With no new companies making it past his 5 Strikes filter, Richard examines transport software house and consultancy Tracsis’ rise and fall. To rise again, he thinks it must navigate a strategic minefield.

5 Strikes

Since my last update, three big and ugly looking companies have published annual reports and passed my minimum quality filter. Having scrutinised their financial track records, none appeal. All received more than two strikes.

| Name | TIDM | Prev AR | Strikes | # Strikes |

|---|---|---|---|---|

| British American Tobacco | BATS | 13/2/26 | – Holdings – Debt – Growth – ROCE | 4 |

| AstraZeneca | AZN | 10/2/26 | ? Holdings ? Acquisitions – Debt ? Growth – ROCE – Shares | X |

| BP | BP. | 10/2/26 | – Holdings – Growth – ROCE | 3 |

| Click here for our 5 Strikes explainer | 19/02/2026 | |||

Although a few companies with December year ends have published annual reports, the winter lull in reporting continues. Things will pick up in March.

Today, I’m taking a look at Tracsis (TRCS), which published its annual report in December and scraped through 5 Strikes. I awarded the business two strikes, while noting that turnover growth has also been questionable.

Tracsis [- Holdings – ROCE ? Growth]

Tracsis is not a big company. In the year to July 2025 its turnover was £82 million. But it is quite difficult to describe. This may belie complexity and strategic incoherence.

The company’s origins are in railway scheduling software, which is still a component of its Rail division. Most of the turnover in this division is from software, which also includes software that, along with hardware dataloggers, remotely monitors the condition of points, level crossings, signals and other railway infrastructure, and powers “tap and pay” style ticketing.

The other division is a group of consultancies that have expertise in data, analysis, geographic information systems, and event traffic management. It’s called Data, Analytics, Consultancy & Events, but for brevity I’m calling it Data etc.

These capabilities are applicable to transport markets generally and other markets, like agriculture. The division is less profitable and its performance is more lumpy, as demonstrated by the company’s segmental reports.

| Rail Technology and Services | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Turnover | 29,935 | 37,862 | 37,608 | 37,945 |

| Adjusted EBITA | 9,032 | 9,460 | 8,818 | 8,686 |

| Adjusted EBITA margin | 30% | 25% | 23% | 23% |

| Source: Figures derived from Tracsis annual reports | ||||

The Rail division earns a very healthy profit (EBITA) margin, although it has declined since 2022. EBITA is Earnings Before Interest, Tax, and Amortisation. Turnover growth has also stalled since 2023, so profit has contracted slightly.

I use EBITA to measure the profit generated by a businesses’ operations because almost all of the amortisation at Tracsis relates to acquired intangible assets. These costs do not reflect the ongoing investment in Tracsis’ businesses, which is expensed as it is incurred, but the historical cost of buying other companies – costs which have already been paid for.

| Data, Analytics, Consultancy & Events | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Data, Analytics, Consultancy & Events | 38,788 | 44,161 | 43,414 | 43,945 |

| Adjusted EBITA | 3,362 | 4,382 | 1,570 | 1,400 |

| Adjusted EBITA margin | 9% | 10% | 4% | 3% |

| Source: Figures derived from Tracsis annual reports | ||||

The Data etc. division earned a much lower profit margin even at its recent peak in 2023 (10% compared to 25% in Rail), and the recent squeeze on profitability has been much greater. By 2025, adjusted profit margin had fallen to 3%, compared to 23% in Rail. In Data etc. too, revenue growth has flatlined.

While the direction of travel has not been encouraging, it is a good sign that Tracsis provides the numbers that allow us to look under the bonnet in such detail.

The numbers are flattered by significant adjustments, one-off costs Tracsis has added back to give a better impression of underlying profitability and one-off gains the company has deducted. Over the last four years, net of gains the company has added £3.7 million of costs back to the Rail division’s profit, about 10% of cumulative adjusted EBITA:

| Rail Technology and Services | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Exceptional items – net | 444 | 1,816 | 1,474 | |

| Source: Tracsis annual reports | ||||

Most of these costs relate to a restructuring programme, aimed at improving profitability by making Tracsis more efficient.

The company has integrated its businesses so they use the same systems and their products are developed on a common software platform. This has resulted in redundancies, legal fees and other costs. It says this process was completed in 2025.

The absolute cost of restructuring Rail was greater than restructuring Data etc. but proportionally restructuring had a bigger impact on profit in the Data etc. division. There, £1.6million of net costs have been added back over the last four years, comprising nearly 16% of adjusted EBITA.

| Data, Analytics, Consultancy & Events | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Exceptional items – net | 176 | 1,187 | 298 | |

| Source: Tracsis annual reports | ||||

There are a number of external reasons turnover growth has stalled at Tracsis and profit has contracted. Much of Tracsis’ turnover is ultimately dependent on funding from the Government, which is constrained. The rail business has been disrupted as Network Rail moved from one five-year funding period to another, and funding continues to be uncertain. Labour costs have risen. In common with other software companies the Rail business is transitioning to selling software as a service, which replaces windfall turnover from perpetual licenses with staged payments from subscriptions.

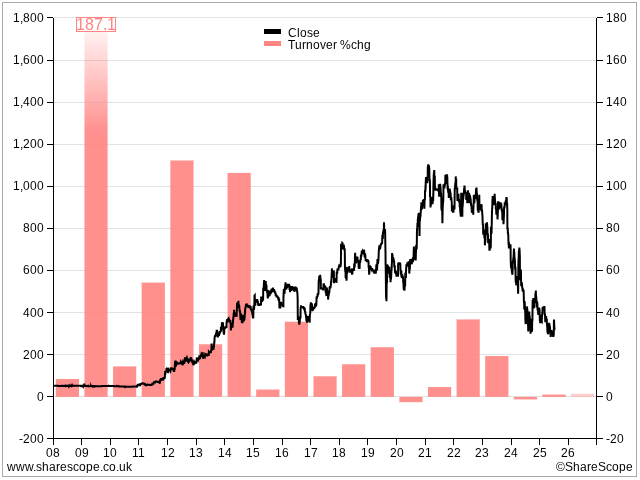

However, Tracsis’ reversal of fortune was also self-inflicted. It had many disparate businesses to integrate in 2022 because it had acquired them over the fifteen year period since 2007, when it floated on the stockmarket. In most of those years, Tracsis grew turnover and profit handsomely and the share price responded:

By pausing acquisitions and restructuring to relieve the indigestion created by the companies it had already eaten, Tracsis believes it has created the conditions for a return to growth. It expects to grow organically, now its businesses are sharing costs and can develop products in a more coherent way, and also by acquiring more businesses.

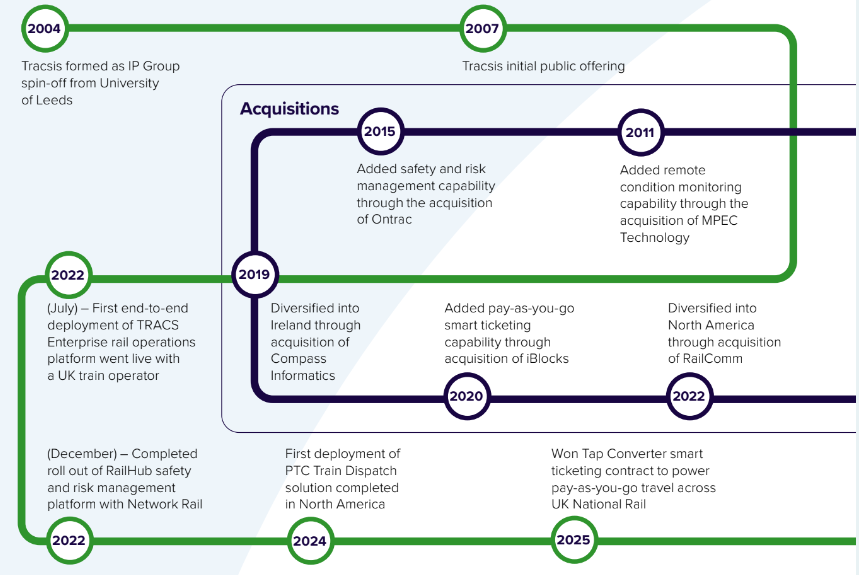

Growth is not a given. The annual report includes a rail network style corporate history that vastly simplifies its acquisition history:

Source: Tracsis annual report 2025

These are highlights. By my count, Tracsis has bought 10 businesses for its Rail division and five for the Data etc. division since 2008. Spending on Rail has been much higher, representing about 80% of total acquisition spend of over £100 million.

Since Tracsis is planning to go back on the acquisition trail, we need to consider the impact that the cost of acquisitions might have on returns. We can do this by deducting the book (amortised) value of intangible assets from capital employed and adding the cost (unamortised) value, which is disclosed in the annual report.

This gives us a ROTIC (Return on Total Invested Capital) of 9%, which is borderline. It suggests that in aggregate Tracsis generated only adequate returns in 2025 once the purchase cost of the businesses it bought is included. In other words, it may have paid a very full price for them.

That wouldn’t matter if Tracsis could grow these businesses organically. But Tracsis’ taste for acquisitions leads me to think opportunities for organic growth are limited in the lucrative Rail business here in the British Isles. It may be faced with a choice between acquiring pricey Rail businesses or less profitable businesses in other transport related segments.

Tracsis’ other option is to enter overseas markets, which it achieved in 2022 with the acquisition of RailComm, now Tracsis’ North American arm. However RailComm is underperforming.

David Frost, Tracsis’ new chief executive, is leading the company through this strategic minefield. He joined the business in July last year, and the first results achieved under his leadership will be for the half year to January 2026. A trading update may be imminent, and the results are anticipated in April .

PS. I recommend Neil’s comment on my article about SaaSy Cerillion. It made me laugh out loud.

Richard Beddard

Contact Richard Beddard by email: richard@beddard.net, web: beddard.net

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.