38 shares have published annual reports and passed Richard’s minimum quality filter. 19 of them score less than three strikes. As he wades through these promising shares, Alfa Financial Software catches his eye.

5 Strikes

Of the 38 shares to have passed my minimum quality filter, 19 score less than three strikes. The flood of annual reports for companies that have financial year ends that coincide with the calendar year end is in full flow.

| Name | TIDM | Prev AR | Strikes | # Strikes |

|---|---|---|---|---|

| MGAM | Morgan Advanced Materials | 26/3/26 | – Holdings ? CROCI – Debt – Growth ? ROCE | 4 |

| TRB | Tribal | 26/3/26 | ? Acquisitions – CROCI – Growth ? ROCE | 3 |

| DRX | Drax | 25/3/26 | – Holdings – Debt – Growth – ROCE | 4 |

| FORT | Forterra | 25/3/26 | – Holdings – CROCI – Growth – ROCE | 4 |

| LUCE | Luceco | 25/3/26 | ? Acquisitions – Debt ? Growth ? ROCE | 2 |

| QTX | Quartix | 25/3/26 | ? ROCE | 0 |

| RKT | Reckitt Benckiser | 25/3/26 | – Holdings – Debt ? Growth ? ROCE | 3 |

| ALFA | Alfa Financial Software | 24/3/26 | – Growth | 1 |

| BA. | BAE Systems | 24/3/26 | ? Holdings ? Acquisitions – Debt ? Growth | 2 |

| DOM | Domino’s Pizza | 24/3/26 | – Holdings – Debt ? Growth | 2 |

| GAMA | Gamma Communications | 24/3/26 | ? Acquisitions – Holdings | 1 |

| INCH | Inchcape | 24/3/26 | – Growth | 1 |

| JUP | Jupiter Fund Management | 24/3/26 | – Holdings – Growth ? ROCE – Shares | 4 |

| MPE | M.P. Evans | 24/3/26 | ? Acquisitions – CROCI – Growth – ROCE | 3 |

| MBH | Michelmersh Brick | 24/3/26 | – Holdings – Growth – ROCE | 3 |

| MNDI | Mondi | 24/3/26 | ? Holdings ? Acquisitions – CROCI – Debt – Growth ? ROCE – Shares | X |

| ITV | ITV | 23/3/26 | – Holdings – Debt – Growth | 3 |

| MEGP | Me Group | 23/3/26 | – Growth ? ROCE | 1 |

| RTC | RTC | 23/3/26 | – CROCI – Growth – ROCE | 3 |

| LSL | LSL Property Services | 20/3/26 | – Holdings – CROCI – Growth ? ROCE | 3 |

| TW. | Taylor Wimpey | 20/3/26 | – Holdings – Growth – ROCE ? Shares | 3 |

| JSG | Johnson Service | 19/3/26 | – Holdings – Debt | 2 |

| HIK | Hikma Pharmaceuticals | 18/3/26 | ? Acquisitions – Debt | 2 |

| NXQ | Nexteq | 18/3/26 | – CROCI – Growth – ROCE | 3 |

| SRP | Serco | 18/3/26 | – Holdings ? Acquisitions ? CROCI – Debt | 3 |

| YU. | Yu | 18/3/26 | – CROCI ? ROCE | 2 |

| BNZL | Bunzl | 17/3/26 | ? Holdings – Debt – Growth | 2 |

| MSLH | Marshalls | 16/3/26 | – Holdings ? CROCI ? Debt – Growth – ROCE – Shares | X |

| SN. | Smith & Nephew | 16/3/26 | – Holdings – Debt – ROCE | 3 |

| PSON | Pearson | 13/3/26 | – Holdings – Debt – Growth ? ROCE | 3 |

| SHEL | Shell | 12/3/26 | ? Holdings – Growth – ROCE | 3 |

| ULVR | Unilever | 12/3/26 | – Debt – Growth | 2 |

| FOUR | 4imprint | 11/3/26 | ? Holdings ? Growth | 0 |

| PRV | Porvair | 11/3/26 | ? Holdings | 0 |

| CTEC | ConvaTec | 10/3/26 | ? holdings – Debt ? Growth ? ROCE | 2 |

| MONY | Mony | 9/3/26 | – Holdings ? Growth | 2 |

| STEM | SThree | 9/3/26 | – Holdings – Growth | 2 |

| HWDN | Howden Joinery | 25/2/26 | ? Holdings | 0 |

| Click here for our 5 Strikes explainer | 30/03/2026 | |||

4Imprint, Bunzl, Howden Joinery, Quartix and Porvair are in the Share Sleuth portfolio I run for Interactive Investor, so I will explore them in more detail there.

The other 14 shares blighted by less than three strikes are candidates for research here on ShareScope. I am taking them one by one alphabetically. The first five are below (bad luck to Yu – it might be a month until I get round to sussing out your potential).

Put my arm right up behind my back until I squeal, and I might confess to being most attracted to Alfa Financial Software, because software companies are historically cheap, may not be doomed, and I feel that if I keep throwing myself at them I might find one I have the confidence to invest in.

Remember, judging by the numbers these have been strong businesses. I’m focusing on the wrinkles to judge whether I can get comfortable enough to invest.

4Imprint [? Holdings ? Growth]

4Imprint markets promotional goods that are imprinted with corporate logos and given away by companies and other organisations to customers and staff.

The company sits between importers and customisers of blank products like t-shirts, notebooks, and mugs, and their end-customers. It is a giant marketing and order processing machine that often does not even touch the product, which is typically drop-shipped.

Turnover contracted slightly in the year to December 2025, which outside the pandemic is a first in my memory. 4Imprint was a victim of tariffs and economic uncertainty associated with the Trump administration in the US, where it makes almost all of its sales.

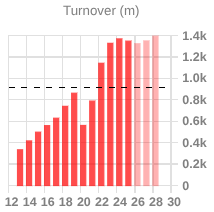

Alfa Financial Software [- Growth]

I do not know Alfa well, but perhaps I should. It gets a strike for growth because turnover fell in 2018 and 2019. The contraction merits attention, but was some time ago.

Alfa is a software platform for lessors and lenders of motor vehicles and equipment.

Software platforms are bewildering investments because of their specialised niches, complex accounting, and because investors fear they may become obsolete in the age of AI.

Unusually, in my experience, Alfa’s chief executive tackles the threat of AI in the annual report (see page 7). Most companies focus on the benefits (which Alfa does too), and relegate the threat to a vague statement in the Risk report.

In summary, he says:

- Alfa’s capabilities are too deep and leasing and lending is too complex and highly regulated to be replicated by generic AI: “standardisation, compliance, reliability, reversibility, integration, speed, authority models, security and specific industry practice matter much more than generic automation”.

- The software is embedded in complex business systems and although AI will increase the efficiency of implementation, it will not replace the process. Alfa believes this is an area in which it does better than competitors.

- Volume based pricing (as opposed to per-user pricing) means customer job losses will not impact Alfa.

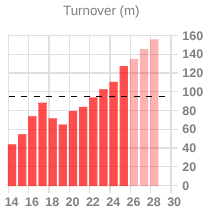

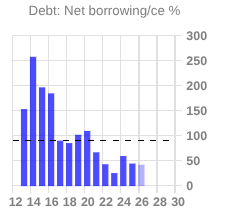

BAE [? Holdings ? Acquisitions – Debt ? Growth]

We all know BAE, and I doubt I know it any better than you – probably less well. It is a massive defence contractor, the UK’s biggest. It’s building frigates for the Norwegians:

Source: BAE annual report 2025

BAE gets a strike for debt, which is nearly 50% of capital employed. Debt has come down a lot over the years though, and is a little more than three years of free cash flow. Perhaps on closer inspection, it would not be a major concern.

Turnover at BAE contracted very slightly in 2018, which is almost ancient history. Although it has spent less on acquisitions than it has earned in free cash flow over the last eight years, it really splurged in 2020 and 2024.

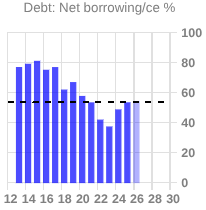

Bunzl [? Holdings – Debt – Growth]

Bunzl distributes essential consumables to all manner of organisations. Without realising it you have almost certainly eaten food wrapped in packaging supplied by Bunzl, used a bathroom equipped with toilet paper it supplied, or been dressed in hospital with a bandage from Bunzl.

Like BAE, its level of debt has fallen to about 50% of capital employed in recent years, about three times free cash flow – not an alarming level, perhaps for a company with such stable returns.

Like 4Imprint, Bunzl contracted slightly in the year to December 2025. It too has experienced headwinds, self inflicted, and due to tariffs and uncertainty in North America where it earned a slim majority of turnover.

ConvaTec [? holdings – Debt ? Growth ? ROCE]

ConvaTec is yet another business that earns most of its turnover in North America. It scrapes into my research list because two of its sins, sub-inflationary growth and low Returns on Capital, appear to be in the past. The numbers have improved this decade.

Also, ConvaTec supplies medical products like Advanced Medical Solutions (AMS), a share I own. There may be lessons to be learned about the industry from studying ConvaTec.

ConvaTec specialises in chronic conditions. It professes to be “forever caring”. The first page of its annual report contains a homage to its former chief executive who died last year. Karim Bitar led the company’s turnaround and transformation after his appointment in 2019.

It may say something about ConvaTec’s culture that his successor was an internal appointment:

Source: ConvaTec annual report 2025

Healthcare product companies are easy to like. Dressings and catheters and so on prevent infection, speed up healing, and help us live with unpleasant conditions. Commercially they are attractive too, because there is a technical element which enables manufacturers to differentiate their products, and they are consumables, generating repeat business.

But I’ve learned by holding AMS shares about the buying power of their biggest customers. This is revealed in ConvaTec’s annual report, which tells of a decision by the Centers for Medicare & Medicaid Services (CMS) in October 2025 to lower their payment rate for skin substitutes. CMS provides healthcare to 160 Americans.

The decision impacts one of ConvaTec’s fast growing products: InnovaMatrix, which was launched in the US in 2022. InnovaMatrix contributed 1.2% to turnover growth in 2023 and 1.1% to turnover growth in 2024, but reduced growth by 1.6% in 2025:

Source: ConvaTec annual report 2025

In 2026, ConvaTec anticipates $20 million of turnover from InnovaMatrix, compared to $69 million in 2025. This contraction will reduce turnover growth by 2% to 3%-5% in 2026, the company estimates.

Barring further disruption, I imagine InnovaMatrix should start contributing to growth again in 2027. The company says as well as clinical benefits, it is cheaper to manufacture than rival products.

It is not so much the impact of this particular decision that worries me, but the potential for similar events. The procurement arms of health authorities can decide which products vast numbers of hospitals use and how much they pay for them, complicating the picture.

Richard Beddard

Contact Richard Beddard by email: richard@beddard.net, web: beddard.net

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.