Higher energy bills are supporting significant dividend advances at Telecom Plus. Maynard Paton weighs up the group’s illustrious growth and ambitious targets against a leadership change and unusual marketing.

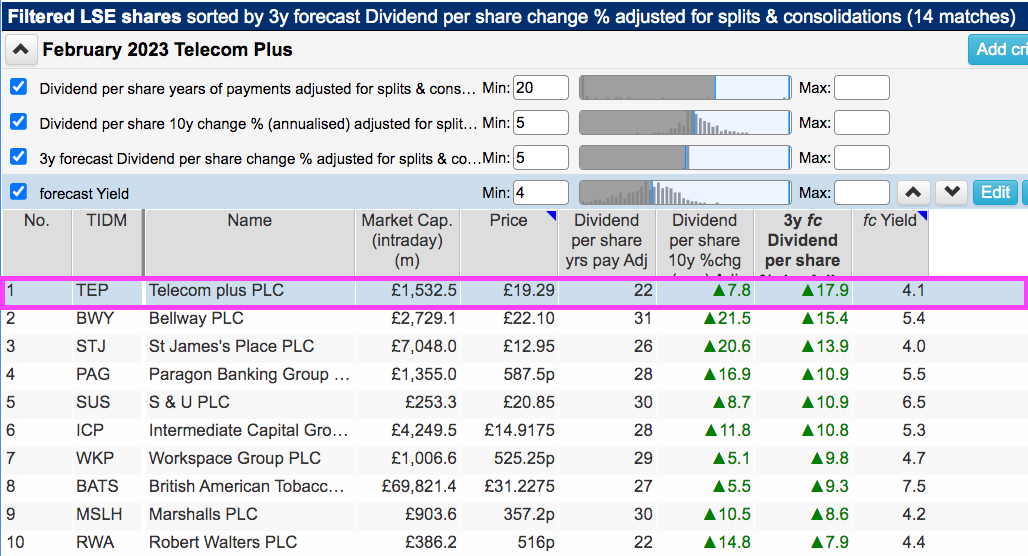

Difficult market conditions have prompted many investors to find safety through attractive dividend shares.

Hence a new screen to pinpoint companies that boast a dependable payout, a meaningful yield and respectable prospects.

The exact criteria I employed for this search were:

- A record of dividend payments spanning at least 20 years;

- A 10-year dividend growth record of 5% or more;

- A minimum forecast three-year dividend growth rate of 5%, and;

- A forecast dividend yield of at least 4%.

I applied the screen the other day and SharePad returned 14 matches:

(You can run this screen for yourself by selecting the “Maynard Paton 10/02/23: Telecom Plus” filter within SharePad’s terrific Filter Library. My instructions show you how.)

I selected Telecom Plus from the shortlist as the company offered the highest forecast dividend growth for the next three years:

Let’s take a closer look.

The history of Telecom Plus

A £1 million rights issue funded by Charles Wigoder during 1998 was the beginning of a superb investment that presently boasts a £100 million market value.

Mr Wigoder’s involvement with Telecom Plus followed his exit from People’s Phone, a mobile-phone retailer he launched during the late 1980s that established the world’s first virtual mobile network. Mr Wigoder earned more than £6m from the chain’s sale to Vodafone.

Telecom Plus took the reseller route pioneered by People’s Phone and resold landline connections to consumers via ‘word of mouth’ network marketing. Reselling mobile services, broadband connections and gas and electricity supplies soon followed.

“The market was dominated by British Telecom and British Gas and there was a real opportunity to take on these monopoly suppliers and start delivering something they really weren’t — better value, better service and real savings to large numbers of people who were getting a lousy deal.“

Today Telecom Plus serves more than 800,000 customers reselling energy and telecom services through its Utility Warehouse (UW) brand. The group’s gas and electricity is bought wholesale from EON while telecom services are acquired wholesale from TalkTalk and EE.

Customers are attracted to consistent lower ‘bundle’ pricing charged through a simple monthly bill. Marketing continues to be undertaken by a network of independent ‘partners’, who recommend friends and family switch to UW in return for commission.

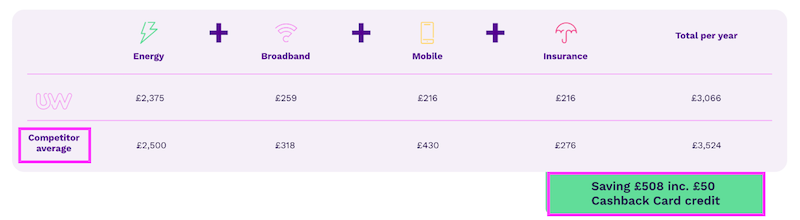

Telecom Plus claims to be the UK’s “only genuine multi-service provider“, with tariffs kept low due to “spreading a single set of overheads across multiple… revenue streams”. The UW website states new customers can “save up to £508 when bundling energy, broadband, mobile and insurance into one great value monthly bill“.

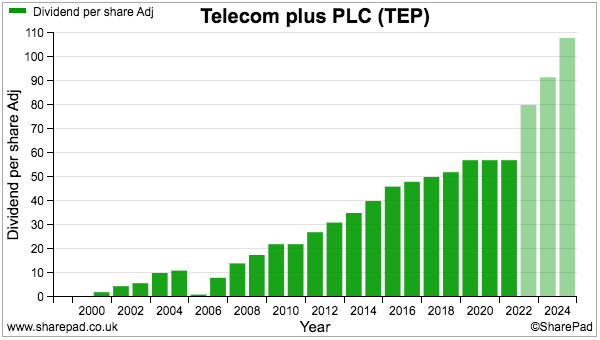

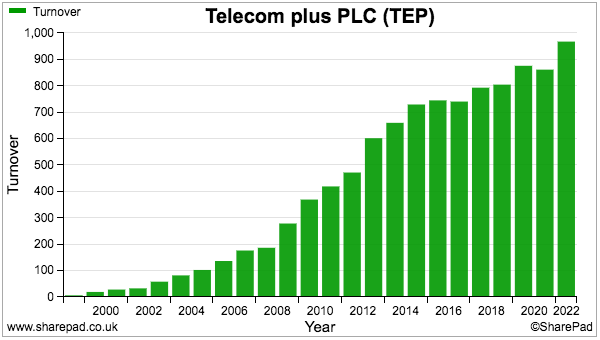

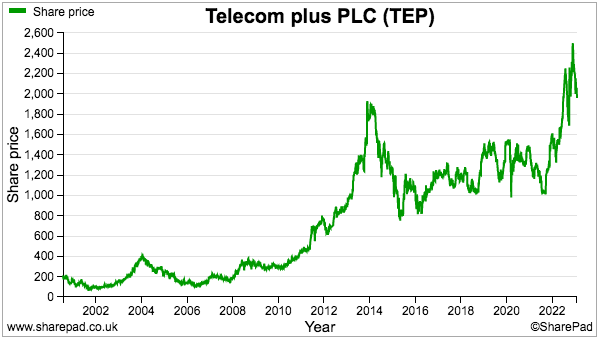

Telecom Plus joined the main market during 2000 at 200p a share and progress thereafter has been mostly positive:

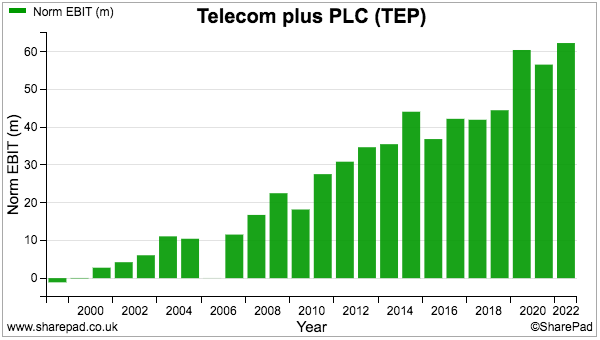

Revenue has surged from £20 million at the time of flotation to close to £1 billion, while a small loss has transformed into an underlying profit beyond £60 million.

The profit setback during 2006 was caused by “increasingly volatile” wholesale gas prices that at the time had reached “unprecedented highs“.

Telecom Plus had originally took on the hedging risk with energy prices, but was caught out by sudden movements that thumped margins. A new supply deal from 2006 passed on the hedging risk to what is now EON.

The share price hit £24 last year and the recent £19 supports a £1.5 billion market cap:

Customers and services

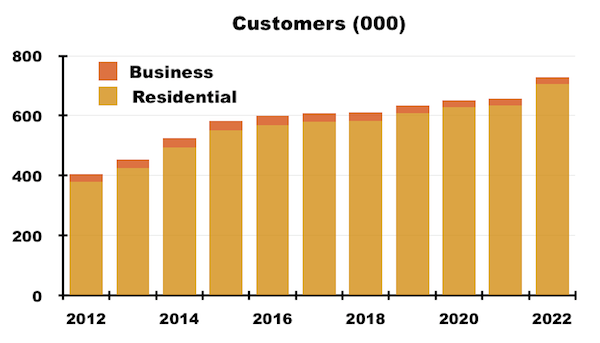

Telecom Plus provides numerous statistics to help assess the group’s progress. Customer numbers for instance have grown consistently over time:

But competitive pricing from alternative suppliers has caused annual revenue per customer to bob around the £1,200-£1,300 level for the last ten years:

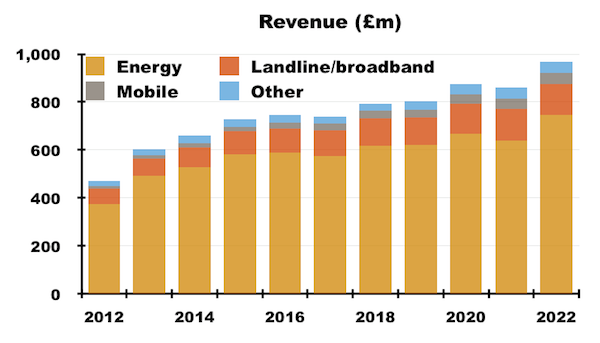

Telecom Plus’s revenue sources have been remarkably consistent, with energy representing 75%-80% of total sales and landline/broadband at approximately 14%:

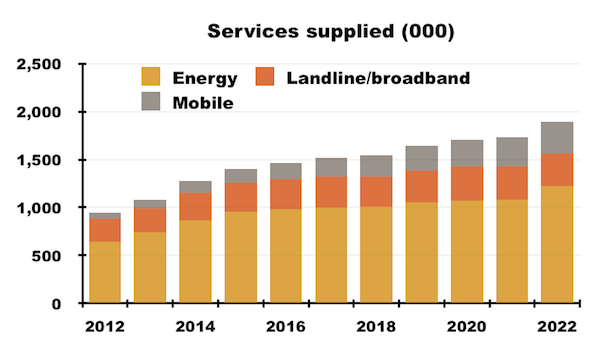

The total number of services supplied to all customers has regularly advanced:

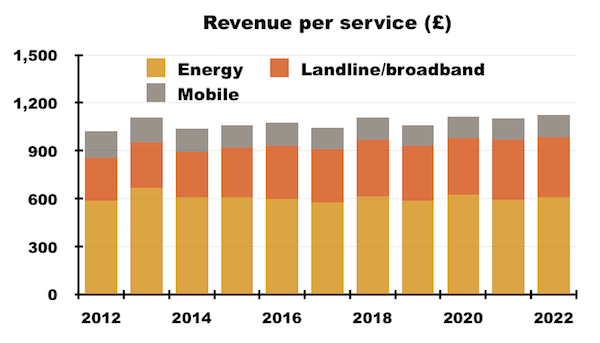

But similar to revenue per customer, revenue per service supplied has remained rather constant:

Customers have typically paid around £600 a year for gas or electricity, with almost £140 a year paid for mobile connections. Only landline/broadband services have seen higher bills, with the average payment rising £100 to £373 a year since 2012.

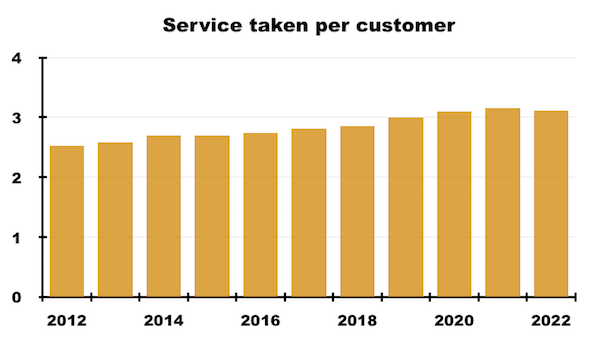

The chart below perhaps validates the growing popularity of Telecom Plus’s multi-utility offering. The number of services taken by customers has increased from 2.5 to 3.1 during the last ten years:

Partners and multi-level marketing

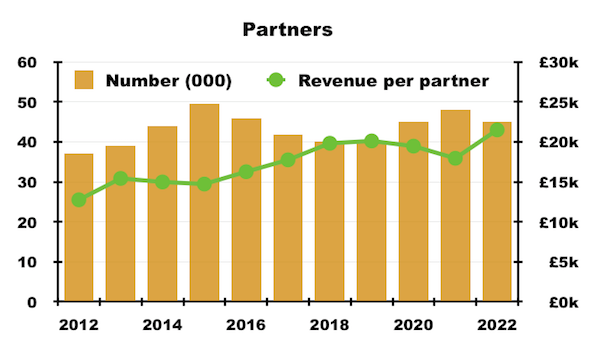

Some intriguing ratios are derived from Telecom Plus’s 50,000 or so network-marketing partners.

The quality of partners appears to have improved. Revenue per partner has advanced from £13k to £21k since 2012:

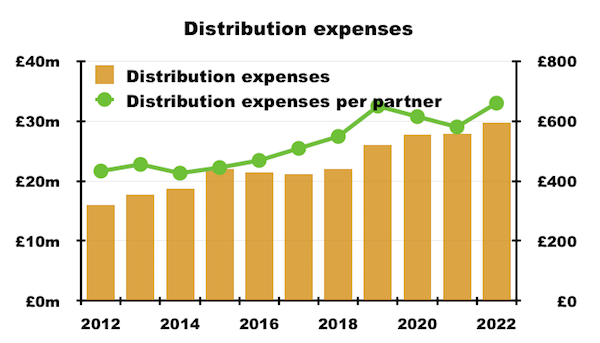

Distribution expenses — essentially payments to partners and other customer acquisition costs — have meanwhile risen to almost £30 million a year or £660 per partner:

I must admit, I had thought the average partner would be earning much more than £660 a year — especially as the UW website claims they can earn up to £250 for each new customer.

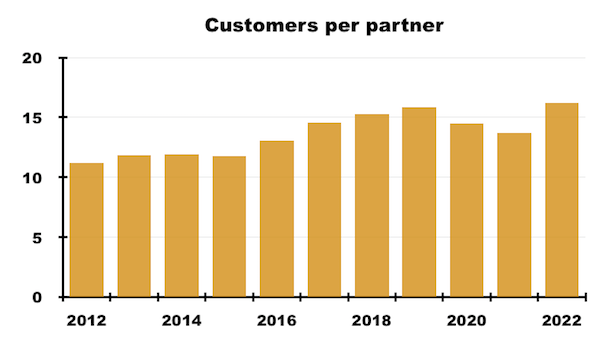

I assume finding customers beyond friends and family is hard going. The average number of customers per partner is only 16:

The stats may be skewed because successful partners recruit ‘sub partners’ and take a share of their income.

During this Sack, The Boss video, UW’s “No1 earner” Steve Critchley reveals he has just 18 personal customers…

…but also 390,000 “group” customers that allow him to get paid for 1.25 million services (representing a staggering 48% of Telecom Plus’s entire business!).

Mr Critchley got started with Telecom Plus at its inception, and his 25 years with the business has told him “the real juice is building a team” and “it is easier to get a partner than a customer“.

Telecom Plus’s growth may well boil down to ‘multi-level marketing‘ (MLM), whereby partners must recruit other partners in order to expand their income to a significant level.

The sales approach has attracted adverse attention, with Rupert Jones at the Guardian for example providing coverage since at least 2009 (Get rich quick? Not with Utility Warehouse, Utility Warehouse: is its ‘life-changing’ scheme really ab fab? and Utility Warehouse under the spotlight).

This sceptical blogger meanwhile received a meeting invitation from Mr Wigoder to explain the MLM strategy.

Margins and cash flow

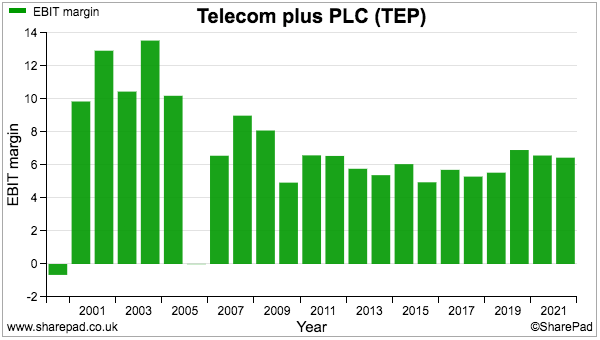

The refreshed energy-supply deal from 2006 looks to have caused Telecom Plus’s margin to fall from 10%-plus to somewhere around 5%-6%:

Reselling energy and telecom services will never be a high-margin activity, but the group boasts “considerable visibility” from its wholesale energy purchasing:

“The group’s wholesale [energy] costs are calculated by reference to a discount to the prevailing standard variable retail tariffs offered by the ‘Big 6’ to their domestic customers, which gives the Group considerable visibility over profit margins”.

This particular wholesale arrangement has become very favourable of late after standard variable tariffs became the default for consumers due to rising energy prices reaching the government’s price cap.

Telecom Plus now claims customers can save up to £125 a year on energy bills using UW — although such savings do require taking on additional non-energy services.

The 2006 supply agreement was extended during 2013, when Telecom Plus paid £222 million to EON for a further 20-year arrangement that would “substantially increase the energy margins available“.

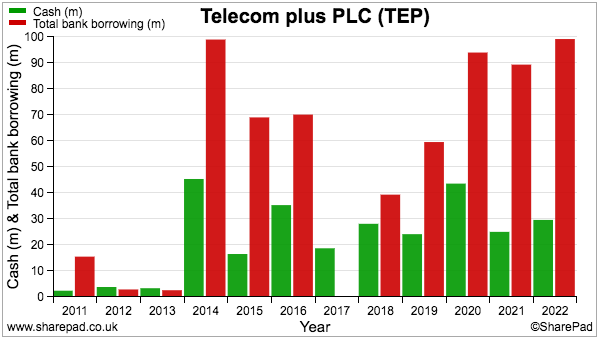

I do not know whether Telecom Plus will have to stump up another £222 million to renew the agreement in 2033. But funding the agreement did mean Telecom Plus was left with net debt during 2014:

After the disposal of an investment cleared all the borrowings during 2017, debt has since reappeared and presently stands at £100 million.

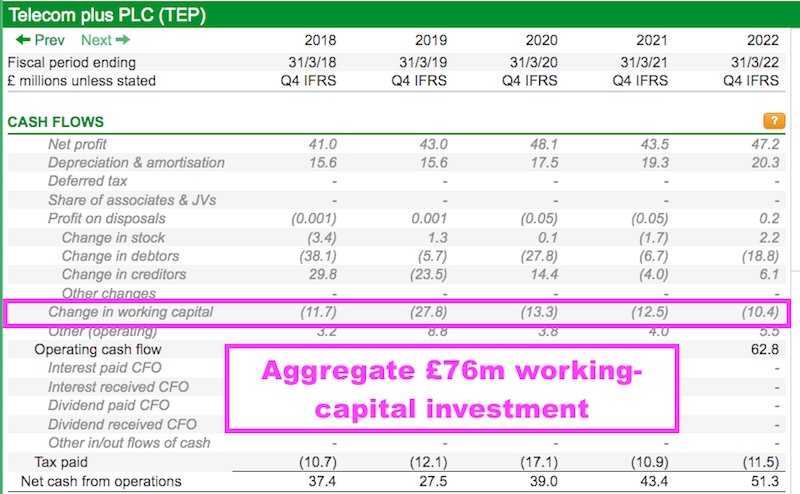

Cash working-capital movements have absorbed a hefty £76 million during the last five years and appear partly responsible for the greater borrowings:

Cash flow does not seem Telecom Plus’s strong point, with customers billed monthly in arrears and bad debts of £12 million being incurred last year. The balance sheet meanwhile carries capitalised partner commissions of £15 million and capitalised IT costs of £21 million, which represent past cash expenses that have yet to trouble the income statement.

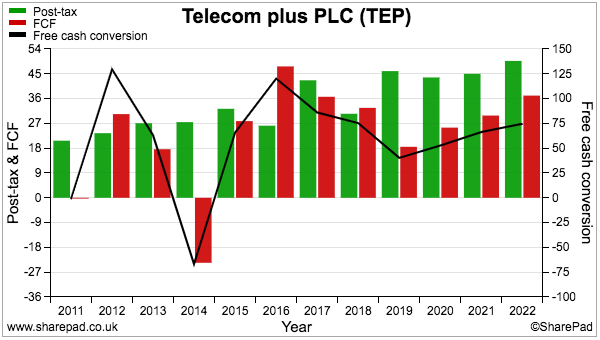

The conversion of reported profit to free cash flow is therefore not spectacular at less than 75% during recent years:

Management and employees

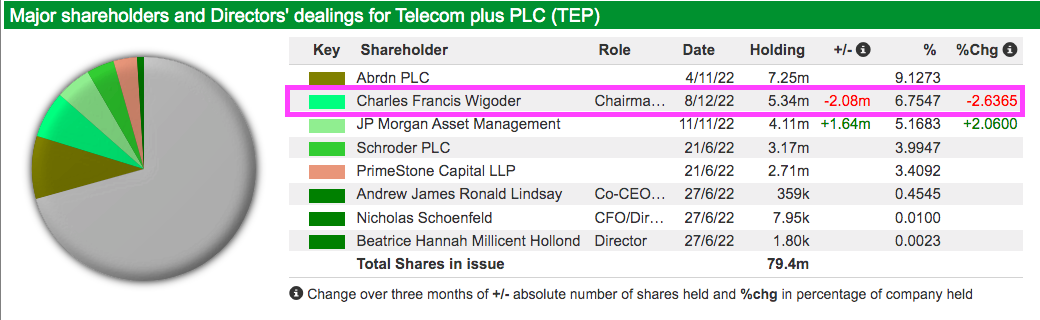

Mr Wigoder sadly appears to be making his exit from Telecom Plus. He gave up his executive duties to become non-exec chairman last year and has reduced his shareholding by more than half through placings (selling at £13.50 during 2020, £14.50 during 2021 and £24 during 2022).

At least Mr Wigoder retains a near-7% stake that is worth approximately £100 million, which should keep him active at board meetings:

Executive duties now rest upon a peculiar dual chief-exec set-up, with Andrew Lindsay (appointed 2010) focusing on partners and growth strategies and Stuart Burnett (appointed 2021) overseeing day-to-day matters.

Executive wages are a healthy £500k-plus, with Mr Lindsay owning shares worth almost £7 million and Mr Burnett owning none. I note nobody on the board brings hands-on experience from the important energy sector.

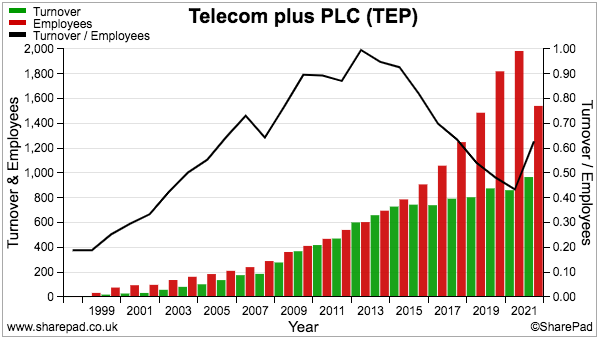

Maintaining tip-top customer service has prompted a significant increase to the workforce since 2013 and caused revenue per employee to decline considerably:

Total staff wages have advanced from 3% to almost 8% of revenue during the last ten years, which has negated any (theoretical) economies of scale from serving more customers and in turn kept the group’s overall margin around that 5%-6% level.

Distribution expenses (including those payments to partners) have remained steady at 3% of revenue.

Recent trading and guidance

November’s first-half figures were very upbeat. The group reported customer numbers up 23% which pushed revenue 52% higher, adjusted profit 23% higher and the dividend 26% higher.

Independent energy suppliers going bust and the favourable EON agreement has apparently left UW as “the only meaningful energy switching option in the UK”. Another positive was the partner count growing 18% as more consumers look to earn additional money in a shaky economy.

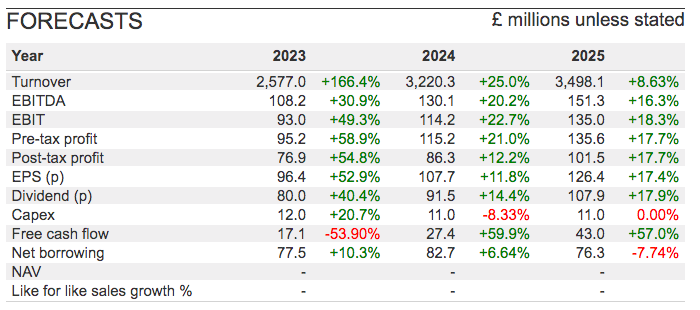

The icing on the cake was the uplifted guidance; current-year profit ought to be at least £95m (previously c£75m) and the dividend ought to be at least 80p per share (previously at least 65p per share):

The projections for 2025 place the £19 shares on P/E of 15 and yield of 5.7%. Note the dividend forecasts reflect the group’s “medium-term intention” to return to a very generous 85% payout ratio.

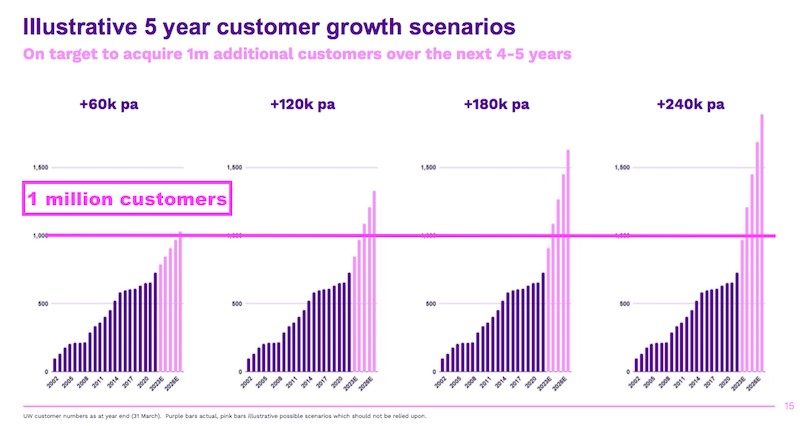

The interim statement reiterated the group’s target of acquiring an additional million customers during the next four or five years, which the presentation slides implied may be a low-ball estimate:

An extra million customers would more than double the present customer base and presumably more than double the present earnings and the dividend.

But do bear in mind Telecom Plus has offered ambitious targets before. For example, the group said during 2013 it had a “goal of supplying our unique, multi-utility proposition to more than one million customers over the medium term“…

…and ten years later, the customer count has yet to surpass one million.

Summary

Telecom Plus’s dividends seem relatively secure for anybody who believes elevated energy prices will not subside anytime soon.

Higher bills should of course translate into higher earnings, and very few quoted companies are bold enough to say their customer base could more than double within five years!

But drawbacks exist, not least the share sales and executive withdrawal by Mr Wigoder. The group’s driving force turns 63 next month, so prospective investors will have to balance legitimate retirement planning against selling out while the going is exceptionally good.

The accounts are acceptable but not spectacular, with the large working-capital requirements not ideal and leading to greater borrowings that have arguably underpinned the dividend. But the debt does look quite manageable and will become even more manageable if the uplifted guidance proves accurate.

Do bear in mind UW’s energy savings only really emerge when customers add on a telecoms service, and the group’s headline pricing claims are made versus competitor averages — not against the best-value product in each category.

Probably the most worrying aspect is the group’s sales approach that looks ominously based on MLM tactics. I am somewhat uneasy at the advice dispensed by UW’s “No1 earner“, while the earnings reality for most partners may not be typical of these UW stories. I would happily venture Telecom Plus’s dividends would be a better source of secondary income.

Until next time, I wish you safe and healthy investing with SharePad.

Maynard Paton

Maynard writes about his portfolio at maynardpaton.com and co-hosts the Private Investor’s Podcast with Roland Head. He does not own shares in Telecom Plus.

Got some thoughts on this week’s article from Maynard? Share these in the SharePad chat. Login to SharePad – click on the chat icon in the top right – select or search for a specific share.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.