Our funds expert turns his attention to the slowly recovering property-focused real estate investment trusts sector. His new addition to the Dynamic 35 is a very actively managed pan European fund of funds that invests across a wide range of real asset-backed niches.

Overall, I have been fairly cautious about the real estate investment trust (REIT) sector in the last few months. As we slowly re-emerge from lockdown, I’m not sure how the varying niches within the commercial property market will play out. I am absolutely not convinced by the idea that we’ll all be working from home and city centres are dead. I’m not even completely convinced that every high street is dead. Yet you would have to be a fool to think working from home will return to pre-COVID levels, or that e-commerce growth will slow down. My sense is that it is probably a bit too early to call specific trends and my hunch is that different bits of the property spectrum will recover at different speeds.

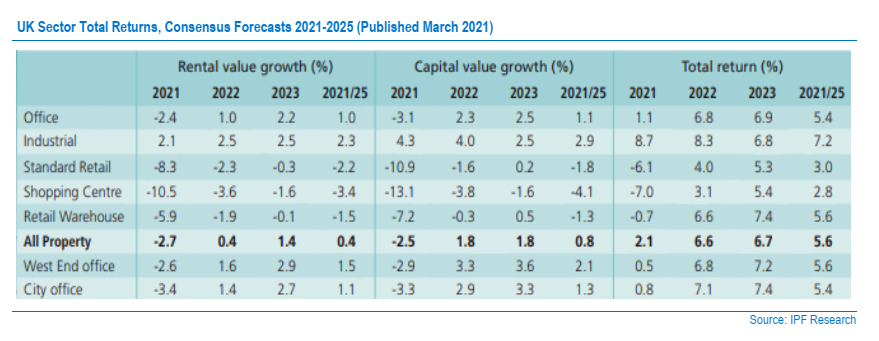

A recent research report on the UK listed property fund space from the excellent analysts at Investec quoted some industry benchmark research which nicely maps out the possibility that different types of real assets might have diverging performance. It also reminds us that the recovery might not be a classic high growth recovery spurt, and that prices might only rise gently as investors work out the new landscape. Overall, the latest “IPF UK Consensus Forecasts are for an All Property total return of 2.1% this year”, the Investec report observes, “and an average 5.6% over the next five years, while the Industrial and Standard Retail sector five-year forecast total returns are 7.2% and 3.0% respectively.” The detailed table below from the Investec report drills a bit further into the detail.

For me, the key observation – apart from that cautious recovery – is the divergence in returns between different types of assets. This introduces the idea of polarisation around subsector returns. Or as the Investec report summarises: Industrials are “expected to produce a total return of 8.7% this year, and an average 7.2% over the next five years. However, Standard Retail (-6.1% in 2021 and a five-year average of 3.0%) and Shopping Centres (-7.0% in 2021 and a five-year average of 2.8%) are expected to continue to struggle”.

So, navigating around this new post-pandemic landscape will be difficult. That, for me, means you need a careful hand at the tiller working through various choices: Retail vs Office, UK vs Europe, Industrial vs Student property.

My clear preference is for actively managed funds and a little later we’ll show that returns from some actively managed funds have been superior to the growing number of REIT ETFs.

But there is one other alternative way to play property – open-ended property funds. I have always thought that this structure is a terrible idea in real estate. You are combining a difficult-to-liquidate real asset with a daily redemption unit trust structure. In my view, this was always going to end in tears – as it has in recent years. The Investec report is especially punchy on this last point: “we wonder how advisors who have shunned investment companies are able to look their clients in the eye”. If you want to invest in real assets and property, use REITs.

But which REITs?

That is a really tricky question to answer. I think there are some excellent individual funds but as I have already said, navigating through the dozens of listed UK funds plus a longer list of European property funds is a near unimaginable task for the retail investor (and their advisers). You could use ETFs but I have my doubts – although these invest in shares of REITs they are simply led by momentum flows and market cap measures.

I would prefer a fund of funds that invests in a wide, geographically dispersed range of REITs (and European property funds). This is where the long-established TR Property Investment Trust comes in, managed under the BMO umbrella by the experienced Marcus Phayre Mudge. The idea here is very simple – TR invests across Europe and the UK in REITs and property funds, with a very active mandate to seek good value and a decent income yield. That yield is above 3% and the fund is absolutely no minnow with net assets of over £1.4 billion. The tables below give you some fund basics.

Fund Basics

|

Fund manager(s): Marcus Phayre-Mudge |

|

Fund type: UK Investment Trust |

|

Sector: AIC Property Securities |

|

Benchmark: FTSE EPRA/NAREIT |

|

Fund currency: GBP |

|

Fund size: £1433.8m |

|

Share price: 426.0p |

|

Historic Yield: 3.3% |

|

Net gearing: 14.5% |

|

Manager: Marcus Phayre-Mudge |

|

Initial charge: 0.00% |

|

Ongoing charge: 0.59% |

|

Ann. Mgmt fee: £3.745m plus 0.20% |

|

Ann. Return 5 Years: 9.69% |

|

Price frequency: Daily |

|

Performance fee: 15% of outperformance |

|

Distribution policy: Semi-annual |

|

Share currency: GBP |

|

Payment date(s): January, August |

|

Current discount: 4.4% |

Performance

Before I dig into the portfolio, I want to highlight why I have opted for a fund of funds, multi-geography approach. In simple terms you not only get that active management, but you are also benefitting from a fund with a clear performance track record, or should I say outperformance.

The first piece of evidence comes from the table, which is from TR Property. It shows discrete year-on-year performance. Bar the strange market of 2020, you will see that the fund has beaten its benchmark in share price terms in all years – in fund NAV terms, it’s outperformed the index every year.

Discrete rolling annual performance as at 30.04.2021 (%):

|

2021 |

2020 |

2019 |

2018 |

2017 | |

|

Fund NAV |

27.92 |

-9.56 |

3.54 |

17.87 |

12.50 |

|

Benchmark |

22.14 |

-11.44 |

-0.02 |

12.79 |

10.00 |

|

Share Price |

32.00 |

-13.65 |

2.72 |

24.75 |

15.39 |

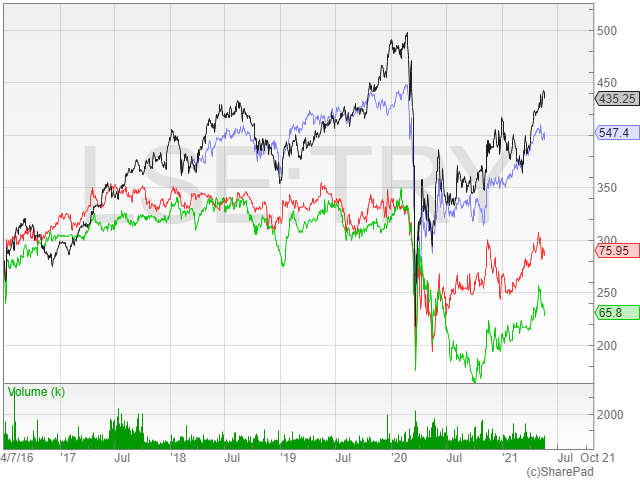

Next up we have this chart which looks at recent returns for TR Property versus a bunch of sensible peers including the big ETF from iShares in this space plus Standard Life Property and UK Commercial Property. The ETF was only issued in 2018. My impression is that over most periods’ TR Property has clearly delivered superior returns although the ETF has also produced fairly decent returns compared to its UK rivals.

Comparing performance of TR vs peers

Blue Line : iShares Developed Markets Property Yield ETF DPYG

Red line : UK Commercial property UKCM

Green Line: Standard Life Inv Property Income Trust SLI

The Portfolio

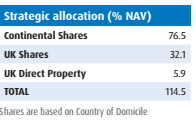

What is behind these superior returns? Put simply, a highly differentiated portfolio of REITs and funds that spans Europe: the Trust’s non-sterling exposure is around 75%. That international diversification is important as it brings with it FX implications: weaker sterling provides additional valuation gains, although that can work in reverse if sterling strengthens as it has done very recently.

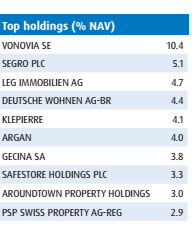

The two tables below sum up the diversification. The top holdings are in a German residential business called Vonovia while the second biggest holding is in UK industrial property business SEGRO. The fund does invest in well-known UK names, but that exposure is very low. Instead, the two key exposures are to German residential property (around a quarter of the fund) and European wide industrial estate businesses at 17% of the fund. By contrast, UK London property exposure is very low at under 5% while European shopping centres exposure is much higher at 8.4%.

It’s also worth dwelling on recent performance, reported in the fund’s last fact sheet.

The fund reports a “significant divergence in sub-sector returns as logistics and industrials continued to perform well, alongside German residential and the secure income of specialist healthcare and supermarket sectors. The fund maintains its limited exposure to retail which again proved beneficial, particularly in central London where the company avoided names such as Shaftesbury and Capco.”

What’s happening in Germany

I also wanted to focus a little on that German focus, which represents something akin to a quarter of the value of the fund. These are investments in residential businesses who rent out (mostly) flats to residents as well as sell on properties that they have refurbished. Business was booming but then Berlin become something of a cause célèbre when its state government imposed a rent freeze. This attracted huge controversy, not least from German politicians who argued that it would do little to help the great mass of renters but would also worsen new supply of residential units. I have a great deal of sympathy for young Berliners worried that their city might turn into a Teutonic version of London where anyone who is under 40 and not in possession of a very high-paid job struggles to buy their own flat or home. This is a very real problem but rent controls are not, in my view, the solution. I also think rent controls can be highly discriminatory and somewhat arbitrary. Which is also what the German judicial system concluded. Here’s TR Property’s own account of recent events, which I think is very fair.

“The German Constitutional Court ruled that the Meitendekel (rent freeze) imposed by the State of Berlin was unlawful and that rent controls were the preserve of federal law not local state regulation. Our exposure to Berlin is through Phoenix Spree (+10.5%) and Deutsche Wohnen (+13.1%), which both enjoyed a relief rally. However, the German political landscape is in a state of flux ahead of the general election in September, and the demands for further rent controls (beyond the already strident restrictions) will always be vote winners. We can only hope that the collapse in the number of new apartments under construction in Berlin, a direct response to the rent cap, is a message now understood by lawmakers looking beyond the self-interest of those fortunate enough to already be renting at sub-market regulated rents. “

I think that German residential property funds are not completely out of the woods but the environment is much more hospitable now, with more certainty about the long term. The key insight here is that German houses are cheap, in relative terms, and its big cities are even cheaper by global standards – Berlin in particular. Germany also has a well-established and vibrant institutional rental market which shows no signs of slowing down.

Risks

I have already carefully identified some risks investors need to be aware of. I’d repeat and highlight the following:

- Currency exposure. A very large portion of the fund is in Euros which could work against the investor if sterling continues to strengthen.

- The German property exposure is substantial and still presents policy-based risks. Rent freezes may be off the agenda but other measures may be introduced.

- It’s still not remotely clear how the post pandemic recovery will play out in real asset terms.

- The fund has a strong focus on industrial property which is, in relative terms, very highly priced and one could argue it is too expensive compared to, say, prime office property in London.

My bottom line

My hunch is that real assets such as commercial and residential property will continue to prosper in the imminent recovery. Investors are growing mindful of the risks of accelerating inflation, with property-based assets providing a useful hedge against rising prices. That said, I have my doubts about the resilience of the office and retail-based recovery, but by using an actively managed fund like TR Property you should benefit from a very diversified portfolio, both at the geographical and sub-sector level. I would certainly prioritise holding TR Property over any individual fund within the space e.g an office-based REIT. That said, I think there are some niche segments within the property spectrum that I might hold alongside this fund – I am especially interested in the student property market as well as social housing for the homeless. But for multi-segment, diversified exposure to REITs as an asset class, I cannot think of a better investment than TR Property. And if all that wasn’t enough, you also get a handy and well-backed dividend stream, plus overall gearing on the fund is low and the discount at 4% feels about right as we head into a new recovery phase.

David Stevenson

One important note – the funds annual results are due any day now and so there might be some elevated price volatility ahead and after the results.

Are you currently holding TR Property or a similar fund of funds? We’d love to hear from you! Share your experiences in the comments section below.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.

I have held TRY since 2014 and it has given me an annual return of 11.4%, which has only been bettered by BBOX in this sector. I also have SLI, whose performance has been poor and I was going to sell out until I realised they were on a discount of 40% which I thought excessive so I held on with the comfort of a good yield and they have recovered. I have moved away from open-ended property funds altogether after getting caught in the first M&G Property freezing and also am focussing on warehouses and healthcare rather than high street retail. My exposure to offices is more outside London through RGL.

I tend to regard my own property as a fairly large investment in this sector which I limit accordingly. Of course there are sectors that I am not exposed to, and a dwelling whilst part of one’s wealth, is not necessarily an investment.

I would like to suggest David Stevenson takes a look at UK-listed Sirius Real Estate (SRE), which has an excellent growth record as a property developer and operator of German business parks. NAV about £1.1 billion, plus a joint venture with Legal and General to expand further by acquisition.

I like their model of end-to-end ownership, so they own the sites, develop and adapt them for the local market, including WeWork-style micro-units, but also do the tenant recruitment, property management and offer add-on services that seem to keep tenants happy. They are not just landlords passively collecting the rent, taking their cut and paying most of their revenue out in dividends. Their business barely rippled through Covid.