Screening For My Next Quality Winner: Alfa Financial Software (LSE: ALFA)

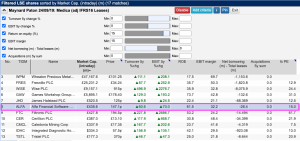

The lead executives at Alfa Financial Software were paid just £29k last year to match the London Living Wage. Maynard Paton links the commendable remuneration to the run of eleven special dividends declared by this high-margin, high-ROE business. Can you imagine company directors working for £14.80 an hour? If not, then say hello to Andrew