Strix is the world’s leading developer of kettle safety controls, but a recent profit warning has sent the shares tumbling. Maynard Paton wonders whether the group’s competitive advantage can support an eventual recovery.

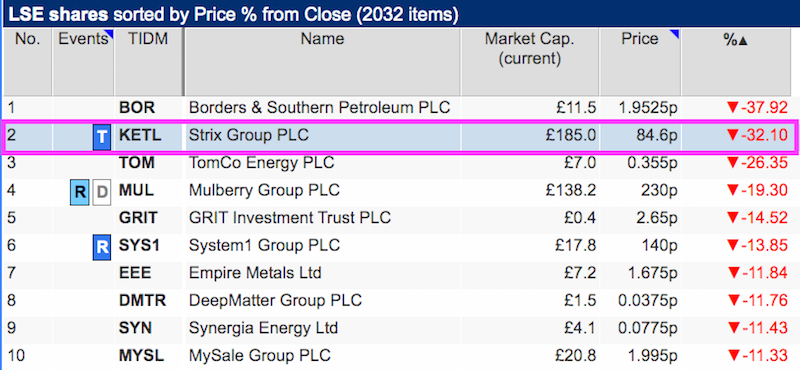

A profit warning and 32% share-price crash brought Strix to my attention the other week:

This small-cap dominates the market for kettle controls, and I wondered whether that strong competitive position could support an eventual recovery.

Let’s take a closer look.

Bi-metal blades and electric kettles

“I can go to any high street in the Western world, look in the window of any shop selling kettles, and say “I designed that one, designed that one, designed the controls on that one”, and it’s a very satisfying feeling to be able to say that.”

So recalls John Taylor on his website after he developed a bi-metal blade during the 1960s that could be used in thermostats.

Dr Taylor demonstrates how the blades react to different temperatures within this informative two-minute video. He also explains the technical history of the blades during this great 55-minute talk:

Jaguar was an early customer when the car manufacturer included the blades within its cooling fans.

But the growing popularity of electric kettles during the 1970s — which prompted Dr Taylor to devise blades that could switch off kettles when the water had boiled — was where the real money would be made.

By 1982 Dr Taylor had separated his business ventures and changed the name of his kettle-control operation from Castletown Thermostats to Strix.

Today Strix is the world leading supplier of kettle controls, with the group claiming a 56% global market share by value. The company’s proportion within regions that enforce higher kettle safety standards — such as the UK, the EU and the USA — is apparently 75%.

A clutch of patents alongside high-quality manufacturing and ongoing product innovation have helped Strix sell more than two billion kettle controls since its formation.

Dr Taylor’s bi-metal blades have been so successful, they feature on stamps issued by the Isle of Man, where Dr Taylor resides and where Strix is located:

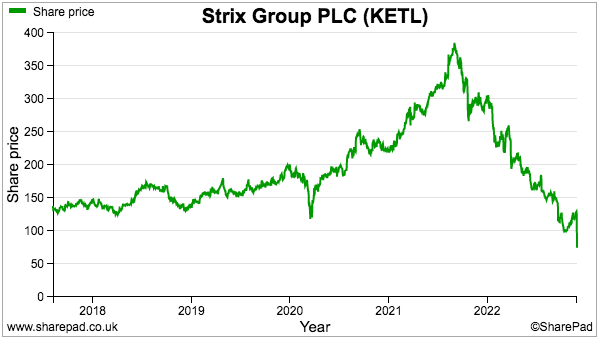

Dr Taylor retired during 1999 and had sold Strix to private equity by 2005. The company joined AIM during 2017 at 100p and the shares peaked at 387p last year:

Rough market conditions, subdued results and the aforementioned profit warning have since reduced the shares to 85p to support a market cap of £185 million.

Revenue, profit and margin

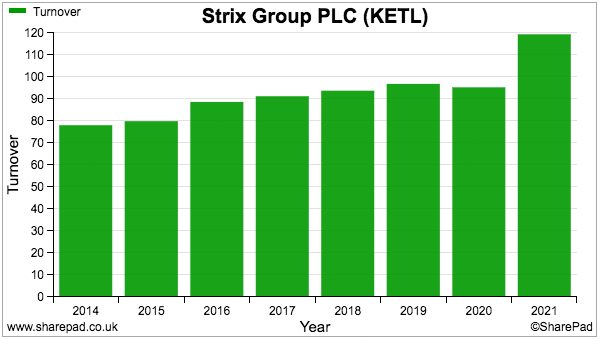

Strix has not made incredible financial headway following the flotation.

Revenue had been inching beyond £90 million until the purchase of Italian firm LAICA bolstered the top line for 2021:

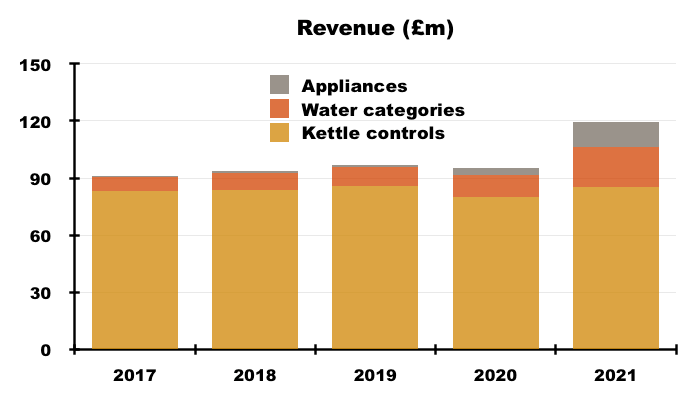

The LAICA acquisition cost £24 million and brought with it sales of £22 million through the manufacture of water and coffee filters. The acquisition helped Strix diversify from the slower-growing kettle-controls division:

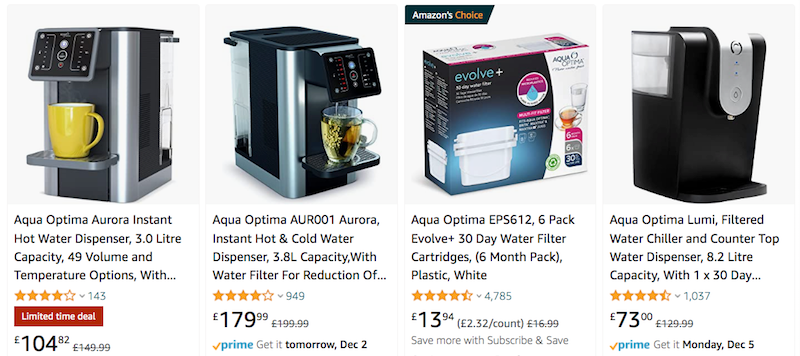

The LAICA purchase has since allowed Strix to combine “classic Italian design” with its own technology to manufacture an in-house range of sophisticated kettles. The Appliances division also includes the Aqua Optima range of water dispensers that Strix says sells well on Amazon:

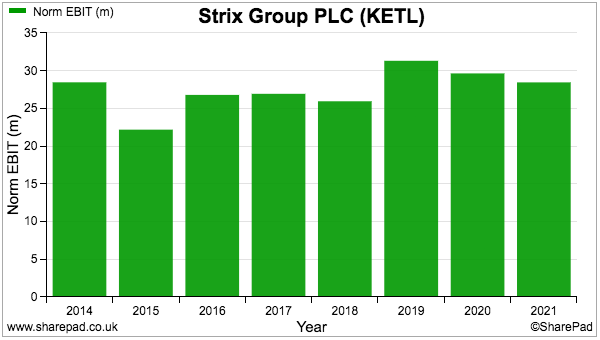

Operating profit has unfortunately not followed revenue higher and has instead bobbed between £25 million and £30 million:

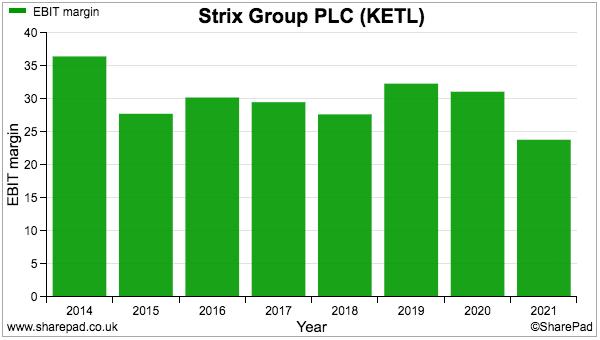

Perhaps the most impressive SharePad chart is operating margin:

Strix has consistently managed to convert at least 20% of revenue into profit, which suggests the aforementioned patents and innovations are indeed the foundation of a notable competitive ‘moat’.

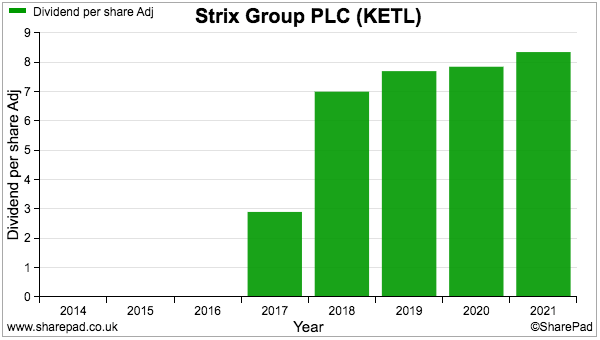

The dividend has improved modestly over time:

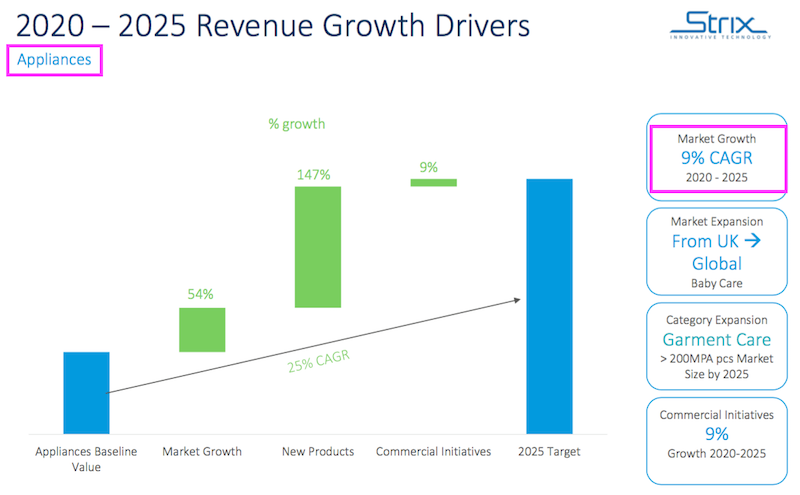

Beyond kettles via a five-year growth plan

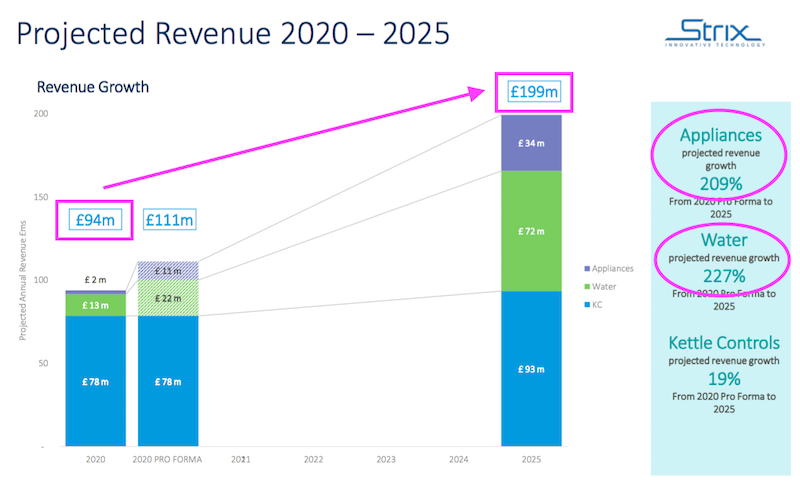

Strix revealed its five-year ambitions during a November 2020 presentation. The headline target was to double revenue to £199 million by 2025:

Note that growth will be derived from the Water and Appliances divisions rather than through kettle controls.

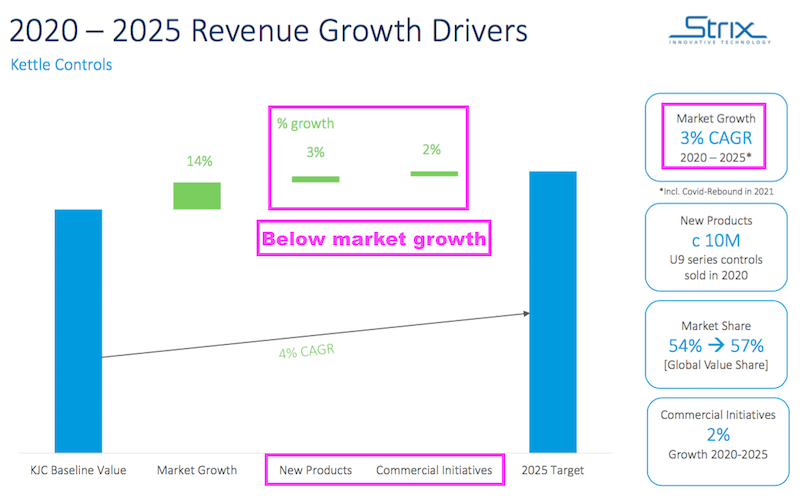

The slide below refers to kettle-control market growth of 3% a year, and implies minimal contributions from new products and “commercial initiatives“:

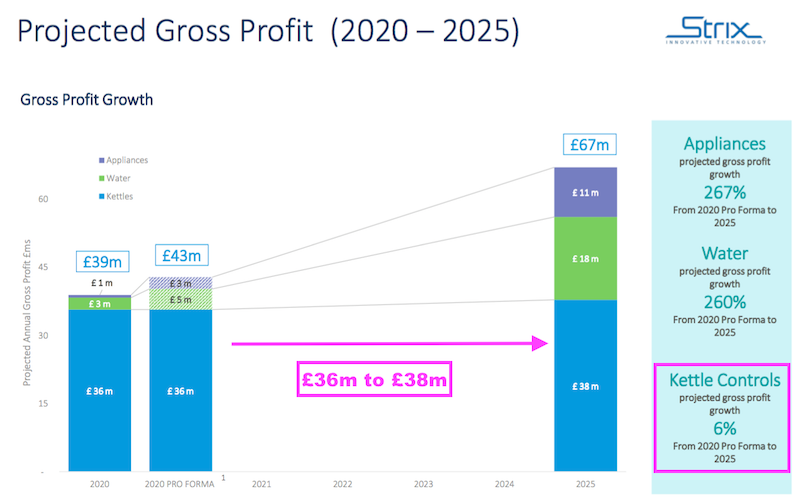

Kettle margins may be facing extra pressure. The slide below shows gross profit for the division advancing by just 6% during the five years:

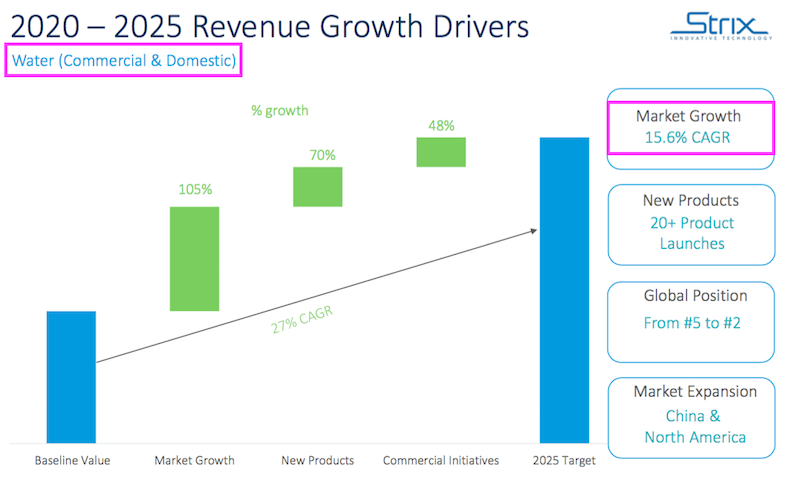

The Water and Appliances divisions could in contrast enjoy market growth CAGRs of 15.6%…

…and 9% respectively:

Despite the appealing projected CAGRs, the Water and Appliances divisions are not expected to be as profitable as kettle controls. For 2025, Strix expects Kettles to enjoy a 41% gross margin versus 25% for Water and 32% for Appliances.

Assisting the five-year revenue target is last month’s £38 million purchase of Billi.

Billi manufactures systems that provide instant hot, chilled and sparkling tap water. According to Strix, Billi delivered a double-digit revenue CAGR during the five years prior to purchase. Anticipated sales for 2022 are £44 million.

Strix also noted the Billi deal “materially accelerates the trajectory of and is accretive to Strix’s medium term targets with these targets now expected to be reached ahead of the initial 2025 timeframe“.

The downside to the purchase is additional debt. Strix raised £10 million by issuing new shares to help fund the Billi deal, but net borrowings are now nearly three times the size of forecast 2022 earnings.

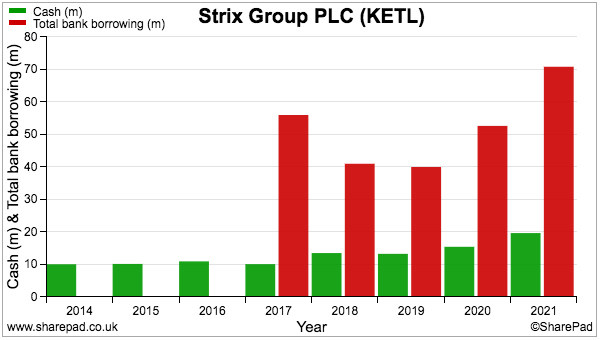

Borrowings, cash conversion and ‘leverage ratio’

Strix’s former owners saddled the company with debt at the flotation, with net borrowings at the end of 2021 (and before the Billi transaction) standing at £51 million:

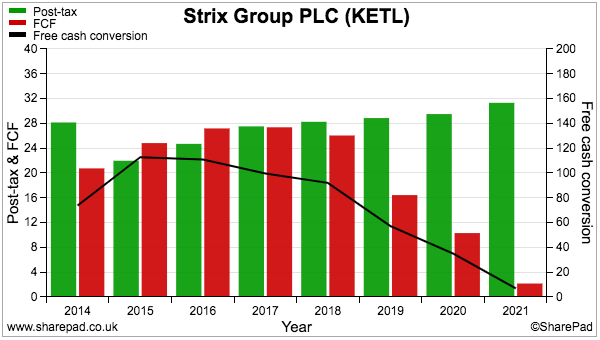

A deteriorating conversion of reported earnings into free cash (black line, right axis) goes some way to explain the higher borrowings:

Earnings often convert into low levels of cash flow due to:

1) Significant cash being absorbed into additional working capital (i.e. through increased stock, later customer payments and earlier supplier payments), and;

2) Expenditure on tangible assets (i.e. property, plant and equipment) and intangible assets (e.g. capitalised development costs) substantially exceeding the associated depreciation and amortisation charged against profit.

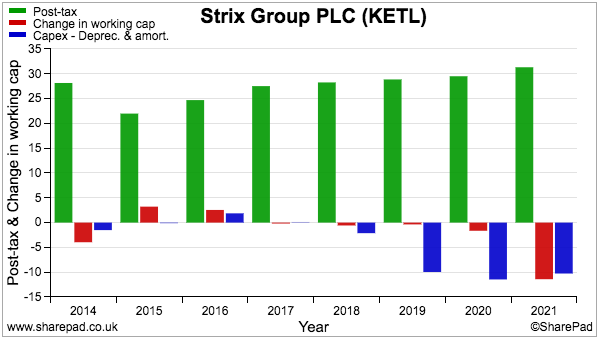

The chart below compares Strix’s earnings to the additional working-capital cash and ‘excess’ capital expenditure:

SharePad shows cash capital expenditure for each of 2019, 2020 and 2021 running at approximately £10 million beyond the amount charged as depreciation against earnings.

The chart also shows an extra £11 million absorbed into working capital during 2021.

The last annual report confirms the Capex was spent mostly constructing and kitting out a new factory in China, while the additional working capital was due in part to the “forward procurement of commodities to secure future profits” .

The annual report also disclosed the company’s maximum “leverage ratio” to be 2.5 times:

The Billi acquisition implied the same ratio would be approximately 1.9x:

“Expecting net debt as at 31 December 2022 to be approximately 1.9x Strix’s 2022 pro forma adjusted EBITDA, with strong deleveraging thereafter to c.1.4x by end of 2023”

The danger of course is the recent profit warning will lift that 1.9x ratio towards the maximum 2.5x, and perhaps prompt awkward conversations between Strix and its banks. More on that in a minute.

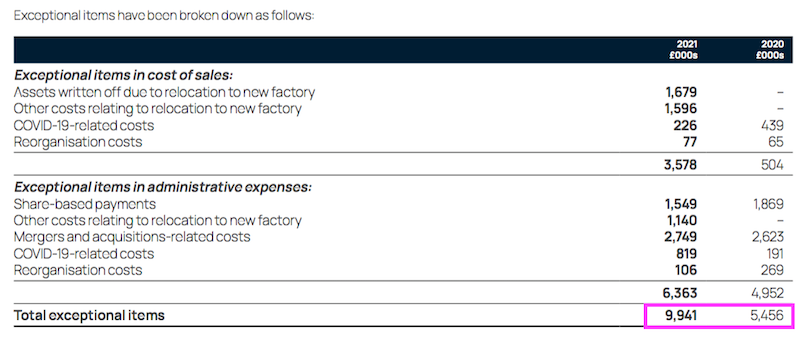

.Exceptional items and useful lives

Strix’s accounts are not perfect, with reported earnings, in particular, being blighted by regular adjustments:

Strix has incurred exceptional “reorganisation” costs every year since at least 2014 and incurred exceptional charges associated with “strategic projects” every year since 2018.

Such items have totalled £15 million during the last five years and would have reduced aggregate adjusted earnings by 10% during the same period.

Furthermore, share-based payments of some £16 million have been deemed to be ‘adjusting’ items since the flotation.

First-half results issued during September contained further exceptional items (£3.7 million) alongside a niggling accounting change.

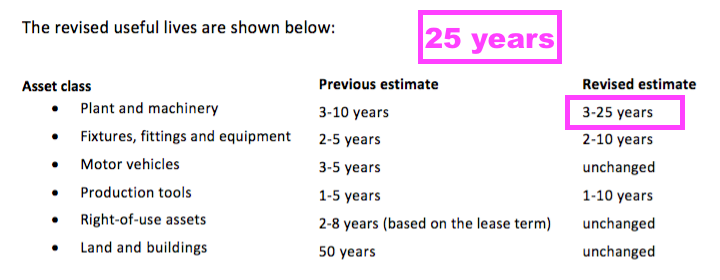

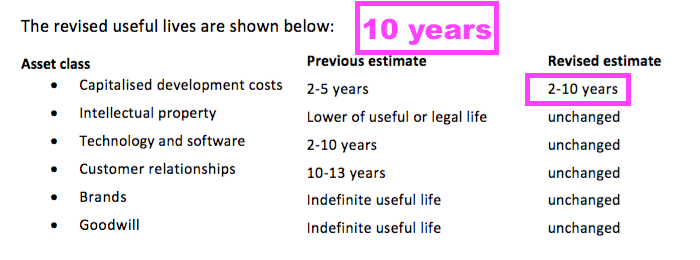

Strix lengthened the ‘useful lives’ of certain tangible and intangible assets, which has spread the associated depreciation and amortisation charges over longer periods… and which in turn has increased accounting profit.

The revised useful lives do look extended.

Certain plant and machinery may now be employed for 25 years…

… while capitalised development costs may now be written down over ten years:

My rule of thumb with useful lives is to question anything beyond ten years for tangible assets and anything beyond five years for capitalised development costs.

Strix confirmed the changes increased half-year profit by £0.9 million and ought to increase current-year profit by £1.8m:

“As highlighted in Note 2, Management revised the useful lives of certain assets at the beginning of the year. As part of this assessment, the useful lives of fixtures and fittings, plant and machinery and production tools were reassessed and extended with the resulting impact being a decrease of £546,000 in the depreciation charged to the condensed interim consolidated statement of comprehensive income for the current H1 period and an expected decrease of £1,098,000 for the full year 2022.”

“As highlighted in Note 2, Management revised the useful lives of certain assets at the beginning of the year. As part of this assessment, the useful lives of capitalised development costs were reassessed and extended with the resulting impact being a decrease of £395,000 in the amortisation charged to the condensed interim consolidated statement of comprehensive income for the current H1 period and an expected decrease of £694,000 for the full year 2022.”

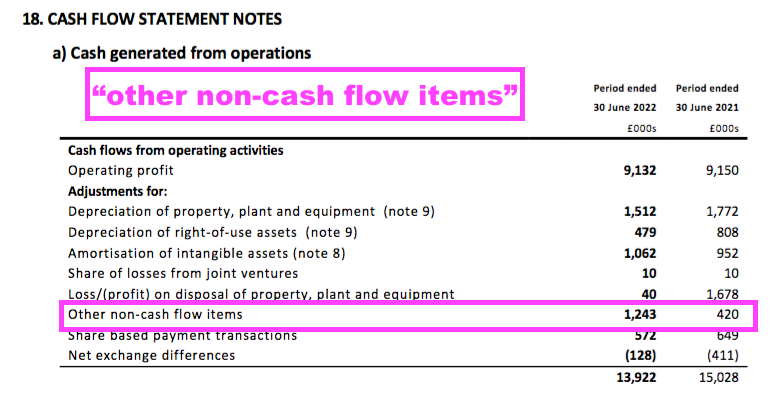

Another irritating first-half entry was the mysterious “other non-cash flow items“, which has quietly become a significant cash-flow figure during the last 18 months:

Bear in mind Strix’s Isle of Man domicile means its financial disclosures are not quite up to the standard of UK-domiciled companies.

Conventional information missing from the accounting notes include geographical revenue, employee numbers and debtor ageing. The all-important auditor’s report is only three pages long, versus at least five pages for a typical AIM small-cap.

And the finance director’s review being tucked away on page 67 of the 2021 annual report is not encouraging.

ESG targets versus LTIP targets

Strix is the first company I have come across that has established a formal ESG board committee:

Management has set a commendable ‘net zero’ target for 2023, and the annual report discloses a number of useful kettle facts that include:

- Global kettle penetration increasing from 38% to 50% would save approximately 14 billion kg of CO2 a year;

- A two-second saving in “steam switch-off time” would save 44GWh per annum, equivalent to £9 million every year in the UK alone, and;

- The average kettle overfill is 30%, meaning £190 million is wasted boiling excess water every year in the UK alone.

The recent profit warning could mean the board’s ESG targets become more achievable than its LTIP earnings targets.

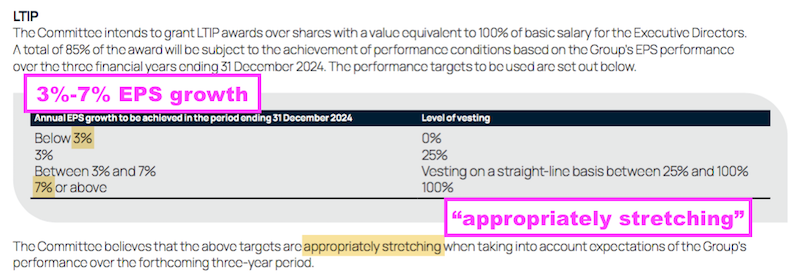

The executives will collect LTIP shares if earnings per share (EPS) advance by at least 3% per annum during the next three years:

85% of the LTIP grant will be awarded if earnings compound at 7% a year — which does not sound that demanding versus that five-year plan to double revenue (requiring approximately 15% compound growth).

Strix describes the minimum 3% LTIP EPS growth target as “appropriately stretching“.

The other 15% of the LTIP is linked to a “reduction in energy usage” of at least 5% per annum.

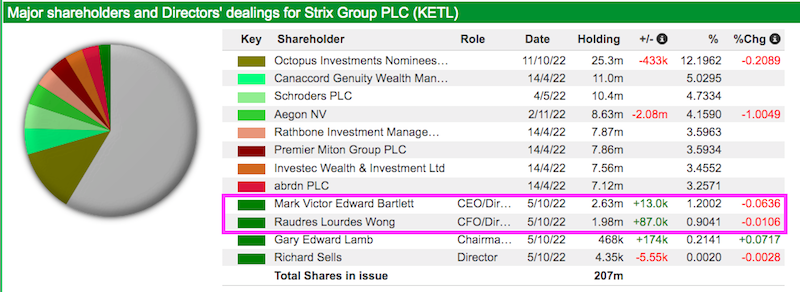

Both the chief exec and finance director have worked at Strix for at least ten years and, from what can tell from the remuneration report, both reside in Hong Kong.

The two executives enjoy a collective £4 million shareholding…

… but appeared somewhat reluctant to participate within the recent placing to help fund the Billi purchase:

Valuation and summary

Last month’s profit warning cited Covid-19 lockdowns in China:

“In recent weeks it has become increasingly evident that the disruptive effect of ongoing lockdowns being enforced in China, whilst relatively short in length, have adversely impacted two of the top five of Strix’s major OEM customers, with further disruption anticipated…

…As a result of lockdown situations as described above and continued macroeconomic and geopolitical uncertainty, not only in China but across a number of its key export markets it now anticipates adjusted profit after tax for the full year to be approximately £23m. The Board recognises that these uncertainties could continue into 2023.”

September’s interims showed adjusted earnings of £11.5 million, which means Strix’s new £23 million projection implies second-half earnings will also be £11.5 million — some 40% below the level from the second-half of 2021.

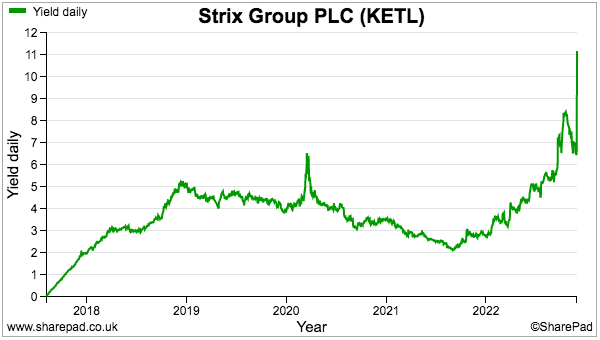

Extrapolate that 40% profit drop to the first-half of 2023, and adjusted earnings could be running at approximately £19 million — which just about covers the £18 million needed to sustain last year’s 8.35p per share dividend.

No wonder Strix’s dividend yield has rocketed beyond 10%:

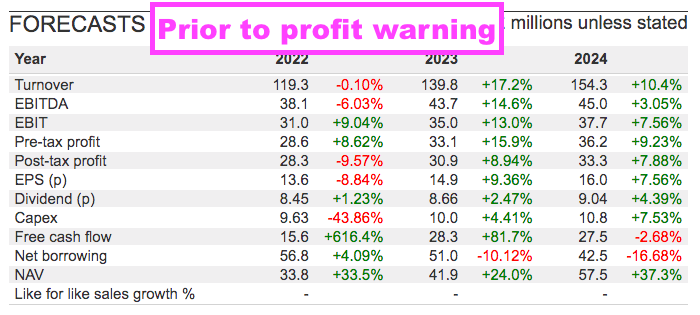

Strix’s new £23 million earnings projection for 2022 is 19% below the £28.3 million SharePad was showing before the bad news:

If Strix’s adjusted Ebitda falls a commensurate 19%, then that could mean the aforementioned 1.9x net-debt-to-Ebitda ratio…

“Expecting net debt as at 31 December 2022 to be approximately 1.9x Strix’s 2022 pro forma adjusted EBITDA, with strong deleveraging thereafter to c.1.4x by end of 2023”

…will rise to beyond 2.3x and closer to that 2.5x covenant limit.

I have to say, the 32% share-price fall looks very understandable given the unsettling mix of the trading difficulties, significant acquisitions and notable borrowings. Not helping matters are the regular exceptional items and recent useful-life extensions, both of which arguably flatter the group’s headline accounting.

Right now the drawbacks seem sufficient to offset Strix’s leading kettle-control position, which is really quite sad as the business does appear to enjoy a genuine competitive ‘moat’ following years of innovation.

With the shares trading 15% below their 2017 flotation price, current Strix investors may well question whether the group’s expansion strategy of the last few years has been worth it.

Perhaps focusing on kettle controls and foregoing major expansion expenditure may have kept Strix a much simpler (and conservatively financed) business that could have been less vulnerable to adverse global events.

Do bear in mind that, back in the day, founder Dr Taylor did like to keep Strix’s financials very straightforward:

“Too little is discussed these days about business financial freedom and job creation while too much attention is paid to venture capitalist business models, which can leave an inventor with little ownership. One of my proudest achievements in business is that I never borrowed a penny from anyone. This is because I always focussed on cash flow and used the revenue from manufacturing to fund innovation.”

Until next time, I wish you safe and healthy investing with SharePad.

Maynard Paton

Maynard writes about his portfolio at maynardpaton.com and co-hosts the Private Investor’s Podcast with Mark Atkinson. He does not own shares in Strix.

Got some thoughts on this week’s article from Maynard? Share these in the SharePad chat. Login to SharePad – click on the chat icon in the top right – select or search for a specific share.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.