Tenpin bowling chains are like London buses. You wait around for years and then two of them list almost at the same time. Phil Oakley has already reviewed the UK’s biggest operator, Hollywood Bowl, but there’s more to be learned from the number two.

Private equity owners of companies tend to list them on the stock market at propitious times: when trading is brisk, prospects are good, and they are likely to get a good price for the business and a good return on their investment.

New listings and how to find them

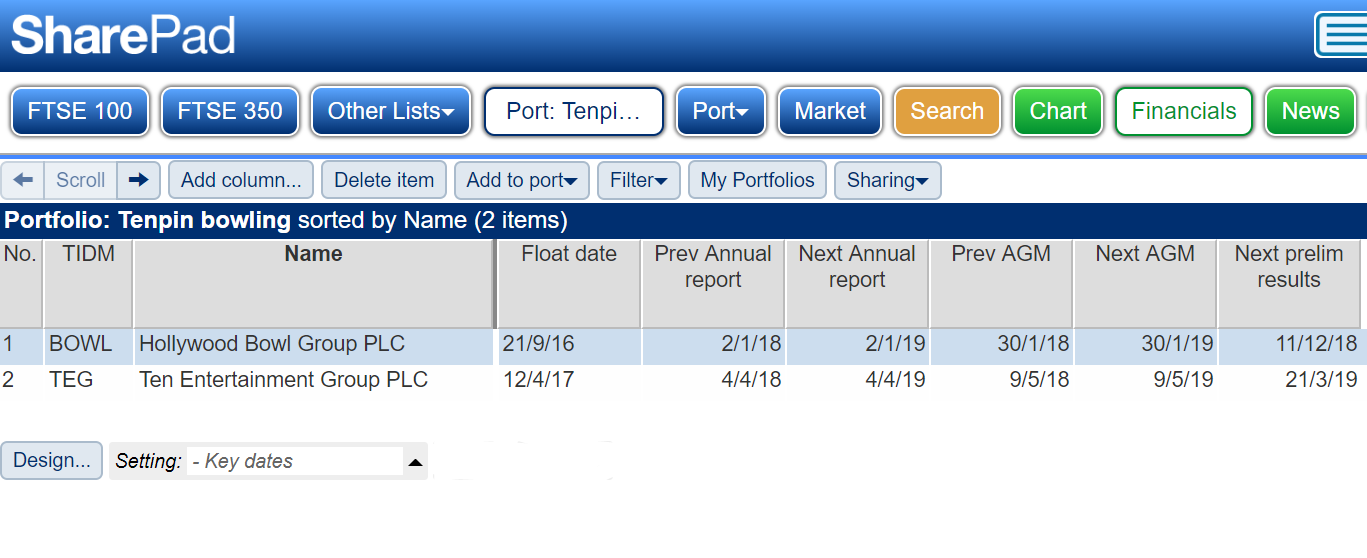

In SharePad, it’s easy to find out when a company listed, it’s in the Company tab of the green Financials view, or you can create a Table showing when all the shares you are interested in floated:

Here, I’ve added a Float date column to my ‘Key dates’ setting in the blue List view. To do this, click on Add column, type ‘float’ into the search box and select Company float date.

Hollywood Bowl listed in September 2016 and Ten Entertainment Group, parent of the Tenpin chain, listed in April 2017. I doubt it’s a coincidence. The fact that Britain’s two biggest bowling operators listed within about six months of each other suggests it’s a good time to be in the tenpin bowling business.

Bowling boom

Business is booming because people have been spending more money on going out and less on possessions, which is one of the reasons shops are struggling and leisure venues have been doing well. The boom in restaurants may have gone too far, leading to overcapacity and some closures, but despite four years of growth in the tenpin bowling industry there are still fewer bowling lanes in Britain now than there were in 2007. Sensing an opportunity to expand, the big operators are improving their customer service, sprucing up their brands, introducing new technology and opening new centres.

Hollywood Bowl is Britain’s biggest bowling brand; it has more centres, more lanes, and higher revenues than any other brand. According to Phil, it could well make a good investment. So why bother investigating Tenpin, the number two, when we can invest in the number one?

Two reasons: We may learn something about the number one by studying the number two, and the number two could be a better investment. It may be cheaper, more innovative or likely to grow faster.

Comparing companies #1 – the prospectus

Private companies publish far less information than public companies so they publish a prospectus to bring new investors up to speed when they float. These contain valuable industry information and the prospectuses of Tenpin and Hollywood Bowl show they have much in common.

They’re not even that different in size. Tenpin has 42 centres to Hollywood Bowl’s 59 (I’ve updated these figures to include new centres since the companies floated). Both companies favour high footfall locations co-located with cinemas and restaurants. They are both using technology to improve efficiency, from the way the bowling pins are set once they have been knocked over, to customer relationship management. Both say they put customers and staff first and are both are targeting the business of families, although Tenpin also targets groups of young adults who, it says, tend to use the centres at different times.

As a result, Tenpin operates a wider range of ancillary amusements from soft-play to pool tables, and a slightly lower proportion of its revenue is from bowling – just under half – compared to just over half at Hollywood Bowl. Both companies also earn revenue from food and drink.

Perhaps the biggest difference is how the companies plan to grow. Hollywood Bowl is opening new centres at a fairly pedestrian rate of two centres a year although it may also acquire them. Tenpin does not open new centres; it solely relies on acquisitions, which it subsequently “tenpinises”. Tenpin expects to acquire two to four centres a year and ultimately double in size. Acquiring larger multiples like Hollywood Bowl or number three, MFA Bowl, is out of the question. The Competition and Markets Authority wouldn’t allow it. The top three already operate nearly 40% of all bowling centres.

I don’t think the big brands are locked in particularly intense competition. They’re not generally located near each other and most of us probably go to our closest centre, whoever runs it. Competition is most likely to be a factor in acquiring centres, rather than operating them, and it’s possible all the big brands could prosper as the industry consolidates, so long as our propensity to bowl remains.

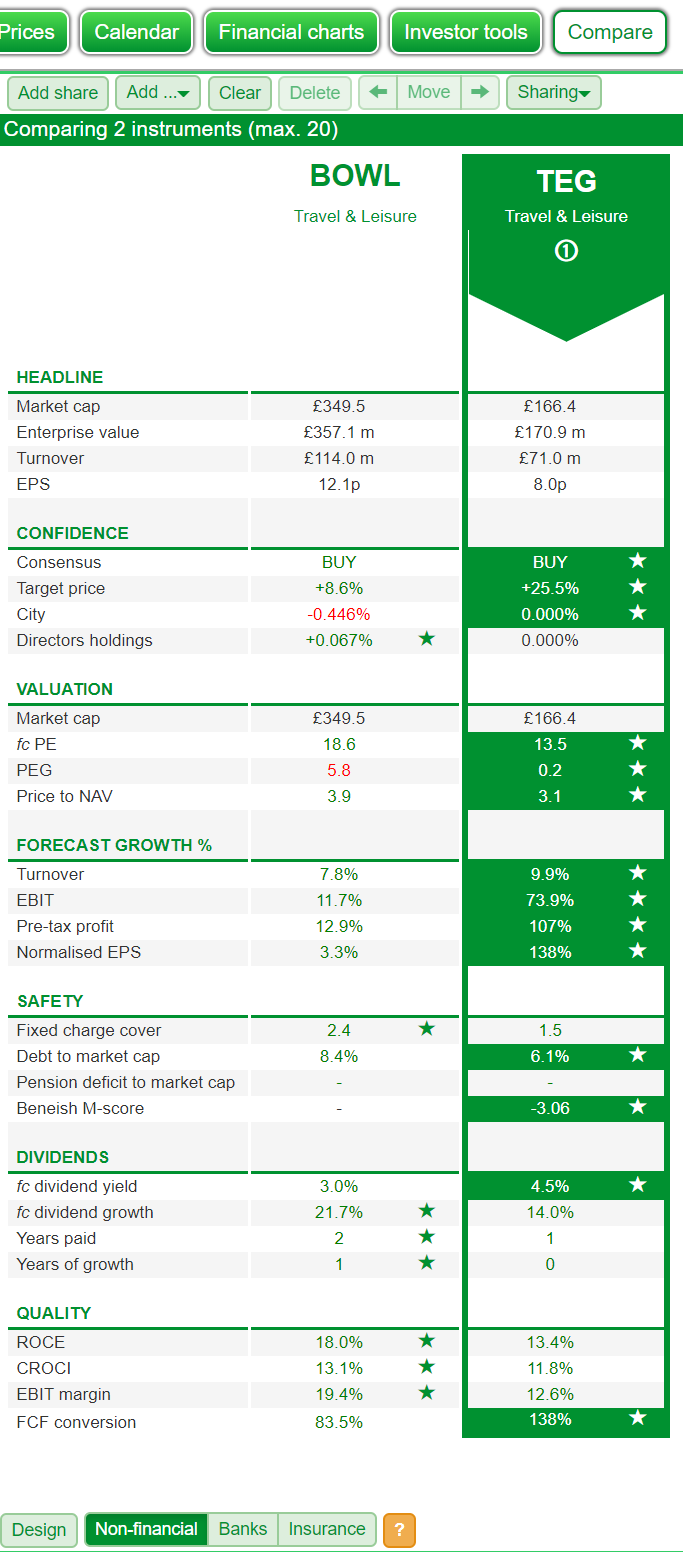

Comparing companies #2 – SharePad

One of the quickest ways to compare two companies in SharePad is to use the green Comparison view located on the far right of the screen. You can compare up to twenty companies using this view, though I’ve chosen just Hollywood Bowl (BOWL) and Tenpin (TEG). As usual in SharePad, you can change the criteria by clicking on the Design button at the bottom of the screen.

We need to be cautious about interpreting this table. Tenpin is highlighted because it has better stats based on a simple count of the default criteria SharePad uses to judge a firm. Some of these criteria may be more important than others, though.

Shares in Tenpin trade on a lower valuation than shares in Hollywood Bowl, and analysts expect Tenpin to grow much more quickly in the coming financial year. In terms of safety, though, honours are more evenly split and of the ratios included, I’d give fixed charge cover the highest weighting. Profit at Hollywood Bowl could fall much further before it struggles to pay rent and interest.

Hollywood Bowl is also more efficient at turning investment into profit. That’s what the ratios in the Quality section show. While it’s worth being in business for a 13% return on capital employed, Tenpin’s profitability in its most recent financial year, these are good times for the bowling industry. I prefer to invest in businesses that should earn a 10% return on capital employed even during bad times, for example in a recession, or, perhaps, if we return to buying more things than experiences. While Tenpin appears to be on a roll, its relatively low profitability increases the chances of disappointment.

But the stats may tell a different story. Tenpin scores best on the criteria that use analysts’ forecasts: growth, valuation (the PE is a forecast), and the PEG ratio are based on the firms’ forecast growth rate. Hollywood Bowl scores highly on figures the company has already achieved. If I were to make the comparison using historical valuation ratios, Hollywood Bowl would look cheaper too. But if Tenpin doubles its profit, it will look much stronger and more profitable, like Hollywood Bowl.

Meeting the forecasts requires a dramatic improvement but Hollywood Bowl has been through a similar transition in recent years. Given the similarities between them, Tenpin could just be a year or two behind as the two companies capitalise on a wave of popularity with a wave of investment.

As a safety-first investor my instinctive reaction is to abandon my newfound infatuation with tenpin bowling. I prefer to base my decisions on what I know rather than what other analysts believe, and on the long-term prospects of businesses rather than short-term forecasts.

Tenpin shares may look cheaper than Hollywood Bowl’s, but it’s also more speculative and my long-term vision is failing me. Though the tenpin bowling industry has been growing for the last four years, it seems to have been moribund before then.

Tenpin has a somewhat chequered history too. Trading as Essenden it could have gone bust in 2011 had it not negotiated a voluntary agreement with some of its creditors.

The awakening of tenpin bowling has been so sudden, I wonder if it could just as easily slip back into a coma.

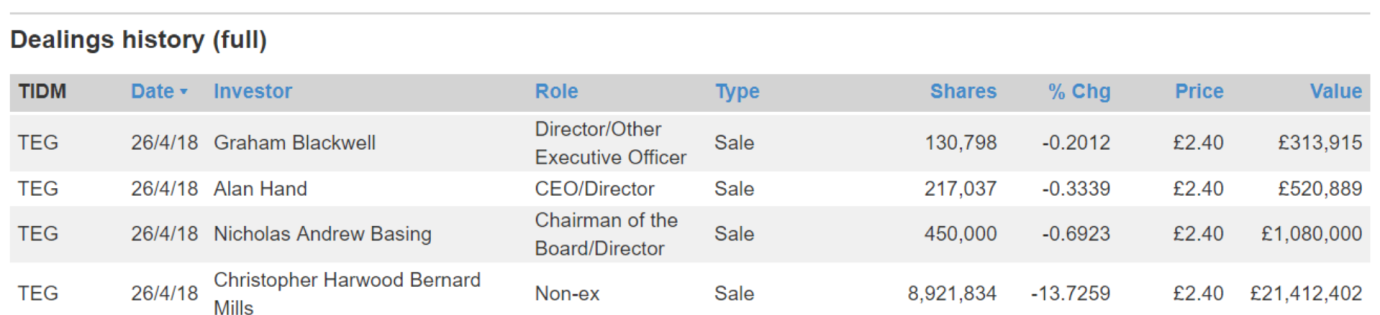

While I don’t like speculating about other people’s motives and they still own handsome stakes, large sales by Tenpin’s directors including its owner when it was a private company, Chris Mills, make me wonder about the board’s confidence in Tenpin’s prospects too.