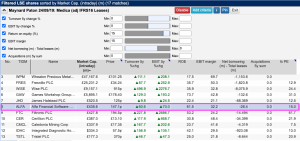

Screening For My Next Value Winner: SThree (LSE: STEM)

Recruitment agency SThree surprises Maynard Paton by appearing in a screen that hunts for asset-backed bargains. A notable cash position and a huge debtor book are the key deep-value attractions. I am once again looking for ‘value bargains’ and revisiting a screen that identifies companies trading at less than book value. Importantly, this screen attempts