I must say I’m very excited to be writing for SharePad and ShareScope. I’ve been an avid user of both for more than 10 years and I know that both products are widely used by smart investors who want to a more in-depth analysis of stocks and funds.

Many of you will know me from regular columns in the Financial Times (The Adventurous Investor), Citywire and MoneyWeek. Some of you may also know me from my regular blog – www.adventurousinvestor.com – where you’ll find a great deal more macro commentary and a running commentary on interesting new funds.

My plan with this bi-weekly article is to focus in on investment trusts and not stray too much into broader market views – you’ll continue to find those at the FT and Citywire as well as on my blog. I want to focus here on actionable ideas for experienced investors relating to investment trusts.

Every two weeks I’ll focus on one investment trust where I’ll dig a little deeper into the strategy and the holdings. Along the way I’ll build up two crucial lists – the Dynamic 35, and the Prudent 15.

The Dynamic35 will consist of the, you guessed it, 35 most interesting growth-oriented investment trusts on the London market. These are funds for the long-term investor who can live with market volatility but wants to grow their capital.

In my humble opinion no one should buy into these funds unless they are willing to sit tight for 10 years or more. I’ll also be attaching either a BUY or HOLD rating to a fund in the list – my sense is that if it’s on the list it’s probably a long term buy but I’m also aware that market timing does matter and sometimes (as in this weeks example) I think one has to accept that a share or fund might be fully valued in a particular moment in time. That presents a challenge for say a lump sum investor who has to invest the whole consideration now – which is why I might post a HOLD rating. If you are drip feeding on a regular basis, then I’d assume a buy rating.

Crucially I’ve made the list long at 35 investment funds because I want to include much more adventurous ideas which may not appeal to all readers. My working assumption is that within 35 funds nearly every growth investor should find something worth investing in. I certainly don’t assume that readers will buy all 35!!

The Prudent 15 is also, I think, fairly self-explanatory – I’m after the best 15 funds for the more defensive and prudent investor who has a more ‘balanced’ view of the markets. This means they are seeking some market downside protection and are more concerned about market volatility. Again, I’ll move between Buy and HOLD ratings on this list, as I introduce a new constituent of the Prudent 15 List every few articles.

Focus on investment trusts – Scottish Mortgage

So, lets kick off with our first investment trust member of the Dynamic 35 – Scottish Mortgage. I’m sure many of you will know about this massive fund, especially if you’re into global growth stocks. Familiarity might breed contempt but I think SMT – Scottish Mortgage – really does deserve its place at the core of any active investment trust portfolio. I personally own shares in this fund in one of my portfolios and I also constantly drip feed money into it on a monthly basis for the very long term.

That said readers might notice that I have a HOLDS rating on the fund. This is me being cautious. As we’ll see SMT is an avowedly growth-oriented fund with lots of (expensive) techy holdings inside the portfolio. If I were a lump sum investor looking to deploy all my cash now, I’d be super cautious. Although my overall view is that 2020 should be another good year for equities, I’m also very cautious about market volatility over the next six to nine months (especially leading up to the US Presidential election).

OK, with each investment trust I’ll go through a number of steps:

- The basic facts

- Fund analysis

- Recent results plus a smattering of comments from brokers analyst who closely follow the fund. This more in depth will usually be found on my blog, http://www.adventurousinvestor.com

The Basic Facts

| Trust/fund | Scottish Mortgage |

| Ticker | SMT |

| Discount or premium | 1.4% |

| Current rating | HOLD |

| Style | Global Growth |

| Market Cap | £8.5 billion |

| Managers | James Anderson and Tom Slater |

| Yield | 0.5% |

| Average bid offer spread | 0.1% |

| Benchmark outperformance (MSCI World):

1 year 3 year 5 year |

Yes

Yes Yes |

| Gearing | 7% |

| Website | www.scottishmortgageit.com |

| TER (Total Expense Ratio) | 0.37% |

Correct as 8th January 2020

Please note that David Stevenson currently owns shares in Scottish Mortgage

My analysis

Short term HOLD, long term BUY

SMT could very easily sit at the very heart of a core portfolio of long-term growth equities from around the world. It’s fairly unique in that it contains an interesting mix of both publicly listed mega cap large companies (around 80 to 75%) as well as a substantial portfolio of private, unlisted private equity investments (roughly 20% of the fund’s value).

That latter bunch of companies would normally make me suspicious. I’m not convinced that most public equities fund managers can do private venture capital very well (I’m thinking of Neil Woodford here) but my sense is that if anyone can make a go of it, then its Baillie Gifford (the fund manager behind the SMT).

One other key initial observation. Scottish Worldwide has a sister fund called Edinburgh Worldwide which has a similar mandate but is more focused on mid to small cap publicly quoted businesses. I invest in both funds but with Scottish Mortgage I deploy the larger allocation – a mirror of the market cap split between the two funds.

SMT is a vehicle for the long-term investor who is willing to weather the ups and downs of investing in a particular type of company.

If I had to characterise a typical SMT portfolio investment it is likely to have some or all of the following attributes:

- Businesses that boast a strong proprietal advantage in a technology system or platform of some sort

- The business is likely to be a globally scaleable business that uses that technology (or smart IP) to build a global presence with high margins

- Many of the businesses in the portfolio are led by charismatic entrepreneurs such as Jeff Bezos or Elon Musk (Amazon and Tesla are two top ten holdings). The philosophy is all about building relationships with business creatives rather than doing specific transactions.

This tech heavy, global focus is likely to result in a portfolio of fast growth stocks with high share price valuations. It’s also likely to have a high beta to the US equity markets i.e. it’ll move disproportionately against the benchmark, more on the upside as well as on the downside. SMT has also been developing a strong focus on Asian businesses with Tencent and Alibaba as top ten holdings. That introduces an obvious source of volatility given the current US China face off. The BG managers aren’t afraid of this Chinese connection though – Baillie Gifford last year opened an office in Shanghai, so its obvious that the fund will continue to invest aggressively in scale tech businesses that have a deep understanding of their customers.

We can dig a little deeper into the philosophy of the fund by listening to what the management have been telling investors at recent Investor Days. Matt Hose, a funds analyst at Jefferies, attended the most recent one (January 202) and reported back on what the managers saw as three decade long drivers.

These were:

“the impact of the advancement of Moore’s Law; increasingly advanced software; and the ubiquity of mobile communications. The rise of online marketplaces and the power of their datasets was also a recurring theme, with the managers seeing companies such as Amazon as still in control of their own destiny. To this end, the example was given of how Amazon’s dataset last year supported the launch of one-day shipping for Prime customers, resulting in an acceleration of the marketplace’s growth.”

What’s obvious from this narrative is that you are buying into a portfolio of growth oriented businesses, many of them private, most expensive on classic fundamental measures. But manager James Anderson reckons ‘haven’t seen anything yet’ regarding the performance of growth and that some companies expected to mean revert (in terms of value) ‘will be destroyed’.

One last point from this Investors meeting, reported on by Matt Hose. The managers are proud of their investments in private businesses, and regard this as a way to try to understand emergent technologies, like synthetic biology.

If we look at the businesses in the portfolio – many of which have been in there for many years – we’ll instantly see some familiar names. Amazon is a big long-term bet on lots of things as are its Chinese rivals. Illumina might not be a familiar name, but this medical diagnostics business is a favourite amongst many healthcare investors who think that we are on the verge of a genomics revolution, led by sequencing machines and array-based systems. You’ll also see Tesla in there. I’m very ambivalent about the world’s favourite e-car manufacturer but despite my cynicism this stock as defied the bears and short sellers and has recently been pushing new highs. I’m also a tad cynical about Ferrari but think that ASML is a wonderful business.

Scottish Mortgage – Top 10 Holdings

| Total Return % in Sterling | |||||

| Company | Business | % total assets | Market cap £bn | HY19 | Since 30 September |

| Amazon | Online retailer | 9.0% | 691.6 | 3.1 | (1.2) |

| Illumina | Gene Sequencing | 7.5% | 33.9 | 3.5 | (6.9) |

| Alibaba | Online platform | 6.1% | 379.1 | (3.1) | 7.0 |

| Tencent | Internet service portal | 6.1% | 318.2 | (4.4) | (1.9) |

| Tesla Inc | Electric cars | 4.6% | 47.2 | (9.0) | 33.6 |

| ASML | Photolithography for semiconductors | 3.8% | 88.6 | 41.2 | 4.5 |

| Kering | Luxury fashion | 3.3% | 56.7 | (4.8) | 8.9 |

| Ferrari | Luxury cars | 3.0% | 23.9 | 22.8 | 2.7 |

| Netflix | Online video streaming | 2.4% | 99.0 | (20.7) | 3.8 |

| Ant International | Online financial services | 2.40% | n/a | n/a | n/a |

| Top 10 Holdings | 48.2% | ||||

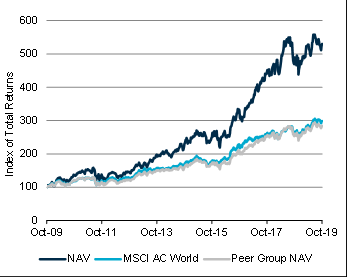

The true measure of a fund like Scottish Mortgage is its track record. And on this measure, as these charts from Numis below show, SMT has consistently delivered excellent returns for investors. That has largely come from a strong active bias, focusing on a small number of hugely successful businesses, as well as the current mania for global tech firms. The cynic might argue that this astonishing bull run must be about to come to an end – echoes of 2001 perhaps – but I wouldn’t bet the bank on that contrarianism. My sense is that we are only mid-way through an astonishing technological leap forward and many of the businesses in this portfolio are at the forefront of revolutions that not only favour the brave but also those with giant market caps and easy access to capital markets.

Scottish Mortgage – 10 Year Performance History

It’s also worth taking note of what I call fund hygiene i.e how considerate are the managers of private shareholders? On this score SMT does very well. The shares are very liquid with a typical bid offer spread of around 0.1% and the total cost of ownership is an amazing 0.37%. I say amazing because this TER (Total Expense Ratio) is not that far off what many index tracking ETFs charge but instead you get a disciplined, active portfolio.

I also like the fact that the fund has kept issuing stock which has helped keep the premium to acceptable levels. As I write the premium is at 1.5% although in tech sell offs that premium tends to move into a discount, making this fund a classic leveraged play on growth stocks. The fund also deploys some very cheap long-term leverage – debt is at 12% of NAV (Net Asset Value) – which helps boost those returns.

Scottish Mortgage – 10 Year Discount History

My Bottom Line

I think Scottish Mortgage is a classic core holding for a long-term investor looking for growth stocks with lots of upside but also potentially lots of downside volatility. It’s well run, cheap, and is globally diversified. My own hunch is that it might be closer to being fully valued in the short to medium term which is why I have a HOLD rating on it at the moment but for the long-term type who can invest through thick and thin this is the classic Dynamic 35 fund!

Summary of recent results and research from brokers

Scottish Mortgage Half Year Report Announcement (London Stock Exchange RNS)

NAV TR (Net Asset Value Total Return) +3.2% vs +9.9% for the FTSE All-World index. Share price TR -1.3%. Returns over the period lagged as companies with low sensitivity to economic growth outperformed, and the longevity of internet platform companies came under question – a theme well represented in SMT’s portfolio. Portfolio allocation at period end was 76% listed equities and 22.1% unlisted securities.

The NAV per share (with debt at fair) increased 3.2% over the six month period to 30/09/19, against a 9.9% total return from the FTSE All-World Index (£). Post the period-end, the NAV has increased a further 2%, against 0.1% from the FTSE All-World (£). The shares currently trade on a 1.5% estimated discount to NAV.

Statement from Chair: “We see no evidence that the dim global economic conditions or the unappealing international political environment are undermining the tectonic shifts and structural advances driven by broadening and accelerating technological progress.”

Portfolio activity (Jefferies): “Portfolio turnover remains low, consistent with the manager’s long-term time horizon, with 60% of assets having a holding period of over five years. Furthermore, activity remains focused on investment at the unquoted stage. To this end, purchases were made of Chinese search engine Bytedance, luggage designer and retailer JRSK, Aurora Innovation – a developer of driverless vehicle technology, and Zoom – a remote conferencing provider. SMT also participated in subsequent funding rounds for the existing holdings in Ginkgo Bioworks, Tempus Labs, and Thumbtack”.

Portfolio (Numis): “There were 84 holdings at 30 September including 42 unlisted investments representing 22.2% of the portfolio in aggregate. This compares with 80 at 30 September 2018 including 37 unlisted investments representing 15.0% of the portfolio. The portfolio remains concentrated, with 48.4% of the value represented by the top 10 investments. The fund currently has gearing of 7% and an active share of 94%.”

Portfolio Activity (Numis): “The manager takes a long-term approach, reflected in portfolio turnover is just 10%. The largest new purchase was Bytedance (0.7% of total assets), the Chinese technology company that owns TikTok. There was a significant addition made to Tempus Labs Series E (molecular diagnostic tests), while there was a significant reduction in Zalando (online clothing retail).” Holdings at 30 September. Performance to 7 November. Source: Company & Bloomberg

Unquoted holdings (Jefferies): Unlisted investments represented 22% of total assets at 30/09/19. This is approaching the 25% investment policy limit (measured at the time of purchase) and a little ahead of the 20% that the managers have stated is around the right level. … The potential listings next year of Ant Financial and Airbnb could help address the issue and maintain the throughput of holding certain investments in both the unquoted and quoted stages that has so far worked well for the fund.

Numis View: “Scottish Mortgage (£7.6bn market cap) has a unique long-term investment approach that focuses on disruptive growth companies with no regard to market indices and is differentiated by its ability to source investments from both quoted and unquoted markets. It benefits from a low expense ratio of 0.36%, an active discount control, and has an outstanding track record, with NAV total returns of 17.8% pa over the past decade, compared with 11.6% pa from the MSCI AC World Index (total return in Sterling

Source: Report from Annual Investors Forum by Matt Hose from Jefferies

One last update, from Matt Hose at Jefferies who picks up the impact on the fund from the share price ascent of Tesla’s which ended last week up 15%, and is now up 79% YTD.

According to Matt “based on the December factsheet, we estimate Tesla now represents c.12% of the portfolio, becoming the trust’s largest holding if the position has been run. SMT’s resulting strong NAV performance of late will have also reduced the weighting to unquoted investments to 18%, thereby offering some useful headroom to the 25% limit (at the time of purchase) within the investment policy”.

I have to say I’m a bit nonplussed by the rocketing Tesla share price. I’m absolutely not a Tesla hater but even I struggle to think that the share price is remotely realistic. But hey, what do I know.

David Stevenson

Contact on Twitter: @advinvestor

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.