Cerillion has a perfect track record selling software to a challenging sector. Goldplat knows how to profit consistently from miners in troubled economies. Renew has figured out how to make big returns from labour intensive infrastructure repair and maintenance. All pass the 5 Strikes test.

Unsurprisingly companies haven’t been busy churning out annual reports over the Christmas period.

5 Strikes

Of the seven that did report, only two scored less than three strikes and warrant further investigation.

|

Name |

TIDM |

Prev AR |

Holdings (%) |

Strikes |

# Strikes |

|---|---|---|---|---|---|

|

Catalyst Media |

CMX |

24/12/24 |

43.1 |

– CROCI – Growth – ROCE |

3 |

|

Premier Miton |

PMI |

24/12/24 |

3.1 |

– Growth – ROCE – Shares |

3 |

|

Future |

FUTR |

23/12/24 |

0.1 |

– Holdings ? Acquisitions – Growth ? ROCE – Shares |

4 |

|

Goldplat |

GDP |

23/12/24 |

29.7 |

– Growth ? ROCE |

1 |

|

NCC |

NCC |

23/12/24 |

0.4 |

– Holdings ? Acquisitions ? Growth – ROCE – Shares |

4 |

|

Renew Holdings |

RNWH |

23/12/24 |

0.7 |

? Holdings – Shares |

1 |

|

Oxford Metrics |

OMG |

20/12/24 |

0.8 |

– Holdings – CROCI – Growth – ROCE |

4 |

They are Renew Holdings (? Holdings – Shares) and Goldplat (- Growth ? ROCE).

Renew maintains and repairs our national infrastructure: railways, roads, water, electricity and nuclear power. If you’re thinking this sounds like low-margin labour intensive work, it is quite low margin and quite labour intensive.

But given the state of infrastructure in the UK there is plenty of work about, and Renew has found a way to profit consistently and handsomely from it. That’s not just the verdict of 5 Strikes, it was also my conclusion when I investigated the business more closely last March.

Since I will be updating that research shortly, I won’t dwell on Renew today. Its strikes are not particularly serious. It would be reassuring if the directors held more of the shares and I gave Renew a strike for the growth in its share count over the last eight years.

Most of the new shares were issued to fund an acquisition in 2018. Renew rarely spends more on acquisitions than it earns in free cash flow, but it did that year.

The second company to score less than three strikes was Goldplat (? CROCI – Growth ? ROCE), which puts me in a rather uncomfortable position.

Goldplat [- Growth ? ROCE]

When I noticed Goldplat was in the gold mining subsector, I panicked. I consider any investment that achieves less than 3 strikes worthy of further investigation but really? A miner?

I should have read ShareScope’s company profile more closely.

Goldplat produces gold and other materials by processing by-products of the mining industry rather than operating mines.

Mining is an industry I’ve never invested in. I assume the profits of mining companies depend on the price of the commodity they mine, which is beyond their control.

The fact that mines are a finite resource also bothers me. It means the long-term future of the business depends on the operator’s ability to find or acquire new mining rights.

Miners also have a reputation for despoiling the environment.

Maybe these undesirable attributes are not such a big concern for a company that provides a service to mining companies. Since Goldplat recovers materials from waste, perhaps it is part of the environmental solution.

As I take my first ginger steps into this unknown territory, these largely positive thoughts

are offset by negative ones.

Goldplat operates in South Africa and Ghana. They are hardly the most stable of economies, although both currently may be on the “up”. While Goldplat isn’t mining, its profits are still sensitive to the supply of waste material from mines. Volumes depend on mining activity, which is in turn dependent on commodity prices.

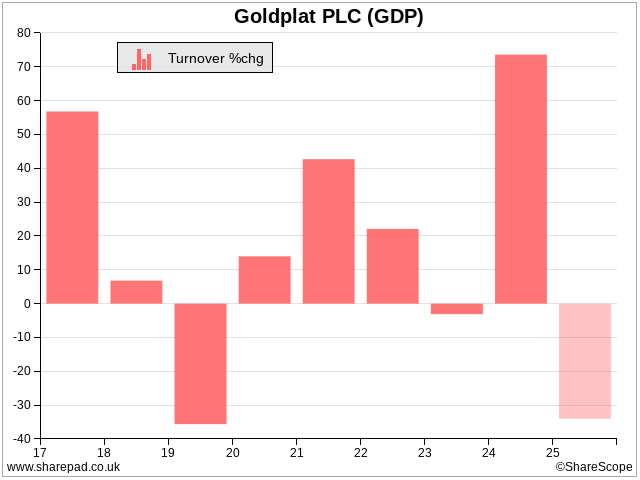

These reservations may be evident in the single full strike I gave Goldplat. It was for growth, which has been somewhat inconsistent:

There have been two down years in the last eight. Revenue is also expected to decline in 2025 after very strong growth in 2024.

The outlook statement in Goldplat’s annual report does not forecast revenue but acknowledges the business is cyclical and states that the South African gold industry is in slow long-term decline.

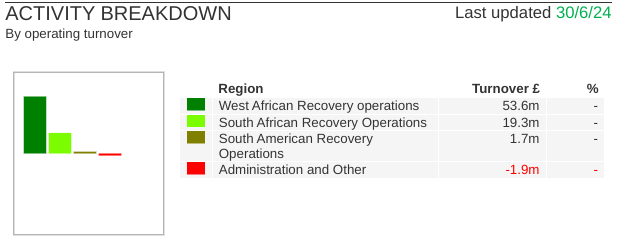

We can see from ShareScope’s activity report that South Africa is the smaller of its two main operations:

Over the medium to long term, the company intends to overcome this challenge through diversification: by expanding its nascent Brazilian operation and moving into other commodities.

The 2019 down year is also the reason I questioned profitability (ROCE). That year, though, when reported ROCE was below 8%, Goldplat’s profit from “recovery” operations, now its only business, was offset by losses from a Kenyan mining operation it is no longer involved in.

The decision to exit mining in Kenya may have been influenced by long-time shareholder Martin Ooi, who became a non-executive director around the time of the disposal. He owns 29% of the shares and his biography in the annual report states that he focuses on “capital allocation decisions and maximising the per-share intrinsic value of the company.”

If Goldplat feels like an edgy investment to you, it does to me too. But I think the business as it stands today is more reliable than it looks. I want to get to know it better, so it has joined my watch list.

Cerillion [0 Strikes]

Cerillion provides billing and customer relationship management (CRM) software, mostly to telecom companies. It flew through the five-strikes process last time I updated you. I gave the business no strikes, but had no space in that article to introduce the company. Today I am putting that right.

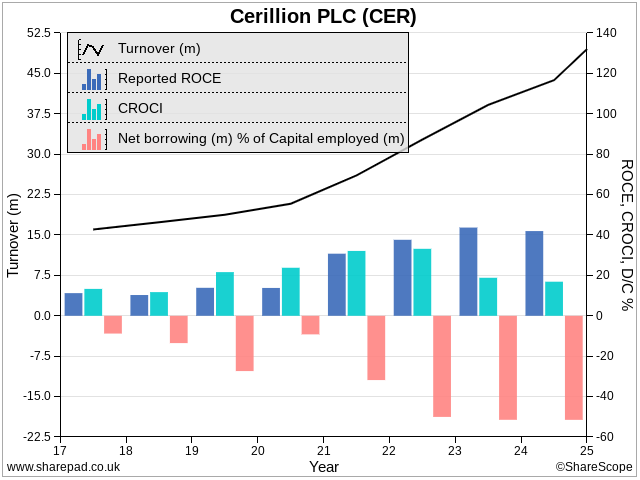

This chart shows four of the six key financial 5 Strikes criteria: Turnover, ROCE, CROCI and debt to capital, all of them well within the bounds I set. The other two are not significant. Acquisitions have been negligible and the company’s share count is static.

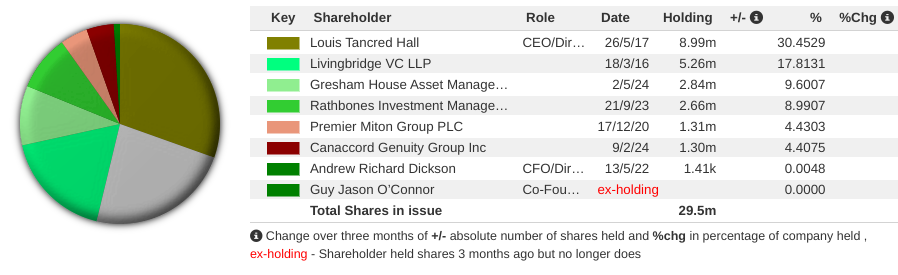

Rounding out the 5 Strikes criteria, founder and chief executive Louis Hall owns 30% of the shares:

Source: Sharescope

Hall led a management buyout from Logica in 1999.

Never satisfied until I have found things to worry about, I have skim-read the annual report looking for problems. Fortunately, the company is upfront about challenges, which is in itself a very good sign.

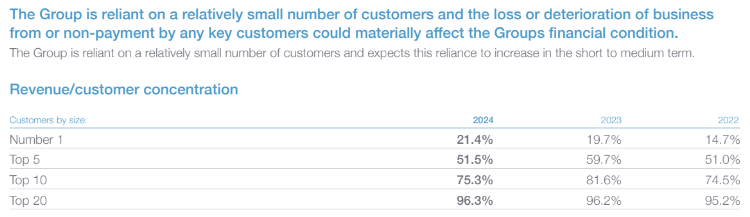

To invest, I would need to satisfy myself that Cerillion can continue to grow while its customers slug it out in a highly competitive industry (mobile and fixed-line telecoms). Their customers are switching to internet communications.

The telecoms industry is consolidating, which could reduce Carillion’s hitherto very sticky customer base. Since that is already highly concentrated as the table below shows, there is quite a bit to think about after all:

Source: Cerillion Annual Report 2024

~

Richard Beddard

Contact Richard Beddard by email: richard@beddard.net, Twitter: @RichardBeddard, web: beddard.net

Got some thoughts on this week’s article from Richard? Share these in the Sharescope chat. Login to Sharescope – click on the chat icon in the top right – select or search for a specific share.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.