Marketing specialist Brave Bison undertook five acquisitions last year and recently purchased 28% of System1. Maynard Paton wonders if the acquisitions are creating value and whether he should join System1’s founder as a Brave Bison.

Oh dear. This ShareScope report has not turned out as I first hoped.

I had wondered whether Brave Bison — an £83 million “next-generation marketing and technology partner for global brands” — might have been a dynamic small-cap suitable for my portfolio.

You see, Bison suddenly loomed into view the other week after acquiring a 28% stake in System1 — an advert-testing business in which I am a shareholder — through a somewhat remarkable transaction.

System1’s founder John Kearon exchanged his entire System1 shareholding for Bison shares worth £7 million, and effectively told the market Bison had become a better investment than his old company.

I therefore asked myself whether I should follow Mr Kearon and switch from System1 into Brave Bison as well.

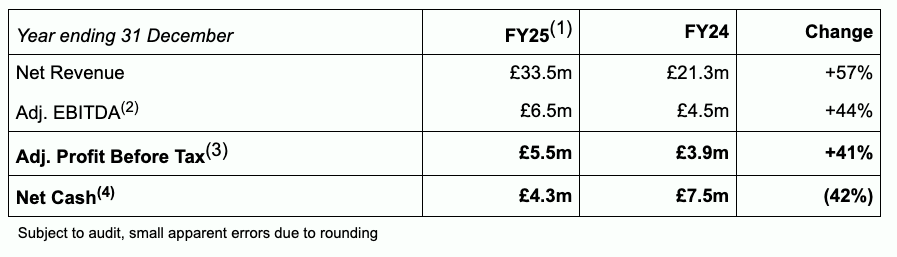

Indeed, Bison — unlike System1 — appears to be performing very well at present. The group’s January update confirmed net revenue, adjusted Ebitda and net cash had all finished 2025 “ahead of consensus expectations“.

But after delving into Bison’s history, I just could not get comfortable with what has been a very hectic acquisition strategy. Simply put, I don’t foresee Bison delivering the progress necessary to re-rate its shares to a premium valuation.

Let’s take a closer look.

Introducing Brave Bison

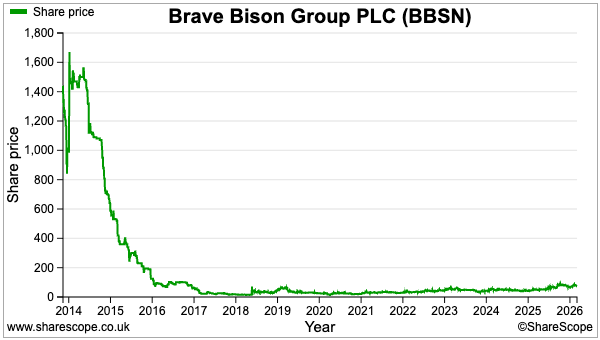

Bison’s story started during 2011 when the company began as a video-syndication specialist called Rightster.

Clients uploaded their videos to Rightster, had them distributed around the internet and in return paid a proportion of the advertising revenue the videos earned.

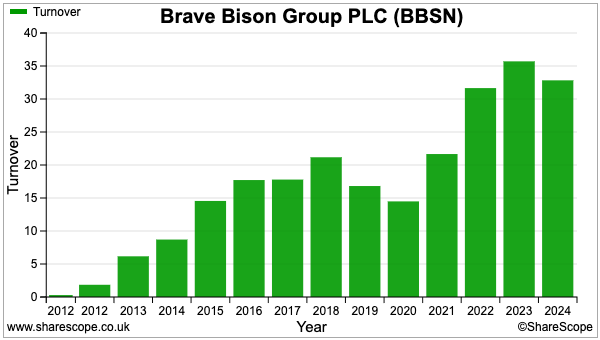

Rightster joined AIM during 2013 at the equivalent of £12 a share and the chart below shows the early business did not work:

Losses quickly surpassed £12 million…

…and soon prompted a strategic review, fresh leadership and a £10 million rescue fundraise.

By 2019 the group was on its fifth chief executive, the third of whom renamed Rightster as Brave Bison. According to the chief exec at the time:

“Brave Bison embodies the spirit and values, the attitude and energy, necessary for our company’s essential next chapter.”

Another board refresh was undertaken during 2020 after Bison had become the “biggest Facebook publisher globally based on views“… only for Facebook to change its algorithms and “demonetise” many of Bison’s popular pages.

Backed by a 27% family shareholding, Oliver Green became Bison’s executive chairman during the 2020 refresh. Mr Green then employed acquisitions to reduce the group’s dependence on advertising agreements.

Two major purchases were:

- Greenlight, a “digital advertising and technology company” acquired during 2021 for approximately £8 million, and;

- Social Chain, one of “the UK’s leading social media and influencer marketing agencies“, acquired during 2023 for an initial £5 million.

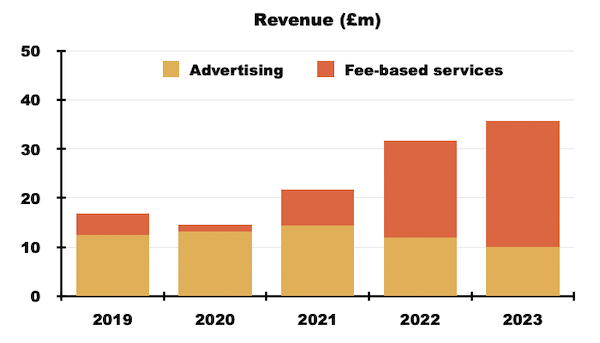

By 2023, fee-based income supported more than 70% of revenue…

…and fee-based activities included performance marketing, influencer marketing, SEO marketing as well as building e-commerce websites.

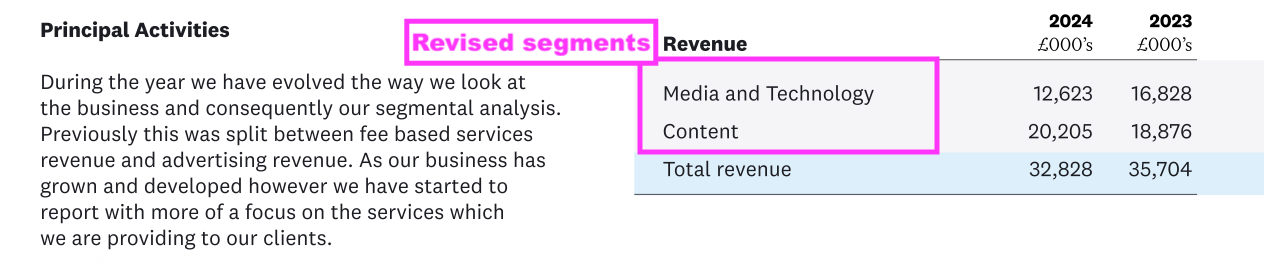

Bison decided to change its segmental reporting for 2024 and no longer discloses income from advertising agreements:

But Companies House suggests 2024 advertising income from YouTube, Facebook and similar declined 13% to £9.6 million despite monthly views increasing by 100 million to 1.5 billion.

Lower advertising income meant total 2024 revenue declined 8% to £33 million. Bison also admitted it had “mothballed” its US operations while clients had reduced e-commerce website expenditure due to “macroeconomic factors“.

Have the early acquisitions worked out?

Weaker ad income, the US withdrawal and an adverse economy probably explain why buying Greenlight and Social Chain may not have worked out quite as Bison had expected.

First, consider Bison’s annual revenue was £14.5 million for 2020.

Second, consider Greenlight’s trailing revenue was £14.3 million at the time of its 2021 purchase.

And third, consider Social Chain’s trailing revenue was £13.8 million at the time of its 2023 purchase.

Add the £14.5 million, £14.3 million and £13.8 million together, and Bison’s revenue ought to have become £42 million.

And yet revenue for 2024 — the first year when both Greenlight and Social Chain made full twelve-month contributions — was only £33 million:

Bison was certainly anticipating revenue to surpass £40 million — the company said as much at the time of the 2023 Social Chain purchase:

“On a pro-forma basis, the [Social Chain] Acquisition is expected to increase Brave Bison’s revenues from social media advertising seven-fold to £15 million, and the consolidated businesses (the “Enlarged Brave Bison”) is expected to generate total revenues in excess of £40 million for the financial year ending 31 December 2023.”

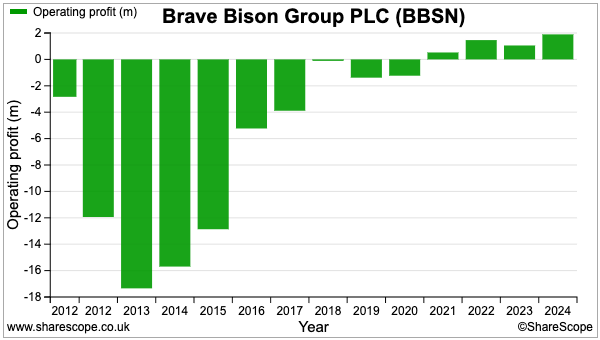

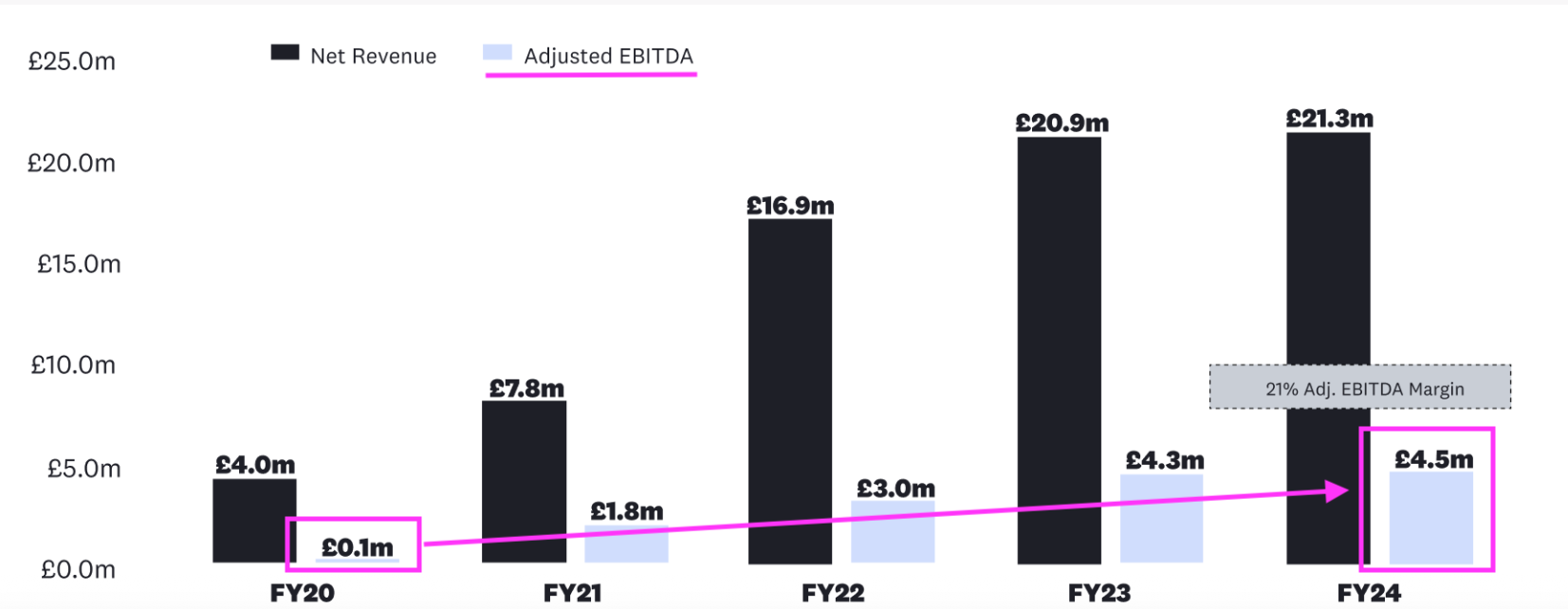

While some sales have vanished during recent years, extra profit — at least in the form of adjusted Ebitda — has in fact materialised. Bison’s 2024 results presentation showcased how adjusted Ebitda has advanced from £0.1 million to £4.5 million:

Given 2024 revenue was way below the previously expected £40 million, I surmise Bison’s 2020-2024 adjusted Ebitda progress was due entirely to cost savings. Bison says it integrates acquisitions by operating “centralised” IT, HR and finance functions.

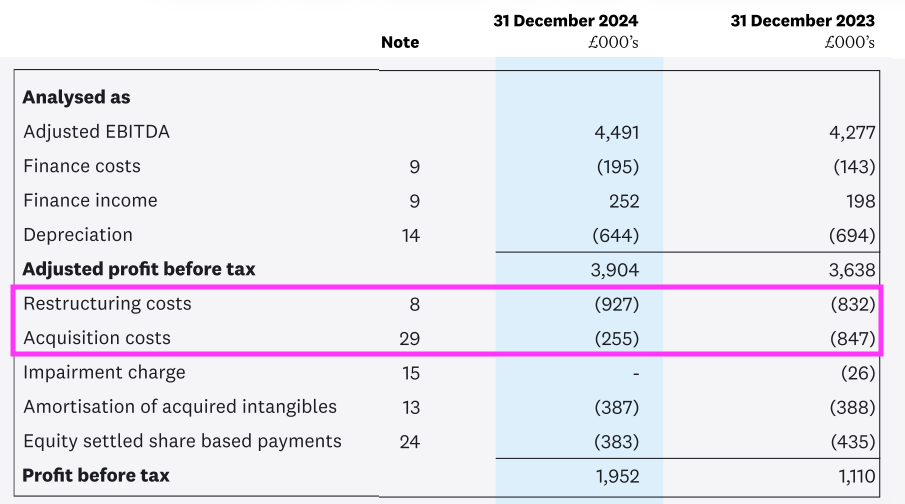

Be aware that Bison’s adjusted Ebitda is, er, adjusted… and excludes restructuring and acquisition costs:

Between 2020 and 2024, aggregate restructuring and acquisition costs amounted to £4.6 million — a significant sum given aggregate adjusted Ebitda during the same five years came to £13.7 million.

2025 acquisitions and System1 investment

Bison undertook no acquisitions during 2024 but restarted during 2025. No less than five transactions were completed last year at a total initial cost of approximately £28 million:

- Engage Digital Parters, a “global sports-marketing company” with revenue of £6.9 million;

- Builtvisible, a “leading performance-marketing agency” with revenue of £4.1 million;

- The Fifth, a “market leader in the influencer-marketing and creator economy“, with revenue of £6.2 million;

- MiniMBA, a “marketing and skills training platform” with gross profit of £11 million, and;

- MTM, a “strategy and insights consultancy” with gross profit of £8.3 million.

The pick of the 2025 deals was undoubtedly MiniMBA. This marketing-training website was by far the most profitable of the five acquisitions; at the time of purchase, MiniMBA’s expected gross profit of £11 million was expected to lead to adjusted Ebitda of £3.6m.

Bison describes MiniMBA as a “highly scalable digital-learning product that benefits from repeatable, non-cyclical revenues and a fixed cost base with very low marginal costs to service additional customers.”

MiniMBA provides MBA-level courses priced at £1,949 + VAT for 6,000 or so marketing professionals every year. Courses are led by Mark Ritson, a prominent marketing commentator renowned for his colourful language:

The 2025 acquisitions were followed up the other week by that 28% System1 investment for nearly £9 million.

Bison suggested its MiniMBA subsidiary would help sell System1’s services:

“System1’s evidence-based principles of marketing effectiveness align directly with the marketing science foundations taught through the MiniMBA and delivered through Brave Bison’s agency services, as is evidenced by a significant overlap across our existing customer bases.”

MiniMBA’s Mr Ritson has certainly been a System1 fan. He has undertaken many podcasts for System1, and System1’s H1 2022 presentation even included a testimonial from the MiniMBA tutor:

Bison’s System1 investment was particularly remarkable because the deal witnessed John Kearon, System1’s founder:

- Swap his entire 23%/£7 million System1 shareholding for new Bison shares, and;

- Abruptly leave System1’s board.

Despite establishing System1 and then serving as a director for 25 years, Mr Kearon was not ‘thanked‘ via the RNS by his former company. I can only speculate he was effectively ousted by the rest of the board.

I recall MiniMBA’s Mr Ritson saying three years ago that “trying to oust the founder” of a business was “never a good idea“:

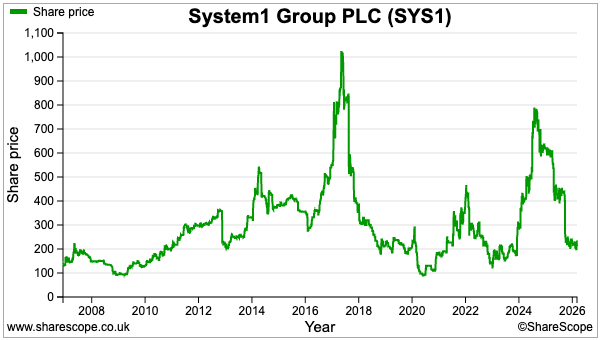

That said, System1’s share price has (aside from a few spikes) broadly gone sideways for the last two decades. Over time I have suspected System1’s founder had actually held his company back:

Bison’s System1 investment was conducted at an average 242p.

Rejected approaches and extra shares

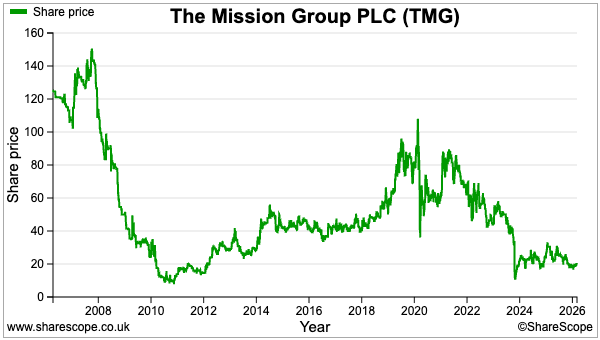

System1 was Bison’s third attempt of completing a quoted-company investment. The group has previously made overtures to Mission Group and M&C Saatchi.

Bison approached Mission with a proposed 29p per share offer that valued the advertising agency at £27 million. Despite lifting the proposal to 35p per share — almost double the 18p the shares had traded at before the approach — Mission shareholders rejected Bison’s advances.

Bison was then rebuffed by M&C after submitting a possible £50 million bid for M&C’s performance-marketing division.

Recent board changes at M&C — the chief executive will soon leave and a major shareholder has become a non-executive — probably preclude Bison from pursuing M&C any further.

But Mission could re-appear in Bison’s sights; Mission’s shares are now back at 19p following a January profit warning:

Acquiring Mission or M&C should have at least doubled the size of Bison, and funding would have been supported by issuing extra shares…

…and Bison is certainly not afraid of issuing extra shares.

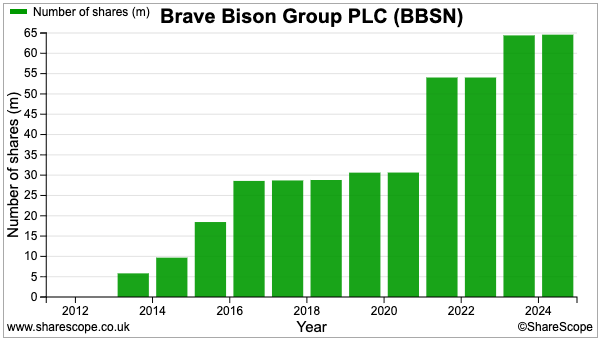

Those Greenlight and Social Chain purchases took the share count from 30 million to 65 million…

…while those five acquisitions of 2025, the System1 investment plus various option exercises have since increased the share count by 74% to 112 million.

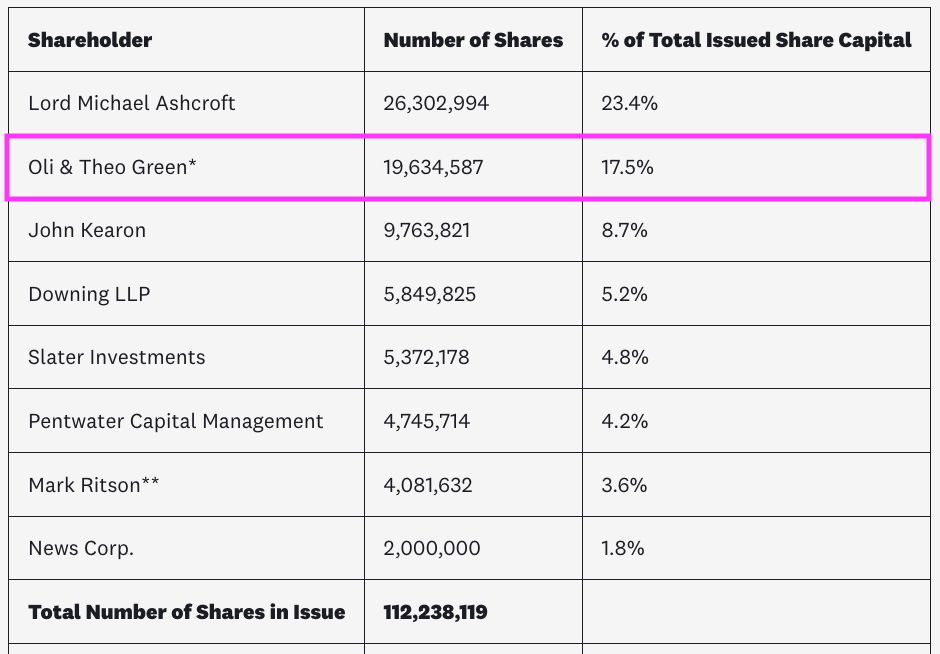

Option exercises have helped the aforementioned executive chairman, Oliver Green, and his brother, Theodore Green (a fellow Bison executive), remain sizeable shareholders. The Green brothers currently enjoy a combined 17% stake worth more than £14 million:

The Green brothers are sons of Michael Green, the broadcasting entrepreneur who floated Carlton Communications that would, after some notable acquisitions, become one half of ITV. Media deal-making therefore runs deep within the Green family:

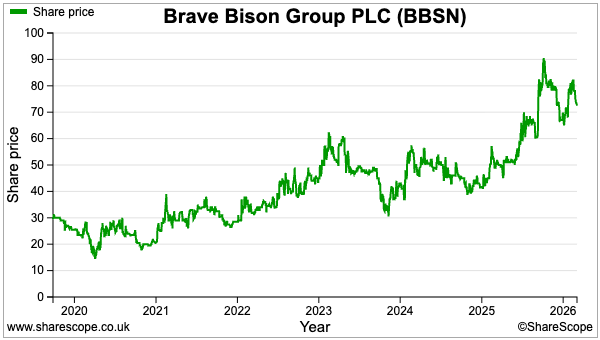

Bison’s expansion and greater adjusted Ebitda have seen the shares rally almost three-fold from 26p since Oliver Green took executive control:

But not every Bison shareholder is 100% happy.

Businessman Lord (Michael) Ashcroft owns 23% and requisitioned a general meeting last year to appoint a new non-executive who would “strengthen the corporate governance of the Company, add significant strategic and operational capability as the Company scales to meet its ambitious targets, and promote long term value for all shareholders.”

Although the Green brothers and other shareholders outvoted Lord Ashcroft, perhaps Lord Ashcroft senses Bison’s breakneck acquisition activity needs to be reigned in. He, too, may have realised Greenlight and Social Chain did not take the group past revenue of £40 million.

Valuation and verdict

A trading statement during January said net revenue (equivalent to gross profit), adjusted Ebitda and net cash would all be “ahead of consensus expectations“:

The statement added Bison was “comfortable” with 2026 forecasts of £45 million gross profit and £9.4 million adjusted Ebitda.

Mind you, a £9.4 million adjusted Ebitda should be the very minimum Bison reports for next year.

After all, adjusted Ebitda was £4.5 million for 2024 and, when added to MiniMBA’s £3.6 million adjusted Ebitda and MTM’s £1.3 million adjusted Ebitda, gives exactly £9.4 million…

..before cost savings, synergies and any contributions from the other three 2025 acquisitions.

Brokers translate adjusted Ebitda of £9.4 million into earnings of 6.6p per share…

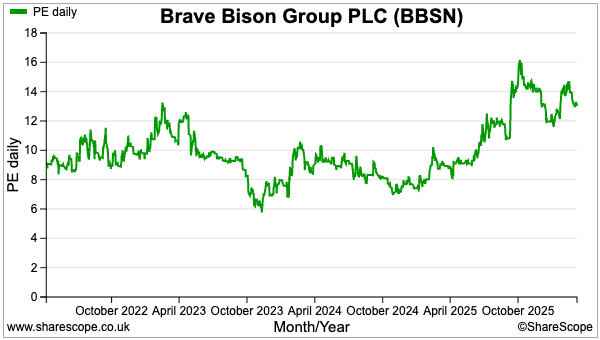

…which support a P/E of approximately 11 with the price at 74p. Bison’s shares have historically traded on a modest trailing multiple…

…as the market awaits proof the acquisition strategy goes beyond cost cutting and one day delivers the revenue equivalent of 2 + 2 = 5.

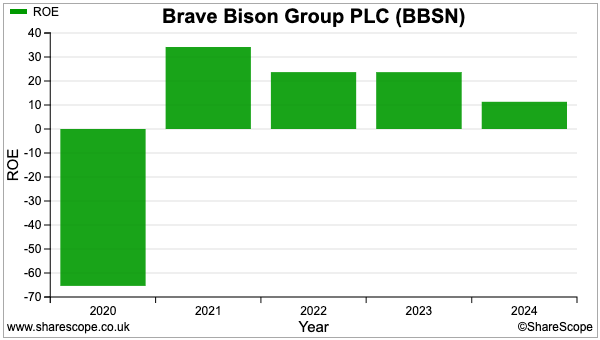

ShareScope’s calculations do not reveal encouraging post-2020 progress, with return on equity now standing at an unexceptional 11%…

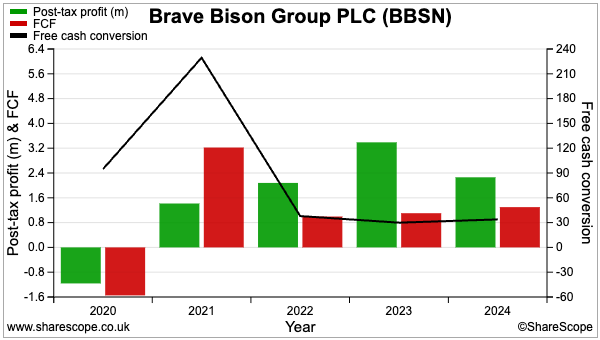

…cash conversion at a lowly 30%…

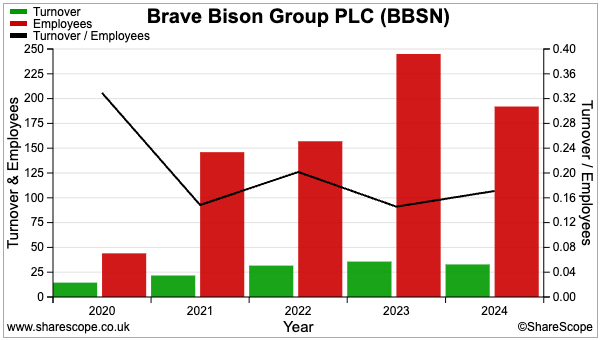

…and revenue per employee not displaying any tangible improvements:

Perhaps Bison’s 2025 results — due very soon — and its 2026 numbers in particular will begin to showcase the financial credibility of the enlarged group.

MiniMBA certainly has potential to advance the bull case; the ‘scalable’ nature of MiniMBA is underpinned in particular by its revenue topping a mighty £500k per employee. Mr Ritson could even revive the fortunes of System1 as well.

For now though, Bison offers no obvious sign of organic revenue growth while shareholder value to date has generally relied upon issuing shares to buy private companies at lowly multiples and then cutting central costs. The business progress to date just does not seem deserving of a premium rating.

And as I have found to my cost with System1, you do have various inherent risks with companies involved with marketing:

- Employee talent can always leave to start their own business;

- Client budgets always seem extremely sensitive to economic events;

- Directors with gifted advertising skills can present very persuasive investment ‘stories’, and;

- ‘Creative’ activities may incur greater disruption from AI and other technologies.

Suffice to say, I will not be following Mr Kearon from System1 into Brave Bison. If Mr Ritson can work wonders with System1 through MiniMBA, then I might as well stay in System1.

But whether I should stay in System1 is a different matter entirely. I get the feeling many other shares — or maybe even cash — could over time outperform both Bison and System1 from here.

Until next time, I wish you safe and healthy investing with ShareScope.

Maynard Paton

Disclosure: Maynard owns shares in System1 but does not own shares in Brave Bison.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.