declined since a peak in the late 1940s. That gap between economic weight and market weight is striking. The US got to where it is through strong stock returns and a relentless pipeline of IPOs and share issuances, not simply because its economy grew the fastest. Meanwhile, China, which began the 20th century as a significant economic force, has clawed back its GDP share in recent decades but remains far less dominant in equity markets relative to its economic size.

Industries have been turned upside down

Of the US firms listed in 1900, some 80% of their value was in industries that are small or extinct today, including railroads, textiles, iron, coal and steel. Flip that around, and 70% of today’s companies in the US come from industries that were small or non-existent in 1900 -technology and healthcare were almost totally absent from stock markets back then. Investors tend to assume new technology sectors will bubble up and then crash, but the old declining industries have actually held their own rather well. Railroads, despite falling from 63% of the US market to less than 1% today, actually outperformed both the US stock market and their newer technology competitors since 1900.

Stocks win. By a lot.

This one is probably the most consistently useful finding across every edition of the Yearbook. Equities have outperformed bonds, bills and inflation since 1900 -an initial investment of USD 1 grew to USD 124,854 in nominal terms by end-2025. Bonds and bills still beat inflation over the same period, but the gap is enormous. In real terms, equities compounded at 6.6% per year versus just 1.6% for bonds and 0.5% for bills. And crucially, this outperformance isn’t just a US phenomenon – equities were the best-performing asset class in all 21 Yearbook countries with continuous investment histories, and bonds beat bills in every country except Portugal.

Developed vs. emerging markets -it’s complicated

The annualised return from investing in emerging markets since 1900 has been 6.9%, compared with 8.5% for developed markets. Therefore, over the very long term, developed markets outperform. However, the more recent data reverses this trend: from 1960 to 2025, emerging markets achieved an annualised return of 10.9%, while developed markets returned 9.6%.

Inflation matters more than people think

Although the US had the third-lowest rate of inflation in the DMS 35 markets, averaging 2.9% per year since 1900, that still means $1 in 1900 had the same purchasing power as $38 today. The compounding effect of even modest inflation over a century is severe. More importantly, the report challenges a widely held belief: although it is often claimed that equities are a hedge against inflation, the data show that for both equities and bonds, real returns tend to be higher when economic growth is stronger and inflation is lower. In other words, equities don’t necessarily protect you in a high-inflation environment—they simply tend to perform better when the macroeconomic backdrop is benign.

Gold – not quite the inflation hedge you think

Gold should be seen more as a long-term store of value rather than a short-term hedge against inflation. Since 1900, the real USD gold price has increased by 5.2 times, yielding an annualised return of 1.3% — positive, but not remarkable. Its performance after Bretton Woods has been more robust, but its short-term correlation with inflation remains unpredictable.

Geopolitics vs. economics -economics usually wins

Using a simple regression of future world equity returns against a geopolitical threat index, the authors found no relationship, whether they looked a month or a year ahead. Most of the time, geopolitical noise is just that—noise. World War I, World War II, and the 1973-74 Oil Shock were geopolitical events that led to three of the six worst episodes for large global equity markets since 1900— but extreme events like those are rare. Of the four largest peacetime bear markets, three were triggered by economic factors.

Diversification still works, just less easily

By the end of 2025, the US equity market concentration was at its highest level in at least 100 years, while correlations between developed and emerging markets, and between equities and bonds, have also risen. But the case for diversification hasn’t collapsed. When currency risk was hedged, investors in the vast majority of markets were better off investing globally rather than domestically. And the equity-bond blend still offers meaningful downside protection: since 1900, equities and bonds have, on several occasions, lost more than 70% in real terms, yet a 60/40 equity-bond blend has never declined by more than 50%.

Momentum is the factor king

On factor investing, the momentum factor has offered the strongest and most persistent factor performance over the long term, delivering a premium of 7.7% per year in the US and ranking top in 13 of the 24 country-decades studied. That said, 22% of country-decades saw negative factor premiums, even over entire decades – a useful reminder that factor investing requires patience and conviction, and that no strategy works all the time.

David Stevenson

Twitter: @advinvestor

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

Gold. Your thoughts about holding gold and your excellent table of ways of holding gold were most helpful.

I noted that you did not include thepuregoldcompany.co.uk. Could you explain why please?

Hi Roy

If I’m honest, I’ve never heard of them. I have heard of BullionVault – I tend to focus on on-exchange funds or products, which BullionVault isn’t. Also, I am a big fan of physical gold via coins (for which you pay a premium), but again, these aren’t on the exchange.

Thanks

DSavid