Investing in mining stocks is always a speculative exercise.

On a practical level, although there is some logic to investing in large diversified global mining groups – the Rios, BHPs and Glencores – there are also some very obvious ‘execution’ risks which vary company by company. All it takes is for one disaster at one site – or a big policy change in a home country – and the share price can start gyrating.

The obvious alternative is to invest in a basket of these large-cap stocks, but this introduces an obvious additional problem. How do you navigate between different individual stocks and the range of individual commodity markets these businesses are involved in?

But if we step back even further there’s another challenge; commodity markets exhibit high correlations between each other i.e. they tend to move in one broad cycle. There are some outlier markets around energy and specialist metals, but by and large interest in commodities waxes and wanes with the broad economic cycle (and worries about inflation).

But even that last statement is a broad generalisation – do have a look at my recent Citywire column on the subject for a more detailed explanation of how commodity markets are impacted by very broad forces within modern society. You can see that article here.

Where are we in the cycle?

So, with these numerous caveats in place, I’d still make one core argument. My sense is that we are at the start of a multiyear bull cycle for commodities, powered by lots of different forces. I might be wrong about this and maybe commodities will have a bad few years but I think the odds are stacked against that bear case. Here is my thought experiment: if you think that the current reflation will end badly in an inflationary resurgence, then commodities are, usually, a great place to be and the recent gains are just the beginning.

But let us assume it doesn’t end well and that the economies slump again. Recessions loom again. Worries about systemic instability prompt crisis measures. Stockmarkets tumble. Fear spreads. What do you think investors will turn to? Surely a decent number might turn to precious metals and gold (and I suppose Bitcoin?!).

Mining resilience

That’s why you have a fund that can move back and forth between cyclical commodities such as iron or copper and contracyclical precious metals. And in addition there’s some evidence that over the top of these cyclical rallies and slumps, there might be some specific commodities related to the green transition that might move in very different cycles and require different strategies.

If you are happy to do this all using single stocks, fine – be my guest and take that stock specific risk. I also think using a broad passive fund is not exactly perfect, but I can see some investors saying “Hey, I don’t need to know which cycles works when, just give me exposure to what the market decides via a tracker fund”.

My own preference is for active management and in that case, I think the best option is also the most well established one – the BlackRock World Mining Trust. This London listed investment trust has been around for decades, has respected managers and is of a decent size – over a billion market cap. It’s had a good few months after the initial panic surrounding the virus but I don’t think it’s too late to maybe think about allocating some capital to this fund.

BlackRock World Mining factsheet

- Fund Manager Evy Hambro, Olivia Markham

- Price 608p

- Fund yield 3.3%

- Premium 1.7%

- Market cap £1084m

- Ticker BRWM

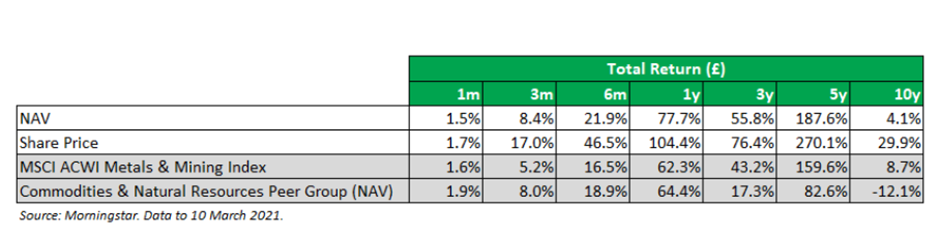

Performance

The table below is from a recent report on the trust from fund analysts at Winterfloods in early March. As you can see the trust has pretty comprehensively beaten the stated benchmarks over most periods although if we are honest, long-term, 10-year returns have been fairly dismal. But that’s in large part because we’ve had many years over the last decade where commodities have produced negative returns as spot prices have in some cases fallen back sharply.

The trust has also recently produced its annual results to the end of last year, and those numbers look much more impressive: NAV up 31.8% on a total return basis, outperforming the MSCI ACWI Metals & Mining Index, which rose 20.6%, and the EMIX Global Mining Index, which was up 21.8%. It seems like its main holding – mining companies – found themselves in a sweet spot following the initial pandemic panic, helped along by a recent focus on balance sheet discipline which involved cutting costs and being careful with capex spending. In particular, the trust benefitted from significant copper exposure in the second half of the year and gold exposure in the first half of the year, all of which was a key driver of performance. Since 31 December the NAV is up a further 6.4% versus a 6.7% rise for the EMIX Global Mining Index. BlackRock World Mining also pays quarterly dividends, which totalled 20.3p in 2020, down 7.7% from 22.0p for 2019. This equates to a yield of 3.4% on the current BlackRock World Mining Trust share price and reflects the 9.2% year-on-year decline to 20.4p in its revenue per share.

Analysts at Winterfloods also report that average commodity prices for 2020 were substantially “higher year-on-year for precious metals including Palladium (+43%), Gold (+27%) and Silver (+27%) as well as Iron Ore (+16%) and Uranium (+14%). Base Metals rerated significantly since the lows of March, with all prices finishing the year higher, however with the exception of copper average prices were actually lower on a year-on-year basis reflecting the steep Covid-19 drawdown in March”.

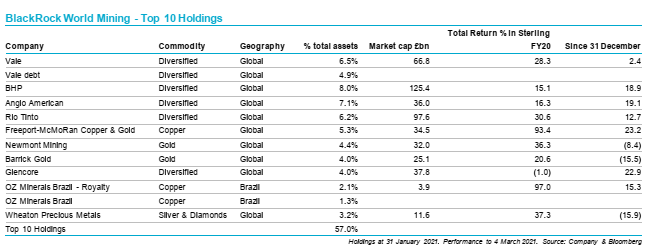

What’s in the portfolio?

The two sets of graphics below – a table first and then two pie charts – outline what’s inside the trust’s portfolio. I’d make a couple of observations. The first is that you are heavily exposed to the big, mega cap globally diversified mining giants. These top nine globally diversified giants – ranging from Value to Glencore – comprise over 50% of the total assets (including debt). Their underlying commodity exposure is also reflected in the fund though there are probably two big overweight exposures – copper at just under 20% of the value of the fund and precious metals (gold, silver and platinum) at just under 30%.

Bottom line

One key feature of all investment trusts, but especially marked in the case of this trust, is that discounts between NAV and the share price can vary greatly. Precisely because many investors see this fund as somewhat cyclical in nature, the discount has expanded to double digits in years of poor returns for commodities. In 2020 that discount shot out to 12% (roughly the average for the last ten years) and then came back in sharply to end the year at around 3% and is now trading at a 3% premium to NAV. Partly as a result, the fund also moves back and forth between buying in shares – when the discount is large – and issuing new shares at a premium. The trust has issued 3.7m shares since 31 December (2.1% of share capital) whereas over the last ten years the trust has bought back a total of 3.8m shares, worth £13.4m.

If I’m honest, the current 3% premium doesn’t look a bargain. Although I think the current bullish cycle has much further to run (possibly as much as a year or two), I think we will have scares over the next three to six months. That might be a stock market scare – a big sell off – or a scare about increasing interest rates – another taper tantrum – or a growth scare if the virus comes back again. At that point, all those high expectations for a cyclical recovery will look a bit more tentative again and I wouldn’t be surprised to see the share price come down again and that premium revert to a small discount. Thus, if I were timing a big purchase, I would possibly bide my time. But if this isn’t your bag – market timing is usually a fruitless task – then simply use this excellent trust as your core exposure to commodities.

So, to sum it all up, by investing in this fund you are gaining exposure to the following portfolio:

- All the main globally diversified large cap mining equities

- A mixed bag of underlying commodities with a current emphasis on PMs and metals that will do well in a reflationary growth environment

- But you also have experienced managers who can switch into different strategies as the rebound matures

- There’s also a smaller overlay of income-focused assets that help push up the dividend yield

There are some very obvious risks. The first I have already detailed – I do not think the shares are that cheap by historic standards at the moment. They will also be vulnerable to growth scares as investors worry about rising interest rates in the USA. That in turn makes these shares volatile – these are not for bog standard middle of the road cautious investors – stick with a sensible mix of bonds and equities. And last but by no means least this trust isn’t heavily exposed to the mid to small cap miners where the growth potential is arguably greater – but the risk levels are also much higher. If that is your bag, look at Baker Steel resources Fund.

Winterflood view

“BlackRock World Mining and the commodities sector enjoyed a good year in 2020, which, as Evy Hambro acknowledged in a results call last week, is not what might have been expected given a global downturn. However, China’s rapid recovery from the impact of Covid-19, accompanied by the discipline of mining companies, protected value and, in our opinion, leaves the sector well placed to prosper in the global economic recovery that is projected for this year.

The decision to reduce the total dividend in respect of 2020 in line with the decline in the fund’s revenue may be seen as a disappointing development. However, we believe the decision was the correct one, given the stated policy of fully distributing all of the income in any one year rather than pursuing a progressive dividend. We would expect the fund to see an increase in its dividend in respect of 2021 as a result of growing dividends from its portfolio companies.

We continue to rate the experienced investment team highly and note the fund’s impressive performance over the last 12 months, with its NAV up 78% and its share price rising 104% as it has been re-rated. With a market capitalisation of over £1bn, the fund is by far the largest in the peer group and, as such, offers good secondary market liquidity. We continue to recommend BlackRock World Mining Fund for investors looking for well-managed, diversified exposure to the commodities sector.”

Numis Views:

“We believe that BlackRock World Mining (£719m market cap) is a good way to gain diversified exposure to the mining sector, which can be highly volatile on a stock-specific basis. The managers remain optimistic for the sector driven by a strong corporate outlook (strong balance sheets, higher margins, discipline in returns to shareholders) and commodity market imbalances. Sentiment towards the sector is strong, reflected in the fund’s premium of 3%, as it is expected to benefit from the pickup in fiscal spending which should drive commodity demand.”

David Stevenson

Contact on Twitter: @advinvestor

Check out my blog at www.adventurousinvestor.com

Executive editor at www.altfi.com and www.etfstream.com

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.